–7.3

–9.1

–1.4

0.4

ADDITIONAL CASE STUDY

19–3 Structural and Cyclical Deficits

Deficits and surpluses arise naturally in an economy experiencing business–cycle fluctuations because of

the presence of automatic stabilizers. This suggests a decomposition of the overall budget deficit (or

surplus) into a cyclical deficit, because of automatic stabilizers, and a structural (or full–employment)

deficit, which may better reflect the overall stance of fiscal policy. That is, the structural deficit is a

of output, the cyclical balance also moved into a moderate surplus. But a structural deficit emerged once

again during the early and mid–2000s following tax cuts and increased spending associated with two wars.

The onset of the financial crisis and steep recession led to a sharp increase in the structural deficit as a

result of the stimulus program passed by Congress.

Table 1 shows the structural balances of seven countries in 2009 and again in 2013. All of these

France

–6.5

–3.4

Italy

–3.7

0.2

Britain

–10.1

–4.9

Canada

–3.5

–2.6

Source: Organization for Economic Cooperation and Development, Economic Outlook, 2014.

LECTURE SUPPLEMENT

19–4 Generational Accounting

Laurence Kotlikoff and others argue that the analysis of government budget deficits should be informed by

the insights of the life–cycle model (discussed in Chapter 16). From the point of view of an individual,

taxes and transfers in any given year are less important than the pattern of taxes and transfers over that

individual’s entire lifetime. Kotlikoff’s system of generational accounting takes this approach.1 The aim is

to calculate the net effect of lifetime taxes and transfers for a given cohort of people born at the same time.

Generational accounting often comes to very different conclusions than the officially measured

budget deficit about the effects of fiscal policy. For example, during the 1980s, many analysts viewed tax

cuts and associated deficits as a burden on young workers who would some day have to pay off the

LECTURE SUPPLEMENT

19–5 The Government Budget Constraint

To better understand the link between government debt and future taxes, it is useful to imagine that the

economy lasts for only two periods. Period one represents the present, period two the future. In period one,

the government collects taxes T1 and makes purchases G1; in period two, it collects taxes T2 and makes

purchases G2. Because the government can run a budget deficit or a budget surplus, taxes and purchases in

the first equation for D into the second equation to obtain

T2 = (1 + r) (G1 – T1) + G2.

This equation relates purchases in the two periods to taxes in the two periods. To make the equation easier

to interpret, we rearrange terms. After a little algebra, we obtain

This equation is the government budget constraint. It states that the present value of government purchases

period two. The consumer’s lifetime income is the same as before the change in fiscal policy. Therefore,

the consumer chooses the same level of consumption as she would have without the tax cut, which implies

that private saving rises by the amount of the tax cut. Hence, by combining the government budget

constraint and Irving Fisher’s model of intertemporal choice, we obtain the Ricardian result that a debt–

financed tax cut does not affect consumption.

468

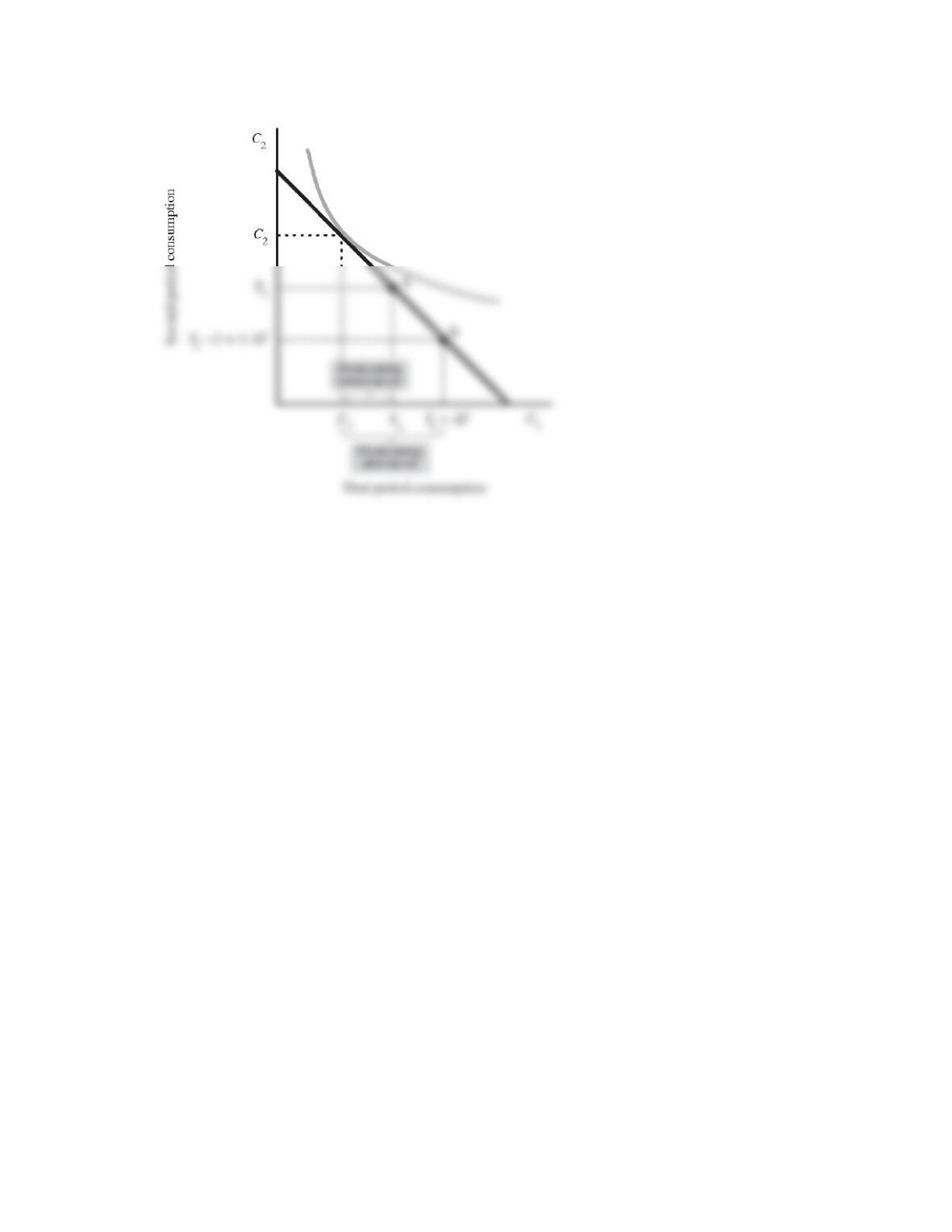

Figure 1 A Debt–Financed Tax Cut in the Fisher Diagram

469

LECTURE SUPPLEMENT

19–6 Borrowing Constraints Using the Fisher Diagram

Suppose a consumer faces two constraints: a budget constraint and a borrowing constraint (see Chapter 16

for more details). The budget constraint says that the present value of consumption must not exceed the

present value of income. The borrowing constraint says that first–period consumption must not exceed

Figure 1

ADDITIONAL CASE STUDY

19–7 Social Security Benefits and Ricardian Equivalence

David Wilcox’s work on consumers’ responses to changes in Social Security benefits (see Supplement 16–

5) provides a test of Ricardian equivalence.1 Recall that Ricardian equivalence suggests that the timing of

taxes is irrelevant to forward–looking, altruistic consumers. This result should hold equally for transfer

1989): 288–304. Wilcox’s study is discussed in more detail in Supplement 16–5, “Do Consumers Anticipate Changes in Social Security Benefits?”

471

ADVANCED TOPIC

19–8 Is Everything Neutral?

One of the most clever arguments against Ricardian equivalence is a reductio ad absurdum put forth by

Douglas Bernheim and Kyle Bagwell.1 They consider Robert Barro’s argument for intergenerational

altruism and point out that, in fact, we would not only expect to see dynasties that are linked, but we

should expect to see interconnected chains of individuals. The consequence is that everyone is ultimately

472

CASE STUDY EXTENSION

19–9 Does Altruism Matter?

Much of the debate over Ricardian equivalence considers the intergenerational altruism argument of

Robert Barro. Even if current deficits will ultimately be paid for by taxes on future generations, the effects

of these deficits may be limited by parents’ taking account of their children’s tax liabilities and leaving

larger bequests. James Poterba and Lawrence Summers suggest that this aspect of the debate may be

something of a red herring, at least for evaluating the effects of deficits on consumption and saving.1

Even though tax burdens may be shifted onto future generations so that the wealth of those currently

alive is increased by deficits, life–cycle consumers have a small marginal propensity to consume out of

wealth. Poterba and Summers calculated the size of this effect by considering the behavior of an economy

peopled by life–cycle consumers who work for 45 years and are retired for 10. They then considered the

effects of a $1 transfer to all living people, working or retired, financed by a government deficit (under an

assumption that, after some period of time, the government would then tax workers to pay the interest on

the debt).2

473

LECTURE SUPPLEMENT

19–10 Unpleasant Monetarist Arithmetic

Thomas Sargent and Neil Wallace emphasized the interdependence of monetary and fiscal policy that is

implied by the government budget constraints:

Dt = ∆Mt + ∆Bt;

Bt = Bt–1 + ∆Bt.

They note that there is a limit on the stock of (real, per–capita) debt that the private sector is willing to

hold. As a consequence, fiscal policy and monetary policy will not be independent in the long run.1

Suppose that the fiscal authorities establish a policy setting out all current and future deficits. Since

there is a limit to the amount of debt that the public will hold, it may eventually not be possible to finance

deficits with new bonds. Instead, the monetary authorities will then be forced to finance the deficits by

issuing new money.

CASE STUDY EXTENSION

19–11 Inflation Indexed Bonds and Expected Inflation

One way to measure expected inflation, as the text points out, is to look at the difference in yields on

0.5 percent by December. In late 2009, the expected inflation rate had moved back up to about 2 percent.

One should not, however, place too much emphasis on the inflation expectations number as measured

by the difference in these yields on government securities. One factor may lead the difference in yields to

overstate expected inflation and two other factors may lead it to understate expected inflation. First,

because investors holding nominal bonds face the risk that actual inflation will turn out to be different than

though you continue to hold the bond and don’t receive the $30 until you sell it or it matures. Investors

may demand a higher yield on TIPS to compensate for this accelerated taxation of principal, so the

difference in yields will tend to understate expected inflation.

Depending on the extent to which these factors matter, expected inflation measured as the difference

in these yields might be overstated or understated. If we assume, however, that the relative importance of

475

476

LECTURE SUPPLEMENT

19–12 Additional Readings

The Spring 1989 issue of the Journal of Economic Perspectives 3 contains a symposium on “Budget

Deficits.” Two papers in particular address Ricardian equivalence: Robert Barro, “The Ricardian

Approach to Budget Deficits,” pp. 37–55; and Douglas Bernheim, “A Neoclassical Perspective on Budget

Deficits,” pp. 55–72,. Bernheim also discusses Ricardian equivalence in D. Bernheim, “Ricardian

Equivalence: An Evaluation of Theory and Evidence,” in S. Fischer (ed.), NBER Macroeconomics Annual,

1987 (Cambridge, Mass.: MIT Press), pp. 263–316.