1

2

3

15

16

17

18

29

30

A B C D E F G H I J K L M N O P Q

17 Chapter model 12/12/2018

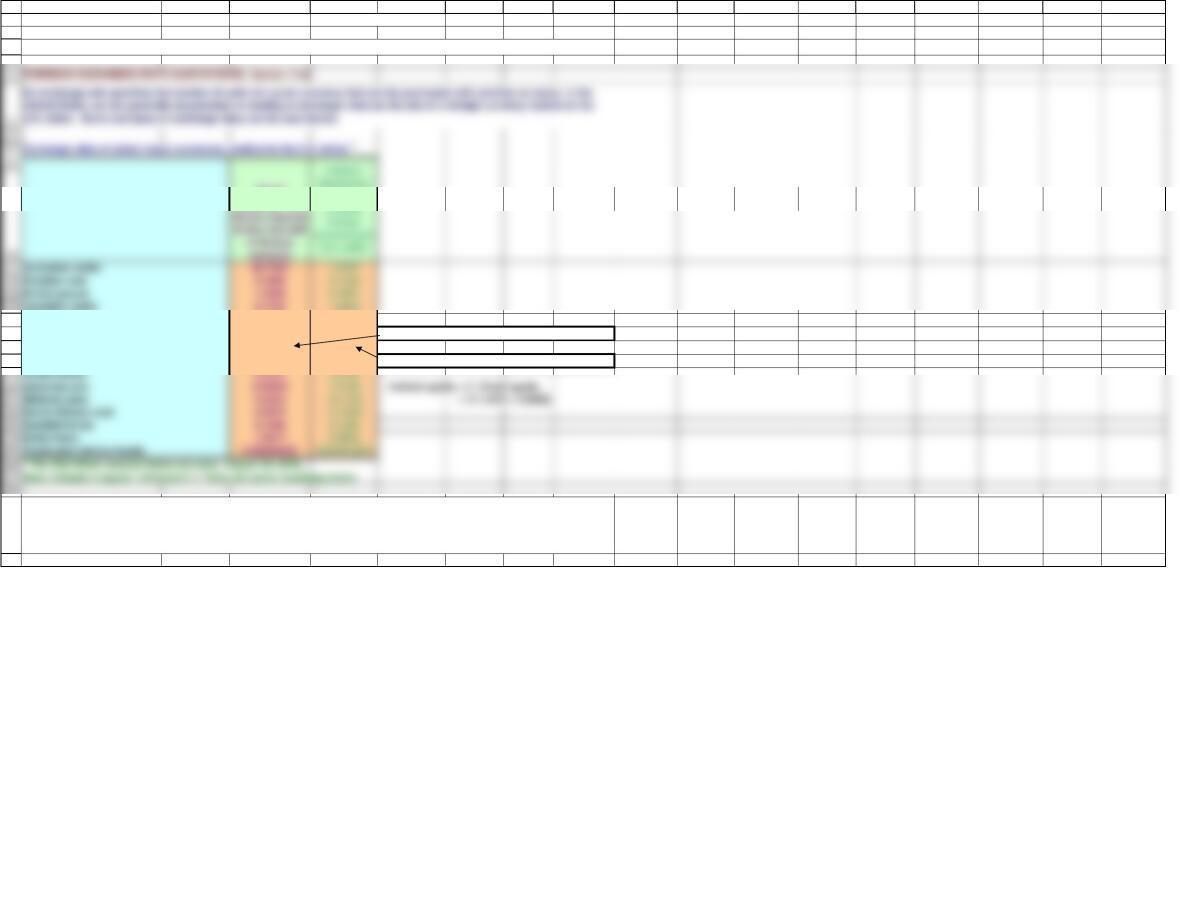

Chinese yuan 0.1461 6.8448

Danish krone 0.1565 6.3889 Direct quote: 1 euro will buy 1.1670 dollars.

EMU euro 1.1670 0.8569

Hungarian forint 0.00357015 280.10 Indirect quote: 1 dollar will buy 0.8569 euro.

Notice that the exchange rates were quoted in two ways (direct and indirect). A direct quotation tells you how many U.S.

dollars can be purchased per one unit of the foreign currency. The indirect quotation tells you how many units of foreign

currency can be purchased per one U.S. dollar. These values are merely inverses of each other.

Chapter 17. Multinational Financial Management

Direct

Quotation: U.S.

Number of

31

32

33

34

35

37

38

39

40

41

42

49

50

51

52

53

A B C D E F G H I J K L M N O P Q

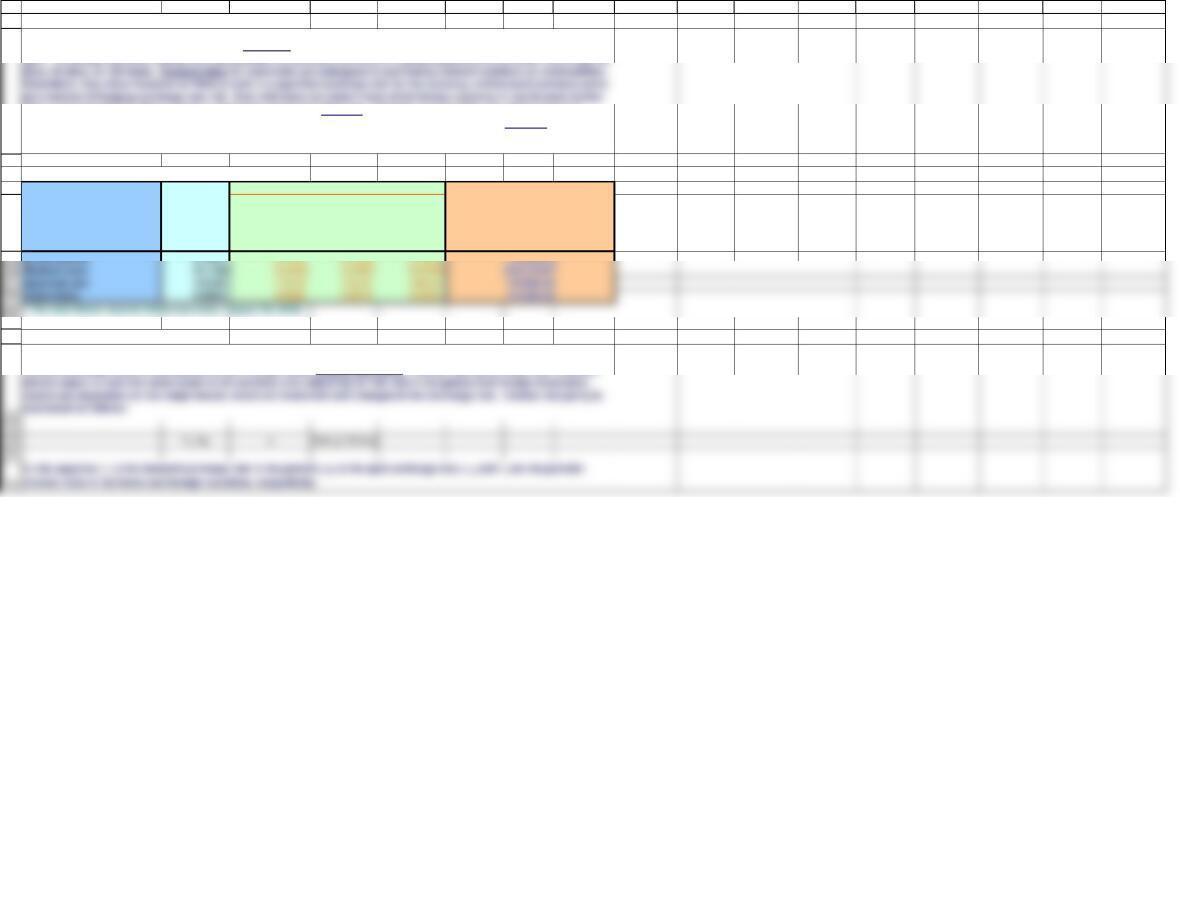

CROSS RATES

Cross rate of Swiss francs per British pound =

( Swiss francs/British pounds )

Key Currency Cross-Exchange Rates

U.S. Venezuelan Swiss Swedish So African Mexican Japanese Israeli Hungarian European Danish Chinese Canadian British Brazil Australian

Dollar Bolivar Fuerte Franc Krona Rand Peso Yen Shekel Forint Euro Krone Yuan Dollar Pound Real Dollar

Australian dollar 1.3767 0.00000554 1.4203 0.1509 0.0935 0.0720 0.0124 0.3809 0.0049 1.6066 0.2154 0.2011 1.0603 1.7909 0.3316 1

Hungarian forint 280.10 0.00112758 288.9795 30.6990 19.0188 14.6492 2.5237 77.5037 1326.8770 43.8357 40.9227 215.7332 364.3824 67.4762 203.4648

Israeli shekel 3.6140 0.00001455 3.7286 0.3961 0.2454 0.1890 0.0326 10.0129 4.2176 0.5656 0.5280 2.7835 4.7015 0.8706 2.6252

Japanese yen 110.99 0.00044679 114.5061 12.1643 7.5361 5.8047 130.7103 0.3962 129.5228 17.3696 16.2153 85.4828 144.3840 26.7370 80.6215

Mexican peso 19.1205 0.00007697 19.7266 2.0956 1.2983 10.1723 5.2906 0.0683 22.3136 2.9924 2.7935 14.7266 24.8738 4.6061 13.8891

South African rand 14.7275 0.00005929 15.1944 1.6141 10.7703 0.1327 4.0751 0.0526 17.1870 2.3049 2.1517 11.3432 19.1591 3.5479 10.6981

indicate that a currency‘s cross rate with itself is 1.0.

A cross rate allows you to express the value of one country’s currency relative to a currency other than the U.S. dollar.

Calculating cross rates does, however, involve using the U.S. dollar exchange rates of those currencies. For instance, to

calculate the cross rate between Swiss francs and British pounds, we will use their U.S. dollar exchange rates. Initially, let

Once we have established what we are looking for, we can now determine how to get there. As mentioned in the text, most

exchange rates are stated indirectly (except for the British pound). For this reason, it will be easier to generate this

construction using indirect quotations. If we take the indirect quotation of Swiss francs and divide it by the indirect

quotation of British pounds, we will see:

59

60

61

62

63

64

70

71

A B C D E F G H I J K L M N O P Q

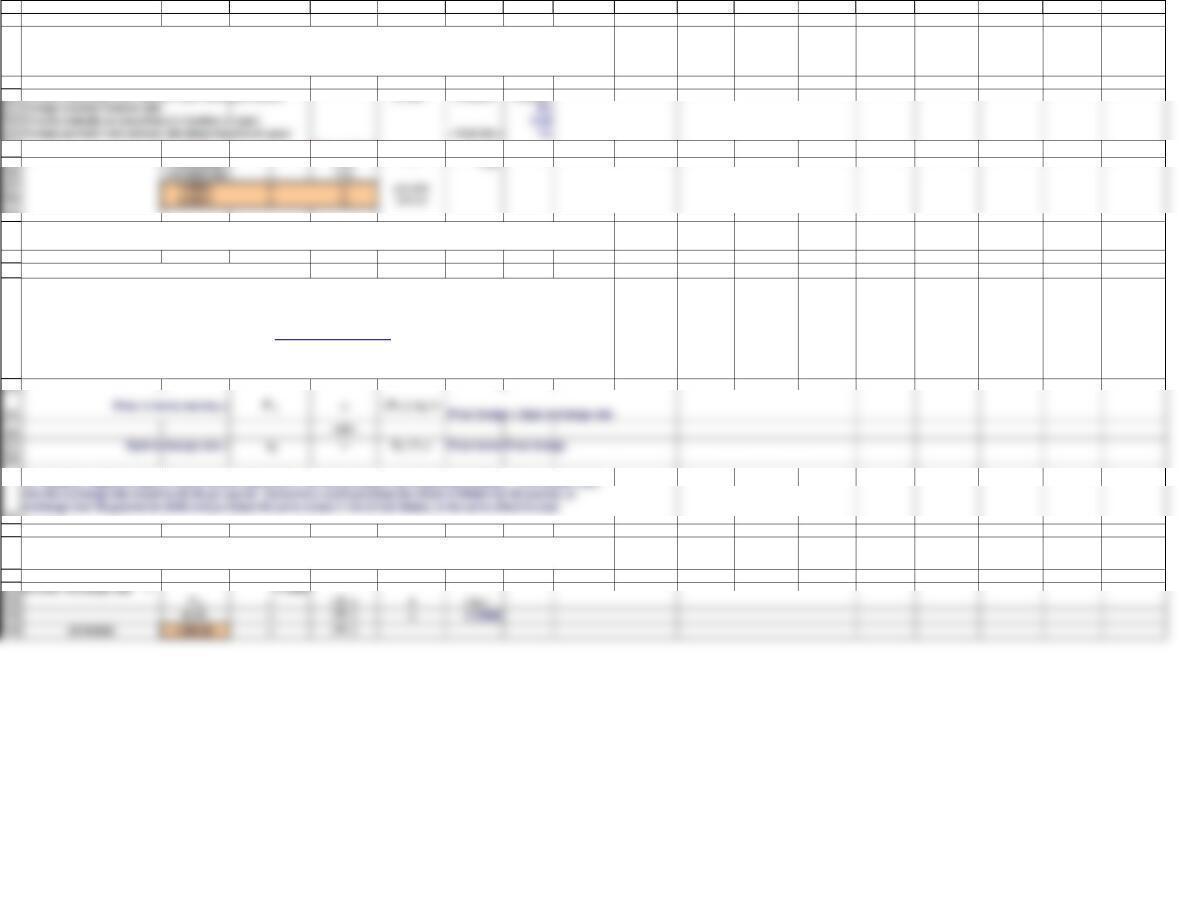

TRADING IN FOREIGN EXCHANGE (Section 17-5)

Selected spot and forward rates (in indirect notation)a

Indirect

Spot Rate:

units $1 will

buy

30 days 90 days 180 days

INTEREST RATE PARITY (Section 17-6)

Forward rate: more $ later, spot

rate at a discount, less $ later, at a

premium

Market forces determine whether a currency sells at a forward premium or discount, and the relationship between spot and

forward exchange rates is summarized by the concept called interest rate parity. Interest rate parity holds that investors

Forward Rates

The exchange rates discussed thus far are all spot rates, which means the rate paid for delivery of the currency “on the

spot.” In foreign currency trading, it is also possible to purchase currency at a predetermined price at some future date (30

than in the spot market, that currency is said to be selling at a discount. Likewise, if an investor can obtain more of a

foreign currency in the spot market than in the forward market, the currency is said to be selling at a premium. Below are

some examples of spot and forward rates for selected major currencies.

77

78

79

80

84

85

87

89

90

91

92

93

94

99

100

101

102

A B C D E F G H I J K L M N O P Q

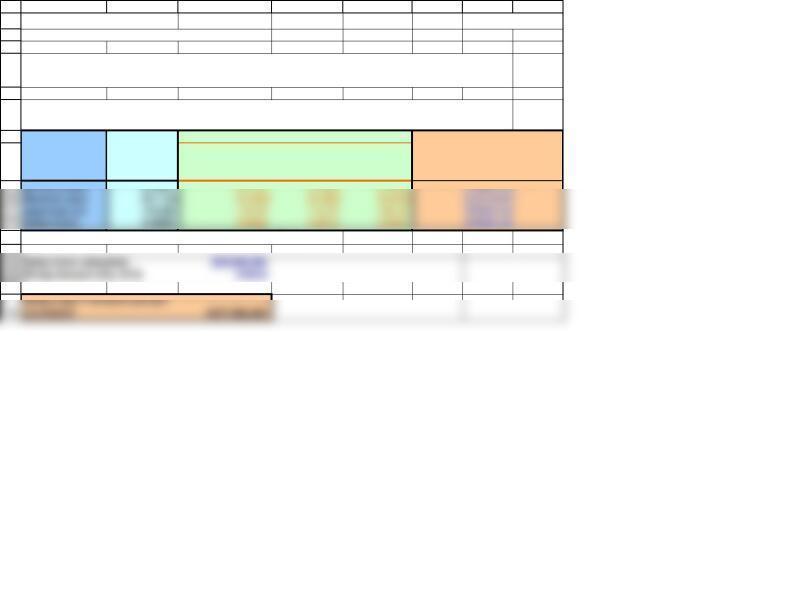

EXAMPLE

Spot exchange rate: dollars 1 yen will buy now =1/B67 =1/96.02 0.00901

Forward exchange rate: dollars 1 yen will buy in future =1/D67 =1/95.97 0.00907

f t / e0=(1+r h) / (1+r f)

1.006529428 = 1+rh/ 1.01

PURCHASING POWER PARITY (Section 17-7)

EXAMPLE

Price in the U.S. = $110

Having discussed the relationship between spot and future rates, we now turn to the determinants of exchange rate levels

in countries. Exchange rates are impacted by a multitude of factors, many of which are difficult to predict. However,

market forces work to ensure that similar goods sell for similar prices in different countries, adjusted for exchange rates

and transportation costs. This relationship is called purchasing power parity (also called the law of one price), and it

implies that exchange rate levels adjust so that identical goods cost the same real amount in different countries.

Purchasing power parity is illustrated by the following equation.

Suppose a certain microwave oven is selling for $110 in the United States today. What price should this same microwave

oven be selling for in Sweden if purchasing power parity holds?

From this example, we see that this investment is expected to generate a 6.638% return, denominated in dollars, consisting

of the 4% interest in yen plus the 2.638% gain because the yen will buy more dollars.

Suppose a U.S. investor buys a default-free 90-day Japanese bond that promises a 4% nominal return, denominated in yen.

Assume that the spot and forward exchange rates are those described in the previous section, i.e., indirect spot = 110.99

and forward rates as shown above.

For instance, suppose a pair of tennis shoes costs $100 in the United States, and 50 pounds in Britain. This would imply

1

2

3

4

9

10

A B C D E F G H

SECTION 17-4 12/12/2018

SOLUTIONS TO SELF-TEST QUESTIONS

4. Assume that 1 U.S. dollar can be exchanged for 105 Japanese yen or for 0.80 euro. What is the

euro/yen exchange rate?

3. Assume that today one Canadian dollar is worth 0.75 U.S. dollar. How many Canadian dollars

would you receive for 1 U.S. dollar?

1

2

3

4

5

6

7

8

13

17

18

A B C D E F G H

SECTION 17-5 12/12/2018

SOLUTIONS TO SELF-TEST QUESTIONS

Indirect

Spot Rate:

units $1 will

buy

30 days 90 days 180 days

a The Wall Street Journal (www.wsj.com), August 30, 2018.

Table 17.3 Selected Spot and Forward Exchange Rates

(Number of Units of Foreign Currency per U.S. Dollar): Monday, August 30, 2018

Forward Rates

3. Using data in Table 17.3, if a U.S. firm entered into a 90-day forward contract, how many dollars

would be required to honor the 200 million Swiss franc obligation when it is due?

Forward rate: more $ later,

spot rate at a discount, less $

later, at a premium

12

1

2

3

4

5

6

7

A B C D E F

SECTION 17-6 12/12/2018

SOLUTIONS TO SELF-TEST QUESTIONS

Canadian dollar / U.S. dollar spot rate 1.4

U.S. nominal annual rate 3.5%

3. Assume that 90-day U.S. securities have a 3.5% annualized interest rate, whereas 90-day

Canadian securities have a 4% annualized interest rate. In the spot market, 1 U.S. dollar can be

exchanged for 1.4 Canadian dollars. If interest rate parity holds, what is the 90-day forward

exchange rate between U.S. and Canadian dollars?

Canadian nominal annual rate 4.0%

U.S. dollar/Canadian dollar spot rate 0.7143

90-day U.S. rate 0.9%

90-day Canadian rate 1.0%

U.S. dollar/Canadian dollar 90-day forward rate 0.7134

1

2

3

4

5

A B C D E F G H

SECTION 17-7 12/12/2018

SOLUTIONS TO SELF-TEST QUESTIONS

2. A television set sells for 3,000 U.S. dollars. In the spot market, $1 = 111 Japanese yen. If

purchasing power parity holds, what should be the price (in yen) of the same television set in

Japan?