Chapter 17

Exchange Rates and International Economic Policy

◼ Chapter Outline, Overview, and Teaching Tips

Chapter Outline

Foreign Exchange Market and Exchange Rates

Foreign Exchange Rates

The Distinction Between Real and Nominal Exchange Rates

Macroeconomics in the News: Foreign Exchange Rates

Exchange Rates in the Long Run

Law of One Price

Theory of Purchasing Power Parity

Exchange Rates in the Short Run

Supply Curve for Domestic Assets

Application: The Global Financial Crisis and the Dollar

Application: Why Are Exchange Rates So Volatile?

Exchange Rates and Aggregate Demand and Supply Analysis

Intervention in the Foreign Exchange Market

Foreign Exchange Intervention

Intervention and the Exchange Rate

Fixed Exchange Rate Regimes

Fixed Exchange Rate Regime Dynamics

Chapter 17 Exchange Rates and International Economic Policy 191

Chapter 17 Web Appendix: The Interest Parity Condition

Chapter 17 Web Appendix: Speculative Attacks and Foreign Exchange Crises

Chapter Overview and Teaching Tips

Chapter 17 discusses policy issues related to the exchange rate and the international economy. This

chapter is self-contained, and for instructors who have less of an international orientation to their courses,

this chapter can be skipped without loss of continuity. The chapter focuses on three basic questions: How

do swings in the exchange rate affect economic activity? What determines fluctuations in the exchange

rate? How do fluctuations in exchange rate affect macroeconomic policy?

Chapter 17 explains behavior in the foreign exchange market by using a modern asset-market approach to

exchange rate determination. This asset-market approach is now the dominant method of analyzing

The asset-market approach is developed in several steps. First, the long-run determinants of the exchange

rate are laid out, and then the information about the long-run determinants is embedded in a model of the

short-run determination of exchange rates. The key idea that must be transmitted to the student is that the

demand for domestic currency (say, dollar) assets is determined by the relative expected return on these

assets. To help students achieve an intuitive grasp of how the relative expected return on domestic assets,

and hence the demand curve shifts, tell them to put themselves in the shoes of an investor who is thinking

about putting his or her money into foreign or domestic assets. When a factor changes, have them ask

themselves whether at the same exchange rate, they would earn a higher expected return on domestic

assets—if so, the demand curve has shifted to the right. This kind of thinking will help them manipulate

the demand curve, so they can predict which way the exchange rate changes.

The rest of the chapter shows how international financial transactions have important implications for the

conduct of monetary policy. It explains how foreign exchange market intervention affects the exchange

rate, a country’s international reserves, liquidity in the economy, and interest rates. It also explains how

192 Mishkin • Macroeconomics: Policy and Practice, Second Edition

of students because huge profits were made during these crises and because government intervention in the

markets was massive. These applications also give students further practice with the model of the foreign

exchange market developed in Chapter 17.

◼ Answers to End of Chapter Review Questions and Problems

Answers to Review Questions

Foreign Exchange Market and Exchange Rates

1. Currencies and bank deposits denominated in particular currencies are traded in the foreign exchange

market. These transactions determine foreign exchange rates—the price of one currency in terms of

2. The nominal exchange rate tells you how many euros you can buy with your dollars. The real

exchange rate tells you how cheap or expensive U.S. goods and services are relative to European

goods and services. Because of sticky prices in the short run, nominal and real exchange rates move

Exchange Rates in the Long Run

3. The law of one price says that if two countries produce an identical good and transportation costs and

trade barriers are low, the price of the good should be identical in both countries, no matter which

currency is used to pay for it. This means that the real exchange rate will be 1.0, and the nominal

the goods and services they produce are not traded with other countries.

Exchange Rates in the Short Run

4. If the foreign exchange rate Et is above its equilibrium value E*, there is excess supply of dollar

assets in the foreign exchange market. More people want to sell dollar assets than want to buy them,

Chapter 17 Exchange Rates and International Economic Policy 193

and the value of the dollar falls. As it does so, the expected appreciation of the dollar relative to its

expected future value Eet+1 rises, which increases the expected return on holding dollar assets,

Analysis of Changes in Exchange Rates

5. The exchange rate for a currency will rise if the domestic real interest rate increases, if the foreign

Aggregate Demand and Supply Analysis of Exchange Rate Effects

6. Because appreciation of the domestic currency increases the real as well as the nominal exchange rate

in the short run, it makes exports more expensive and imports less expensive. This causes net exports

Intervention in the Foreign Exchange Market

7. Central banks intervene in foreign exchange markets to adjust their holdings of international reserves

(foreign-currency denominated assets), influence exchange rates, or both. When a central bank buys

assets denominated in the domestic currency, it is selling some of its foreign-currency denominated

Fixed Exchange Rate Regimes

8. In a fixed exchange rate regime, the value of one currency is pegged to another currency (called the

anchor currency), and central banks intervene in foreign exchange markets to keep the exchange rate

9. A currency is overvalued relative to another currency if the fixed exchange rate (par value of the

currency) is higher than the equilibrium exchange rate between the two currencies in the foreign

exchange market. To keep the exchange rate from falling to the equilibrium value, the central bank

194 Mishkin • Macroeconomics: Policy and Practice, Second Edition

10. The policy trilemma is the reality that a country or monetary union cannot simultaneously have free

To Peg or Not to Peg

11. Exchange-rate pegging helps keep inflation low and anchors inflation expectations in the pegging

country to those in the anchor country. It replaces the pegging country’s monetary policy, which may

not have done a good job in the past of stabilizing the economy, with that of the anchor country.

Answers to Problems

Foreign Exchange Market and Exchange Rates

1. a. The real exchange rate is: (16 0.75)/10 = 1.2, which means that U.S. wine is more expensive

that French wine (i.e., the real exchange rate is higher than 1).

Exchange Rates in the Long Run

2. a. For the law of one price to hold, the nominal exchange rate should be 5 yuan per dollar, so that

an individual holding $2 can buy the same coffee priced at 10 yuan in China.

3. a. In the case of sugar, trade restrictions prevent the law of one price from holding. The United

States imposes significant trade restrictions, mostly in the form of quotas. This makes sugar more

expensive in the United States. This is an example of a tradable good, but subject to

transportation costs and trade restrictions, both of which do not allow the law of one price to

Chapter 17 Exchange Rates and International Economic Policy 195

Analysis of Changes in Exchange Rates

4. a. An expected reduction in the size of asset purchases would lead to an increase in expected future

interest rates, which would increase the demand for dollar denominated assets, and hence an

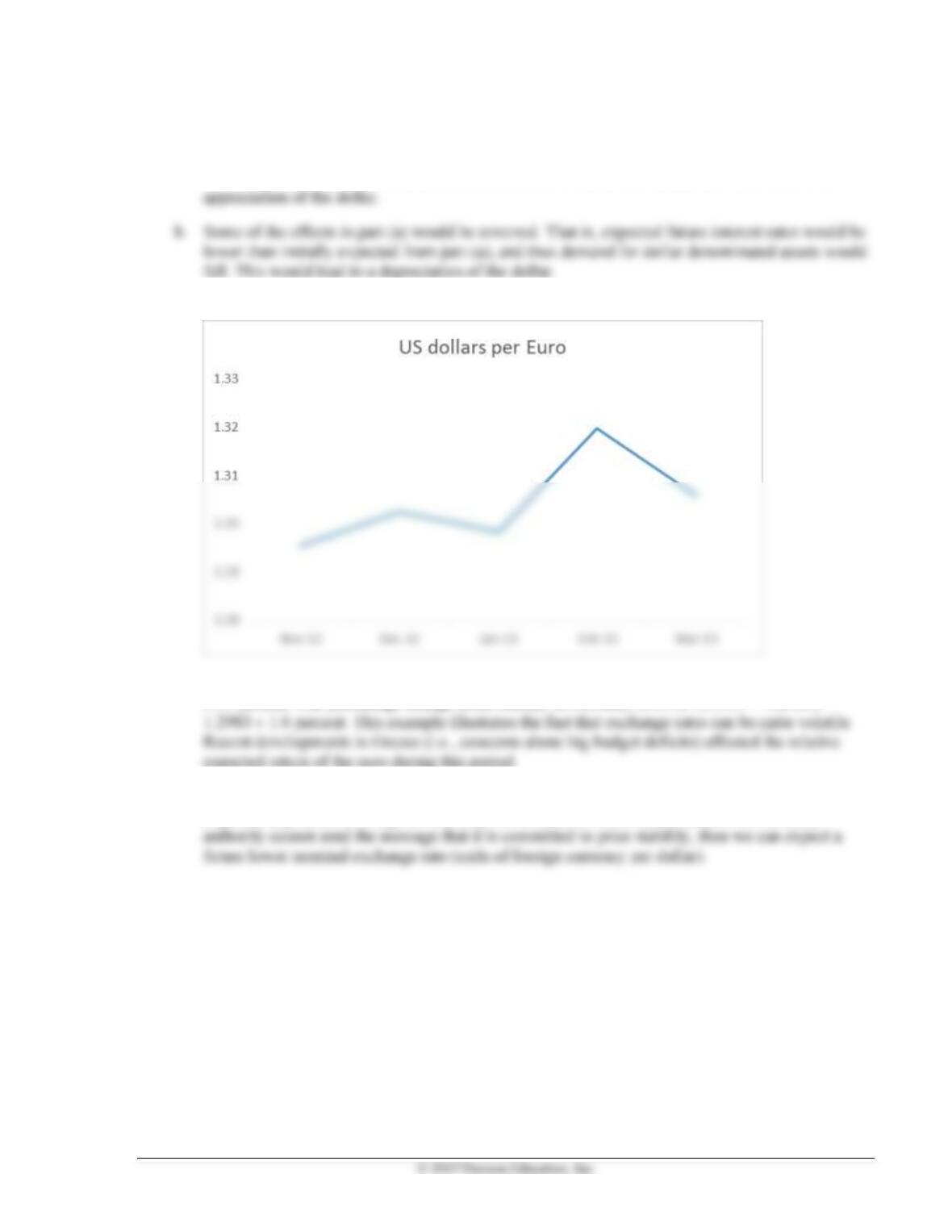

5. a.

b. The percentage change from November to December 2012 is: (1.3095–1.2953) / 1.2953 =

0.55 percent. The percentage change from January to February 2013 is: (1.3197 – 1.2983) /

expected return of the euro during this period.

6. a. According to the purchasing power parity theory, high expected inflation rates result in an

expected depreciation of a given currency. In the case of the United States, if its monetary

196 Mishkin • Macroeconomics: Policy and Practice, Second Edition

b. A future lower value of the nominal exchange rate decreases the relative expected return of U.S.

dollar-denominated assets. Graphically, the demand curve shifts to the left and the spot exchange

rate decreases. Intuitively, if investors expect the dollar to depreciate in the future, they will not

be as willing to hold U.S. dollar-denominated assets today.

Aggregate Demand and Supply Analysis of the Effects of Exchange Rates

7. a. An increase in Brazilian net exports will result in an inflow of foreign currency. If the central

bank of Brazil does not want to accumulate foreign assets, it will sell them and get Brazilian reals

in exchange. This reduces Brazil’s money supply and increases domestic interest rates.

minimize the effect of the foreign currency inflow on Brazil’s exchange rate.

Intervention in the Foreign Exchange Market

8. a. The Federal Reserve exchanged U.S. dollars for foreign assets (i.e., the Fed bought foreign assets

and paid for them with U.S. dollars). As a consequence, the Fed now holds more foreign assets,

intervention.

Fixed Exchange Rate Regimes

9. Even if a central bank adheres to a floating exchange rate regime (i.e., to allow its currency to

respond to supply and demand conditions in the foreign exchange market), it might still have

incentives to intervene in the foreign exchange market. An excessive appreciation of its currency will

hurt that country’s exports, as exports will become more expensive in terms of the foreign currency.

Chapter 17 Exchange Rates and International Economic Policy 197

To Peg or Not to Peg

10. a. An increase in the interest rate of the anchor country results in an overvaluation of the pegging

currency. In addition to fears of a speculative attack, an overvalued currency reduces net exports

by making exports more expensive. Importing firms will benefit from a stronger currency, and

◼ Answers to Data Analysis Problems

1. a. See table below for August 2, 2012 and 2013.

b. The euro (EUR) and Chinese yuan appreciated against the dollar. The yen (JPY), Canadian dollar

(CAD), and British pound (GBP) depreciated against the dollar. Thus, you would expect exports

2. a. The exchange rate for August 2, 2013 was $1.5277/£ or 0.6546£/$. The real exchange rate is then

[(0.6546£/$) × ($23,495/Boston mini )]/[£17,865/London mini] = 0.86 London mini/Boston

mini.

3. a See table below for data from August 2, 2012 and 2013.

b. The British LIBOR rate decreased against the dollar LIBOR rate, thus you would expect the

British pound to depreciate relative to the dollar. The euro and yen LIBOR rates both increased

relative to the dollar LIBOR rate; thus, you would expect the euro and yen to appreciate relative

to the dollar.

198 Mishkin • Macroeconomics: Policy and Practice, Second Edition

c. See table below. The interest rate differentials would have predicted that the British pound would

Date

USD per

GBP

USD per

EUR

JPY per

USD

2012-08-02

1.5500

1.2149

78.22

2013-08-02

1.5277

1.3268

99.04

GBP

depreciated

EUR

appreciated

JPY

depreciated

dollar

10.95%

4. a. See table below for July 2008 to July 2013.

b. See table below. The Chinese yuan has a much smaller band that it moves in relative to the

average value; at only 11 percent of the average, this is three to four times smaller than the

◼ Answers to Review Questions and Problems in Web Appendix,

“The Interest Parity Condition”

1. The interest parity condition holds that the domestic interest rate equals the foreign interest rate

minus the expected appreciation of the domestic currency. If capital is mobile and domestic and

2. a The expected return of dollar assets in terms of Japanese yen would be 4 percent higher than the

interest rate paid by the dollar-denominated asset. In addition to the 2 percent earned in dollars,

an investor will earn 4 percent due to the appreciation of the dollar. The expected return of

3. As long as the interest rate on the domestic asset is lower than the interest rate on the foreign asset,

the interest parity condition implies an expected appreciation of the domestic currency. This happens

4. Rumors about a future depreciation of the domestic currency lower the expected appreciation of the

domestic currency by (everything else the same) lowering the value of the expected future exchange

rate (foreign currency per domestic currency). This results in an increase in the righthand side of the

5. According to the interest parity condition, the dollar is expected to depreciate by 1 percent: 4% = 3%

6. According to the interest parity condition, if a government decides to peg the value of its currency to

◼ Answers to Review Questions and Problems in Web Appendix,

“Speculative Attacks and Foreign Exchange Crises”

1. Speculators attack a currency when they believe it is overvalued and that the government is near to

exhausting its international reserves or its willingness to use them to continue intervening in the

200 Mishkin • Macroeconomics: Policy and Practice, Second Edition

2. The countries in the ERM faced difficulties when the German Bundesbank sharply increased interest

rates to deal with the jump in inflation that accompanied German reunification in the early 1990s

because they would have to raise their interest rates also to keep the exchange rates for their

3. If a country’s fiscal policy decisions result in budget deficits that it cannot finance by selling

government bonds, its money supply will rise because it will have to either simply print money to

4. Problems in the banking sector can lead to a currency crisis in a couple of different ways. If a

country’s banking system is weakening and there is a financial crisis leading to a slowdown in the

5. a. The central bank of the overvalued currency should intervene in the foreign exchange market and

buy its own currency (paying with international reserves) in order to increase the value of its

domestic currency. Doing so will result in a shift to the right of the demand curve for domestic

assets to D2 (where the currency is not overvalued anymore).

b. If this country does not have enough international reserves to support its own currency, then it

will not be possible to buy its own currency and solve this situation. The stage for a speculative

Chapter 17 Exchange Rates and International Economic Policy 201

◼ Data Sources, Related Articles, and Discussion Questions

A. For Information About Application: The Subprime Financial Crisis and the

Dollar

Data Source

Federal Reserve Bank of St. Louis database (FRED):

value of the U.S. dollar. You can edit the graph to see data from 2006 to 2010 to see the value of the U.S.

dollar as described in the Application.

Related Article

Colvin, Geoff, “What’s Sinking the Dollar?” (11/13/2007):

article, you can find some arguments for the decrease in the value of the U.S. dollar during the first stages

of the financial crisis. Later, the dollar would appreciate, as noted in the Application.

Discussion Question

By mid-2010, Greece experienced financial problems, mostly related to the size of its budget deficits.

Country members of the European Union debated how to support Greece, as rumors of other countries

being in the same situation circulated. How do you think these events affected the exchange rate between

the euro and the U.S. dollar?

Answer: Greece’s announcement about its huge budget deficits, linked to rumors of default of other

B. For Information About Application: Why Are Exchange Rates So Volatile?

Data Source

Federal Reserve Bank of St. Louis database (FRED):

change the data range to one year to see daily fluctuations even more clearly.)

Related Article

Aghion, Philippe et al., “Exchange Rate Volatility and Productivity Growth: The Role of Financial

Discussion Question

Suppose that during the same day that the United States announces extremely high productivity growth

rates, Mexico’s monthly inflation rate increases above 10 percent, and the European Central Bank

announces a rescue plan for Ireland, Portugal, and Spain. Which would be the consequence of these events

for the value of these currencies? Conclude by discussing the implied volatility of exchange rates.

Answer: News about increased productivity growth in the United States will increase the expected value of

202 Mishkin • Macroeconomics: Policy and Practice, Second Edition

D. For Information About Application: How Did China Accumulate Over $3

Trillion of International Reserves?

Data Source

Federal Reserve Bank of St. Louis database (FRED):

China/U.S. foreign exchange. Note how recent efforts by the United States and other countries forced

China to allow an appreciation (a decline in this series) of the Chinese currency.

Related Article

Seo, EunKyung (Bloomberg, 09/28/2010), “G–20 Officials Seek Currency Policy Compromise”:

cheapening-currencies.html. This article shows how difficult it is for governments to agree on an exchange

rate policy. Note in particular the pressure exerted over the Chinese currency policy by many countries.

Discussion Question

Describe the effect on the value of the U.S. dollar of a sell-off of U.S. Treasury bonds and purchase of

euro denominated assets by the Chinese government.

Answer: If the Chinese government decides to use its holdings of U.S. Treasury bonds to buy euro-

D. For Information About Policy and Practice: Will the Euro Survive?

Data Source

Federal Reserve Bank of St. Louis database (FRED):

2000 to the latest data available. Here you can find data about unit labor costs in Spain, and note that

because Spain cannot devalue its currency (it is a member of the euro zone), the way around that

“straitjacket” is “internal” devaluation, which amounts to a significant decrease in unit labor costs.

Related Article

greatly strengthened. Note the use of the terms “internal devaluation” on the last subtitle “Restoring

Growth in Euroland.”

Discussion Question

Why do you think that Eurozone member countries that suffered from their inability to set their own

monetary policy did not simply exit the Eurozone and came back to using their own currency?

Chapter 17 Exchange Rates and International Economic Policy 203

Answer: Although it was clear that the inability to set their own monetary policy did not help countries

that were in trouble during the recent crisis in Europe, it is also important to note that the establishment of

E. For Information About Policy and Practice: The Collapse of the Argentine

Currency Board

Data Source

peso” as target currency and then select 2000 to 2002 for the data range).

Related Article

announcements about the Argentinean default. Note the expected effects on its currency, expressed in the

third paragraph: “currency uncertainty.”

Discussion Question

Which are the main consequences on monetary policy flexibility of establishing a currency board?

Answer: By definition, when a country establishes a currency board, it forgoes its ability to conduct

F. For Information About Application: The Foreign Exchange Crisis of

September 1992

Data Source

The University of British Columbia (Pacific Exchange Rate Service): http://fx.sauder.ubc.ca/data.html.

Use this application to access data about the British pound/German mark exchange rate (select “British

pound” as base currency and “German mark” as target currency and then select 1992 to 1993 for the data

range). Check what happened to that exchange rate in the aftermath of Wednesday, September 16, 1992.

Related Article

The New York Times, “When Soros Decided to ‘Go for the Jugular’:

Soros’ role in the events of the September 1992 crisis are detailed.

Discussion Question

In light of the events of September 1992, what do you think the most important peril of engaging in a

system of fixed exchange rates when cooperation among countries is difficult to achieve is?

204 Mishkin • Macroeconomics: Policy and Practice, Second Edition

Answer: The events of September 1992 clearly illustrated the idea that a system of fixed exchange rates

G. For Information About Application: Foreign Exchange Crises in Emerging

Market Countries: Mexico 1994; East Asia 1997; Brazil 1999 and Argentina

2002

The University of British Columbia (Pacific Exchange Rate Service): http://fx.sauder.ubc.ca/data.html.

Use this application to access data about the Mexican peso/U.S. dollar exchange rate (select “Mexican

pesos” as target currency and then select 1994 to 1995 for the data range). Note the evolution of the

exchange rate beginning in December 19, 1994.

Related Article

Mishkin.pdf. In this paper, the author of the textbook identifies the most important differences between

financial crises in emerging and industrialized countries and draws conclusions about how to deal with

financial crises in emerging market economies.

Discussion Question

Suppose that in 2001 you bought an apartment in Buenos Aires, Argentina, valued at $100,000

Argentinean pesos. For that purpose, you took a mortgage loan for $80,000 U.S. dollars. What do you

think happened to the value of your loan in Argentinean pesos after the Argentinean peso was devalued by

more than 50 percent on January 2002?

Answer: In 2001, the exchange rate between the Argentinean peso and the U.S. dollar was 1. This meant