375

CHAPTER 16

Understanding Consumer Behavior

Notes to the Instructor

Chapter Summary

This chapter discusses the theory of the consumer. It is structured so as to follow, more or less,

the history of thought on the topic. It first presents the Keynesian consumption function, then

discusses Irving Fisher’s model of intertemporal choice, and then addresses the life–cycle and

permanent–income theories of consumption. The chapter also includes a discussion of rational–

expectations theories of consumption.

Comments

This material probably requires two to three lectures. This is a good time to discuss the

importance of microfoundations in macroeconomic models. I suggest to students that the

material in Part V of the book allows us to both justify and to refine the important behavioral

assumptions that underlie the earlier models. In the case of consumption theory, looking at the

underlying microeconomics improves the performance of the short–run macroeconomic model.

This chapter can be treated as an extended case study on the development of a theory in

Use of the Web Site

One important advantage of the Web–based software is that it allows students to see explicit life–

cycle behavior with a nonzero interest rate and also to see how much difference interest rate

changes can make. Students may also be surprised at how difficult it is to smooth their

consumption over their lifetime. Students could also try to obtain something other than a

completely smooth consumption path—one possibility would be consumption increasing

gradually through the lifetime; another would be smooth consumption except for a blip

somewhere in middle age (say, for financing children through college).

376 | CHAPTER 16 Understanding Consumer Behavior

Use of the Dismal Scientist Web Site

Go to the Dismal Scientist Web site and download quarterly data on the major components of

personal consumption expenditures (durable, nondurable, and services) in the U.S. over the past

ten years. Assess the effect of the recession of 2001 and the recession of 2008–2009 on

consumer spending. Did it decline during these recessions? Did certain components decline but

Chapter Supplements

16-2 The Stock Market and Consumer Spending

16-4 The 1975 Tax Cut (Case Study)

16-5 Do Consumers Anticipate Changes in Social Security Benefits? (Case Study)

16-6 Is Unemployment Insurance Really an Automatic Stabilizer?

16-7 Additional Readings

Lecture Notes | 377

Lecture Notes

Introduction

Modern macroeconomics emphasizes the need for solid microeconomic foundations. Although

we make many simplifications in macroeconomics and ignore most differences among

individuals, we still hope that our macroeconomic theory is grounded in sensible

microeconomics. Macroeconomics and microeconomics, after all, should not be completely

separate disciplines; they are attempts to understand economic phenomena on different scales.

16–1 John Maynard Keynes and the Consumption Function

The consumption function was introduced into macroeconomics by John Maynard Keynes in

The General Theory of Employment, Interest and Money. We start our analysis by considering

Keynes’s ideas about the consumption function.

Keynes’s Conjectures

Recall that our models are based on a simple consumption function:

C = C(Y – T).

This simple Keynesian consumption function is not a bad starting point. It captures a number of

plausible notions about people’s behavior—that they will always want to consume something;

that they will consume more as their income goes up; and that they will tend to spend some and

save some of each additional dollar of disposable income that they earn. We can summarize

these features as follows:

2. The average propensity to consume (C/Y) is a decreasing function of income.

Keynes conjectured that these features were characteristics of actual consumption behavior.

This consumption function is also a bit naive. First, the consumption decision is,

equivalently, a saving decision. Therefore, consumption theory should be about the choice

between consuming now and consuming at some point in the future. That intertemporal aspect is

The Early Empirical Successes

Early work seemed to support the Keynesian consumption function. Surveys of households

found that households with higher incomes both consumed more and saved a higher proportion

!

Figure 16-1

that both consumption and saving were low when income was low.

Secular Stagnation, Simon Kuznets, and the Consumption

Puzzle

As more data became available and more studies were conducted, the evidence became less

clear. First, the Keynesian consumption function implies that saving increases as income

growing, the Keynesian function did not do so well. Instead, consumption was approximately

proportional to income. One way to summarize these findings is that the long–run marginal

propensity to consume differed from the short–run marginal propensity to consume. Another way

of putting this is that the long–run consumption function was steeper than the short–run

views today’s consumption as part of a plan that extends into the future. This plan is not

immutable: As time goes by, people revise their consumption plans, perhaps because they get

new information, or perhaps simply because they change their minds about what they want to

do. Nonetheless, most people’s consumption decisions probably incorporate a forward–looking

element.

16–2 Irving Fisher and Intertemporal Choice

The consumption function Keynes used does not consider how people make decisions over time.

In other words, when people decide how much to consume and how much to save, they take into

account both the present and the future. People face a tradeoff in that more consumption today

The Intertemporal Budget Constraint

We consider an individual who gets income today and tomorrow and who consumes today and

tomorrow. He has to decide how much he wants to save and how much he wants to consume

today. First, what is his budget constraint? In the first period, he gets income of Y1, which he

!Figure 16-2

Lecture Notes | 379

Y1 = C1 + S.

In the second period, he earns interest on his saving, so he has S(1 + r), where r is the real

interest rate. His consumption in the second period is thus

C2 = Y2 + S(1 + r).

FYI: Present Value, or Why a $1,000,000 Prize Is Worth Only

$623,000

If you put $100 in a bank account earning 5 percent interest a year, in ten years you would have

$162.89. Thus, the present value of $162.89 received ten years from now is $100. Formally

Consumer Preferences

We can now analyze the consumer’s problem using standard tools from microeconomics. His

preferences over consumption today and tomorrow can be summarized by indifference curves,

which give combinations of C1 and C2 that yield equal satisfaction. The slope of an indifference

curve gives the rate at which the consumer is willing to trade current for future consumption; it

is called the marginal rate of substitution (MRS).

Optimization

As standard microeconomics teaches, the consumer chooses to consume where he is just

indifferent between giving up a unit of consumption today for extra consumption tomorrow,

which is the point of tangency of his indifference curve and the budget line. At this point, MRS =

1 + r.

How Changes in Income Affect Consumption

The intertemporal budget constraint reveals that changes in income in either period will alter the

present value of income. In terms of the diagram, a change in income in either period shifts the

budget constraint out. Thus, the consumer will consume more in both periods. (In

microeconomics, we pay attention to the possibility that the consumer might consume less of a

good as his income rises. In a macroeconomic analysis, where we are considering an individual’s

!

Figure 16-4

!

Figure 16-5

!

Figure 16-6

!

Figure 16-3

380 | CHAPTER 16 Understanding Consumer Behavior

How Changes in the Real Interest Rate Affect Consumption

Suppose that the real interest rate increases. This means that the budget line becomes steeper—

the consumer gets more additional consumption in the future for giving up a unit of consumption

In the previous discussion, the person was presumed to be a saver in the first period. If he

were a borrower, then the increase in the interest rate would reduce his income. We can see this

on the diagram by noting that the budget line rotates around the endowment point (Y1, Y2). If the

individual is a saver, then the new budget line lies outside the old one, and the individual is

better off. If he is a borrower, then increases in the interest rate make him worse off, as

Constraints on Borrowing

Not everyone can borrow freely against future income as the Fisher model supposes. In reality, it

is often difficult to obtain loans to finance current consumption. Thus, some consumers may face

borrowing constraints (also known as liquidity constraints). When a liquidity constraint binds on

the consumer, so he would like to borrow but cannot, his first–period consumption equals his

16–3 Franco Modigliani and the Life–Cycle Hypothesis

We now return to the attempts to explain the conflicting results on consumption, that is, the idea

that the long–run consumption function is steeper than the short–run consumption function.

Franco Modigliani, Albert Ando, and Richard Brumberg proposed an explanation based on the

ideas in the Fisher model. In particular, they focused on the role of saving in smoothing

individuals’ consumption over their lifetimes.

The Hypothesis

A stylized fact of economic data is that consumption is much smoother than income. This

suggests that people may use saving to shift resources from times of high income to times of low

income to maintain a relatively constant level of consumption. The life–cycle hypothesis is based

on the idea that people wish to smooth their consumption over their lifetime. In particular,

therefore, they save during their working years to finance consumption during their retirement.

Lecture Notes | 381

Now suppose that earnings equal Y in every working year and that the individual wishes to

smooth his consumption perfectly, so that he consumes C in every year. Then the budget

constraint implies that

CT = W + RY.

Consumption is given by

Implications

The life–cycle model reconciles the short–run and long–run consumption functions. In the

short run, wealth is approximately constant, so we obtain a Keynesian consumption function.

But in the long run, wealth increases with income, so the average propensity to consume is

constant:

uncertainty about future income and about time of death, and so on. All these amendments make

the model more complicated, but the basic message is the same; we still end up with a picture

that resembles Figure 16–12 in the textbook.

Case Study: The Consumption and Saving of the Elderly

The life–cycle model predicts that the elderly dissave; however, empirical research suggests that

16–4 Milton Friedman and the Permanent–Income Hypothesis

Milton Friedman’s approach to consumption theory complements the life–cycle model. Unlike

that model, however, Friedman’s permanent–income hypothesis focuses on the effects on

consumption of random and unpredictable changes in income.

The Hypothesis

Spending”

C = αYP.

This is similar to the life–cycle hypothesis if we view transitory income as changes in

wealth and permanent income as changes in income. The marginal propensity to consume out of

transitory income (wealth) is low; the marginal propensity to consume out of (permanent)

income is high.

Implications

We can write YP = Y – YT. We thus obtain that the average propensity to consume is

APC = αYP/Y = α(1 – YT/Y).

When transitory income is positive, APC will be lower, and vice versa. High–income

households, on average, are those with positive transitory income and so exhibit, on average, a

low average propensity to consume. Over time, however, income changes because of changes in

permanent income.

Case Study: The 1964 Tax Cut and the 1968 Tax Surcharge

The temporary/permanent distinction is very important for correct policy analysis. In 1964 there

to separate the effects of tax policy from other events occurring simultaneously.

Case Study: The Tax Rebates of 2008

In response to an imminent recession, Congress early in 2008 passed the Economic Stimulus

those who received the check later. Overall, the study found that average household spending

increased by about 50 percent to 90 percent of the payment. These results suggest that even if the

“The 1975 Tax

Cut”

Lecture Notes | 383

permanent–income theory is correct in predicting larger effects on consumer spending from

permanent tax changes than from transitory changes, the latter still have significant effects on

16–5 Robert Hall and the Random–Walk Hypothesis

Recent work on consumption has combined rational expectations with the permanent–income

hypothesis, which really means assuming that people are very sophisticated in their guesses

about what their income is going to do.

The Hypothesis

Robert Hall was the first economist to show how rational expectations influence the pattern of

consumption over time. If consumers have rational expectations and follow the permanent–

income hypothesis, then consumption follows a random walk. This means that the best

prediction of consumption during this period is that it will be the same as it was in the recent

past. In other words, changes in consumption are unpredictable. Why is this? If people have

Implications

An implication of this idea is that if we are trying to explain consumption behavior, we need to

know not only if changes in income are temporary or permanent but also if they are anticipated

or unanticipated. If a consumer is told this year that he will receive a raise next year, then the

rational–expectations view of consumption predicts that his consumption will increase this year,

Case Study: Do Predictable Changes in Income Lead to

Predictable Changes in Consumption?

If changes in income are predictable, then according to the random–walk theory we should

observe no change in consumption when income changes. Individuals should adjust their

consumption as soon as they know that their income will change rather than wait for the change

to occur.

The observation that income and consumption fluctuate together over the business cycle

does not negate the random–walk theory because many changes in income are unpredictable.

Studies of predictable income changes show that when income is expected to change,

16–6 David Laibson and the Pull of Instant Gratification

Economists in recent years have turned to psychology for explanations of consumer behavior.

One of the more prominent economists bringing insights from psychology into the study of

consumption is David Laibson. He finds that many consumers believe themselves to be poor

decision–makers. For example, many respondents to surveys understand perfectly well that they

!

Supplement 16–5,

“Do Consumers

Anticipate Changes

in Social Security

Benefits?”

!Supplement 16–6,

“Is Unemployment

Insurance Really an

Automatic

384 | CHAPTER 16 Understanding Consumer Behavior

consumers alter their decisions simply because time has passed. Work is proceeding on this

promising area of research from which we may gain new insights regarding the effects of

economic policies on consumer behavior.

Case Study: How to Get People to Save More

The field of behavioral economics offers some suggestions for getting people to save more. One

approach is to take advantage of inertia in people’s decision making, for example, by

automatically enrolling employees in a company’s 401K retirement plan rather than requiring

employees to “sign–up” for the plan in advance. Studies have shown that people are far less

16–7 Conclusion

The permanent–income and life–cycle hypotheses break the strong, simple link between

disposable income and consumption that the Keynesian consumption function posits. This link

underlies the multiplier in the IS–LM model. These more sophisticated theories of consumption

ADDITIONAL CASE STUDY

16–1 The Components of Consumption

Personal consumption expenditures are divided into durables, nondurables, and services. In 2014, for

example, total consumption expenditures were about $12 trillion, of which services were $8 trillion,

nondurables were $2.7 trillion, and durables were $1.32 trillion1. Thus, spending on services accounts for

two–thirds of total consumption expenditures. This dominance of services is a relatively recent

If we subdivide these components of expenditure further, we find that 34 percent of durable goods

spending is accounted for by motor vehicles and parts, while 22 percent is accounted for by furnishings

and household equipment. Food accounts for 33 percent of nondurable spending, with spending on

clothing and shoes contributing 14 percent.

Looking at services, the most striking feature of the data is that spending on health care now accounts

LECTURE SUPPLEMENT

16–2 The Stock Market and Consumer Spending

As the stock market soared in the late 1990s, an important issue for policymakers was determining how

large an effect the gain in wealth might have on consumer spending. Federal Reserve Chairman Alan

Greenspan, testifying before Congress in February 2000, expressed his belief that the wealth effect was an

important factor in the surging U.S. economy:

very small set of households. Even though more than half of all U.S. households now hold some equities

(mainly through 401K retirement accounts), the distribution is still highly skewed, with the richest 5

percent of households owning 75 percent of equity wealth and the richest 20 percent owning 95 percent of

equity wealth.

Some evidence suggests that the largest effects on spending were indeed seen among the very

2000.

2 See K.E. Dynan and D.M. Maki, “Does Stock Market Wealth Matter for Consumption?” Federal Reserve Board Finance and Economics

ADDITIONAL CASE STUDY

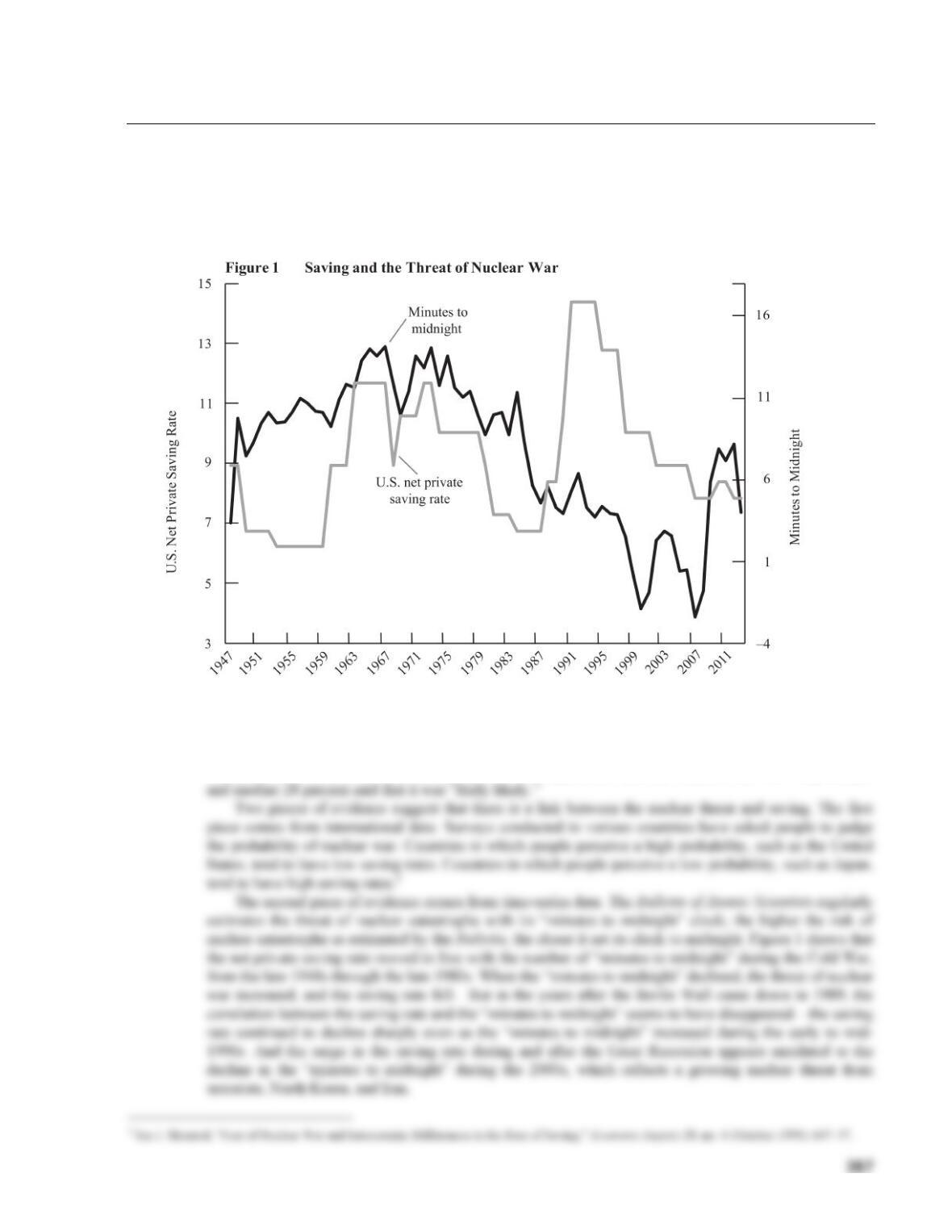

16–3 Saving and the Fear of Nuclear War

One of the more intriguing and controversial hypotheses about saving is that it fluctuates because of

changes in the public’s perception of the probability of nuclear war. Because people save to provide for

consumption in the future, an increase in the probability of nuclear war—and, hence, a decrease in the

probability of surviving into the future—should reduce the amount people save.

Source: Department of Commerce, Bureau of Economic Analysis and Bulletin of Atomic Scientist

Opinion polls indicate that the public has at times considered nuclear war to be a serious threat. In

June 1981, for example, a Gallup poll asked, “How likely do you think we are to get into a nuclear war

within the next ten years?” Nineteen percent of the respondents said that nuclear war was “very likely,”

CASE STUDY EXTENSION

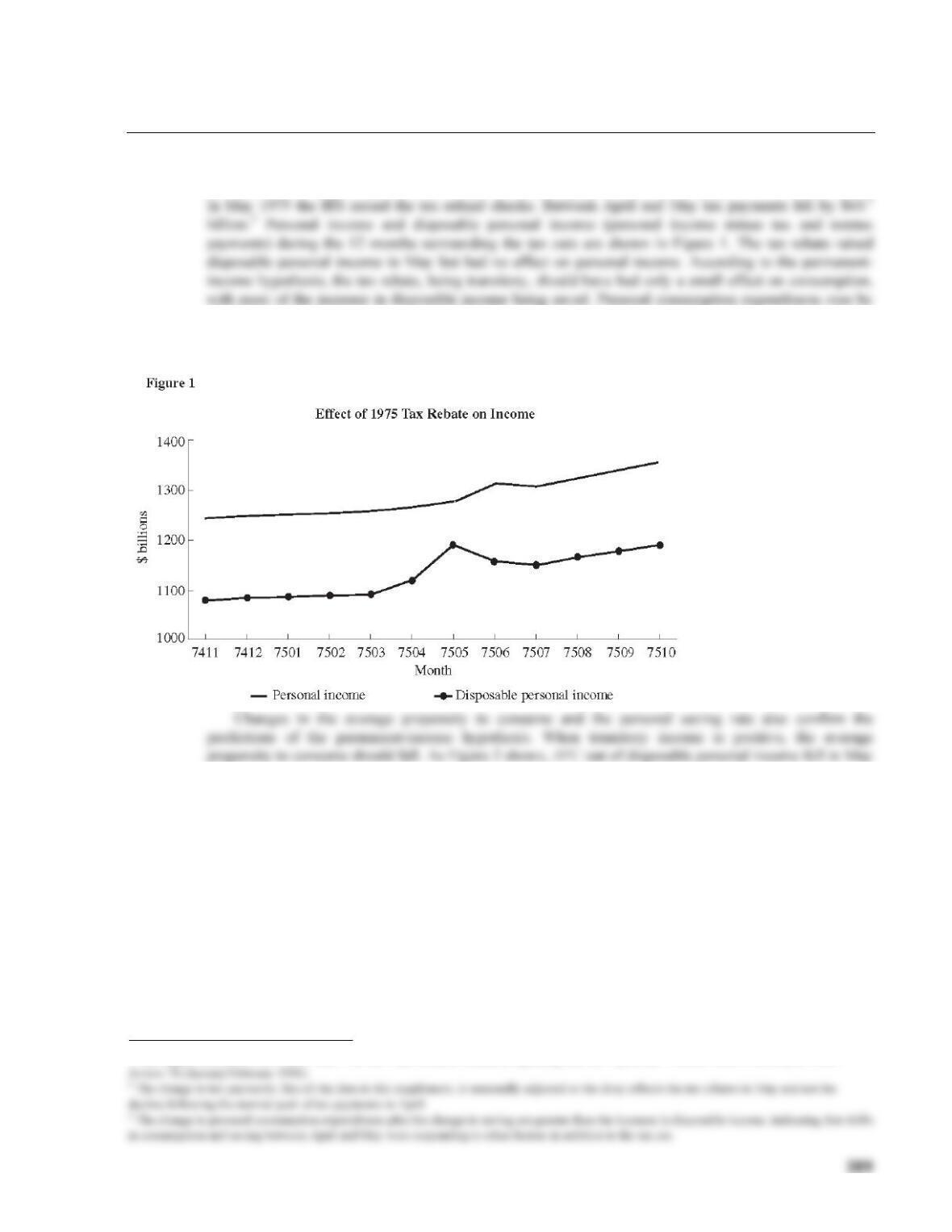

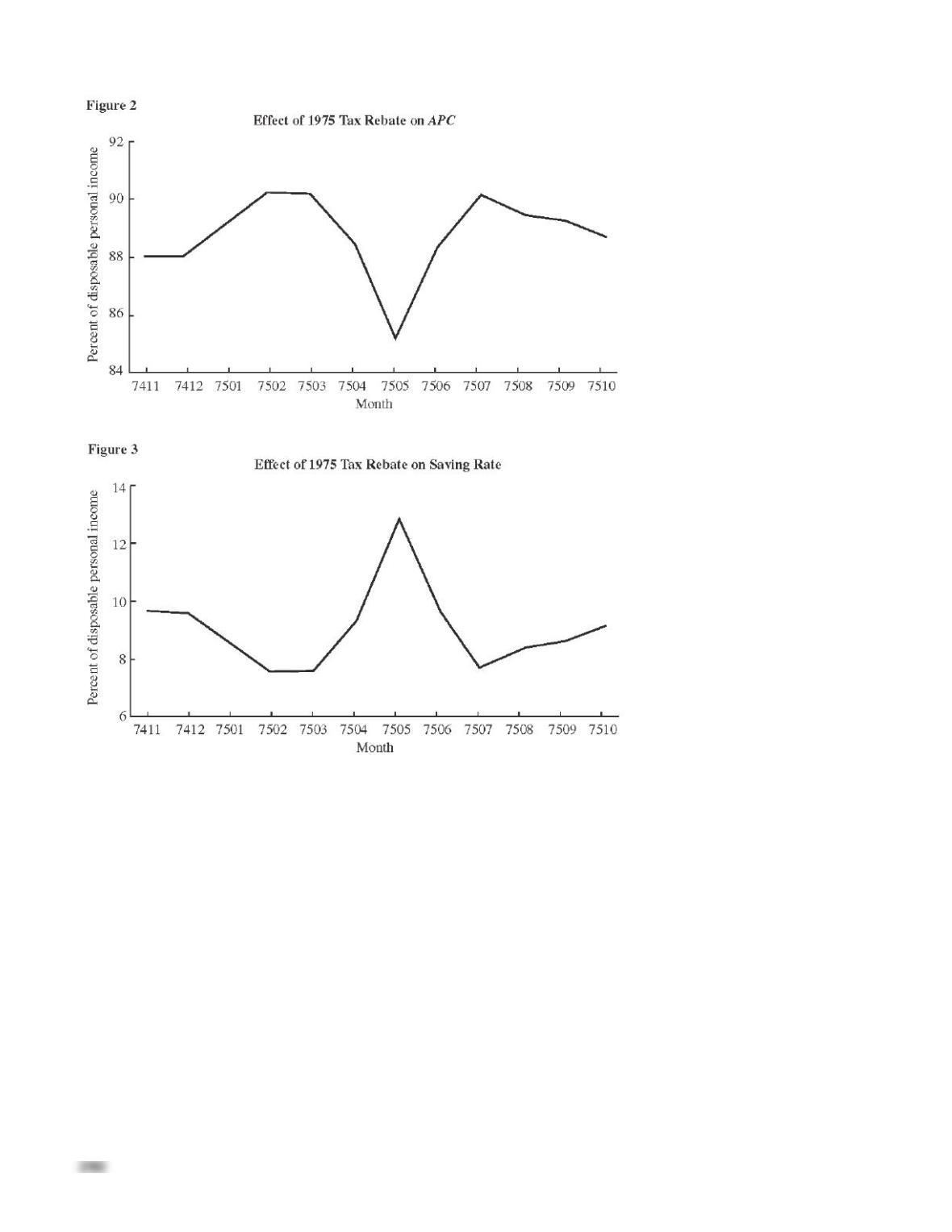

16–4 The 1975 Tax Cut1

In March 1975 Congress passed a tax rebate bill refunding up to $200 of a taxpayer’s 1974 income taxes.

$24.2 billion while savings rose by $49 billion and accounted for most of the increase in disposable

income.3

1975. Saving as a percentage of disposable personal income rose sharply in May 1975, as shown in Figure

3. Notice that both the change in APC and the saving rate were reversed in June 1975, providing further

evidence of the transitory nature of the tax cut.

1 This supplement draws from Peter Yoo, “The Tax Man Cometh: Consumer Spending and Tax Payments,” Federal Reserve Bank of St. Louis

CASE STUDY EXTENSION

16–5 Do Consumers Anticipate Changes in Social Security Benefits?

1989): 228–304.

2 S. Zeldes, “Consumption and Liquidity Constraints: An Empirical Investigation,” Journal of Political Economy 97, no. 2 (April 1989): 305–46. See

also Supplement 16-6, “Is Unemployment Insurance Really an Automatic Stabilizer?”

392

ADDITIONAL CASE STUDY

16–6 Is Unemployment Insurance Really an Automatic Stabilizer?

Chapter 18 of the textbook discusses automatic stabilizers, such as income taxes and unemployment

insurance. The idea of automatic stabilizers is that they tend to stimulate the economy when it is in

recession and decrease aggregate demand in booms. In a recession, for example, tax revenues fall and

transfer payments rise, so disposable income (and hence consumption) falls by less than it would in the

absence of these provisions. The multiplier effects of income changes are lessened.

Permanent–income and life–cycle theories of consumption teach us that the argument is more subtle.

To the extent that people can successfully smooth their consumption over the course of the income

fluctuations of the business cycle, automatic stabilizers are largely irrelevant. Automatic stabilizers work

by making disposable income less variable to make consumption less variable; they do not matter if

consumption is not affected by income fluctuations. Automatic stabilizers are more important when people

393

LECTURE SUPPLEMENT

16–7 Additional Readings

Richard Thaler’s “Anamolies” feature in the Journal of Economic Perspectives 4, no. 1 (Winter 1990):

193–205, discusses some of the failures of the life–cycle model of consumption.

The “Symposium on Consumption Behavior” in the Journal of Economic Perspectives 15, no. 3