Unlock document.

This document is partially blurred.

Unlock all pages and 1 million more documents.

Get Access

1

2

3

4

5

6

7

14

15

16

17

18

19

20

21

22

29

30

31

32

37

38

39

40

41

42

43

44

45

A B C D E F G H I J

12/10/2012

EVA = NOPAT – Capital costs

= EBIT(1 – T) – WACC (Total capital employed).

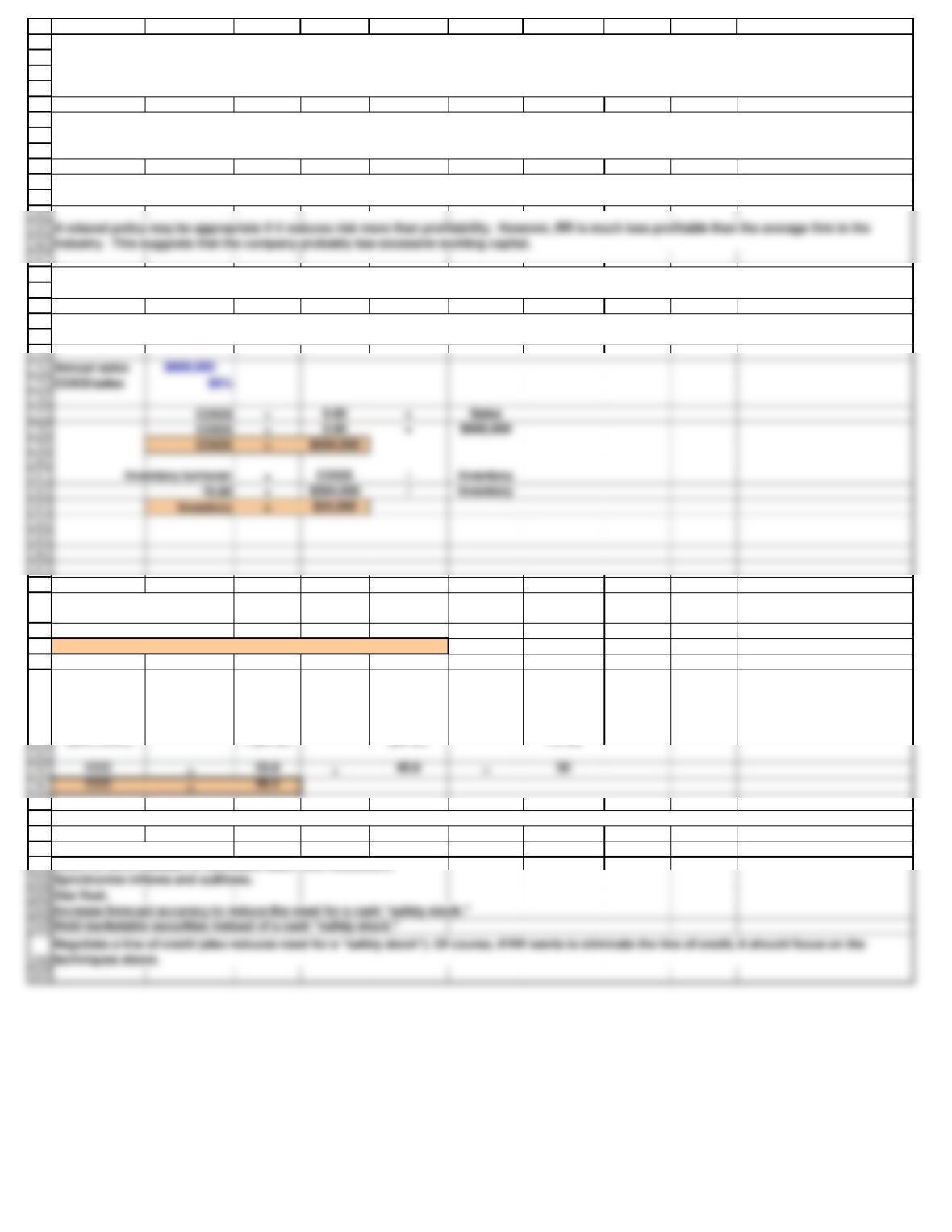

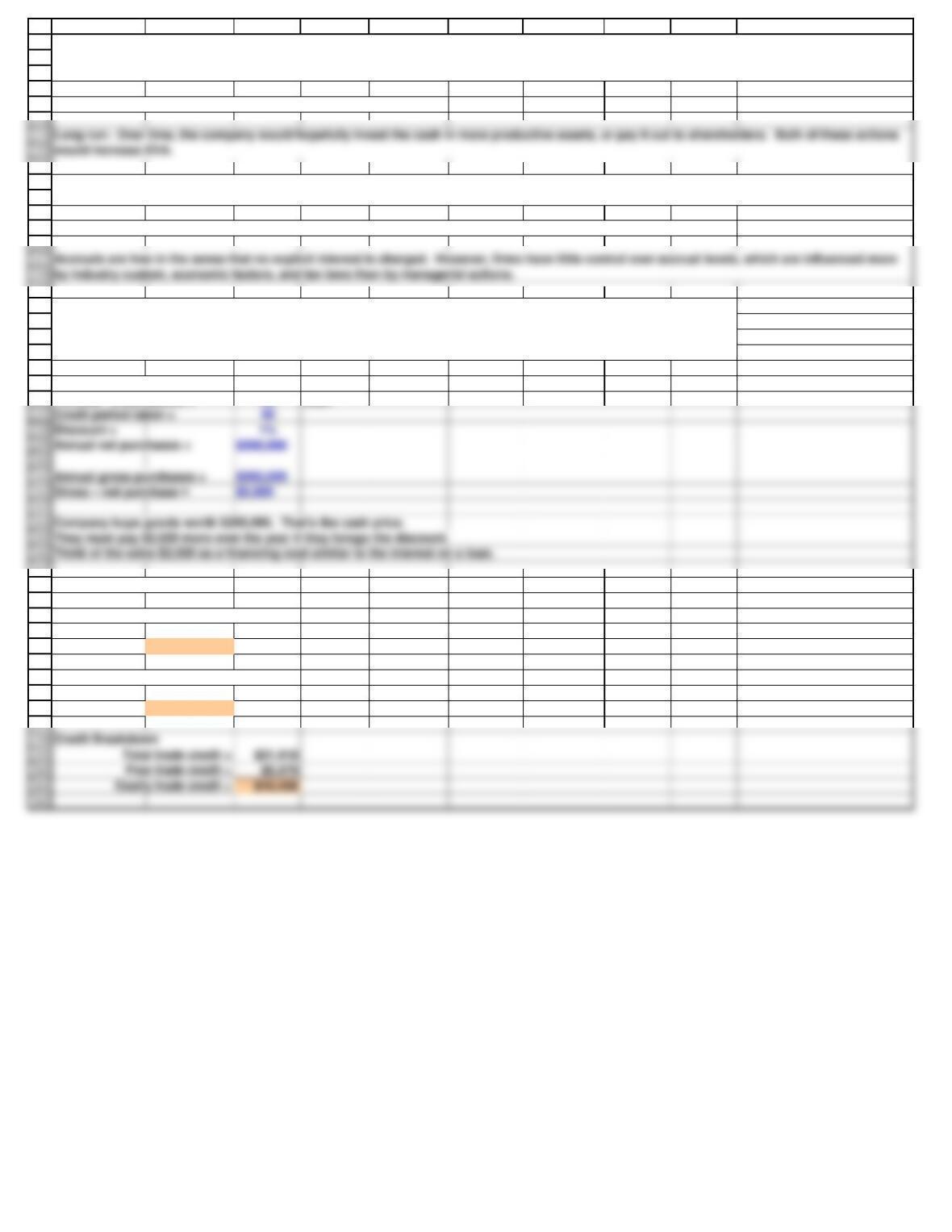

RR Industry

Current 1.75 2.25

Quick 0.92 1.16

TL/assets 58.76% 50.00%

Turnover of cash 16.67 22.22

Days sales outstanding (365-day basis) 45.63 32.00

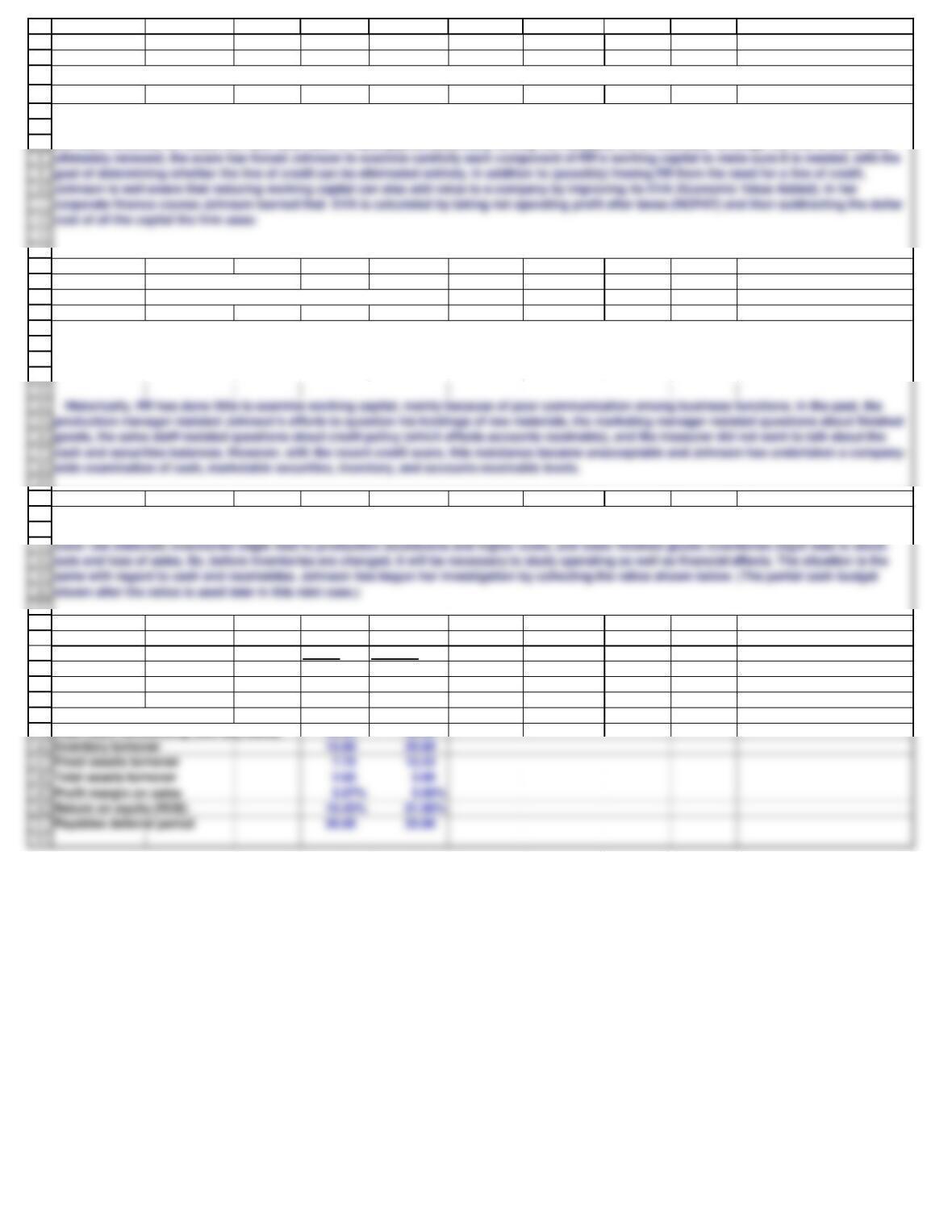

Karen Johnson, CFO for Raucous Roasters (RR), a specialty coffee manufacturer, is rethinking her company’s working capital policy in light of a

recent scare she faced when RR’s corporate banker, citing a nationwide credit crunch, balked at renewing RR’s line of credit. Had the line of credit

not been renewed, RR would not have been able to make payroll, potentially forcing the company out of business. Although the line of credit was

Chapter 16. Mini Case for Supply Chains and Working Capital Management

If EVA is positive then the firm’s management is creating value. On the other hand, if EVA is negative, then the firm is not covering its cost of

capital and stockholders’ value is being eroded. If RR could generate its current level of sales with fewer assets, it would need less capital. This

would, other things held constant, lower capital costs and increase its EVA.

Johnson also knows that decisions about working capital cannot be made in a vacuum. For example, if inventories could be lowered without

adversely affecting operations, then less capital would be required, the dollar cost of capital would decline, and EVA would increase. However,

1 of 6

53

54

55

56

57

58

59

60

61

62

63

68

69

70

71

72

88

89

90

91

92

93

97

98

99

100

101

A B C D E F G H I J

=

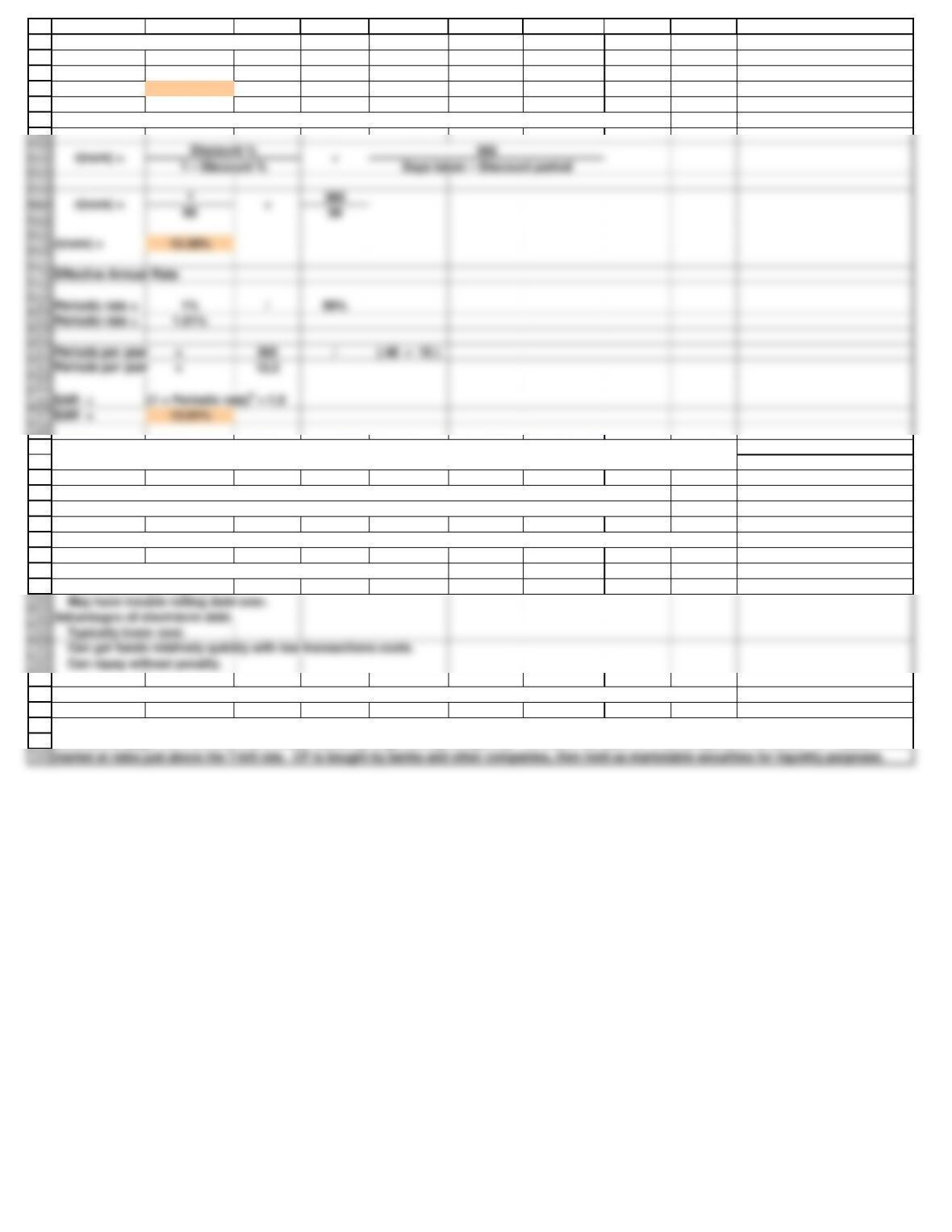

Inventory / Daily COGS

=$55,000 /$1,627.40

=33.8 days

Cash

Conversion

cycle (CCC)

=

Inventory

conversio

n period

+

Average

collection

period

–

Payables

Deferral

Period

Use lockboxes.

Insist on wire transfers or automatic debit from customers.

c. Calculate the firm’s cash conversion cycle given annual sales are $660,000 and cost of goods sold are 90% of sales. Assume a 365-day year.

Need to determine the amount of inventory from the firm's inventory turnover ratio. Then, one can calculate the inventory conversion period from

the data given in the problem.

b. How can one distinguish between a relaxed but rational working capital policy and a situation in which a firm simply has excessive current

assets because it is inefficient? Does RR’s working capital policy seem appropriate?

a. Johnson plans to use the preceding ratios as the starting point for discussions with RR’s operating team. She wants everyone to think about the

pros and cons of changing each type of current asset and how changes would interact to affect profits and EVA. Based on the data, does RR seem

to be following a relaxed, moderate, or restricted working capital policy?

Working capital policy is reflected in a firm’s current ratio, quick ratio, turnover of cash and securities, inventory turnover, and DSO. These ratios

indicate RR has large amounts of working capital relative to its level of sales. Thus, RR is following a relaxed policy.

d. What might RR do to reduce its cash and securities without harming operations?

Inventory conversion period

Inventory conversion period

Inventory conversion period

2 of 6

108

109

110

111

112

113

114

115

116

117

126

127

128

129

130

131

132

133

142

143

144

145

146

147

148

152

153

154

155

156

157

A B C D E F G H I J

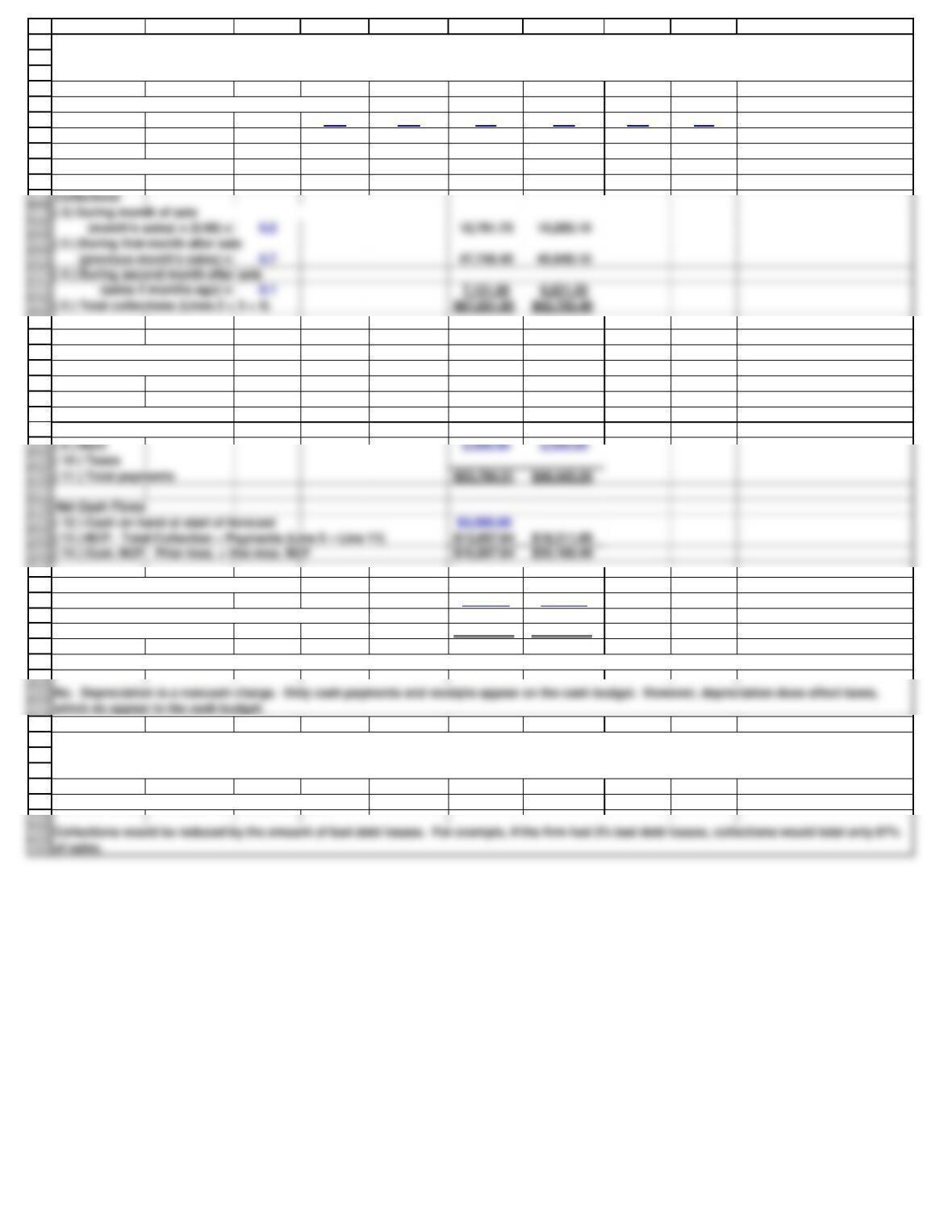

Cash Balance as presented in the Mini Case

Nov Dec Jan Feb Mar Apr

Sales Forecast

( 1 ) Sales (gross) $71,218 $68,212 $65,213 $52,475 $42,909 $30,524

Purchases

( 6 ) During month $44,603.75 $36,472.65 $25,945.40

(forecast sales in 2 months)x 0.85

Payments

( 7 ) Payments (1-month lag) 44,603.75 36,472.65

( 8 ) Wages and salaries 6,690.56 5,470.90

Cash Surplus (or Loan Requirement)

( 15 ) Target cash balance 1,500.00 1,500.00

( 16 ) Cumulative surplus cash or loan needed

(Line 16 – Line 17) $15,357.64 $33,669.49

No! In almost all situations there are bad debts.

In an attempt to better understand RR’s cash position, Johnson developed a cash budget. Data for the first 2 months of the year are shown above.

(Note that Johnson’s preliminary cash budget does not account for interest income or interest expense.) She has the figures for the other months,

but they are not shown.

e. Should depreciation expense be explicitly included in the cash budget? Why or why not?

f. In her preliminary cash budget, Johnson has assumed that all sales are collected and thus that RR has no bad debts. Is this realistic? If not, how

would bad debts be dealt with in a cash budgeting sense? (Hint: Bad debts will affect collections but not purchases.)

3 of 6

161

162

163

164

165

166

167

168

169

174

175

176

177

181

182

183

184

187

188

189

190

191

194

195

196

197

198

199

200

201

202

207

208

209

A B C D E F G H I J

If sales turn out to be considerably less than expected, RR could face a cash shortfall.

Short run: Cash will increase as inventory purchases decline.

h. What reasons might RR have for maintaining a relatively high amount of cash?

g. Johnson’s cash budget for the entire year, although not given here, is based heavily on her forecast for monthly sales. Sales are expected to be

extremely low between May and September but then to increase dramatically in the fall and winter. November is typically the firm’s best month,

when RR ships its holiday blend of coffee. Johnson’s forecasted cash budget indicates that the company’s cash holdings will exceed the targeted

cash balance every month except for October and November, when shipments will be high but collections will not be coming in until later. Based on

the ratios shown earlier, does it appear that RR’s target cash balance is appropriate? In addition to possibly lowering the target cash balance, what

actions might RR take to better improve its cash management policies, and how might that affect its EVA?

RR's inventory turnover (12.00) is considerably lower than the industry average (20.00). The firm is carrying a lot of inventory per dollar of sales. By

i. Is there any reason to think that RR may be holding too much inventory? If so, how would that affect EVA and ROE?

l. Does RR face any risks if it tightens its credit policy?

k. Johnson knows that RR sells on the same credit terms as other firms in its industry. Use the ratios presented earlier to explain whether RR’s

customers pay more or less promptly than those of its competitors. If there are differences, does that suggest RR should tighten or loosen its credit

policy? What four variables make up a firm’s credit policy, and in what direction should each be changed by RR?

j. If the company reduces its inventory without adversely affecting sales, what effect should this have on the company's cash position

(1) in the short run and (2) in the long run? Explain in terms of the cash budget and the balance sheet.

RR's days’ sales outstanding (DSO) of 45.63 days is well above the industry average (32 days). RR's customers are paying less promptly. So, RR

should consider tightening its credit policy to reduce its DSO.

4 of 6

213

214

215

216

217

221

222

223

224

225

229

230

231

232

233

234

235

236

247

248

249

250

251

252

253

254

255

256

A B C D E F G H I J

Short run: If customers pay sooner, this increases cash holdings.

Terms: free credit period = 10 days.

"Official" credit period = 30 days.

Net daily purchases = $548

Payables level if discount is taken:

Payables = $548 ×10

Payables = $5,479

Payables level if don’t take discount:

Payables = $548 ×40

Payables = $21,918

n. Is it likely that RR could make significantly greater use of accruals?

o. Assume that RR purchases $200,000 (net of discounts) of materials on terms of 1/10, net 30, but that it can get

away with paying on the 40th day if it chooses not to take discounts. How much free trade credit can the company get

from its equipment supplier, how much costly trade credit can it get, and what is the percentage cost of the costly

credit? Should RR take discounts?

m. If the company reduces its DSO without seriously affecting sales, what effect would this have on its cash position (1) in the short run and (2) in

the long run? Answer in terms of the cash budget and the balance sheet. What effect should this have on EVA in the long run?

In addition to improving the management of its current assets, RR is also reviewing the ways in which it finances its current assets. With this

concern in mind, Johnson is also trying to answer the following questions.

5 of 6

263

264

265

266

267

268

288

289

290

291

292

293

294

295

296

297

298

304

305

306

307

308

A B C D E F G H I J

Nominal cost of costly trade credit:

r(nom) = $2,020 /$16,438

r(nom) = 12.29%

But the $2,020 in lost discounts is paid all during the year, not just at year-end, so the EAR is higher.

Aggressive: Uses short-term (temporary) capital to finance some permanent current operating assets.

Conservative: Uses long-term (permanent) capital to finance some temporary current operating assets.

Short-term debt is riskier than long-term debt for the borrower.

Short-term rates may rise.

Commercial paper (CP) are short term notes issued by large, strong companies. RR could not issue CP; the company is too small. CP trades in the

r. Would it be feasible for RR to finance with commercial paper?

p. RR tries to match the maturity of its assets and liabilities. Describe how RR could adopt either a more aggressive

or more conservative financing policy.

q. What are the advantages and disadvantages of using short-term debt as a source of financing?

6 of 6