Chapter 18: Derivatives and Risk Management

Learning Objectives

485

Chapter 18

Derivatives and Risk Management

Learning Objectives

After reading this chapter, students should be able to:

◆ Identify the circumstances in which it makes sense for companies to manage risk.

◆ Describe the various types of derivatives and explain how they can be used to manage risk.

◆ Value options using the Binomial and Black-Scholes Option Pricing Models.

◆ Discuss the various elements of risk management and the different processes that firms use to manage

risks.

486

Lecture Suggestions

Chapter 18: Derivatives and Risk Management

Lecture Suggestions

This chapter provides information on derivatives and how they are used in risk management. We begin by

identifying the reasons why risk should be managed. Then, we give a brief background on derivatives. We

illustrate a riskless hedge and present the Binomial Option Pricing Model. Next, we present the Black-

Scholes Option Pricing Model to discuss the various factors that affect a call option’s value. We specifically

DAYS ON CHAPTER: 2 OF 56 DAYS (50-minute periods)

Chapter 18: Derivatives and Risk Management

Answers and Solutions

487

Answers to End-of-Chapter Questions

18-1 Risk management may increase the value of a firm because it allows corporations to (1) increase

their use of debt; (2) maintain their optimal capital budget over time; (3) avoid costs associated

18-2 The market value of an option is typically higher than its exercise value due to the speculative

18-3 There are several ways to reduce a firm’s risk exposure. First, a firm can transfer its risk to an

insurance company, which requires periodic premium payments established by the insurance

company based on its perception of the firm’s risk exposure. Second, the firm can transfer risk–

18-4 The futures market can be used to guard against interest rate and input price risk through the use

of hedging. If the firm is concerned that interest rates will rise, it would use a short hedge, or sell

18-5 Swaps allow firms to reduce their financial risk by exchanging their debt for another party’s debt,

18-6 If the elimination of volatile cash flows through risk management techniques does not significantly

488

Answers and Solutions

Chapter 18: Derivatives and Risk Management

Solutions to End-of–Chapter Problems

a. Exercise value = Current stock price – Exercise price

Chapter 18: Derivatives and Risk Management

Answers and Solutions

489

18-4 P = $15; X = $15; t = 0.5; rRF = 0.10; 2 = 0.12; d1 = 0.32660; d2 = 0.08165; N(d1) = 0.62795;

N(d2) = 0.53252; V = ?

18-5 Futures contract settled at 10016/32% of $100,000 contract value, so PV = 1.005 $1,000 = $1,005

18-6 a. In this situation, the firm would be hurt if interest rates were to rise by March 2015, so it would

490

Answers and Solutions

Chapter 18: Derivatives and Risk Management

c. In a perfect hedge, the gains on futures contracts exactly offset losses due to rising interest

b. Remember, that the options will be exercised only if they yield a positive payoff. In this case,

c. In this case, the call option will not be exercised. The returns under each of the scenarios are

summarized below:

e. Recall, that the stock price is expected to be either $50 or $70, with equal probability. If

Chapter 18: Derivatives and Risk Management

Answers and Solutions

491

b. Ending Price 0.80 = Ending Stock Value Ending Option Value

18-9

Range of values

Time until expiration

$50.00

Current stock price

492

Answers and Solutions

Chapter 18: Derivatives and Risk Management

c. and d.

Chapter 18: Derivatives and Risk Management

Comprehensive/Spreadsheet Problem

493

Comprehensive/Spreadsheet Problem

Note to Instructors:

The solution to part a of this problem is provided at the back of the text; however, the

solutions to parts b, c, d, and e are not. Instructors can access the

Excel

file on the textbook’s

website.

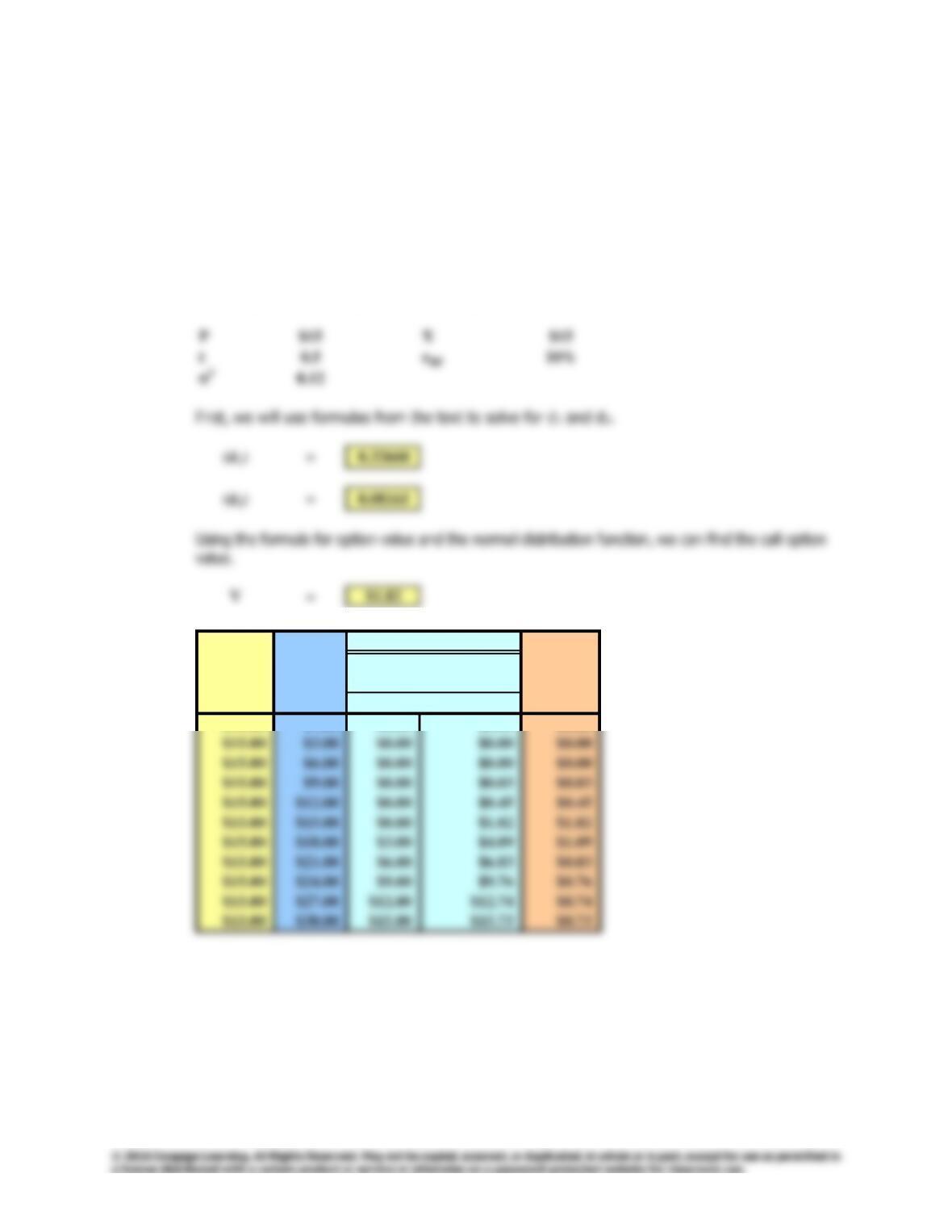

18–10 a. Assume you have been given the following information on Purcell Industries:

b.

Current Intrinsic B-S formula

Exercise stock Value Value Option

Price price $0 $1.82 Premium

$15.00 $1.00 $0.00 $0.00 $0.00

Option Value

494

Comprehensive/Spreadsheet Problem

Chapter 18: Derivatives and Risk Management

$15

Option Value

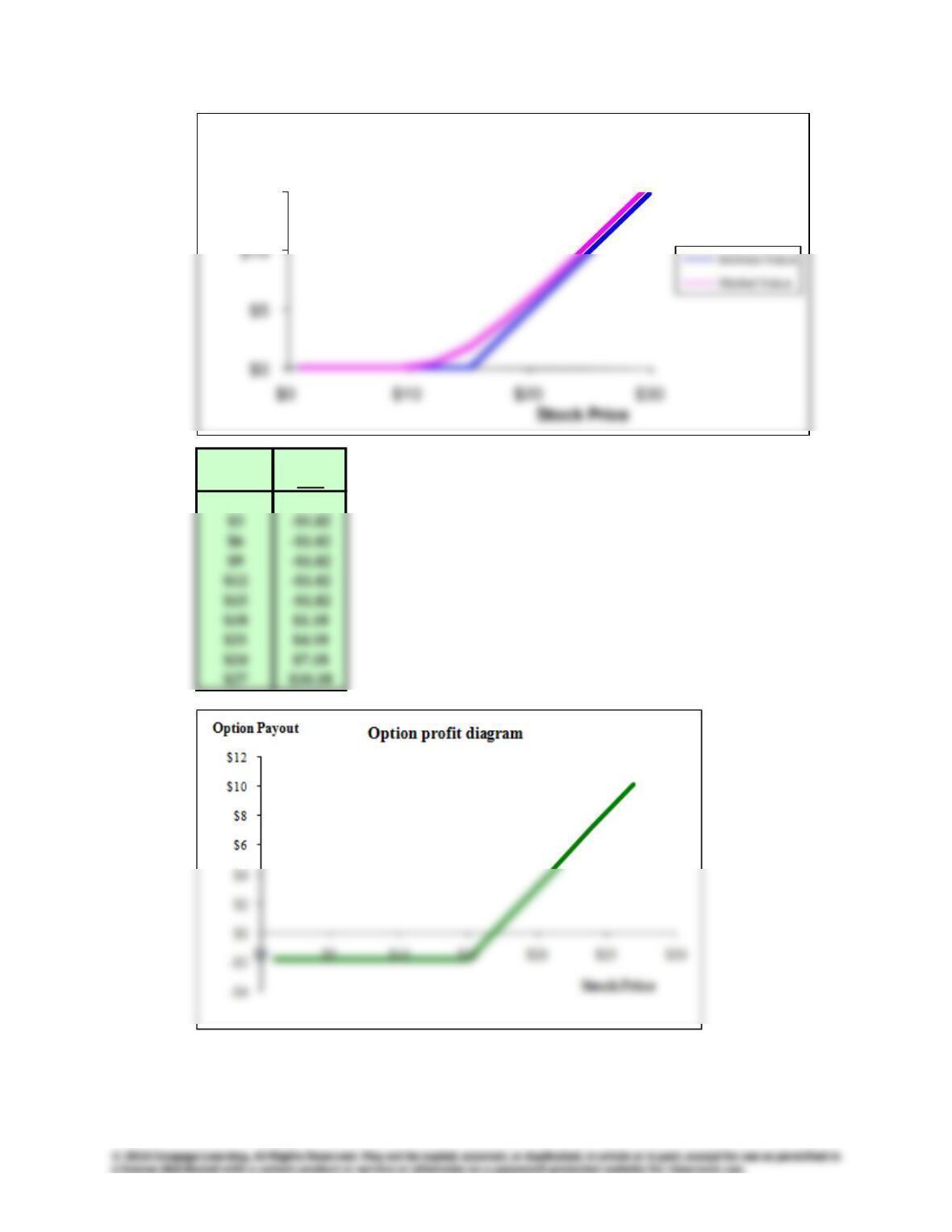

Intrinsic–vs–Market Value of Options

c.

XCALL = $15

if P= … Call

$1 -$1.82

Chapter 18: Derivatives and Risk Management

Comprehensive/Spreadsheet Problem

495

e.

Step 1:

Step 2:

Calculate the present value of the riskless portfolio today.

Calculate the cost of the stock in the portfolio.

Future Portfolio Value

(1 + rRF)t

PV =

496

Integrated Case

Chapter 18: Derivatives and Risk Management

Integrated Case

18-11

Tropical Sweets Inc.

Derivatives and Corporate Risk Management

Assume that you have just been hired as a financial analyst by Tropical Sweets

Inc., a midsized California company that specializes in creating exotic candies

from tropical fruits such as mangoes, papayas, and dates. The firm’s CEO,

George Yamaguchi, recently returned from an industry corporate executive

conference in San Francisco. One of the sessions he attended was on the

pressing need for smaller companies to institute corporate risk management

programs. As no one at Tropical Sweets is familiar with the basics of

derivatives and corporate risk management, Yamaguchi has asked you to

prepare a brief report that the firm’s executives can use to gain at least a

cursory understanding of the topics.

To begin, you gather some outside materials on derivatives and corporate

risk management and use those materials to draft a list of pertinent questions

that need to be answered. In fact, one possible approach to the paper is to

use a question-and-answer format. Now that the questions have been

drafted, you must develop the answers.

A. Why might stockholders be indifferent to whether a firm reduces

the volatility of its cash flows?

Answer: [Show S18-1 and S18-2 here.] If volatility in cash flows is not

caused by systematic risk, then stockholders can eliminate the risk

Chapter 18: Derivatives and Risk Management

Integrated Case

497

B. What are seven reasons risk management might increase the value

of a corporation?

Answer: [Show S18-3 here.] There are no studies proving that risk

management either does or does not add value. However, there are

C. What is an option? What is the single most important characteristic

of an option?

Answer: [Show S18-4 here.] An option is a contract that gives its holder the