D. Options have a unique set of terminology. Define the following

terms: (1) call option; (2) put option; (3) exercise price; (4)

striking, or strike, price; (5) option price; (6) expiration date; (7)

exercise value; (8) covered option; (9) naked option; (10) in-the-

money call; (11) out-of-the-money call; and (12) LEAPS.

Answer: [Show S18–5 through S18-7 here.]

A call option is an option to buy a specified number of shares of a

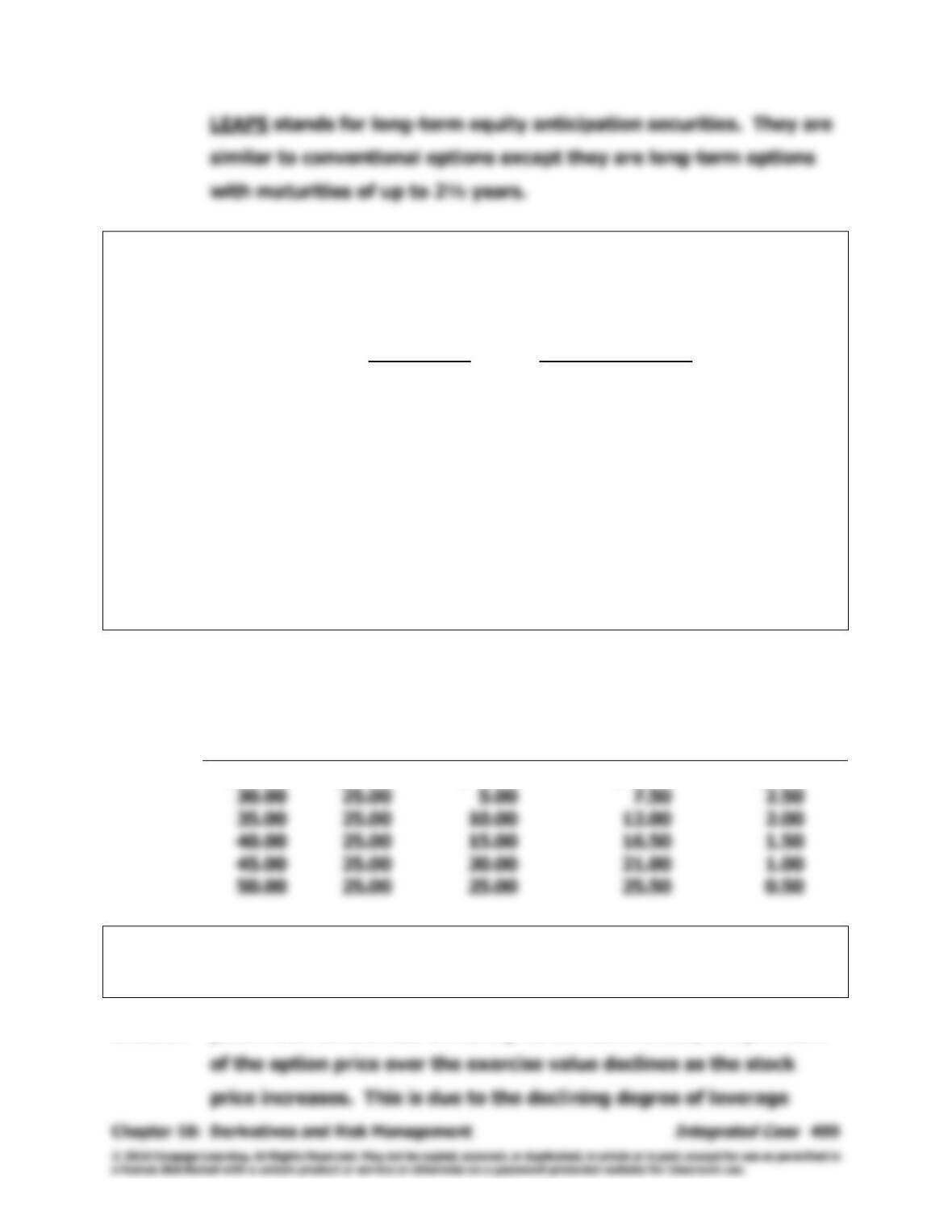

E. Consider Tropical Sweets’ call option with a $25 strike price. The

following table contains historical values for this option at different

stock prices:

Stock Price Call Option Price

$25 $ 3.00

30 7.50

35 12.00

40 16.50

45 21.00

50 25.50

(1) Create a table that shows the (a) stock price, (b) strike price, (c)

exercise value, (d) option price, and (e) premium of option price

over exercise value.

Answer: [Show S18–8 and S18-9 here.]

Price of

Stock

Strike

Price

Exercise Value

of Option

Market Price

of Option

Premium

(a)

(b)

(a) – (b) = (c)

(d)

(d) – (c) = (e)

$25.00

$25.00

$ 0.00

$ 3.00

$3.00

12.00

16.50

E. (2) What happens to the premium of option price over exercise value as

the stock price rises? Why?

Answer: [Show S18–10 and S18-11 here.] As the table shows, the premium

F. In 1973, Fischer Black and Myron Scholes developed the Black-

Scholes Option Pricing Model.

(1) What assumptions underlie this model?

Answer: [Show S18–12 here.] The assumptions that underlie the Black-

Scholes Option Pricing Model are as follows:

F. (2) Write the three equations that constitute the model.

Answer: [Show S18–13 here.] The Black–Scholes Option Pricing Model consists

of the following three equations:

Here,

F. (3) What is the value of the following call option according to this

model?

Stock price = $27.00.

Exercise price = $25.00.

Time to expiration = 6 months.

Risk-free rate = 6.0%.

Stock return variance = 0.11.

Answer: [Show S18–14 and S18-15 here.] The input variables are:

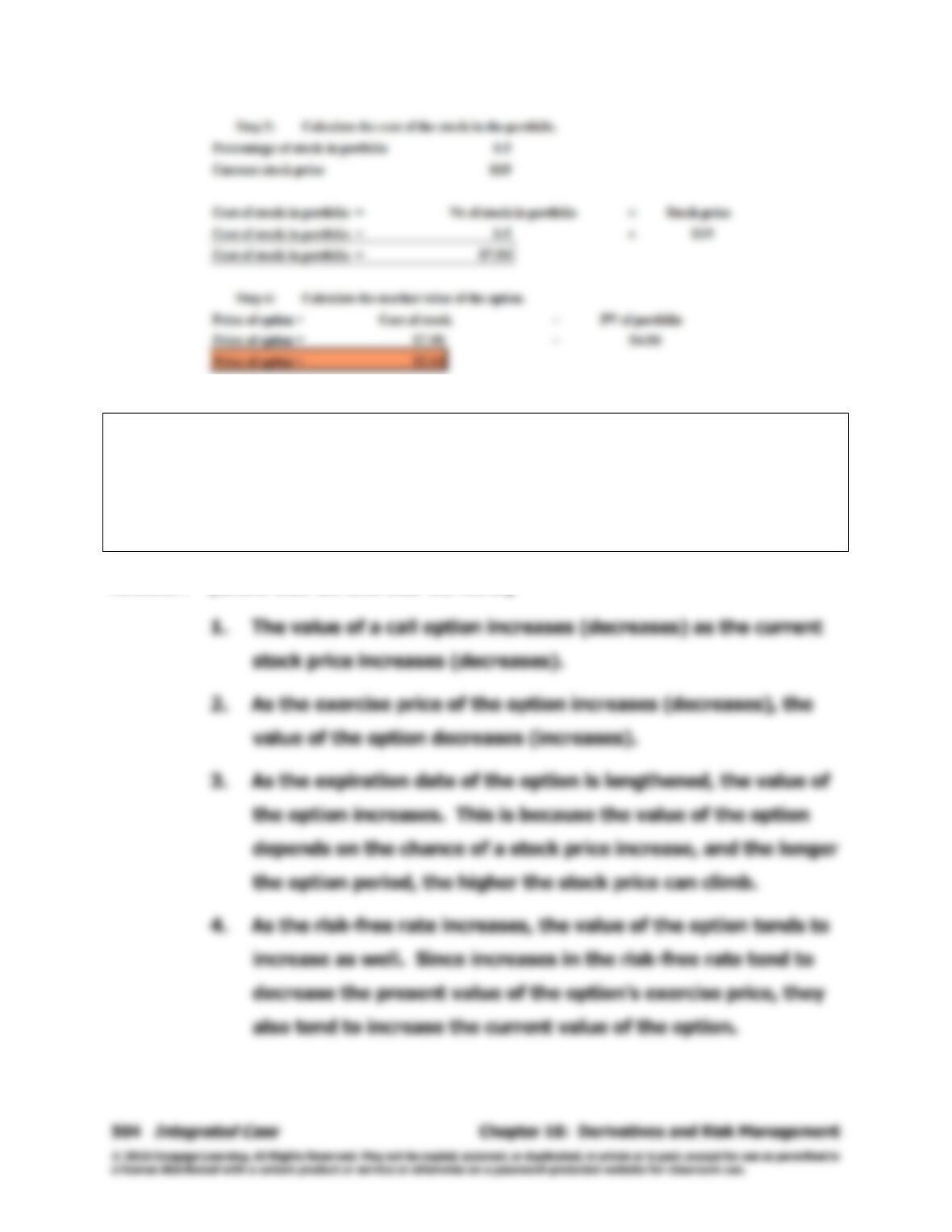

G. Disregard the information in part F. Determine the value of a firm’s

call option using the binomial approach by creating a riskless hedge

given the following information. A firm’s current stock price is $15

per share. Options exist that permit the holder to buy one share of

the firm’s stock at an exercise price of $15. These options expire in

6 months, at which time the firm’s stock will be selling at one of

two prices, $10 or $20. The risk-free rate is 6%. What is the value

of the firm’s call option?

Answer: [Show S18-16 through S18–19 here.]

H. What effect does each of the following call option parameters have

on the value of a call option? (1) Current stock price; (2) exercise

price; (3) length of the option period; (4) risk-free rate; (5)

variability of the stock price.

Answer: [Show S18-20 and S18-21 here.]

I. What are the differences between forward and futures contracts?

Answer: [Show S18-22 here.] Forward contracts are agreements where one

J. Explain briefly how swaps work.

Answer: [Show S18-23 here.] A swap is the exchange of cash payment

K. Explain briefly how a firm can use futures and swaps to hedge risk.

Answer: [Show S18-24 and S18-25 here.] Hedging is usually used when a

L. What is corporate risk management? Why is it important to all firms?

Answer: [Show S18–26 through S18-29 here.] Corporate risk management

Appendix 18A

Valuation of Put Options

Answer to Question

18A-1 The put-call parity relationship is explained by the following equation:

Solutions to Problems

18A-1 Put option = V – P +

trRF

Xe–

where V = value of the call option.

18A-2 Put option = V – P +

trRF

Xe–

where V = value of the call option.