4. The marginal product of medical care declines as

medical expenditures rise because the improve-

ment in health outcomes is very large when med-

ical care goes from non ex is tent to basic (i.e.,

when medical expenditures are low), but, as the

level of treatment rises (and therefore as expendi-

tures rise), patients tend to undergo treatments

supply of health- care providers. In addition, the

investment required for medical school and resi-

dency keeps the supply of doctors lower than

what might be considered optimal for society. Fur–

thermore, the market power that many health-

care providers enjoy because of imperfect

competition keeps supply lower and prices higher

than they would be in a more competitive market.

Hints and Common Errors: Another

supply- related driver of medical care costs is the

Study Prob lems

1. If my insurance com pany charges me a $25

copay, then the marginal cost of my consultation

to me is $25 (though the marginal cost of the

Questions for Review

1. Asymmetric information is an information

imbalance in which one party in an economic

transaction knows more about product cost, qual-

ity, and so forth than the other party. Asymmet–

ric information matters in the health- care

care system.

2. (Answers here will vary.) Adverse se lection

occurs in the used car market because the sellers

of the cars know more about their quality than

the buyers do, and owners of low- quality cars

are generally more willing to sell their cars at a

given price than are owners of high- quality cars.

This observation causes rational consumers to be

suspicious of people who are willing to sell their

used cars, as the cars that the consumers actu-

3. (Answers here will vary.) For the adverse se lection

prob lem, buyers could use an information source

such as CARFAX to verify the history of the vehi-

cle, or the seller could offer a warranty to both

signal quality and insure the buyer against

Solutions to Chapterfi18 Text Prob lems

from the two plans), we can use the following

equation, where x represents the level of

anticipated medical expense:

medical expenses were $666.67.

8. a. This is adverse se lection because the seller of

the ticket has more information about its

legitimacy and because a seller is more willing

to sell a bogus ticket than a legitimate ticket at

any given price.

your agent in order to look out for your lawn-

mowing interests. Unfortunately for the lawn,

the teenager’s incentives aren’t aligned with

yours, and undermowing results.

10. The key characteristic that distinguish the mar–

11. a. You should book every visit for which the

price you’d be willing to pay is at least equal

to the price you actually have to pay, namely

$300. That is another way of saying that you

should buy up to the point where your

demand curve hits the marginal cost curve.

So, you should plan on four visits.

b. Full coverage means that instead of a constant

3. The insurance com pany uses the physical exam,

to the degree pos si ble, to overcome the adverse

se lection prob lem of asymmetric information.

system.

4. a.

An annual physical for someone between the

ages of 20 and 35 likely has fairly elastic

demand because it’s not a crucial procedure.

b. An MRI used to detect cancer likely has fairly

inelastic demand because it is a crucial proce–

dure with few substitutes.

5. If the sale of kidneys were legalized, the price of a

kidney would rise from the current price of zero

to what ever price would bring the supply and

demand of kidneys into equilibrium. (In contrast,

the price of kidneys in illegitimate markets would

Hints and Common Errors: If, in

contrast, the demand for kidneys were to be

defined by the number of people needing

transplants rather than by willingness to pay,

it’spos si ble that a shortage could still exist.

7. If the consumer anticipated $200 per month in

medical bills, she would expect to pay $100

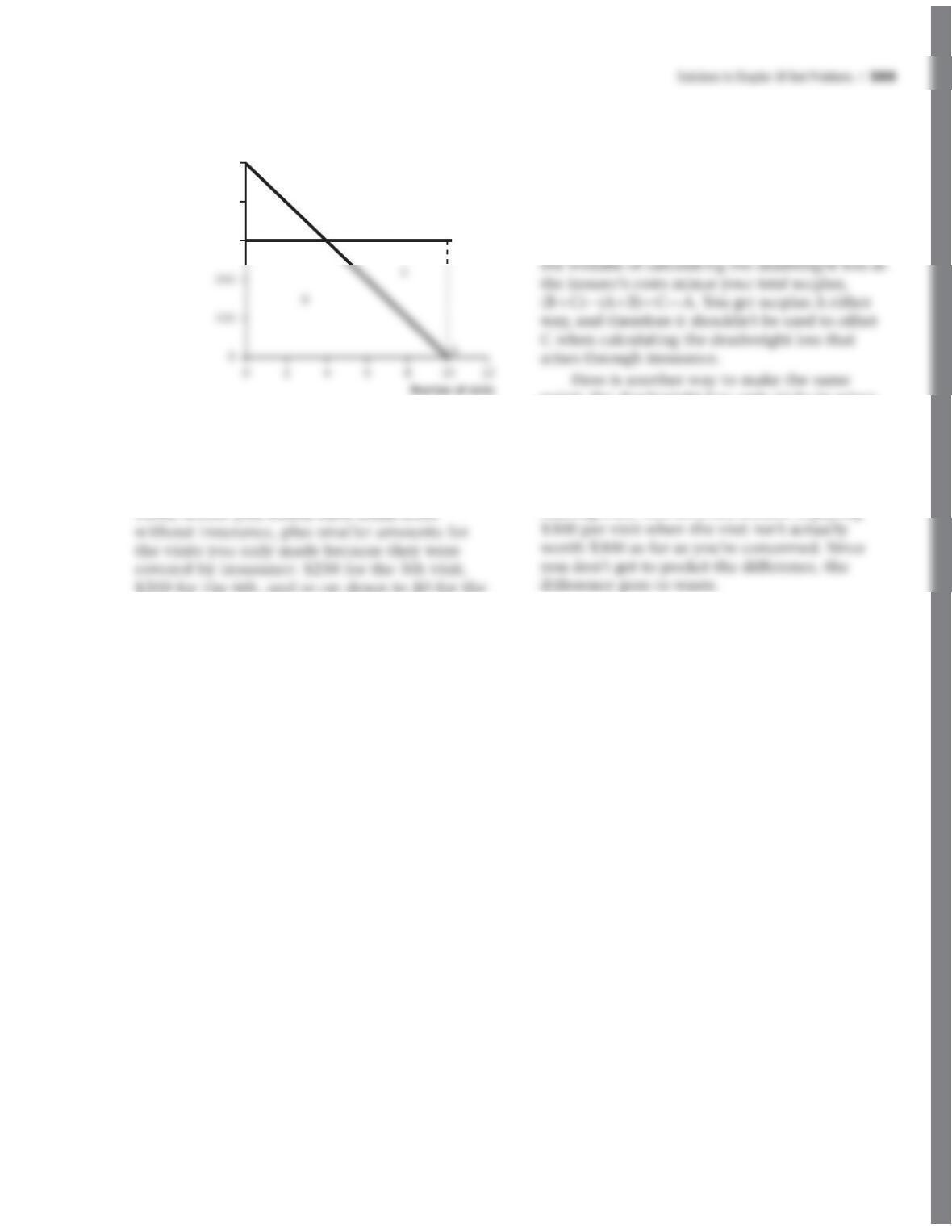

10thvisit, which even with insurance you

were basically indifferent about. Your total

gain in surplus is 4($300) $250 $200 $150

$100 $50 $0 “ $1,950. The difference

between that and the insurer’s cost is

$3,000 $1,950 “ $1,050, and that is the

deadweight loss.

Hints and Common Errors: Don’t make

point: the deadweight loss only kicks in when

your decisions start to be affected. For the four

visits you would have made either way, the $300

insurance coverage is just a transfer from the

insurer to you. There, the insurer’s loss is your

gain, with no benefit going to waste. But

exceeds your gain by area C. That is the dead-

weight loss in graphical terms.

Price

($/visit)

MC

A

$500

400

300

Keeping in mind that visits occur as

discrete units rather than as a continuous

series of fractions, we can calculate the

insurer’s total cost, 10 w $300 “ $3,000. Your

gain in surplus is $300 for each of the first 4