CHAPTER 16

Money in the Open Economy

KEY IDEAS IN THIS CHAPTER

2. In the monetary small open economy model, money is neutral under a flexible

exchange rate.

4. The choice between a flexible exchange rate regime and a fixed exchange rate regime

5. Capital controls involve restrictions on capital inflows and outflows.

6. Capital controls can dampen fluctuations in output, the current account surplus, and

NEW IN THE THIRD EDITION

1. New: “Macroeconomics in Action: Why Did the U.S Currency Appreciate After the

Onset of the Global Financial Crisis?”

2. All data and graphs have been updated.

TEACHING GOALS

The previous chapter covered most of the important issues in open economy

macroeconomics with respect to real variables in the economy. This chapter’s material

covers interactions between real and nominal variables. The most important consequence

of the addition of national monies into the open economy is the need to fully understand

exchange rates. A key building block to understanding the material in this chapter is to

Chapter 16: Money in the Open Economy

chapter all rely on purchasing power parity, and yet evidence suggests that this

relationship is not reliable when dealing with short-horizon developments. In this regard,

it is useful to point out that deviations from purchasing power parity are typically due to

real, as opposed to nominal, factors.

The models developed in this chapter are all classical in nature. Therefore, the nominal

price level has no direct influence on individual welfare or the allocation of resources. A

CLASSROOM DISCUSSION TOPICS

Many times students are disappointed with economics because the discipline rarely offers

strategies for reaping windfall gains. Ask students if they have ever thought of foreign-

exchange speculation as a source of livelihood. Can students work out the proper strategy

if they are confident in their ability to predict future movements in nominal exchange

rates? Is the possibility of windfall profits limited to the case of flexible exchange rates?

Would it be useful to be able to predict devaluations? Remind students that their ability to

forecast must be better than market forecasts. Ask students about the likely consequences

of a widespread change in market expectations about exchange rate movements.

Unfortunately, this point brings us back to the difficulties in making quick money from

learning about economics.

Economists’ theories of exchange rates are very well developed, especially after hundreds

of years of experience. How precisely do you think financial market participants, such as

currency traders, can forecast exchange rates?

It turns out that despite all our economic theories and extensive empirical work, forecasts

of exchange rates are notoriously bad over short horizons. For long time periods, like two

Instructor’s Manual for Macroeconomics, Fourth Canadian Edition

Evidence like this suggests that economists need to do a lot more work to be able to

predict exchange rates effectively. Recently, computers are allowing economists to use

some very fancy models, in which the riskiness of exchange rates changes over time, to

OUTLINE

1. Basic Concepts

a) The Nominal Exchange Rate

b) The Real Exchange Rate

c) Purchasing Power Parity

i) Nontraded Goods

2. Flexible and Fixed Exchange Rates

a) Flexible Exchange Rates

b) Fixed Exchange Rates

i) Hard Pegs

(2) Currency Boards

(3) A Common Currency: The Euro

ii) Soft Pegs

(1) The European Monetary System

(3) The International Monetary Fund

3. A Monetary Small Open Economy: Flexible Exchange Rates

a) Money Market Equilibrium and Exchange Rate Determination

b) The Neutrality of Money under Flexible Exchange Rates

M

↑

i) Price-Level Effect

ii) Depreciation of the Domestic Currency

Chapter 16: Money in the Open Economy

d) A Real Shock *

r↑

4. A Monetary Small Open Economy: Fixed Exchange Rates

a) The Basics

i) Foreign-Exchange Transactions by the Government

ii) The Endogeneity of the Domestic Money Supply

b) A Nominal Shock: *

P↑

i) Money Supply Effects

M

↑

ii) Price-Level Effects P↑

c) A Real Shock *

r↑

i) Money Supply Effects

5. Advantages of Fixed vs. Flexible Exchange Rates

a) Advantages of Flexible Exchange Rates

i) Price-Level Stabilization with Nominal Shocks

6. Capital Controls

a) The Capital Account and the Balance of Payments

i) Capital Flows

(2) Foreign Direct Investment

(3) Portfolio Inflows and Outflows

ii) Balance of Payments: An Accounting Identity

b) Effects of Capital Controls

i) Insulation from Foreign Shocks

ii) Misallocation of Capital

d) Do Capital Controls Work in Practice? (Macroeconomics in Action 14.2)

Instructor’s Manual for Macroeconomics, Fourth Canadian Edition

TEXTBOOK QUESTION SOLUTIONS

Problems

1. Having fixed the foreign exchange market transactions cost, the purchasing power

parity relationship is now P = e(1+a)P*, so the equilibrium condition for the money

market can now be written as

),()1( *rYLPaeM += .

Then, a decrease in a acts to reduce the demand for money, shifting the money

demand curve to the left. In the flexible exchange rate regime this acts to increase e,

so that the exchange rate depreciates. As well, from the purchasing power parity

2. A temporary increase in total factor productivity.

a) The increase in total factor productivity shifts the goods demand curve to the

right. Output increases, absorption is unchanged, and the current account surplus

increases. The money demand curve rotates to the right and, under flexible

exchange rates, the nominal exchange rate and the domestic price level both

decrease.

b) The real effects are independent of the exchange rate regime. Under fixed

exchange rates, the money supply must increase to keep the money market in

3. A temporary increase in government spending shifts both the goods demand curve

and the goods supply curve to the right, with the demand curve shifting by more than

the supply curve. Output increases, absorption increases, and the current account

4. A reduction in the domestic demand for money.

a) The leftward rotation of the money demand curve increases both the nominal

exchange rate and the domestic price level.

5. An anticipated increase in future total factor productivity.

a) The increase in future total factor productivity shifts the output demand curve to

the right. The output supply curve is unaffected. In the absence of capital controls,

output is unchanged, and absorption increases, so the current account moves into

deficit. Investment spending increases by the full amount of the rightward shift in

b) Capital controls, as long as they are effective, keep the current account surplus at

zero. Domestic output and absorption must remain equal, so the domestic real

interest rate must increase to keep output supply and output demand equal. Output

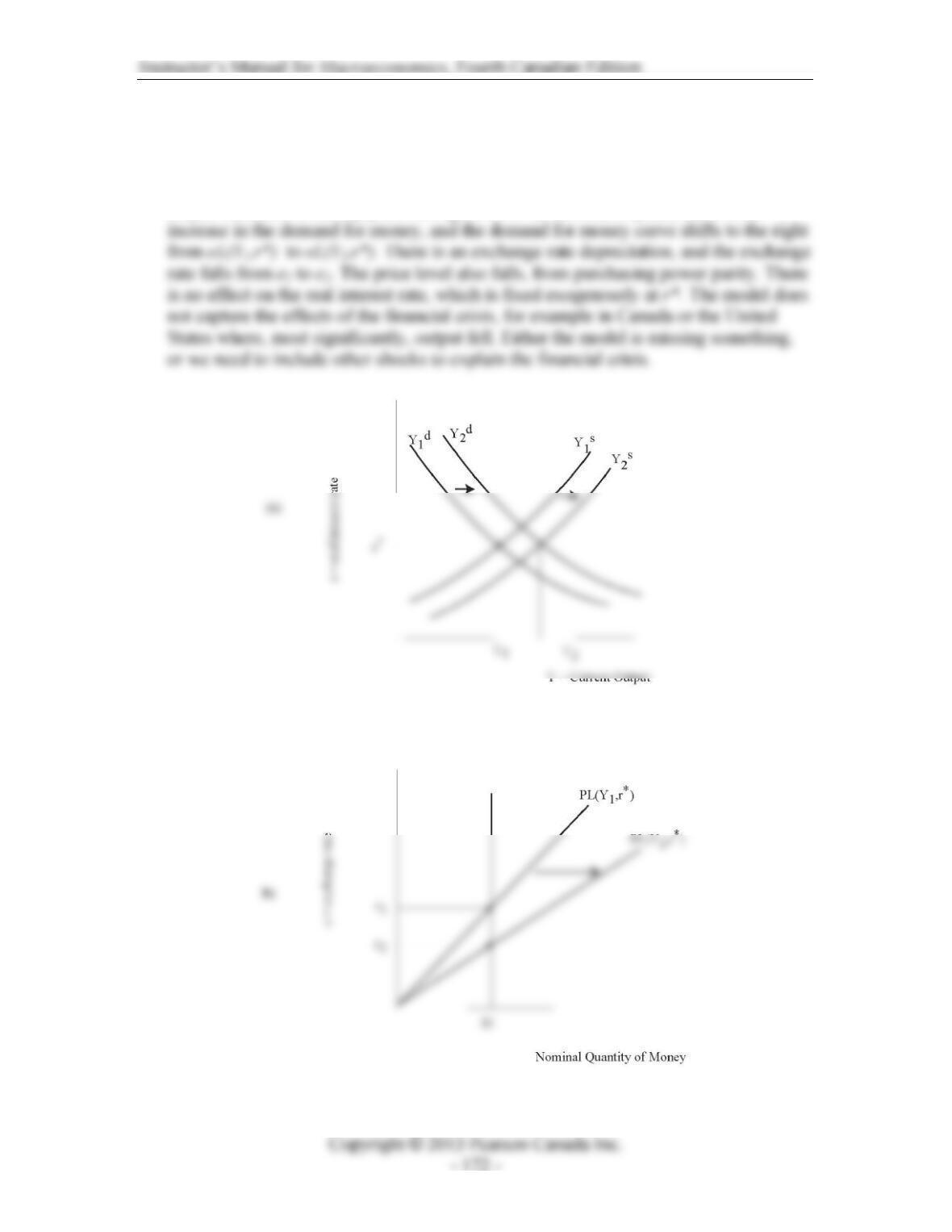

6. As in Chapter 11, an increase in credit market uncertainty results in a shift to the left

in the output demand curve, and a shift to the right in the output supply curve. In the

small open economy, net exports increase so that the output demand curve shifts to

intersect with the output supply curve at the world real interest rate r*. In equilibrium,

output increases in the top panel of Figure 16.1. In the bottom panel, there is an

Figure 16.1

6. An increase in the nominal money supply is neutral under flexible exchange rates.

The increase in the money supply increases the nominal exchange rate and the

7. Suppose for convenience that the current account surplus is initially zero. For a

positive productivity shock, the output supply curve shifts right, and this will tend to