CHAPTER 17

Money, Banking, and Inflation

KEY IDEAS IN THIS CHAPTER

2. Commodity money or fiat money can overcome the double-coincidence-of-needs

problem by providing a universally acceptable medium of exchange.

3. The monetary intertemporal model predicts that a higher growth rate of money

4. In this model, an optimal long-run monetary policy for the central bank is to follow

5. The Diamond-Dybvig banking model has two equilibria: a no bank run equilibrium

7. However, there is a moral hazard problem associated with deposit insurance.

8. According to the too-big-to-fall doctrine, the implicit insurance of deposits and other

NEW IN THE FOURTH EDITION

2. All charts and tables have been updated to reflect new data.

TEACHING GOALS

In the modern world, the use of money as a social contrivance is largely taken for

granted. Although study of the mechanisms of trading may seem rather arcane, it may

Chapter 17: Money, Banking, and Inflation

open some students’ minds to the value of adopting a uniform medium of exchange.

Students should fully understand that a world of rugged individualism in which everyone

is self-sufficient is the most likely alternative to a monetary economy.

The level of the money supply is neutral. The growth rate of the money supply has

allocative effects on the economy. Continuous growth in the money supply causes

inflation. Inflation erodes money’s usefulness as a medium of exchange. As inflation

worsens, households substitute non-market activities, which require no money, for market

activities that do require money. Therefore, as the inflation rate increases, output and

employment decrease.

CLASSROOM DISCUSSION TOPICS

An important tenet of monetary economics is the dominance of monetary economies over

economies without a commonly accepted medium of exchange. Yet we still find the

existence of barter clubs. These clubs sometimes arrange direct one-for-one trades

between individuals or businesses that have a double coincidence of wants. Sometimes

they arrange three-way transactions similar to those depicted in Figure 15.2 in the text.

Some of these clubs utilize credits that circulate as a private medium of exchange

between members. To find some examples, suggest a Google™ search on the term

“barter.” Ask if any student has heard of such arrangements or even participated in them.

Are the users of these services irrational? Does the existence of such organizations

suggest that monetary exchange is becoming outdated?

The widespread use of computer technology has lowered the information costs associated

with barter exchange. But such technology also reduces the cost of engaging in monetary

transactions. Marketing materials provided by these exchanges emphasize that they allow

Instructor’s Manual for Macroeconomics, Fourth Canadian Edition

transactions. It is not likely that the foundations of monetary theory will become outdated

in the near future.

Most of today’s students have not had any personal experience with significant inflation.

Ask students if they ever worry about inflation. There may be students from other

countries (Russia, Eastern Europe, the former Yugoslavia, etc.) who have experienced

high inflation. Can anyone imagine a set of circumstances that would lead to a serious

Canadian inflation problem? Would students find more inflation objectionable? Do the

problems that students ascribe to inflation conform to theory, or are they more a figment

of confusion between real and nominal variables?

The Diamond-Dybvig model provides a useful framework for generating discussion

about financial stability, particularly in light of the recent financial crisis. In the United

States, some observers likened the freezing-up of credit markets, in particular the

reluctance of lenders to lend short-term to some investment banks, as being like a bank

OUTLINE

1. Alternative Forms of Money

a) Commodity Money

b) Circulating Private Bank Notes

c) Commodity-Backed Paper Money

2. Money and the Absence of a Double Coincidence of Wants

a) Barter and the Absence of a Double Coincidence of Wants

b) Commodity Money and Trade

c) Fiat Money and Trade

3. A Growing Money Supply and the Effects of Long-Run Inflation

a) Inflation Effects

CC

(2) Current Leisure-Consumption Choice: ,1

lC

w

MRS

R

=

+

b) A Change in the Growth Rate of the Money Supply

i) Output and Employment Effects

c) Money Growth, Inflation, and Output Growth Across Countries (Macroeconomics

in Action 15.2)

d) Should the Bank of Canada Reduce the Inflation Rate to Zero or Less?

4. Financial Intermediation and Banking

a) Properties of Assets

i) Rate of Return

ii) Risk

(1) Diversifiable

(2) Non-Diversifiable

iii) Maturity

iv) Liquidity

b) Financial Intermediation

i) Characteristics

(2) Diversified

(4) Information Processing

ii) Types of Financial Institutions

(2) Mutual Funds

(3) Depository Institutions

iii) Problems with Direct Lending

(1) Costly Matching

(3) Duplication in Credit Risk Evaluation

(5) Loans are Illiquid

5. The Diamond-Dybvig Model

a) Interrupted Production Processes

6. Deposit Insurance

a) Bank Failures in the Great Depression

b) Moral Hazard

c) Too-Big-to-Fail Policy

TEXTBOOK QUESTION SOLUTIONS

Problems

1. In this case, Type I traders would use the commodity money they produce (good 2) to

2. Consumes 1 Consumes 2 Consumes 3

Type I Type II Type III

Produces 3 Produces 1 Produces 2

3. Suppose that the central bank acquires K units of capital in the current period, and

issues M units of money to finance these purchases, so that

MK

P

=. (1)

Then, in the future period, the central bank earns rK from its holdings of capital, and

‘

and solving, we obtain

Chapter 17: Money, Banking, and Inflation

4. The fact that inflation alters the real opportunity cost of holding money is the only

source of real effects of inflation on the economy. Payment of interest on money

5. With the possibility of theft, the Friedman rule is no longer an optimal policy. In this

case, the nominal interest rate does not reflect the social cost of holding money, and it

6. Asset characteristics.

i) Works of art typically have a low (financial) rate of return. The only source of a

return is appreciation in the market price. Works of art are quite risky and are

ii) U.S. Treasury Bills have a low rate of return in comparison to other financial

iii) Shares in Microsoft have a high expected rate of return, although they are rather

risky, due to fluctuations in price and dividends. The maturity is effectively

iv) Loans to friends generally have a low rate of return as friends generally charge

Instructor’s Manual for Macroeconomics, Fourth Canadian Edition

v) Loans to General Motors likely have a rate of return in excess of Treasury Bills,

7. If the bank can suspend convertibility in this way, then it can always honour all of its

second-period commitments. Early consumers never wait to withdraw in the second

8. Production cannot be interrupted.

a) In the standard model, with no bank, the consumer has no reason not to commit

all of her resources to production. If the consumer turns out to be an early

consumer, production is interrupted and the consumer has 11c=. If the consumer

turns out to be a late consumer, production is completed and the consumer

has 21cr=+. In no case does the consumer consume less than one.

When production cannot be interrupted, the decision of how much to commit to

production becomes important. As long as the good is storable, the consumer can

choose to refrain from production, in which case she obtains 12

1cc==. Now

Chapter 17: Money, Banking, and Inflation

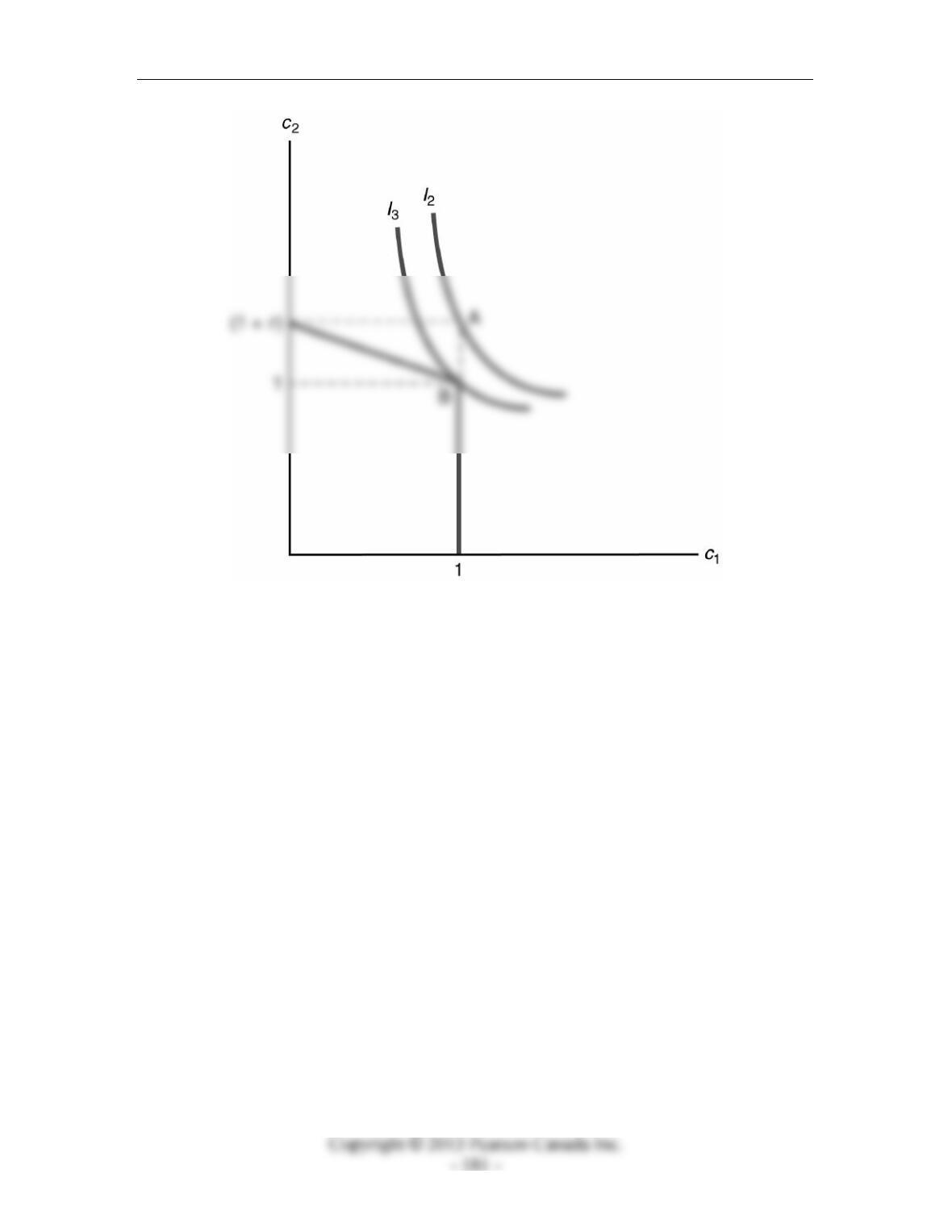

Figure 15.1a

Instructor’s Manual for Macroeconomics, Fourth Canadian Edition

b) As long as banks know the probability of individuals becoming early and late

consumers, the need to commit irreversibly to production does not affect the bank.

Precommitment does not matter when the bank knows in advance how much it

would need to interrupt. Therefore, the optimal bank contract is unchanged. This

possibility is added to Figure 15.1b, below. The optimal bank contract is the

point **

12

,cc.

Figure 15.1b

9. Each consumer will invest their entire endowment of 1 unit in the production

technology in period 0. In period 1, if an early consumer must choose the fraction of

the investment, x, to sell at the price p, and will interrupt the remaining fraction 1 – x

and consume it. The early consumer then chooses x to maximize pxx +−1, and the

solution is x = 0 if p < 1, x = 1 if p > 1, and the consumer is otherwise indifferent. In

period 1, a late consumer chooses y, the fraction of investment to interrupt, to

10. Moral hazard problems.

a) The child is more likely to report having trouble because having trouble is

rewarded with help.