Table 16.1 Additional Funds Needed (AFN) Model (Millions of Dollars) 12/12/2018

Part I. 2019 Data from Chapter 3, Tables 3.1 and 3.2

A0* = Assets at 12/31/19. All assets were needed for 2019 sales $2,000

S0 = 2019 Sales $3,000

Part II. Data Used in the AFN Equation: 2019 Ratios Held Constant

Base Case:

2019 Data

0.6667

0.0488

0.4101

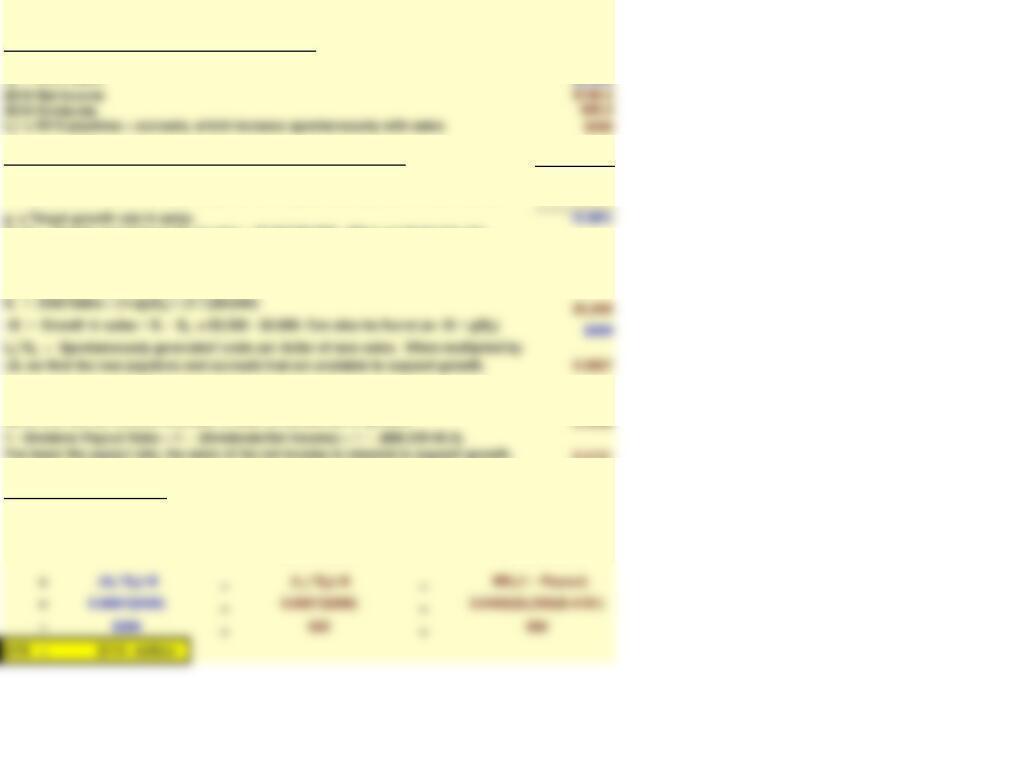

Part III. The AFN Equation

AFN = – –

Required increase

in assets

Spontaneous

increase in payables

and accruals

Funds obtained as new

retained earnings. Based

on 2020 sales

AFN = Additional Funds Needed to buy assets needed to support growth. AFN is

in addition to funds raised internally, i.e., AFN represents required external funds.

A0*/S0 = Assets required per $1 of sales = $2,000/$3,000. When multiplied by the

increase in sales shows the required new assets for the coming year. Also called the

capital intensity ratio . The higher this ratio, the more new assets the firm will need to

support a given amount of growth.

M = Profit margin on sales = 2019 net income/S0 = $146.3/$3,000. Multiply by S1 (not

S0) to find the net income available in 2020 for dividends or growth.

The lower the payout rate, the more of the net income is retained to support growth.

Part IV. Sensitivity Analysis: AFN with Changed Input Values

New

Change:

New – Old

Growth:

Lower

Growth:

$27 -$87

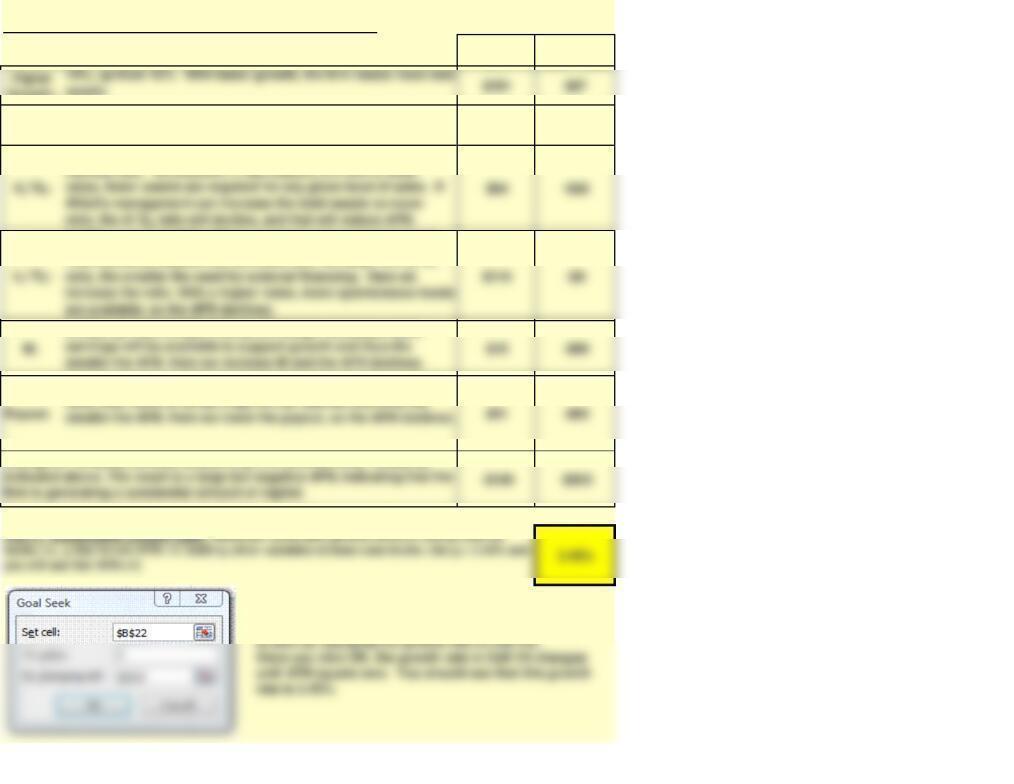

The sustainable growth rate is found using

Excel’s Goal Seek. AFN (calculated in Cell B22) is set

to zero by changing the growth rate in Cell I10.

Once you click OK, the growth rate in Cell I10 changes

until AFN equals zero. You should see that this growth

rate is 3.45%.

AFN (Old = $114)

assets.

5%, down from 10%. With slower growth, the firm needs less

new assets.

0.5000, down from 0.6667. This factor is called the capital

0.0800, up from 0.0667. Allied spontaneously generates funds

from accounts payable and accruals; and the larger the L0*/S0

0.1000, up from 0.0488. If the profit margin increases, more

0.2000, down from 0.5899. If Allied lowers the dividend payout

Change all variables simultaneously to g = 5% and the other values as

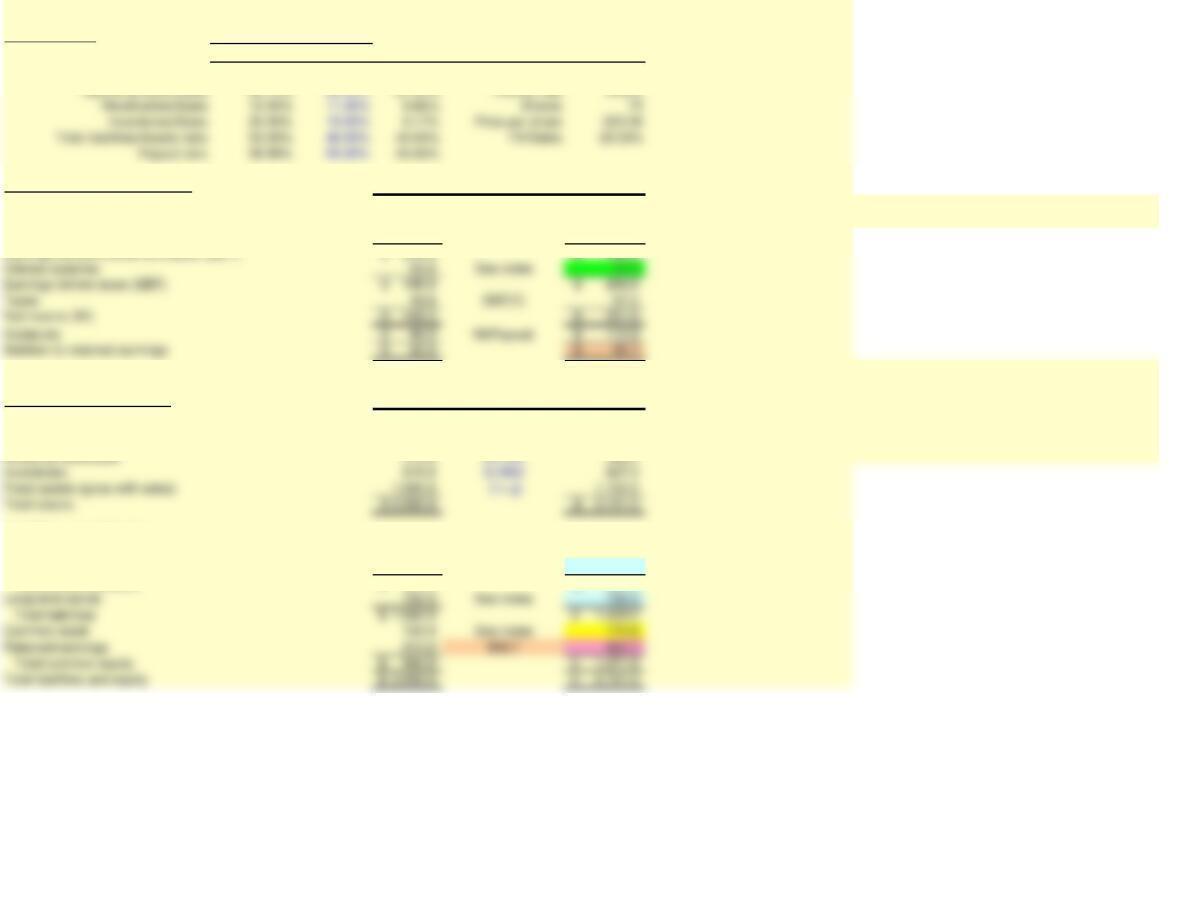

Table 16.2 Forecasted Financial Statements (Total dollars and shares in Millions) 12/12/2018

Part I. Inputs

2019 2020 Industry

Growth rate, g NA 10.00% NA Tax rate (T) 25.00%

Operating costs/Sales 90.73% 89.50% 87.00% Interest rate 9.60%

Part II. Income Statements 2019 Change 2020

Sales 3,000.0$ (1+ g) 3,300.0$

Operating costs (includes depreciation) 2,722.0 0.895 2,953.5

Earnings before interest and taxes (EBIT) 278.0$ 346.5$

Part III. Balance Sheets 2019 Change 2020

Assets

Cash (grow with sales) 10.0$ (1+ g) 11.0$

Accounts receivable 375.0 0.1100 363.0

Liabilities and Equity

Payables + accruals (both grow with sales) 200.0$ (1+ g) 220.0$

Short-term bank loans 110.0 See notes 103.5

Total current liabilities 310.0$ 323.5$

The primary “driver” for income statement changes is operating costs, which moves

toward the industry average: Op cost = New % × forecasted 2020 Sales.

Adjustable Inputs

Fixed Inputs

The “drivers” for the balance sheet changes are the changes in receivables and

inventories, which move toward the industry averages. The balancing items are bank

debt and common stock. The balancing procedure is explained in Part V, Notes on

Calculations.

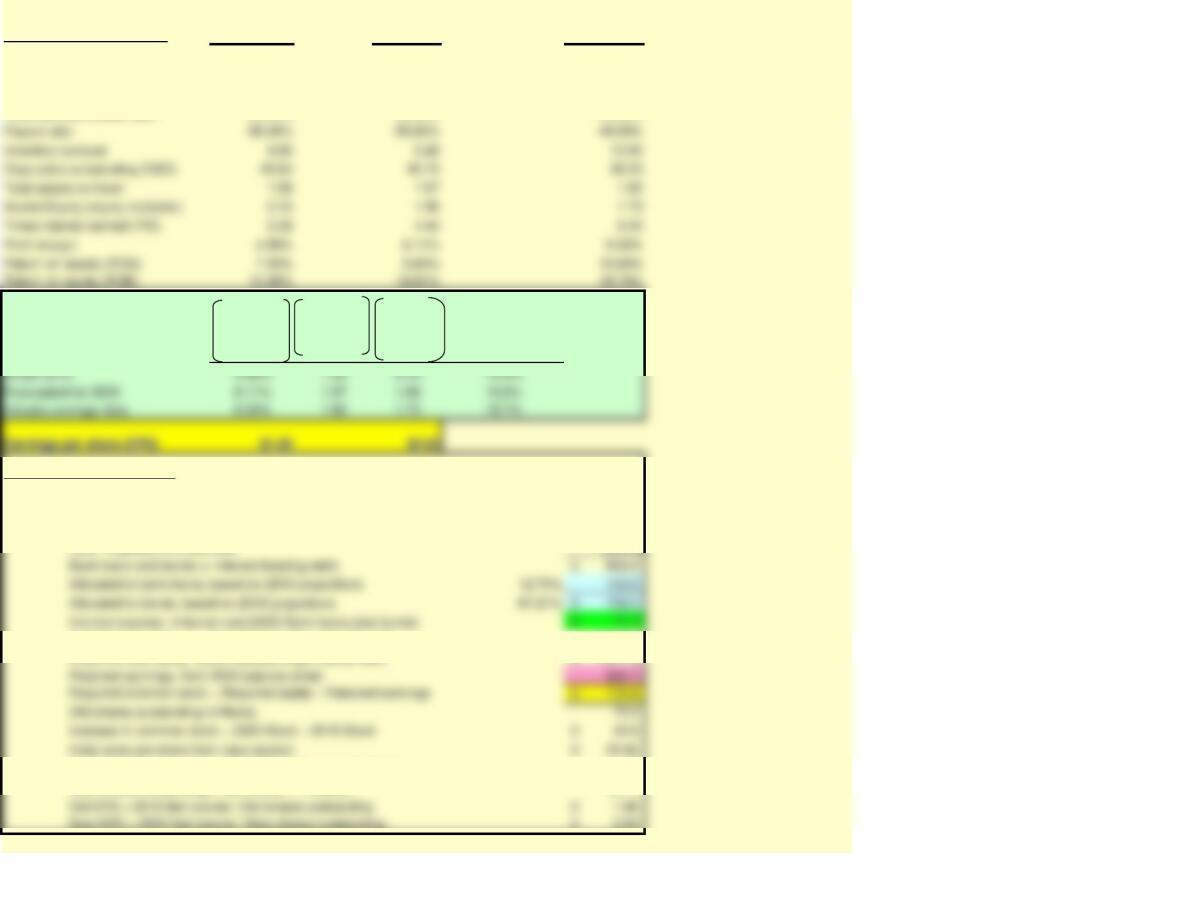

Part IV. Ratios and EPS 2019 2020E Industry

Operating costs/Sales 90.73% 89.50% 87.00%

Receivables/Sales 12.50% 11.00% 9.86%

Inventory/Sales 20.50% 19.00% 9.17%

Total liabilities/Assets ratio 53.00% 49.00% 40.00%

DuPont Calculations

Profit Margin

(NI/S)

Total Assets

Turnover

(S/A)

Equity

Multiplier

(A/ E)

= ROE

Part V. Notes on Calculations

Assets in 2020 will change to this amount, from the balance sheet 2,101.0$

Target total liabilities/assets ratio 49.00%

Resulting total liabilities: (Target total liabilities/assets ratio)( 2020 Assets) 1,029.5$

Less: Payables and accruals (220.0)

Target equity ratio = 1 – Target total liabilities/assets ratio 51.00%

Required total equity: (2020 Assets)(Target equity ratio) 1,071.5$

Change in shares = Change in stock/Initial price per share 1.77

New shares outstanding = Old shares + ∆ Shares 76.77

New EPS = 2020 Net income / New shares outstanding 2.63$

USING REGRESSION TO IMPROVE FORECASTS (Section 16-5) 12/12/2018

Year Sales Inventories Receivables

2015 $2,058 $387 $268

2016 2,534 398 297

2020 3,300 ? ?

Forecasting Inventories

Regression Prior

Forecast Forecast Difference

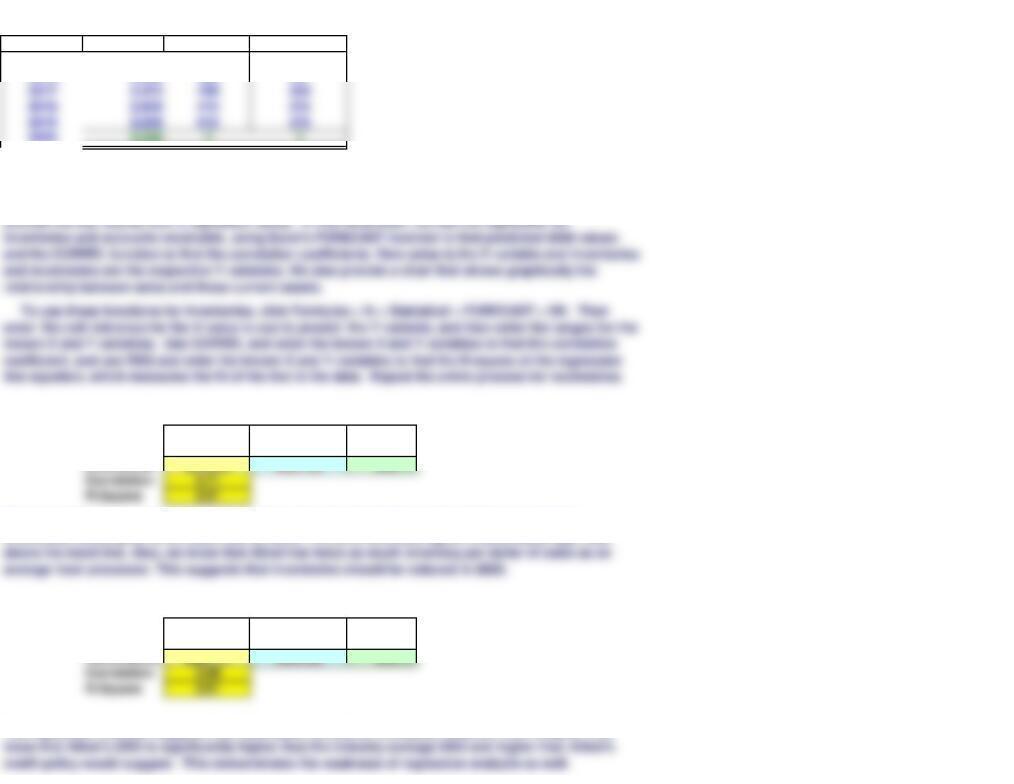

Inventories $578.23 $627.00 -$48.77

R-Square 0.51

Forecasting Accounts Receivable

Regression Prior

Forecast Forecast Difference

Receivables $381.17 $363.00 $18.17

R-Square 0.81

Excel has a full-blown regression tool that can be accessed on the Data tab under Data Analysis. (If

you can’t see this on your screen, you will need to add Excel’s Analysis ToolPak add-in program.)

However, Excel has easier-to-use statistical functions (access through Formulas tab under fx) that

The regression forecast for inventories is lower than the original forecast, which assumed that

inventories would grow at the same rate as sales. The 2019 inventory figure is abnormally high, well

The regression forecast suggests that receivables should be increased; however, from Chapter 4 we

2017 2,472 409 304

2018 2,850 415 315

2019 3,000 615 375