Chapter 17

CAPITAL BUDGETING

QUESTIONS AND ANSWERS

Q17.1 “The decision to start your own firm and go into business can be thought of as a capital

budgeting decision. You only go ahead if projected returns look attractive on a personal

and financial basis.” Discuss this statement.

Q17.1 ANSWER

The decision to start your own firm and go into business can indeed be thought of as a

capital budgeting decision. You only go for it if projected returns look attractive on a

personal and financial basis. Formally, capital budgeting is described as the process of

Q17.2 What major steps are involved in the capital budgeting process?

Q17.2 ANSWER

Conceptually, the capital budgeting process involves six logical steps. First, the cost of

the project must be determined. This is similar to finding the price that must be paid for

Capital Budgeting 533

Q17.3 OIBDA is an abbreviation for “operating income before depreciation and amortization.”

Like its predecessor EBITDA (“earnings before interest, taxes, depreciation and

amortization”), OIBDA is used to analyze profitability before non-cash charges tied to

plant and equipment investments. Can you see any advantages or disadvantages

stemming from the use of OIBDA instead of net income as a measure of investment

project attractiveness?

Q17.3 ANSWER

Because it eliminates the effects of financing and non-cash accounting decisions,

OIBDA can provide a relatively good “apples–to-apples” comparison of profitability

between companies and industries. For example, OIBDA as a percent of sales can be

Q17.4 Toyota Motor Corp., like most major multinational corporations, enjoys easy access to

world financial markets. Explain why the NPV approach is the most appropriate tool

for Toyota’s investment project selection process.

Q17.4 ANSWER

534 Chapter 17

An investment project is attractive and should be pursued so long as the discounted net

present value of cash inflows is greater than the discounted net present value of the

investment requirement, or net cash outlay. Because the attractiveness of individual

Q17.5 Level 3 Communications, Inc., like many emerging telecom carriers, has only limited

and infrequent access to domestic debt and equity markets. Explain the attractiveness of

a “benefit–cost ratio” approach in capital budgeting for Level 3, and illustrate why the

NPV, PI, and IRR capital budgeting decision rules sometimes provide different rank

orderings of investment project alternatives.

Q17.5 ANSWER

Smaller companies often have only limited and infrequent access to domestic debt and

equity markets. In such circumstances, “capital rationing” is in effect and a “benefit–

Capital Budgeting 535

Q17.6 How is a crossover discount rate calculated, and how does it affect capital budgeting

decisions?

Q17.6 ANSWER

A reversal of project rankings occurs at the crossover discount rate, where NPV is equal

for two or more investment alternatives. The ranking reversal problem is typical of

situations where investment projects differ greatly in terms of their underlying NPV

536 Chapter 17

Q17.7 An efficient firm employs inputs in such proportions that the marginal product/price

ratios for all inputs are equal. In terms of capital budgeting, this implies that the

marginal cost of debt should equal the marginal cost of equity in the optimal capital

structure. In practice, firms often issue debt at interest rates substantially below the

yield that investors require on the firm’s equity shares. Does this mean that many firms

are not operating with optimal capital structures? Explain.

Q17.7 ANSWER

No, the phenomenon of lower observed yields for debt versus equity instruments does

not imply suboptimal capital structures. The explanation lies in the less directly

Q17.8 Suppose that Black & Decker’s interest rate on newly–issued debt is 7.5% and the firm’s

marginal federal-plus-state income tax rate is 40%. This implies a 4.5% after-tax

component cost of debt. Also assume that the firm has decided to finance next year’s

projects by selling debt. Does this mean that next year’s investment projects have a

4.5% cost of capital?

Q17.8 ANSWER

The answer is no, at least not usually. In financing a particular set of projects with debt,

the firm typically uses some of its potential for obtaining further low-cost debt financing.

Q17.9 Research in financial economics concludes that stockholders of target firms in takeover

battles “win” (earn abnormal returns) and that stockholders of successful bidders do

not lose subsequent to takeovers, even though takeovers usually occur at substantial

premiums over pre-bid market prices. Is this observation consistent with capital market

efficiency?

Q17.9 ANSWER

Q17.10 “Risky projects are accepted for investment on the basis of favorable expectations

concerning profitability. In the post-audit process, they must not be unfairly criticized

for failing to meet those expectations.” Discuss this statement.

Q17.10 ANSWER

It is a simple fact that some investment projects undertaken on the basis of favorable

expectations of profit fail to work out. The purchase of automobile insurance is not a

538 Chapter 17

SELF-TEST PROBLEMS AND SOLUTIONS

ST17.1 NPV and Payback Period Analysis. Suppose that your college roommate has

approached you with an opportunity to lend $25,000 to her fledgling home healthcare

business. The business, called Home Health Care, Inc., plans to offer home infusion

therapy and monitored in-the-home healthcare services to surgery patients in the

Birmingham, Alabama, area. Funds would be used to lease a delivery vehicle, purchase

supplies, and provide working capital. Terms of the proposal are that you would receive

$5,000 at the end of each year in interest with the full $25,000 to be repaid at the end of

a ten-year period.

A. Assuming a 10% required rate of return, calculate the present value of cash flows

and the net present value of the proposed investment.

B. Based on this same interest rate assumption, calculate the cumulative cash flow of

the proposed investment for each period in both nominal and present-value terms.

C. What is the payback period in both nominal and present-value terms?

D. What is the difference between the nominal and present-value payback period?

Can the present-value payback period ever be shorter than the nominal payback

period?

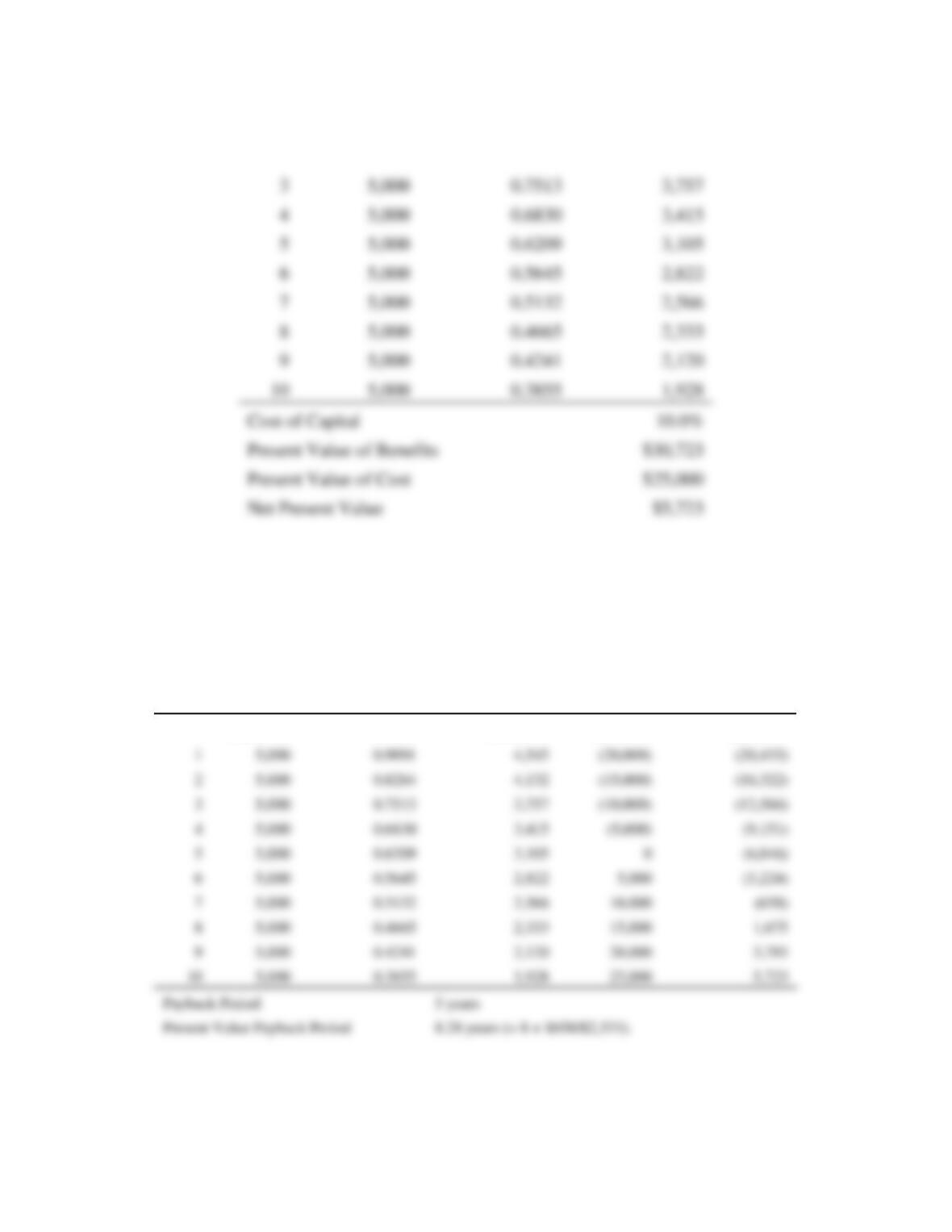

ST17.1 SOLUTION

A. The present value of cash flows and the net present value of the proposed investment can

be calculated as follows:

Year

Cash Flow

Present Value

Interest Factor

Present Value

Cash Flow

Capital Budgeting 539

B. The cumulative cash flow of the proposed investment for each period in both nominal

and present-value terms is:

Year

Cash

Flow

Present Value

Interest Factor

Present Value

Cash Flow

Cumulative

Cash Flow

Cumulative

PV Cash Flow

0

($25,000)

1.0000

($25,000)

($25,000)

($25,000)

0.6209

0.4665

540 Chapter 17

C. Based on the information provided in part B, it is clear that the cumulative cash flow in

ST17.2 Decision Rule Conflict. Bob Sponge has been retained to analyze two proposed capital

investment projects, projects X and Y, by Square Pants, Inc., a local specialty retailer.

Project X is a sophisticated working capital and inventory control system based upon a

powerful personal computer, called a system server, and PC software specifically

designed for inventory processing and control in the retailing business. Project Y is a

similarly sophisticated working capital and inventory control system based upon a

powerful personal computer and general- purpose PC software. Each project has a cost

of $10,000, and the cost of capital for both projects is 12%. The projects’ expected net

cash flows are as follows:

Expected Net Cash Flow

Year

Project X

Project Y

0

($10,000)

($10,000)

1

6,500

3,500

2

3,000

3,500

3

3,000

3,500

4

1,000

3,500

A. Calculate each project’s nominal payback period, net present value (NPV),

internal rate of return (IRR), and profitability index (PI).

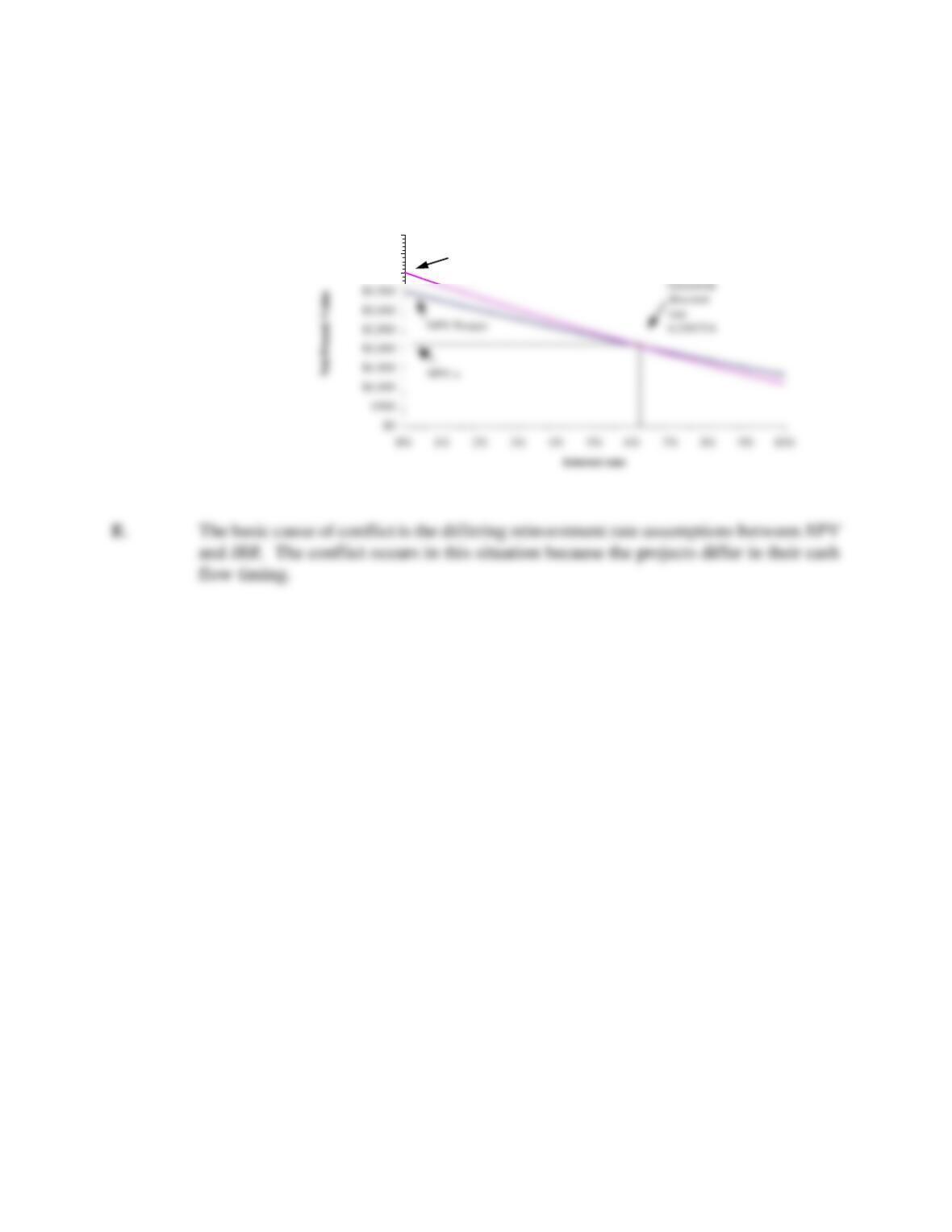

Capital Budgeting 541

(Hint: Plot the NPV profiles for each project to find the crossover discount rate

k.)

E. Why does a conflict exist between NPV and IRR rankings?

ST17.2 SOLUTION

A. Payback:

To determine the nominal payback period, construct the cumulative cash flows for

each project:

Cumulative Cash Flow

Year

Project X

Project Y

Internal Rate of Return (IRR):

B. Using all methods, project X is preferred over project Y. Because both projects are

D. To determine the effects of changing the cost of capital, plot the NPV profiles of each

Then find the IRR of Project Δ:

544 Chapter 17

Square Pants Crossover Rate

$4,000

$4,500

$5,000

NPV Project Y

PROBLEMS AND SOLUTIONS

P17.1 Cost of Capital. Identify each of the following statements as true or false, and explain

your answers.

A. Information costs both increase the marginal cost of capital and reduce the

internal rate of return on investment projects.

B. Depreciation expenses involve no direct cash outlay and can be safely ignored in

investment-project evaluation.

C. The marginal cost of capital will be less elastic for larger firms than for smaller

firms.

D. In practice, the component costs of debt and equity are jointly rather than

independently determined.

E. Investments necessary to replace worn-out or damaged equipment tend to have

low levels of risk.

P17.1 SOLUTION

Capital Budgeting 545

A. True. The need to gather information concerning the creditworthiness of borrowers

increases the interest rates charged by creditors. Similarly, the task of information

P17.2 Decision Rule Criteria. The net present value (NPV), profitability index (PI), and

internal rate of return (IRR) methods are often employed in project valuation. Identify

each of the following statements as true or false, and explain your answers.

A. The IRR method can tend to understate the relative attractiveness of superior

investment projects when the opportunity cost of cash flows is below the IRR.

B. A PI = 1 describes a project with an NPV = 0.

C. Selection solely according to the NPV criterion will tend to favor larger rather

than smaller investment projects.

D. When NPV = 0, the IRR exceeds the cost of capital.

E. Use of the PI criterion is especially appropriate for larger firms with easy access

to capital markets.

P17.2 SOLUTION

A. False. The IRR method implicitly assumes reinvestment of net cash flows during the life

of the project at the IRR and will overstate the relative attractiveness of superior

546 Chapter 17

P17.3 Cost of Capital. Indicate whether each of the following would increase or decrease the

cost of capital that should be used by the firm in investment project evaluation. Explain.

A. Interest rates rise because the Federal Reserve System tightens the money supply.

B. The stock market suffers a sharp decline, as does the company’s stock price,

without (in management’s opinion) any decline in the company’s earnings

potential.

C. The company’s home state eliminates the corporate income tax in an effort to keep

or attract valued employers.

D. In an effort to reduce the federal deficit, Congress raises corporate income tax

rates.

E. A merger with a leading competitor increases the company’s stock price

substantially.

P17.3 SOLUTION

A. Increase. A general rise in interest rates will increase the cost of debt, and increase the

weighted average cost of capital used in investment project evaluation.

Capital Budgeting 547

Of course, average state tax rates are fairly modest compared with federal tax

rates, and the effect of changing state tax rates on the weighted average cost of capital

can be expected to be similarly modest. Still, on balance and holding all else equal, we

would expect the weighted average cost of capital to be marginally less for firms

headquartered in Florida (a no tax state) versus Wisconsin (a relatively high tax state).

P17.4 Present Value. New York City licenses taxicabs in two classes: (1) for operation by

companies with fleets and (2) for operation by independent driver-owners having only

one cab. Strict limits are imposed on the number of taxicabs by restricting the number

of licenses, or medallions, that are issued to provide service on the streets of New York

City. This medallion system dates from a Depression-era city law designed to address

an overabundance of taxis that depressed driver earnings and congested city streets. In

1937, the city slapped a moratorium on the issuance of new taxicab licenses. The

number of cabs, which peaked at 21,000 in 1931, fell from 13,500 in 1937 to 11,787 in

May 1996, when the city broke a 59-year cap and issued an additional 400 licenses.

However, because the city has failed to allow sufficient expansion, taxicab medallions

have developed a trading value in the open market. After decades of often-explosive

medallion price increases, fleet license prices rose to $600,000 in 2007.

A. Discuss the factors determining the value of a license. To make your answer

B. What factors would determine whether a change in the fare fixed by the city would

raise or lower the value of a medallion?

548 Chapter 17

C. Cab drivers, whether hired by companies or as owners of their own cabs, seem

unanimous in opposing any increase in the number of cabs licensed. They argue

that an increase in the number of cabs would increase competition for customers

and drive down what they regard as an already unduly low return to drivers. Is

their economic analysis correct? Who would gain and who would lose from an

expansion in the number of licenses issued at a nominal fee?

P17.4 SOLUTION

A. The price of a medallion will be determined by the above-normal or economic profits

B. The effect of fare changes on medallion values depends on the price elasticity of demand

P17.5 NPV and PI. Suppose the Pacific Princess luxury cruise line is contemplating leasing

an additional cruise ship to expand service from the Hawaiian Islands to Long Beach or

San Diego. A financial analysis by staff personnel resulted in the following projections

for a five-year planning horizon:

Long Beach

San Diego

Cost

$2,000,000

$3,000,00

PV of expected cash flow @ k = 15%

2,500,000

3,600,000

Capital Budgeting 549

A. Calculate the net present value for each service. Which is more desirable

according to the NPV criterion?

P17.5 SOLUTION

A. Long Beach

San Diego

B. Long Beach