514 Chapter 16

A.

Strategy 1: Consumer-Oriented Promotion

Probability

Outcomes

(Sales)

Profit

Expected

Profit

(1)

(2)

(3) = (2) × 0.5

(4) = (3) × (1)

0.32

$250,000

$125,000

$40,000

Strategy 2: Distributor-Oriented Promotion

Probability

Outcomes

(Sales)

Profit

Expected

Profit

(1)

(2)

(3) = (2) × 0.5

(4) = (3) × (1)

Risk Analysis 515

B.

Strategy 1: Consumer Television Promotion

0.6

0.7

Probability (Pr)

Strategy 2: Distributor Oriented Promotion

516 Chapter 16

C.

Strategy 1

Probability

Deviations

(Deviations)2

Variance

(1)

(2)

(3)

(4) = (1) × (3)

Strategy 2

Probability

Deviations

(Deviations)2

Variance

(1)

(2)

(3)

(4) = (1) × (3)

A comparison of the standard deviations and coefficients of variation for each

strategy confirms that Strategy 1 is the more risky promotional strategy.

Risk Analysis 517

D.

Strategy 1

Probability

Profits

Utils

Expected

Utility

(1)

(2)

(3)

(4) = (3) × (1)

Strategy 2

Probability

Profits

Utils

Expected

Utility

(1)

(2)

(3)

(4) = (3) × (1)

0.125

$125,000

750

93.75

P16.6 Risk-Adjusted Discount Rates. One-Hour Dryclean, Inc., is replacing an obsolete dry

cleaning machine with one of two innovative pieces of equipment. Alternative 1 requires

a current investment outlay of $25,373, whereas alternative 2 requires an outlay of

$24,199. The following cash flows (cost savings) will be generated each year over the

new machines’ four-year lives:

Probability

Cash Flow

Alternative 1

0.18

$5,000

0.64

10,000

0.18

15,000

Alternative 2

0.125

$8,000

$125,000

750

240

518 Chapter 16

0.75

10,000

0.125

12,000

A. Calculate the expected cash flow for each investment alternative.

B. Calculate the standard deviation of cash flows (risk) for each investment

alternative.

C. The firm will use a discount rate of 12 percent for the cash flows with a higher

degree of dispersion and a 10 percent rate for the less risky cash flows. Calculate

the expected net present value for each investment. Which alternative should be

chosen?

P16.6 SOLUTION

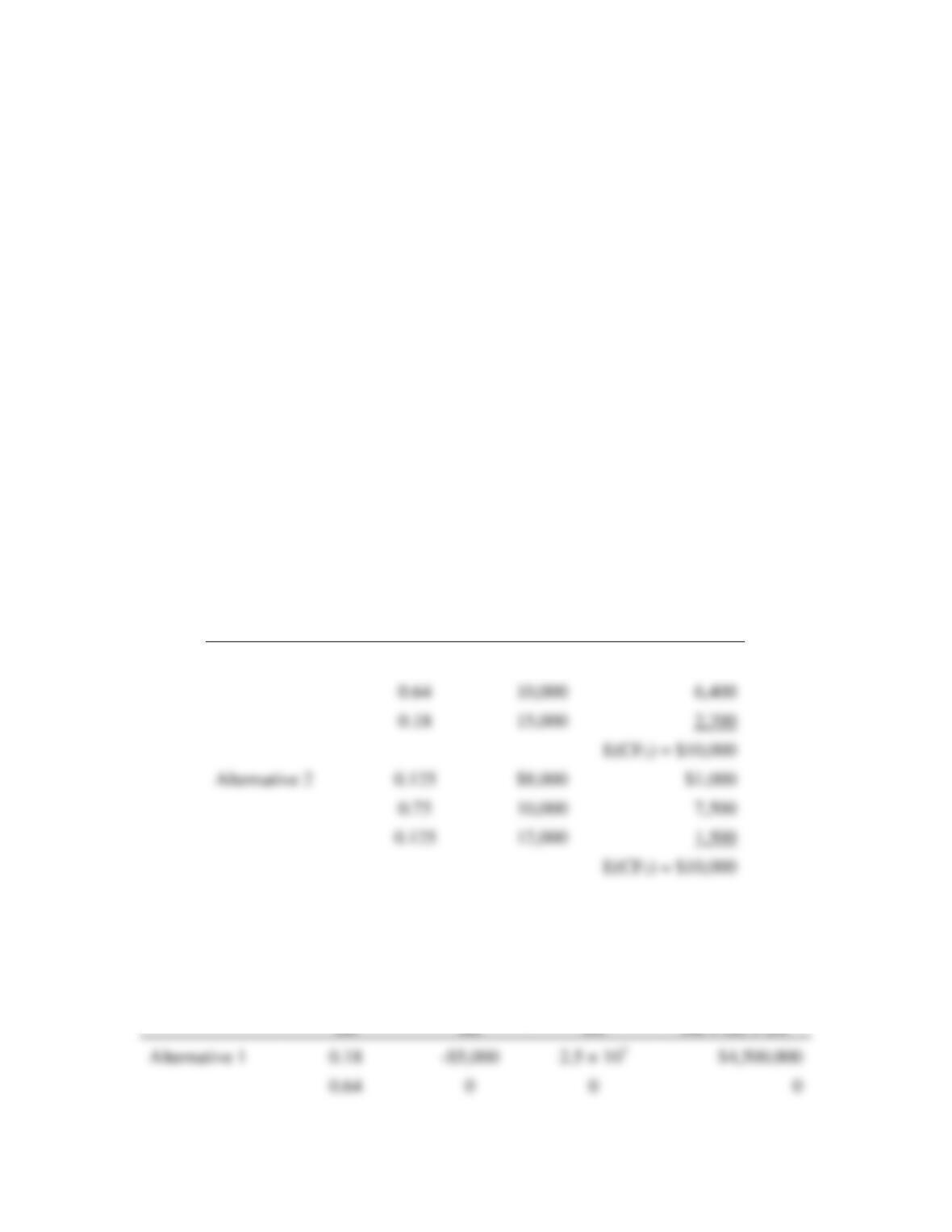

A. Expected values of cash flows

Probability

(1)

Cash Flow

(2)

(3) = (1) × (2)

Alternative 1

0.18

$5,000

$900

B. The relevant standard deviations of cash flows are:

Probability

(1)

Deviation

(2)

Deviation2

(3)

(4) = (1) × (3)

Alternative 1

Risk Analysis 519

Probability

(1)

Deviation

(2)

Deviation2

(3)

(4) = (1) × (3)

Alternative 2

0.125

-$2,000

4 × 106

$500,000

C. Alternative 1 is riskier because it has the greater variability in its probable cash flows.

This is obvious from an inspection of the distributions of possible returns and is verified

520 Chapter 16

P16.7 Certainty Equivalents. Recently, the housing market suffered the worst slump in nearly

two decades. Hot housing markets like Boston, Ft. Lauderdale Florida, and Washington

DC cooled as rising interest rates and tightened lending standards eliminated lots of

potential buyers. With job losses in the auto industry, the housing downturn was

especially serious in Detroit and surrounding areas. Suppose a real estate speculator

seeking to profit from the downturn bought a pool of home mortgages for $1 million on

the expectation of quickly selling them to out-of-town investors for $1.5 million. If the

deal falls through, the speculator would be able to just as quickly dump the pool of home

mortgages in the secondary market for $800,000.

A. Calculate the speculator’s expected payoff if there is a 50/50 chance of successfully

selling the pool of home mortgages to out-of-town investors.

B. Calculate the certainty equivalent adjustment factor for this investment. Is the

speculator’s decision to buy the pool of home mortgages consistent with risk

adverse behavior?

P16.7 SOLUTION

A. If there is a 50/50 chance of successfully selling the bundle of home mortgages to out-

of-town investors, the speculator’s expected payoff is:

Risk Analysis 521

P16.8 Certainty Equivalent Method. Tex-Mex, Inc., is a rapidly growing chain of Mexican

food restaurants. The company has a limited amount of capital for expansion and must

carefully weigh available alternatives. Currently, the company is considering opening

restaurants in Santa Fe or Albuquerque, New Mexico. Projections for the two potential

outlets are as follows:

City

Outcome

Annual Profit

Contribution

Probability

Albuquerque

Failure

$100,000

0.5

Success

200,000

0.5

Santa Fe

Failure

$60,000

0.5

Success

340,000

0.5

Each restaurant would require a capital expenditure of $1.4 million, plus land

acquisition costs of $1million for Albuquerque and $2 million for Santa Fe. The

company uses the 5 percent yield on risk-free U.S. Treasury bills to calculate the risk-

free annual opportunity cost of investment capital.

522 Chapter 16

A. Calculate the expected value, standard deviation, and coefficient of variation for

each outlet’s profit contribution.

B. Calculate the minimum certainty equivalent adjustment factor for each

restaurant’s cash flows that would justify investment in each outlet.

C. Assuming that the management of Tex-Mex is risk averse and uses the certainty

equivalent method in decision making, which is the more attractive outlet? Why?

P16.8 SOLUTION

A. Albuquerque

Santa Fe

B. To justify each investment alternative, the company must have a certainty equivalent

Risk Analysis 523

C. Given managerial risk aversion, Albuquerque is the more attractive outlet because it has

P16.9 Decision Trees. Keystone Manufacturing, Inc., is analyzing a new bid to supply the

company with electronic control systems. Alpha Corporation has been supplying the

systems and Keystone is satisfied with its performance. However, a bid has just been

received from Beta Controls, Ltd., a firm that is aggressively marketing its products.

Beta has offered to supply systems for a price of $120,000. The price for the Alpha

system is $160,000. In addition to an attractive price, Beta offers a money-back

guarantee. That is, if Beta’s systems do not match Alpha’s quality, Keystone can reject

and return them for a full refund. However, if it must reject the machines and return

them to Beta, Keystone will suffer a delay costing the firm $60,000.

524 Chapter 16

A. Construct a decision tree for this problem and determine the maximum probability

that Keystone could assign to rejection of the Beta system before it would reject

that firm’s offer, assuming that it decides on the basis of minimizing expected

costs.

B. Assume that Keystone assigns a 50 percent probability of rejection to Beta

Controls. Would Keystone be willing to pay $15,000 for an assurance bond that

would pay $60,000 in the event that Beta Controls fails the quality check? (Use

the same objective as in part A.) Explain.

P16.9 SOLUTION

A. The decision tree for this decision problem is as follows:

Accept

Probabilit

System Cost

1.0

$160,000

The maximum probability of rejection that could be assigned to the Beta control system

is the probability that makes the expected cost equal for the two alternatives.

Risk Analysis 525

P16.10 Standard Normal Concept. Speedy Business Cards, Inc., supplies customized business

cards to commercial and individual customers. The company is preparing a bid to

supply cards to the Nationwide Realty Company, a large association of independent real

estate agents. Because paper, ink, and other costs cannot be determined precisely,

Speedy anticipates that costs will be normally distributed around a mean of $20 per unit

(each 500-card order) with a standard deviation of $2 per unit.

A. What is the probability that Speedy will make a profit at a price of $20 per unit?

B. Calculate the unit price necessary to give Speedy a 95 percent chance of making a

profit on the order.

C. If Speedy submits a successful bid of $23 per unit, what is the probability that it

will make a profit?

P16.10 SOLUTION

A. If printing costs are normally distributed around a mean of $20 per unit, there is a 50/50

526 Chapter 16

B. In order to have a 95 percent chance of making a profit, 95 percent of the area under the

A Normal Distribution of Unit Costs

for Speedy Business Cards, Inc.

0.5

Probability (Pr)

Risk Analysis 527

528 Chapter 16

CASE STUDY FOR CHAPTER 16

Stock-Price Beta Estimation for Google, Inc.

Statisticians use the Greek letter beta to signify the slope coefficient in a linear relation. Financial

economists use this same Greek letter β to signify stock-price risk because betas are the slope

where Rit is the rate of return on an individual security i during period t, the intercept term is

described by the Greek letter α (alpha), the slope coefficient is the Greek letter β (beta) and signifies

systematic risk (as before), and the random disturbance or error term is depicted by the Greek letter

ε (epsilon). At any point in time, the random disturbance term ε has an expected value of zero, and

capital market, the CAPM asserts that investor rates of return would be solely determined by

systematic risk and both alpha and epsilon would equal zero, α = ε = 0.

As shown in Figure 16.8, managers and investors can estimate beta for individual stocks by

using a simple ordinary least-squares regression model. In this simple regression model, the

dependent Y-variable is the rate of return on an individual stock, and the independent X-variable is

than the Nasdaq market during this period. During a week when the Nasdaq market rose by 1

percent, GOOG rose by 0.9588 percent; during a week when the Nasdaq market fell by 1 percent,

Risk Analysis 529

GOOG fell by 0. 9588 percent. The slope coefficient β = 0.9588 is statistically significant (t = 5.32).

This means that returns on GOOG stock had a statistically significant relationship to returns for

the Nasdaq market during this period.

In the case of GOOG, the usefulness of beta as risk measures is undermined by the fact that

the simple linear model used to estimate stock-price beta fails to include other important systematic

influences on stock market volatility. In the case of GOOG, for example, R2 information shown in

Figure 16.8 indicates that only 36.1 percent of the total variation in GOOG returns can be explained

by variation in the Nasdaq market. This means that 63.9 percent of the variation in weekly returns

for GOOG stock is unexplained by such a simple regression model.

A. Describe some of the attributes of an ideal risk indicator for stock market investors.

B. On the Internet, go to Yahoo! Finance (or msnMoney) and download weekly price

CASE STUDY SOLUTION

A. An ideal measure of stock market risk would be simple to derive, accurate and consistent

from one year to another. With an ideal risk measure, investors are able to control the

risk exposure faced during volatile markets with well-targeted and well-timed investment

buy/sell decisions. For example, suppose an elderly investor wants to maintain an

530 Chapter 16

B. It will be a real eye-opener to students when they estimate stock-price beta for GOOG

over a more recent time period using weekly returns and compare those results with the

C. Empirical estimates of stock-price beta are known to vary according to the time frame

analyzed; length of the daily, weekly, monthly, or annual return period; choice of market

From a theoretical perspective, the most appropriate benchmark would be a market

index that included all capital assets, including stocks, bonds, real estate, collectibles,

and so on. Unfortunately, no such market index is available. To greater or lesser

degree, this affects the accuracy of all beta estimates and undermines confidence in beta

as an accurate measure of security risk. Another important problem faced in obtaining