CASE STUDY EXTENSION

18-5 Are Forecasters Rational?

Although forecasters often make mistakes, they may still be doing the best that they can. The theory of

rational expectations suggests a way of evaluating economists’ and others’ forecasts. Rational expectations

suggest that forecasters should base their predictions on all available information. It should not then be

possible systematically to improve upon a forecast using information that is publicly available at the time

the forecast is made. If it were, then by definition, this could not be the best forecast. One common way to

evaluate forecasts is thus to look at forecast errors (that is, the after–the–fact difference between the actual

values of a variable and the forecast) and to see if those errors are correlated with available information.

The evidence is mixed. Many studies have found that inflation forecasts are not rational in this sense.

But a problem with many of these surveys is that they do not consider the forecasts of professionals who

have a financial stake in the accuracy of their forecasts. Michael Keane and David Runkle describe this

problem as follows1:

1 M. Keane and D. Runkle, “Are Economic Forecasts Rational?” Federal Reserve Bank of Minneapolis Quarterly Review 13, no. 2 (Spring 1989):

26–33. This article also contains discussion of, and references to, other work testing the rationality of forecasts.

LECTURE SUPPLEMENT

18-6 Microfoundations and Aggregation

One area of some methodological dispute in macroeconomics involves the desirability of

microfoundations—microeconomic underpinnings for macroeconomic relationships. Part V of the

textbook considers microfoundations in detail. It shows how careful microeconomic analysis both

provides broad support for, and suggests refinements of, some of the key behavioral relationships in our

clearly traced through their impact on individual behavior.

Yet other economists are skeptical. They point out that such models simply assume that the aggregate

behavior of the economy looks just like the behavior of a single individual. The Nobel–Prize–winning

economist James Tobin expresses this criticism as follows2:

It is possible to give macro relations the veneer of rigorous derivation from utility or profit

agents making inconsistent decisions: there is no way that Robinson the producer of goods will make

choices inconsistent with the wishes of Robinson the consumer. In the real world, these decisions are made

by different people and might not be consistent. But simple representative–agent models based on explicit

microfoundations need not be Robinson Crusoe models. Coordination failure models (see Chapter 19), for

example, typically feature just one type of agent but emphasize that the interdependencies of agents’

CASE STUDY EXTENSION

18-7 Spare a Thought for the Empirical Macroeconomist

One of the most important tests of a theory is its ability to explain the data. Yet over and over again in the

textbook we find that the data do not provide a definitive answer to the questions that concern

macroeconomists and do not allow us to distinguish with complete confidence between different theories.

18-8 The Response to Romer

Prior to Christina Romer’s work, economists accepted as a largely unquestioned stylized fact the view that

the U.S. economy was much more stable after World War II than prior to it. Romer’s work showed that

there could be no such presumption: differences in the quality of the data for the two periods mean that

comparisons are difficult and perhaps unreliable. These same problems with early data, however, led some

economists and economic historians to be skeptical of Romer’s conclusions, since they in turn questioned

whether or not Romer had actually made appropriate corrections to the historical data.1

One problem concerns GDP data before 1919. Prior to that date, information on incomes was lacking

and so estimates are based largely on data on commodity output. Unfortunately, this accounts for only

about half of GDP, since it neglects transportation, distribution, and services. Measuring volatility on the

basis of commodity output is misleading because it is more variable than total GDP; researchers make a

correction for this on the basis of some period in which data exist on both series. The question then is what

period should be used? Romer argued that the period of the Great Depression should be excluded, and that

ADDITIONAL CASE STUDY

18-9 Distrust of Policymakers

Some economists believe that there may be a good case in principle for government intervention in the

macroeconomy but doubt the ability of policymakers to enact the right policy in practice. Certainly, there

is evidence that U.S. presidents lack basic macroeconomic literacy.

We think of civil rights as something like crime in your neighborhoods. And, for example,

when crime figures are going in the right direction that’s good, that’s a civil right. Similarly,

we think of it in terms of quality of life, and that means interest rates.

You know it’s funny, Mr. Mondale talks about real interest rates. The real interest rate is

what you pay when you go down and try to buy a TV set or buy a car, or do whatever it is. The

interest rates when we left [sic] office were 21.5 percent. Inflation! Is it a civil right to have

that going right off the chart so you’re busting every American family, those who can afford it

the less?

ADDITIONAL CASE STUDY

18-10 The Political Business Cycle

That politicians may manipulate the economy to serve partisan aims has been documented by the political

scientist Edward Tufte. As one example, Tufte considered transfer payments between 1961 and 1976. He

noted that the amount of transfer payments was generally increasing through time, implying that we would

expect the volume of transfer payments to be higher in December than in November, and in turn higher in

election or for some other reason remains a matter of controversy. Critics of the Fed have pointed to

Burns’s ties with Nixon for many years and the Burns–Nixon proposal to stimulate the economy before the

1960 election.” Fiscal policy was also expansionary. Whereas the federal government ran a $3 billion

surplus in 1969 and a $3 billion deficit in 1970, it ran $23 billion deficits in 1971 and 1972.4 Tufte also

documents substantial increases in almost all transfer payments in the last quarter of 1972. “It appears that

ADDITIONAL CASE STUDY

18-11 The Political Business Cycle at Its Worst

Theories of the political business cycle suggest that politicians may manipulate the economy to achieve

political ends. For example, an incumbent president may try to generate a boom in an attempt to be

reelected.

There is a flip side to this. A leader presiding over an economy that is doing poorly may need other

828–46.

ADDITIONAL CASE STUDY

18-12 The Economy Under Democratic and Republican Presidents

As discussed in the Chapter 18 of the text and in the previous two supplements, one view of politicians is

that they have a short time horizon that coincides with the election cycle. According to this view, policies

are designed to ensure reelection rather than with the long–term health of the economy in mind. If this

view is correct, then one would expect to find similar patterns of macroeconomic policies regardless of

which political party is in office.

Table 1 Real GDP Growth During Democratic and Republican Administrations (percentage–change, 4th

quarter over 4th quarter)

Year of Term

President

First

Second

Third

Fourth

Democratic Administrations

Truman

–1.5

13.4

5.5

5.3

6.4

4.3

5.2

5.1

8.5

4.5

2.7

5.0

5.0

6.7

1.3

0.0

Clinton I

2.6

4.1

2.3

4.5

Clinton II

4.4

5.0

4.7

2.9

Obama I

–0.2

2.7

1.7

1.6

3.1

2.4

Average

3.5

5.4

3.3

3.5

0.5

2.7

6.6

2.0

0.4

2.7

4.5

0.9

Nixon

2.1

–0.2

4.4

6.9

Nixon/Ford

4.0

–1.9

2.6

4.3

Reagan I

1.3

–1.4

7.8

5.6

Reagan II

4.3

2.9

4.4

3.8

Bush (senior)

2.8

0.6

1.2

4.3

0.2

2.0

4.4

3.1

3.0

2.4

1.9

Average

2.1

1.1

4.2

3.1

828–46.

LECTURE SUPPLEMENT

18-13 Price Level Versus Inflation Targeting

Inflation targeting differs from price level targeting: with price level targeting the central bank must

rate is 6 percent. Prices in both countries rose by 6 percent between year 2 and year 3. The central bank of

country A must act to bring the price level back to its target. Because the actual price level in year 3 is

above the year 4 target level, the central bank must deflate. To meet its target in year 4, prices must fall by

1.8 percent. In contrast, the central bank of country B merely needs to reduce the inflation rate, bringing it

back to the 2 percent target. In country A prices must fall; in country B the rise in prices must be reduced.

Table 1 Price Level Versus Inflation Targeting

Year

Price Level Target

Inflation Target

1

100.0

2

102.0

2%

3

104.0

2%

4

106.1

2%

448

CASE STUDY EXTENSION

18-14 Inflation Targeting

In 1989 New Zealand passed legislation requiring the central bank (in consultation with the Ministry of

Finance) to establish inflation targets. Over subsequent years, many other countries followed New

Zealand’s example. And in 2012, the United States adopted a policy of targeting inflation, when the

Federal Open Market Committee of the Federal Reserve set a target of 2 percent. Table 1 provides details

on inflation targeting in seven industrial countries and the Euro–zone. Most of these countries set a range

within which inflation is allowed to fluctuate and update the target every few years. The Federal Reserve

seeks to “maintain an inflation rate of 2 percent over the medium term,” although actual inflation may

differ from that rate in the short term.

Table 1 Inflation Targeting in Industrial Countries

Country/Area

Current Target

Index Targeted

Who Sets

Target?

Australia

2–3%

CPI

Central Bank and

Government

Canada

1–3%

CPI

Central Bank and

Government

Euro–zone

Below but close to 2%

Harmonized Index of

Consumer Prices

Central Bank

1–3%

CPI

Central Bank and

New Zealand

1–3%

CPI

Central Bank and

Government

United Kingdom

CPI

Government

449

CASE STUDY EXTENSION

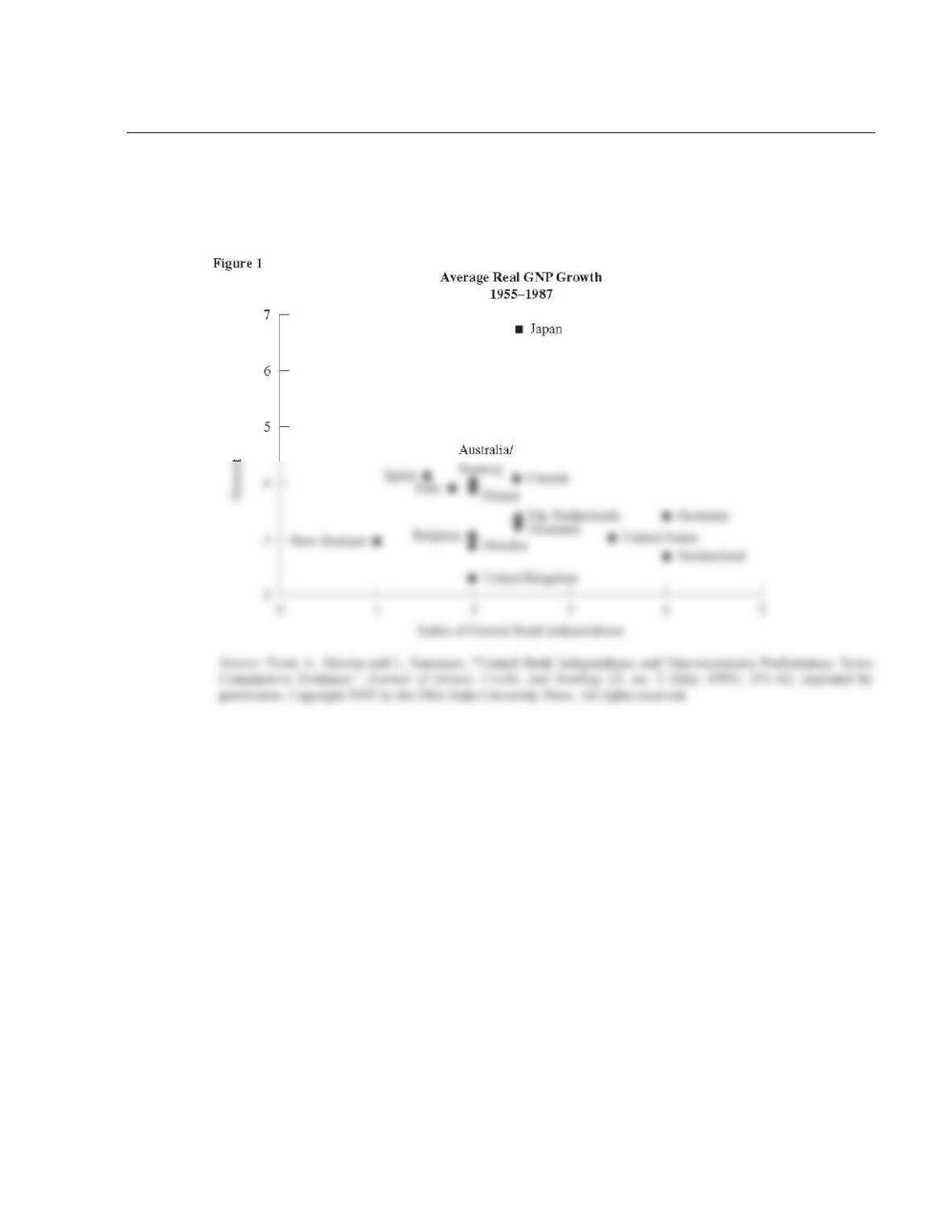

18-15 Central–Bank Independence and Growth

Figure 1 shows the relationship between the degree of central–bank independence and economic growth in

16 countries from 1955 to 1987. There appears to be no connection between an independent central bank

and higher or lower economic growth.

CASE STUDY EXTENSION

18-16 Measuring Central–Bank Independence

Studies of central–bank independence and the macroeconomy measure independence by first establishing a

list of criteria thought to characterize independence and then examining central–bank charters and laws to

determine which criteria are met by each central bank in the study. Legal measures of independence,

however, may not be reflective of the true constraints affecting central banks. Thus a country believing

that it can achieve low inflation simply by granting its central bank legal independence may be sorely

disappointed.

Some countries that recently passed legislation to increase the independence of their central banks are

finding that operational independence is more difficult to achieve. For example, in June 1996 the Russian

parliament passed a law ordering the Central Bank of Russia to transfer $1 billion to the government to

finance President Yeltsin’s preelection spending promises.1 While the central bank protested that such a

requirement jeopardized its independence, it complied with the measure. In January 1993 Venezuela

increased the legal independence of its central bank. Sixteen months later the governor (head) of the

central bank and several board members resigned, claiming that the government was trying to reduce the

autonomy of the central bank.2 Most recently, in June 1996, the governor of Chile’s independent central

bank resigned following a conflict with the government.3 Given that a conflict between the central bank

1 John Thornhill, “Central Bank Attacks Yeltsin ‘Violation,’” Financial Times, June 11, 1996.

2 Joseph Mann, “Venezuelan Policy under Fire as Governor and Directors Resign,” Financial Times, April 28, 1994.

3 Imogen Mark, “Test for Chile’s Central Bank,” Financial Times, July 3, 1996.

4 Alex Cukierman, Central Bank Strategy, Credibility, and Independence: Theory and Evidence (Cambridge, Mass.: The MIT Press, 1992).

5 Guy Debelle and Stanley Fischer, “How Independent Should a Central Bank Be?” Center for Economic Policy Research Publication no. 392,

LECTURE SUPPLEMENT

18-17 Additional Readings

Two very accessible and concise books on stabilization policy are Central Banking in Theory and