CHAPTER 18

Alternative Perspectives on

Stabilization Policy

Notes to the Instructor

Chapter Summary

This chapter discusses issues in macroeconomic policy. Even though the AD–AS model suggests

the desirability and simplicity of stabilization policy, in practice the benefits of stabilization

policy are less clear and its complications are much more evident. The chapter addresses two key

questions. First, should policymakers try to stabilize the economy or instead be content with

Comments

The material in this chapter can be covered in two lectures. The taxonomy set up in this chapter

makes discussion of policy issues very clear, and as a result students like this material. I

emphasize that many economists believe that there is a case in principle for stabilizing the

economy but that pragmatic difficulties may override this case.

Use of the Web Site

This is the natural time to discuss the presidential policy game in the Web–based software. Not

surprisingly, students seem to like this game a lot. As well as being fun, it is intended to teach a

number of lessons about the difficulty of stabilization and of how expansion can be beneficial in

the short run but costly in the long run. Instructors might also choose (at some point) to explain

to the students about the details of the model, as explained in the documentation.

Use of the Dismal Scientist Web Site

Go to the Dismal Scientist Web site and download data for the past three years on the rate of

consumer price inflation for the Euro–zone, the United Kingdom, Canada, Australia, and New

Zealand. These countries all have explicit inflation targets that their central banks use in setting

monetary policy. Visit the central bank Web sites of these countries (or see Supplement 18–16)

426 | CHAPTER 18 Alternative Perspectives on Stabilization Policy

Chapter Supplements

This chapter includes the following supplements:

18-2 Profit Sharing as an Automatic Stabilizer

18-4 The Pitfalls of Forecasting (Case Study)

18–5 Are Forecasters Rational? (Case Study)

18-7 Spare a Thought for the Empirical Macroeconomist (Case Study)

18-9 Distrust of Policymakers

18-11 The Political Business Cycle at Its Worst

18-13 Price Level Versus Inflation Targeting

18-15 Central–Bank Independence and Growth (Case Study)

18-17 Additional Readings

Lecture Notes | 427

Lecture Notes

Introduction

Our interest in macroeconomic phenomena is motivated by a desire to understand not only the

functioning of the economy but also how macroeconomic policies affect the economy, with a

view to understanding, in turn, if there is a role for government policies directed at stabilization.

Ultimately, we wish to answer two questions: Can the government improve the functioning of

the economy by pursuing active stabilization policies? How should a well–designed economic

policy be conducted? Both are considered in this chapter.

To answer these questions, we first need answers to two prior questions: How would the

economy perform in the absence of stabilization policies? How do government policies affect

the overall functioning of the economy? Our analysis to this point provides answers. Given that

18–1 Should Policy Be Active or Passive?

The aggregate demand–aggregate supply model indicates that, in principle, policy–makers could

manipulate aggregate demand in order to stabilize the economy. Despite such a conclusion,

many economists do not advocate an active role for government policy.

New classical economists believe that prices and wages are flexible and usually argue that

stabilization policy is inappropriate. They believe that fluctuations arise either as an efficient

response to shocks (the real–business–cycle view) or as a result of the information problems

summarized in the imperfect–information theory of short–run aggregate supply. Since they

believe in price and wage flexibility, their presumption is that markets serve to allocate goods

Lags in the Implementation and Effects of Policies

If prices and wages are sticky, as Keynesians believe, then the theoretical case for intervention is

much stronger. Nevertheless, some proponents of new Keynesian ideas are also skeptical about

stabilization policy. In reality, the economy is not as easy to influence as our models suggest,

and there are many practical difficulties associated with economic stabilization. Economists

point in particular to lags in the policy process.

First, it takes time to recognize and take actions to respond to shocks that hit the economy.

As just noted, if policymakers cannot recognize shocks any more quickly than private

individuals can, then they have no scope for stabilization. Even after a shock has been identified,

it may take time to change the course of monetary and fiscal policies. This is known as the inside

428 | CHAPTER 18 Alternative Perspectives on Stabilization Policy

money supply affect interest rates and thus investment). The presence of inside and outside lags

makes active use of fiscal and monetary policies imprecise. But these lags do not imply that

policy should remain passive in the presence of a severe and lengthy economic contraction, such

as the downturn that began in 2008.

Some features of the economy help keep GDP close to the natural rate without direct

action by policymakers. When the economy is in a boom, tax revenues increase and transfer

payments, such as unemployment insurance and other welfare benefits, decrease. The opposite

The Difficult Job of Economic Forecasting

A fundamental difficulty with good policymaking is that it depends upon the ability to forecast

future economic events. The large–scale macroeconometric models discussed in Chapter 12 are

of some use here, since they help predict the behavior of key economic variables, given

Case Study: Mistakes in Forecasting

The difficulty of economic forecasting is well illustrated by the failure of forecasters to predict

both the Great Depression and the severe recession of 2008–2009 with any accuracy. Almost all

forecasters predicted that the poor economic performance at the start of the Depression would be

short–lived and that recovery was imminent. And in the early stages of the economic downturn

Ignorance, Expectations, and the Lucas Critique

The economist Robert Lucas has criticized the use of traditional economic and econometric

models for the evaluation of economic policy. Lucas’s point is that individuals’ behavior and

actions—and particularly their expectations—in general depend upon the policies chosen by

government. Therefore, Lucas argues, it is misleading to use standard models for policy

evaluation unless we take account of the effects of policies on expectations. For example, if the

economy has been experiencing moderate and fairly steady inflation, then people’s inflation

expectations might be well approximated by adaptive expectations. But if the Fed then

!Supplement 18–2,

“Profit Sharing as

!Supplement 18–3,

“The Labor

!Figure 18-1

!Supplement 18–5,

“The Pitfalls of

Lecture Notes | 429

The Historical Record

One way to help decide if policy should be active or passive is to try to determine whether

stabilization policies were successfully pursued in the past. Macroeconomists often look to

historical data to answer this question. Casual examination of the data supports the idea that

stabilization policies worked. In the period after World War II, policymakers used the insights of

Keynesian economics as a basis for active demand management. The data on GDP and other

variables indicate that this period was characterized by less severe fluctuations than the prewar

period. This evidence is not conclusive, however. It may have been that the economy was simply

not hit by such severe shocks. Alternatively, the changing composition of the economy may have

Case Study: Is the Stabilization of the Economy a Figment of the

Data?

The economist and economic historian Christina Romer has suggested that it may not even be

true that the economy has been more stable since World War II. She noted that the economy may

simply appear less volatile in recent years as a consequence of improved data collection. By

attempting to acquire better old data and by subjecting more modern data to the methods used in

constructing older data series, she demonstrated that at least part of the volatility of early data is

Case Study: How Does Policy Uncertainty Affect the Economy?

Recent research investigates the effect of policy uncertainty on economic performance. The

researchers developed an index of policy uncertainty that has three components. One component

considers the number of articles in major newspapers during a given month which contain the

words “uncertainty” or “uncertain”, “economic” or “economy, and at least one of the following:

“congress,” “legislation,” “white house,” “regulation,” “federal reserve,” or “deficit.” A second

component considers the number of temporary provisions in the tax code. These provisions are

often extended at the last minute and so create uncertainty in financial planning for businesses

and households. A third component considers the amount of disagreement among private

!Supplement 18–8,

“Spare a Thought

for the Empirical

Macroeconomist”

!Supplement 18–9,

“The Response to

Romer””

18–2 Should Policy Be Conducted by Rule or by Discretion?

Even if economists agreed upon the desirability of active stabilization policies, they would

probably still disagree about exactly how policy should be conducted. One possibility is

Distrust of Policymakers and the Political Process

In practice, the policies enacted by governments need not always be those that are best for the

economy. The idea of a well–informed, benevolent policymaker choosing monetary and fiscal

policy variables to stabilize the economy is a useful fiction for our analysis, but it hardly

describes the realities and complexities of the political process. Policymakers may not be well

The Time Inconsistency of Discretionary Policy

Time inconsistency provides a less pragmatic but perhaps more intriguing argument for favoring

rules over discretion. The insight is that policymakers may want to change their minds about the

appropriate policies to pursue, giving them an incentive to renege on previous policy

announcements. Individuals will understand this incentive and so will not believe the original

announcements. Policymakers’ incentive to deviate from announced policies, in other words,

causes those announcements to not be credible. A fixed–policy rule may be more credible, and

so ultimately better.

Case Study: Alexander Hamilton Versus Time Inconsistency

In the process of achieving independence, the United States incurred a substantial public debt.

The Secretary of the Treasury, Alexander Hamilton, strongly opposed suggestions that the

Rules for Monetary Policy

Various rules for monetary policy have been proposed. Perhaps the simplest and most famous is

Milton Friedman’s monetarist view that the growth rate of the money supply should be kept

constant. The argument for such a rule is that changes in the money supply may be a cause of

!Supplement 18–11,

“The Political

Business Cycle”

!Supplement 18–12,

“The Political

Business Cycle at

Its Worst”

!Chapter 18

Lecture Notes | 431

announced path. A third possible policy rule is an inflation target. In this case, the Fed adjusts

monetary policy in an attempt to maintain some announced target for inflation.

such problems.

Case Study: Inflation Targeting: Rule or Constrained

Discretion?

Inflation targeting, which started to become a popular policy objective for central banks in the

late 1980s, is not a strict commitment to a policy rule. Inflation targets are usually a range (e.g.,

1 to 3 percent), leaving central banks with a fair amount of discretion. In addition, in the face of

temporary shocks, inflation is allowed to deviate from the target range without invoking action

Case Study: Central–Bank Independence

Countries vary in the degree to which their central banks are independent from the government.

For example, in some countries the central bank is under the jurisdiction of the finance or

treasury department while in other countries the central bank is separate from the government.

18–3 Conclusion: Making Policy in an Uncertain World

The best and most careful economists are aware of the limitations of our understanding of the

macroeconomy and are correspondingly cautious about giving advice. But an imperfect

understanding is better than no understanding at all, and so economists cannot abdicate

Appendix: Time Inconsistency and the Tradeoff Between

Inflation and Unemployment

This appendix contains an analytic treatment of the time–inconsistency problem. Suppose that

the Fed’s preferences over inflation and unemployment can be represented by the loss function

L(u, π) = u + γπ2.

!Supplement 18–15,

“Inflation Targeting”

!Figure 18-2

!Supplement 18–16,

“”Central Bank

Independence and

432 | CHAPTER 18 Alternative Perspectives on Stabilization Policy

The Fed likes inflation to be as close to zero as possible and also likes unemployment to be as

low as possible, so the Fed wants to minimize this function. For simplicity, we suppose that the

Fed can simply choose the inflation rate. The behavior of the economy in the short run is

described by a Phillips curve,

u = un – α(π – Eπ).

Given the public’s expectations of inflation (Eπ), the Fed chooses π so as to minimize the

loss function. We can be show (by substituting for u in the loss function and using calculus to

minimize the loss) that the Fed will always choose

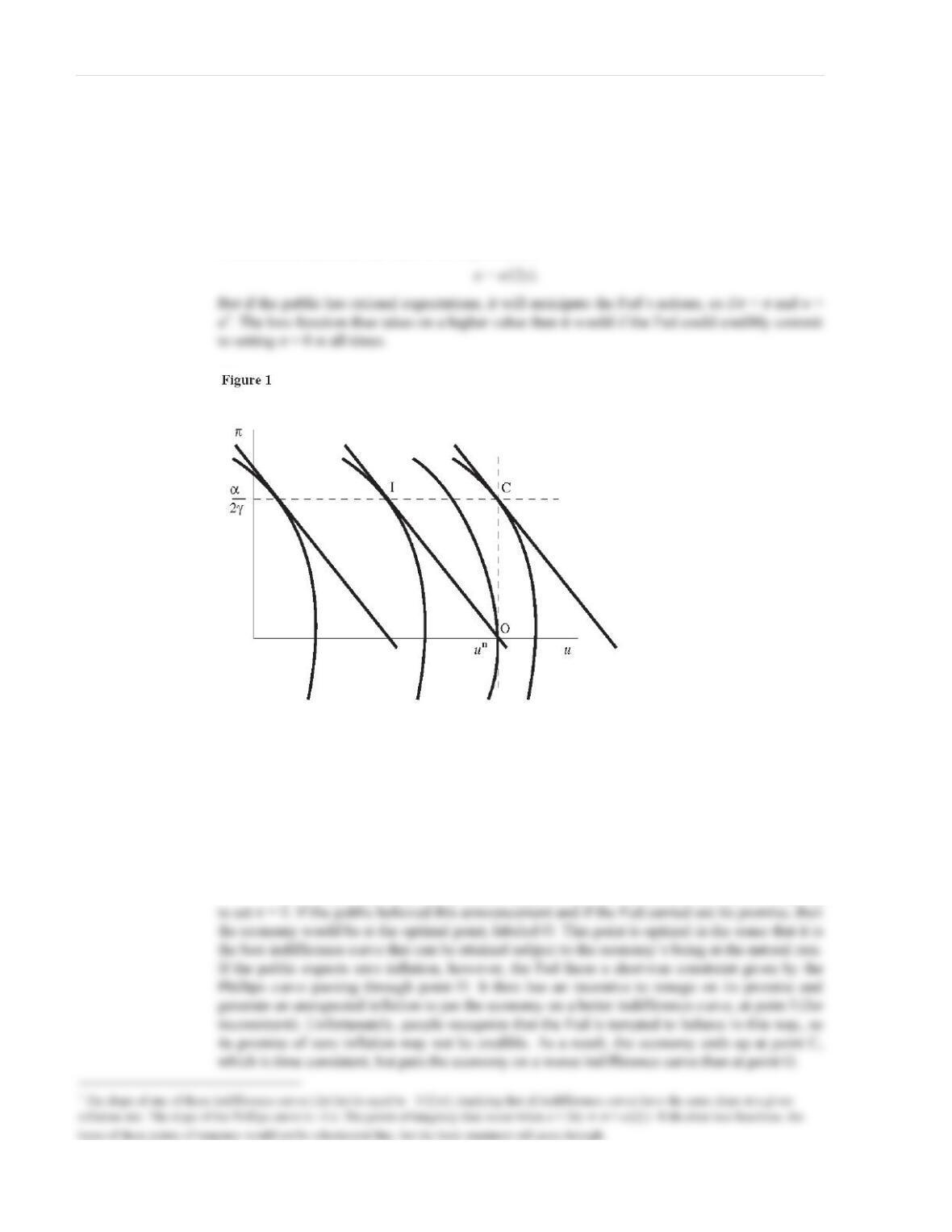

Figure 1 illustrates the problem in a diagram with inflation and unemployment on the axes.

The Fed’s loss function can be illustrated using indifference curves familiar from

microeconomics: all points on a given indifference curve are equivalent as far as the Fed’s

preferences are concerned. Indifference curves further to the left are preferred. Given an

expectation of inflation, we can draw the corresponding Phillips curve (passing through the point

{un, Eπ}). The Phillips curve represents the constraint faced by the Fed, taking expected inflation

as given, and so the Fed will choose the point on the Phillips curve where it is tangent to the loss

function. For the simple loss function in the example, this point of tangency is always at π =

α/(2γ), regardless of the value of expected inflation.1

To see the time–inconsistency problem, suppose that the Fed announced that it was going

433

ADVANCED TOPIC

18–1 Menu Costs, Imperfect Competition, and the Welfare–Improving

Effects of Policy

The presence of menu costs in the situation where firms set prices in imperfectly competitive markets

provides scope for monetary policy to have large effects on economic welfare. This framework thus gives

some support to an active role for policy in stabilizing the economy.

The essential insight of menu costs is disarmingly simple—so much so that it is quite surprising that it

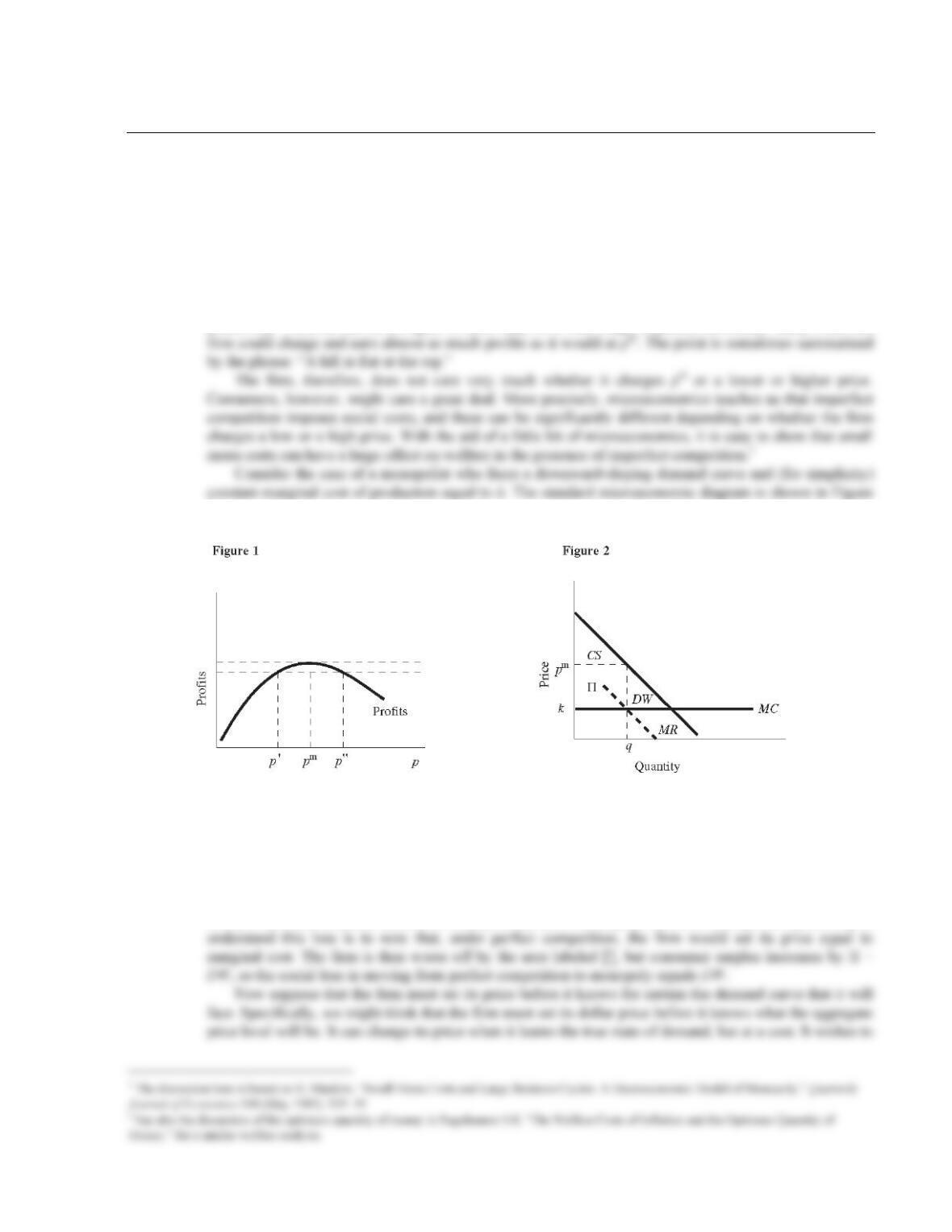

was noted only very recently. Consider a price–setting firm that wants to maximize its profits. We can

graph its profits against the price it charges as shown in Figure 1. The price that maximizes the firm’s

profits is pm. But, as shown in Figure 1, there may be a wide range of prices, between p’ and p”, that the

2.

The firm sets its price (pm) where marginal revenue (MR) equals marginal cost (MC) and produces the

quantity q. The area under the demand curve and above the marginal cost curve can be divided into three

areas. The firm earns profits (∏) equal to pm – k on every unit. (These profits are sometimes referred to as

producer surplus.) The area above the price and below the demand curve (labeled CS) is consumer

surplus—it represents the difference between the amount consumers would be willing to pay and the

amount they actually pay and so is a measure of the gain of consumers.22 The final area is the deadweight

loss (DW), which measures the cost to society of the firm’s monopoly behavior. Perhaps the easiest way to

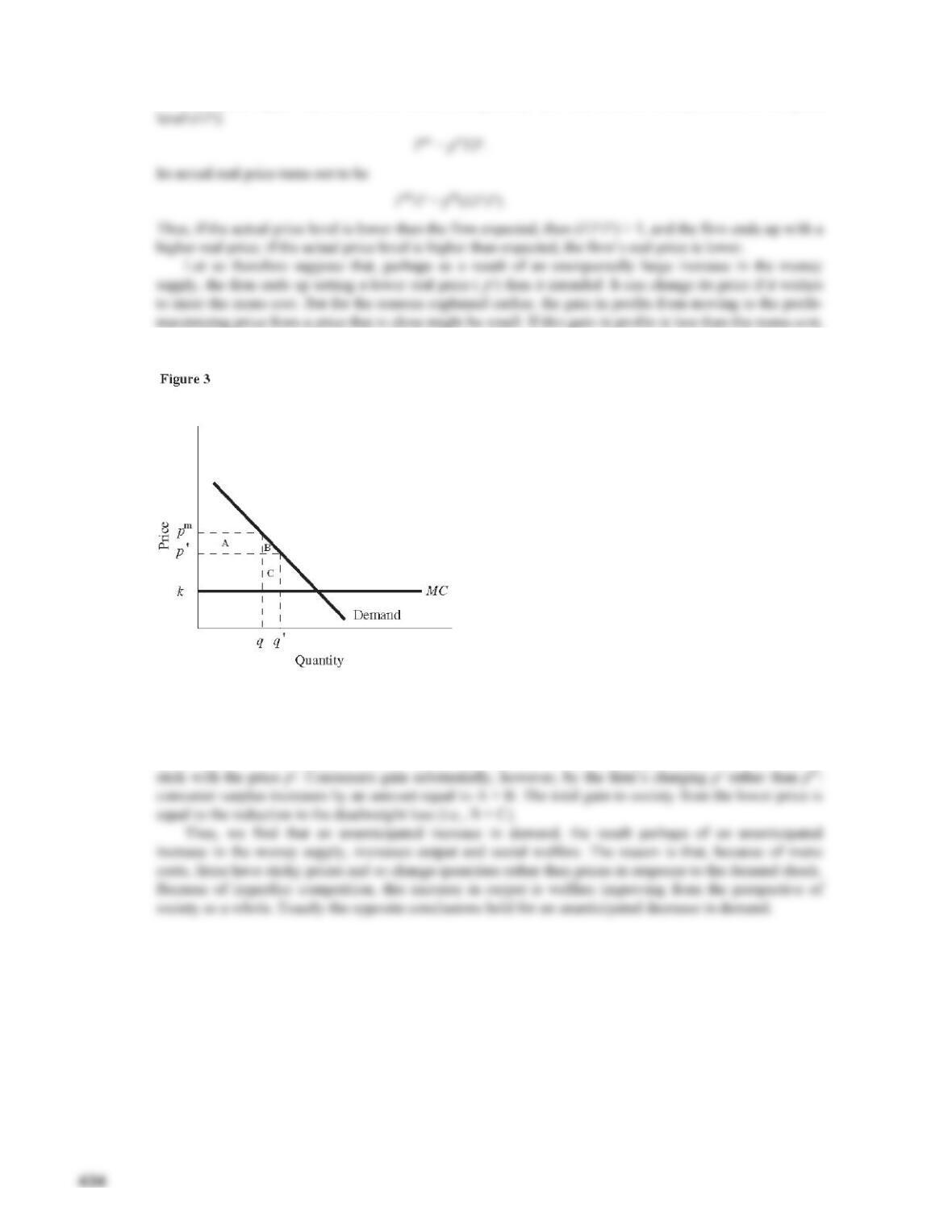

set a real price equal to pm and so sets a nominal price (Pm) on the basis of its expectation of the price

the firm will not bother to change its price. This is shown in Figure 3.

The firm’s loss in profits from charging the price p’ rather than the optimal price pm is equal to (A –

C) (in other words, if it changed its real price, it would lose an amount equal to the area C and gain an

amount equal to the area A). As Figure 3 shows, this may be a small difference (this is because a hill is flat

at the top). If A – C is smaller than the menu cost associated with changing prices, the firm will elect to

435

ADDITIONAL CASE STUDY

18–2 Profit Sharing as an Automatic Stabilizer

Economists often propose policies to improve the automatic–stabilizing powers of the economy. The

economist Martin Weitzman has made one of the most intriguing suggestions: profit sharing. Today, most

labor contracts specify a fixed wage.1 For example, General Motors might pay assembly–line workers $20

an hour. Weitzman recommends that the workers’ total pay should depend on their firm’s profits. A profit–

sharing contract for General Motors might pay workers $10 for each hour of work, but in addition the

workers would divide among themselves a share of the firm’s profit.

Weitzman argues that profit sharing would act as an automatic stabilizer. Under the current wage

system, a fall in demand for a firm’s product causes the firm to lay off workers: it is no longer profitable to

employ them at the old wage. The firm will rehire these workers only if the wage falls or if demand

recovers. Under a profit–sharing system, Weitzman argues, firms would be more likely to maintain

employment after a fall in demand. Under our hypothetical profit–sharing contract with General Motors,

for example, an additional hour of work would cost the firm only $10; the rest of the compensation for

additional workers would come from the workers’ share of profits. Because the marginal cost of labor

would be so much lower under profit sharing, a fall in demand would not normally cause a firm to lay off

workers.

A second argument for profit sharing is that it may make wages more flexible. Under profit sharing,

wages will fall with profits in recessions and rise with profits in booms. Thus firms might be more willing

to retain workers in recession, rather than laying them off. If wage rigidity is a cause of cyclical

unemployment, profit sharing might therefore be desirable. Many economists are uncomfortable with this

argument, however, because it simply takes wage rigidity as exogenously given.3 Without an explanation

of why wages are rigid, we cannot be confident that the introduction of profit sharing would really make

wages more flexible. For example, suppose that wages are rigid because of the power of insider workers.

Such workers would be likely to oppose the introduction of profit sharing.

Weitzman’s argument for profit sharing is more subtle than either of these and is often misunderstood.

He contends that under profit sharing, firms are less likely to lay workers off in recessions because firms

possess excess demand for labor. Under profit sharing, increases in employment reduce profits per worker

and so reduce compensation. Weitzman thus argues that the marginal product of labor will exceed its

marginal cost and firms will always hire all available workers. Contracts with profit sharing, according to

Weitzman, will lead to less employment fluctuation than contracts that specify fixed wages, and so

policies should be enacted to encourage profit sharing.

437

ADDITIONAL CASE STUDY

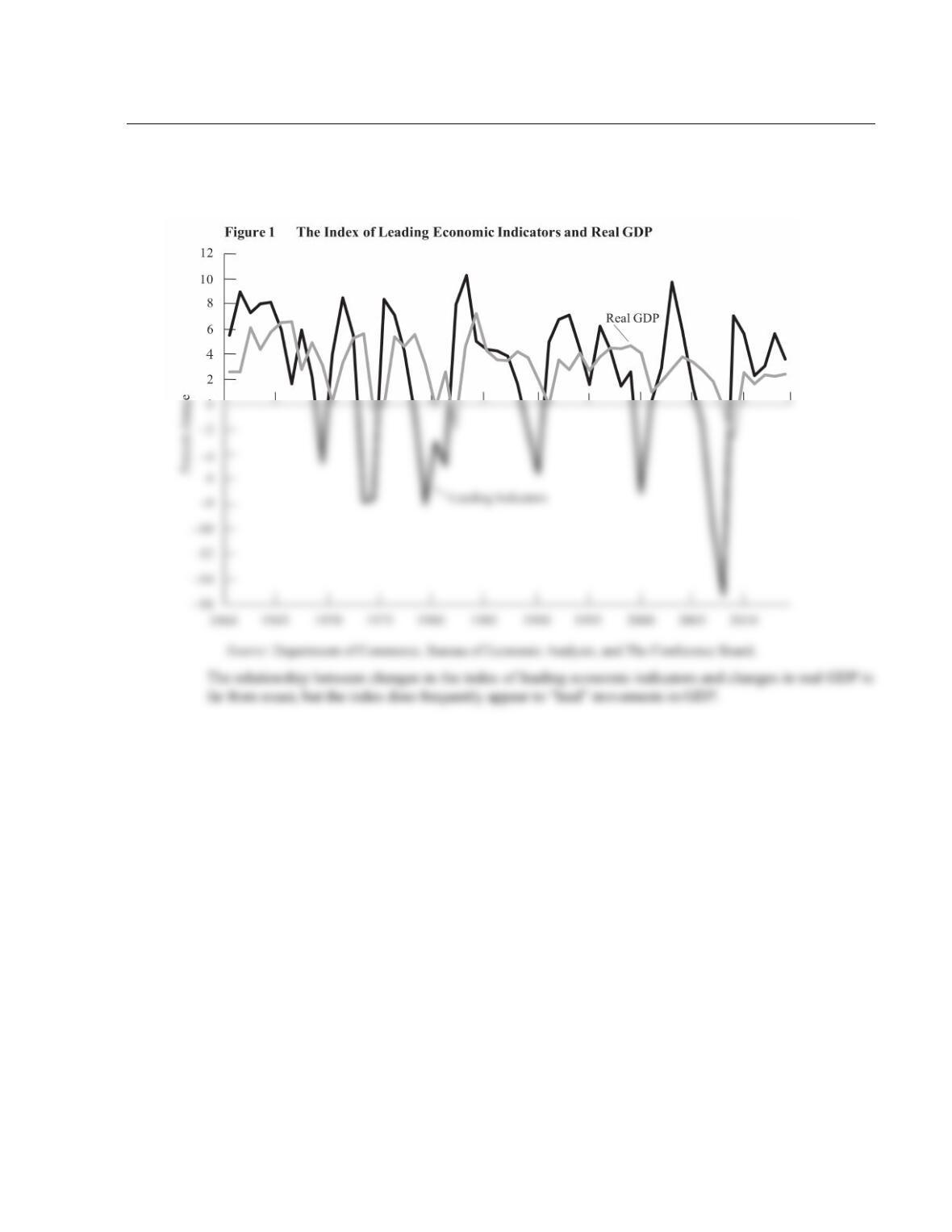

18-3 Leading Indicators in Action

Figure 1 shows the percentage change in real GDP and the percentage change in the index of leading

economic indicators for the period 1960–2014.

CASE STUDY EXTENSION

18–4 The Pitfalls of Forecasting

The case study in Chapter 18 documents some of the difficulties of economic forecasting. Making

economic forecasts is a good way to look foolish. For example, the following statements are from the

eminent economist Irving Fisher.1