Factors That Shift the IS Curve

The following exogenous factors lead to a shift in the IS curve. For each bullet, the first

example is an increase in demand, as illustrated in Figure 18–9.

■ Government purchases:

↑ ⇒ D shifts up ⇒ ↑ Y for a given i and E ⇒ IS shifts right/up

■ Taxes:

↓ ⇒ ↑ C(Y − ) ⇒ D shifts up ⇒ ↑ Y

■ Foreign interest rate or expected future exchange rate: i* or Ee

↑ i* or ↑ Ee ⇒ ↑ FR ⇒ ↑ E ⇒ D shifts up ⇒ IS shifts right/up

These changes can be summarized by expressing the IS curve as a function:

Summing Up the IS Curve

The IS curve is downward-sloping because a decrease in the interest rate leads to an

increase in investment demand and the trade balance, which increases the demand for

goods and therefore output in the short run.

4 Money Market Equilibrium: Deriving the LM Curve

The money and assets market was modeled in earlier chapters. The LM curve is based on

Money Market Recap

We continue to work with the short-run model in which the price level is fixed.

Real money demand (MD) varies inversely with the nominal interest rate, so the demand

for real money balances is downward-sloping. The real money supply is assumed to be

completely determined by the central bank. Since the price level is fixed, the central bank

also controls the real money supply.

Deriving the LM Curve

Figure 18-10 illustrates how we can use the money market to derive the LM curve. Note

that the money market and the LM diagram share a vertical axis (the interest rate), so

they can be aligned horizontally. In this way, we ensure that the interest rate in both

diagrams is the same.

Factors That Shift the LM Curve

We focus most of our attention on the real money supply. A change in the real money

supply is the main exogenous variable that shifts the LM curve. Figure 18-11 shows how

an increase in real money supply leads to a rightward shift in the LM curve.

Real money supply: M/

These changes can be summarized through expressing the LM curve as a function:

In general, any shock that increases interest rates for a given level of output (e. g., a given

L) will shift the LM curve to the left; any shock that decreases interest rates will shift the

LM curve to the right.

Summing Up the LM Curve

The LM curve is upward–sloping because an increase in output leads to an increase in

real money demand, which increases the nominal interest rate in the short run. Similarly,

5 The Short–Run IS‒LM‒FX Model of an Open Economy

We can now combine the IS‒LM diagram with the FX market diagram to study how

changes in the economy affect key macroeconomic variables, such as interest rates and

Macroeconomic Policies in the Short Run

We focus on two main policy actions:

■ Monetary policy is any change in the nominal money supply implemented by the

central bank with the objective of influencing some aspect of the macroeconomy.

The effects of these policies depend critically on the nation’s exchange rate regime.

Assumptions:

■ The economy is initially at long-run equilibrium (full employment, expected

Temporary Policies, Unchanged Expectations Remember that to examine temporary

shocks to the economy, we assume investors do not change exchange rate expectations.

We make this assumption to study how temporary policies (designed to affect output in

the short run) affect the economy.

Monetary Policy Under Floating Exchange Rates

■ Monetary expansion (shown in Figure 18-13):

↑ M/ ⇒ ↑ MS ⇒ ↓ i for a given Y ⇒ LM shifts right ⇒ DR shifts down

■ Direct effect:

↓ i ⇒ ↑ I ⇒ ↑ Y

■ Indirect effects:

Note that a monetary expansion leads to an exchange rate depreciation and a decrease

in the interest rate: both of these imply an increase output.

■ Monetary contraction: LM shifts left ⇒ DR shifts up. Effects: ↑ i, ↓ Y, ↓ E ⇒ ↓ I,

Monetary Policy Under Fixed Exchange Rates

Monetary expansion (shown in Figure 18-14):

↑ M/ ⇒ ↑ MS ⇒ LM shifts right ⇒ DR shifts

Fiscal Policy Under Floating Exchange Rates

■ Fiscal expansion (increase in G; shown in Figure 18-15):

↑ G ⇒ ↑ D ⇒ IS shifts right ⇒ DR shifts up

Note that an increase in government spending (or a decrease in taxes) leads to an

increase in output. However, the increase in output that comes from the increase in

■ Fiscal contraction (decrease in G): IS shifts left ⇒ DR shifts down.

■ Comparison with the closed economy: In the closed economy, there would be no

Note that we can also study fiscal policy in terms of taxes.

■ Fiscal expansion (tax cut): ↓ T ⇒ ↑ C ⇒ ↑ IS shifts right ⇒ DR shifts up.

■ Fiscal contraction (tax increase): ↑ T ⇒ ↓ C: IS shifts left ⇒ DR shifts down.

Fiscal Policy Under Fixed Exchange Rates

It is important to note that under a fixed exchange rate regime, the real money supply

must be adjusted to ensure the nominal exchange rate remains fixed. This means that any

fiscal policy action will be paired with a change in the money supply.

■ Fiscal expansion (increase in G; shown in Figure 18-16):

■ Direct effects:

↑ G ⇒ ↑ Y

■ Indirect effects:

↑ Y ⇒ ↑ C, ↓ TB (increase in output reduces the trade balance)

■ Note that in this case, monetary policy amplifies the effects of fiscal policy

through eliminating crowding out (because interest rates must remain unchanged

■ Fiscal contraction (decrease in G):

↓ G ⇒ ↓ D ⇒ IS shifts left ⇒ DR shifts down

Summary

The effects of monetary and fiscal expansion in floating and fixed exchange rate regimes

are summarized in the table. We can see that it is not possible to have autonomous

monetary policy in a fixed exchange rate regime. However, autonomous fiscal policy is

possible in a fixed exchange rate regime.

6 Stabilization Policy

Stabilization policy refers to monetary and fiscal policies designed to keep output at or

near full employment level. If the economy experiences an adverse shock, fiscal policy

can increase demand through shifting the IS curve to the right, or monetary policy can

Problems in Policy Design and Implementation

Although the model provides policy makers with a relatively straightforward way to

Policy Constraints Policy makers may not have the freedom to implement stabilization

policies. For example, fixed exchange rates or other “rules” for policy may limit their

Incomplete Information and the Inside Lag The model assumes that policy makers can

observe the state of the economy in real time. In practice, they observe macroeconomic

data with a lag. The lag between the timing of the shock and the policy action is known

Policy Response and the Outside Lag Even with perfect information on the economy, it

may take time for an implemented policy to have real economic effects. This is known as

Long–Horizon Plans If households and businesses making decisions about consumption

and investment plan over long horizons, they may be less responsive to policy changes.

Weak Links from the Nominal Exchange Rate to the Real Exchange Rate The model

assumes that changes in nominal exchange rates translate into changes in the real

Pegged Currency Blocs Some countries use a combination of fixed and floating

exchange rates to limit one country from boosting export demand through a real effective

Weak Links from the Real Exchange Rate to the Trade Balance The model assumes

that changes in the real exchange rate imply changes in the trade balance. In practice, the

link between the two may be weak because of transactions costs. The existence of these

APPLICATION

Macroeconomic Policies in the Liquidity Trap

The financial crisis and recession of 2008–2009 provided yet another lesson in the

limitations of monetary policy. The IS curve for most developed economies shifted very

far to the left. This was caused by the extreme risk aversion of banks around the world,

which reduced their lending by unimaginable amounts. The Fed lowered its target for

interest rates to zero in December 2008, leaving no room for more stimulus using

conventional monetary policies.

In fact, the economy was an excess reserves trap. The table below shows reserve

positions as of October 2010:

Excess reserves

$973,504,000,000

No matter how you measure it, the LM curve was effectively identical to the

horizontal axis of the IS‒LM diagram. This is the zero lower bound (ZLB) problem.

Under this situation, fiscal policy is the only tool that can be used to stimulate the

The fiscal stimulus in the United States took two forms. First were the automatic

stabilizers, changes in government spending and taxes that automatically move in

countercyclical directions. The second was the American Recovery and Reinvestment

And, of course, temporary tax cuts never have the multiplier impact of permanent tax

Required reserves

Total reserves

7 Conclusions

This chapter builds a short-run macroeconomic model for the open economy. The trade

balance implies an additional source of demand for goods and services. Changes in

relative prices and nominal exchange rates allow for expenditure switching between

countries.

Appendix 1: The Marshall‒Lerner Condition

This appendix considers the assumption that a depreciation leads to an increase in the

trade balance. For simplicity, assume TB = 0; therefore, EX = IM.

η

:

For the foreign country:

Note that EX* = IM, from the home country’s perspective.

Home imports (in units of home output) = IM(q)

These expressions must be equal:

The real exchange rate converts foreign exports into home country output (recall q = ratio

of home to foreign basket of goods).

In percentage changes, assuming a 1% real depreciation in the home country:

From the previous expression, we see there are two effects of a depreciation. Foreigners

export a lower volume of more expensive goods measured in foreign output units

(volume effect = −

η

*%), but these goods cost more in terms of home output (price effect

This expression is known as the Marshall‒Lerner condition. The trade balance will

increase following a depreciation only if trade volume changes are sufficiently large (e.g.,

they are sufficiently elastic) to offset the price effects.

Appendix 2: Multilateral Real Exchange Rates

This appendix extends the model to more than two countries. Here, we assume there are

N countries in the world. We can then examine macroeconomic consequences in terms of

the real effective exchange rates.

Consider the effects of a small change in the exchange rate. For country 1, the

changes in exports and imports are expressed as

Note that this expression holds for each individual country. Adding up the change in the

trade balances for each individual country gives us

Teaching Tips

Teaching Tip 1: (This is related to the Application: Macroeconomic Policies in the

Liquidity Trap.) As the application notes, once monetary policy reaches the zero lower

bound, it is up to fiscal policy to stimulate the economy. The fiscal stimulus was the

American Recovery and Reinvestment Act (ARRA), signed by President Obama on

February 17, 2009. ARRA included $580 billion in government spending and $212

Teaching Tip 2: (Also related to the Application: Macroeconomic Policies in the

Liquidity Trap.) The textbook uses Keynes’s term “liquidity trap” to describe the state

of the U.S. economy in 2009. In fact, a more correct description would be “excess

reserves trap.” The table below shows banks’ reserve positions with the Fed as of

October 2010. Why were banks holding such large stocks of excess reserves? Have your

class discuss that question. (The discussion should not take more than five minutes.)

IN–CLASS PROBLEMS

1. This question will compare the policies of the federal government and the Federal

Reserve and their likely effects on interest rates, exchange rates, output, and the trade

balance during the mid– to late 1970s.

a. President Lyndon Johnson and Congress passed large increases in government

spending to finance Great Society programs and the Vietnam War. Explain briefly

how such spending affects the trade balance.

Answer: A fiscal expansion leads to an increase in interest rates and an

b. Beginning in the mid-1970s, Federal Reserve Chairman Arthur Burns sought to

lower unemployment below its full employment level by decreasing interest rates.

Does this require a monetary expansion or contraction?

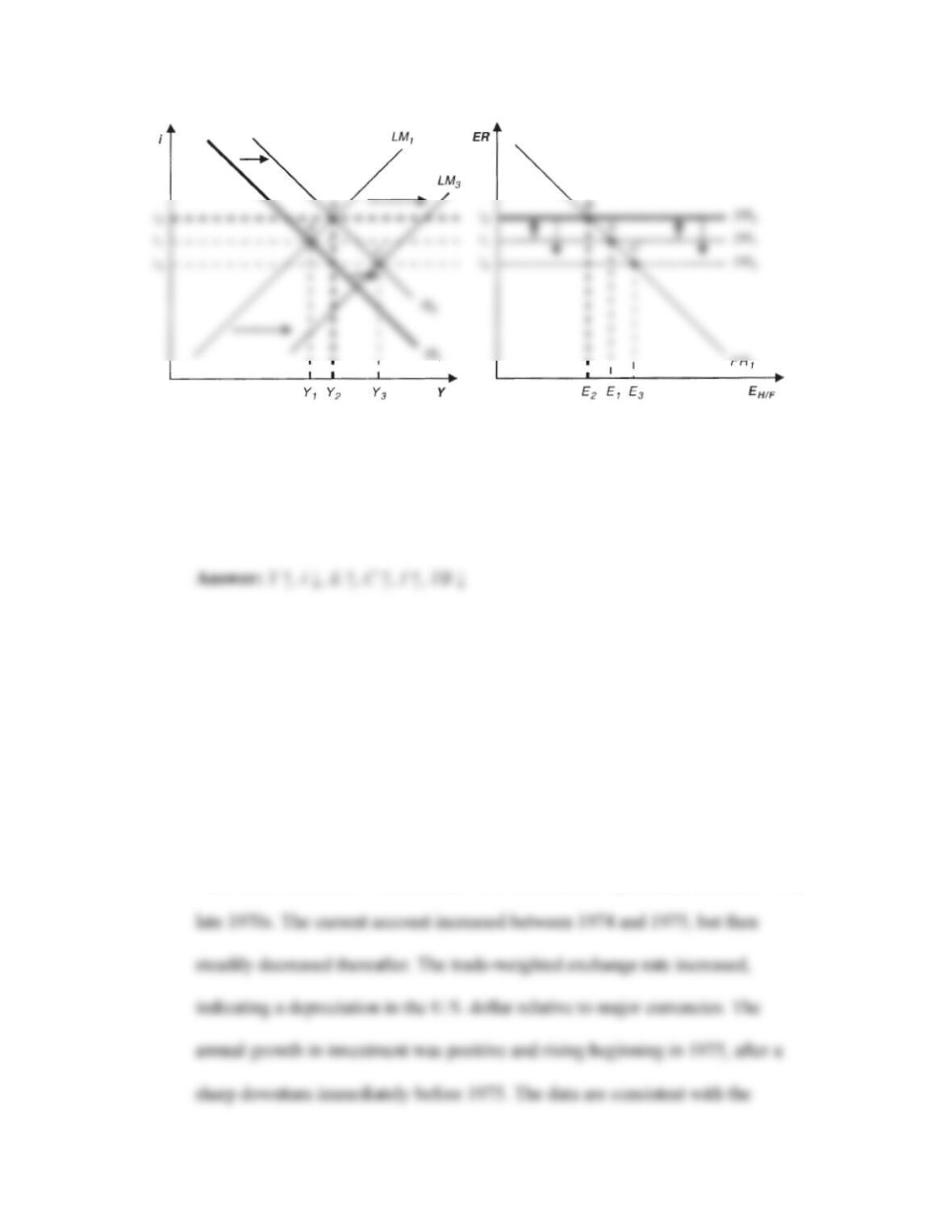

c. Illustrate the effects of the fiscal and monetary policies mentioned previously

using the IS‒LM‒FX market diagram. [Note the change in interest rates observed

in (b).]

Answer: See the following diagram. Because interest rates fell in the mid-1970s,

d. State the effects of these policies on the following variables: output, interest rate,

nominal exchange rate, consumption, investment, and the trade balance.

e. Go to the Federal Reserve Economics Database (FRED). Here, you can look at

graphs of the following variables (1975–78): effective federal funds rate (interest

rate), the effective exchange rate (against major currencies), current account, and

gross private investment (% change from one year ago). Based on these figures,

are the data consistent with the model in this case? Which variables, if any, do not

behave according to the model during this period?

Answer: The effective federal funds rate declined, then gradually increased in the