Mishkin • Instructor’s Manual for The Economics of Money, Banking, and Financial Markets, Twelfth Edition 168

Chapter 15

ANSWERS TO QUESTIONS

1. If the manager of the open market desk hears that a snowstorm is about to strike New York

City, making it difficult to present checks for payment there and so raising the float, what

defensive open market operations will the manager undertake?

2. During the holiday season, when the public’s holdings of currency increase, what defensive

open market operations typically occur? Why?

3. If the Treasury pays a large bill to defense contractors and as a result its deposits with the

Fed fall, what defensive open market operations will the manager of the open market desk

undertake?

4. If float decreases to below its normal level, why might the manager of domestic operations

consider it more desirable to use repurchase agreements to affect the monetary base, rather

than an outright purchase of bonds?

Because the decrease in float is only temporary, the monetary base is expected to decline

5. “The only way that the Fed can affect the level of borrowed reserves is by adjusting the

discount rate.” Is this statement true, false, or uncertain? Explain your answer.

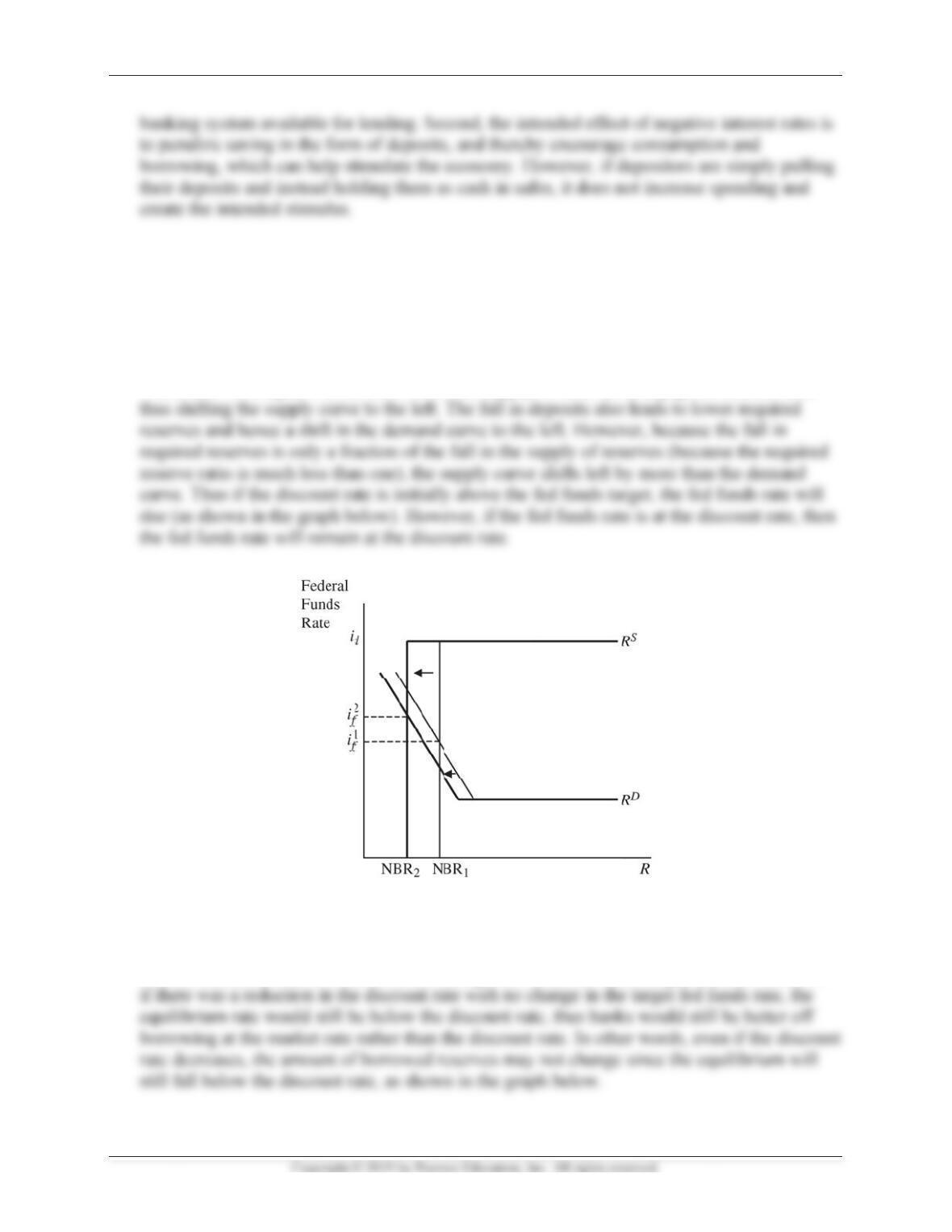

6. “The federal funds rate can never be above the discount rate.” Is this statement true, false,

or uncertain? Explain your answer.

Uncertain. In theory, the market for reserves model indicates that once the fed funds rate

reaches the discount rate, it would never surpass the discount rate since banks would then

7. “The federal funds rate can never be below the interest rate paid on excess reserves.” Is this

statement true, false, or uncertain? Explain your answer.

Uncertain. In theory, the market for reserves model indicates that once the fed funds rate

reaches the interest rate on excess reserves, it would never go below this rate since banks

8. Why is paying interest on excess reserves an important tool for the Federal Reserve in

managing crises?

9. Why are repurchase agreements used to conduct most short-term monetary policy

operations, rather than the simple, outright purchase and sale of securities?

10. Open market operations are typically repurchase agreements. What does this tell you about

the likely volume of defensive open market operations relative to the volume of dynamic open

market operations?

11. Following the global financial crisis in 2008, assets on the Federal Reserve’s balance sheet

increased dramatically, from approximately $800 billion at the end of 2007 to $3 trillion by

2011. Many of the assets held are longer-term securities acquired through various loan

programs instituted as a result of the crisis. In this situation, how could reverse repos

(matched sale–purchase transactions) help the Fed reduce its assets held in an orderly

fashion, while reducing potential inflationary problems in the future?

Because of the large amount of liquidity in banks and the financial system, this could

eventually lead to substantial inflation problems as liquidity in the form of excess reserves

12. “Discount loans are no longer needed because the presence of the FDIC eliminates the

possibility of bank panics.” Is this statement true, false, or uncertain?

13. What are the disadvantages of using loans to financial institutions to prevent bank panics?

Providing loans to financial institutions creates a moral hazard problem. If firms know that

14. “Considering that raising reserve requirements to 100% makes complete control of the

money supply possible, Congress should authorize the Fed to raise reserve requirements to

this level.” Discuss.

One problem with this proposal is that it provides perfect control over the official measure of

15. Compare the methods of controlling the money supply—open market operations, loans to

financial institutions, and changes in reserve requirements—on the basis of the following

criteria: flexibility, reversibility, effectiveness, and speed of implementation.

Open market operations are more flexible, reversible, and faster to implement than the other

16. What are the advantages and disadvantages of quantitative easing as an alternative to

conventional monetary policy when short-term interest rates are at the zero lower bound?

Since short-term interest rates cannot be lowered below the zero bound in this environment,

17. Why is the composition of the Fed’s balance sheet a potentially important aspect of monetary

policy during an economic crisis?

By purchasing particular types of securities, the Fed can impact interest rates and liquidity in

18. What is the main advantage and the main disadvantage of an unconditional policy

commitment?

Mishkin • Instructor’s Manual for The Economics of Money, Banking, and Financial Markets, Twelfth Edition 172

19. In which economic conditions would a central bank want to use a “forward-guidance”

strategy? Based on your previous answer, can we easily measure the effects of such a

strategy?

In general a central bank would use a strategy of “forward guidance” when other types of

conventional tools of monetary policy cannot affect the economy in the desired way. In

20. How do the monetary policy tools of the European System of Central Banks compare to the

monetary policy tools of the Fed? Does the ECB have a discount lending facility? Does the

ECB pay banks an interest rate on their deposits?

In general the set of monetary policy tools available to the ECB is quite similar to the one at

the Fed’s disposal. The ECB has a discount lending facility, called the marginal lending

21. What is the main rationale behind paying negative interest rates to banks for keeping their

deposits at central banks in Sweden, Switzerland, and Japan? What could happen to these

economies if banks decide to loan their excess reserves, but no good investment

opportunities exist?

22. In early 2016 as the Bank of Japan began to push policy interest rates negative, there was a

sharp increase in sales for home in Japan. Why might this be, and what does it mean for the

effectiveness of negative interest rate policy?

Negative policy interest rates have the effect of making deposit rates at banks negative. Thus,

people can avoid negative returns on holding cash by simply pulling their money out of

Mishkin •

o

h

d

t

l

d

n

d

n

s

r

s

ANSW

E

23.

I

f a s

the s

u

The

s

T-ac

c

24.

Why

borr

o

In m

o

d

w

e

a

a

c

c

k

e

k

f

l

h

I

nstructor’s Ma

n

E

RS TO AP

P

w

itch occur

s

u

pply and d

e

s

witch from

c

ounts of C

h

is it that a d

e

o

wed reserv

e

o

st cases, th

e

n

ual for The Ec

o

P

LIED PR

O

s

from depo

s

e

mand anal

y

deposits int

o

h

apter 14, a

n

e

crease in t

h

e

s? Use the

s

e

discount ra

t

o

nomics of Mon

e

O

BLEMS

s

its into cur

r

y

sis of the m

a

o

currency l

o

n

d this lowe

r

h

e discount r

a

s

upply and d

e

t

e is set far

e

e

y, Banking, an

d

r

ency, what

h

a

rket for re

s

o

wers the a

m

r

s the suppl

y

a

te does not

e

mand anal

y

e

nough abov

e

d

Financial Mar

k

h

appens to

t

s

erves to ex

p

m

ount of res

y

of reserves

normally le

a

y

sis of the m

a

e the fed fu

n

k

ets, Twelfth E

d

t

he federal

fu

p

lain your a

n

erves as wa

s

at any give

n

a

d to an inc

r

a

rket for res

n

ds target ra

t

d

ition

fu

nds rate?

U

n

swer.

s

shown in t

h

n

interest ra

t

r

ease in

erves to exp

l

t

e such that,

e

173

U

se

h

e

t

e,

l

ain.

e

ven

25.

Usin

g

the f

e

else

c

a.

T

d

A

a

n

d

i

b

e

n

h

r

e

n

b

r

e

e

d

g

e

j

e

a

u

a

y

u

y

g

the supply

e

deral funds

c

onstant, un

d

T

he econom

y

d

eposits.

A

rise in che

c

n

d thus shif

t

i

scount rate,

and deman

d

rate, borro

w

d

er the follo

is surprisin

g

c

kable depo

s

t

s the deman

d

this then le

a

d

analysis o

f

w

ed reserve

s

wing situati

o

g

ly strong,

l

s

its leads to

a

d

curve to t

h

a

ds to a rise

i

f

the market

f

s

, and nonb

o

o

ns.

l

eading to a

n

a

rise in req

u

h

e right. If th

i

n the federa

l

f

or reserve

s

o

rrowed res

e

n

increase i

n

u

ired reserv

e

h

e federal fu

n

a

l funds rate.

s

, indicate w

e

rves, holdi

n

n

the amoun

t

e

s at any gi

v

n

ds rate is in

i

As shown b

hat happen

s

n

g everythin

g

t

of checkab

v

en interest

r

i

tially belo

w

elow, borro

w

s

to

g

le

r

ate,

w

the

w

ed

Mishkin •

b.

B

i

n

I

f

c.

T

T

s

e

r

a

d

d.

T

r

a

R

e

e

h

n

h

h

h

r

r

r

d

b

l

w

l

s

n

t

n

t

I

nstructor’s Ma

n

B

anks expect

n

the future.

f

banks exp

e

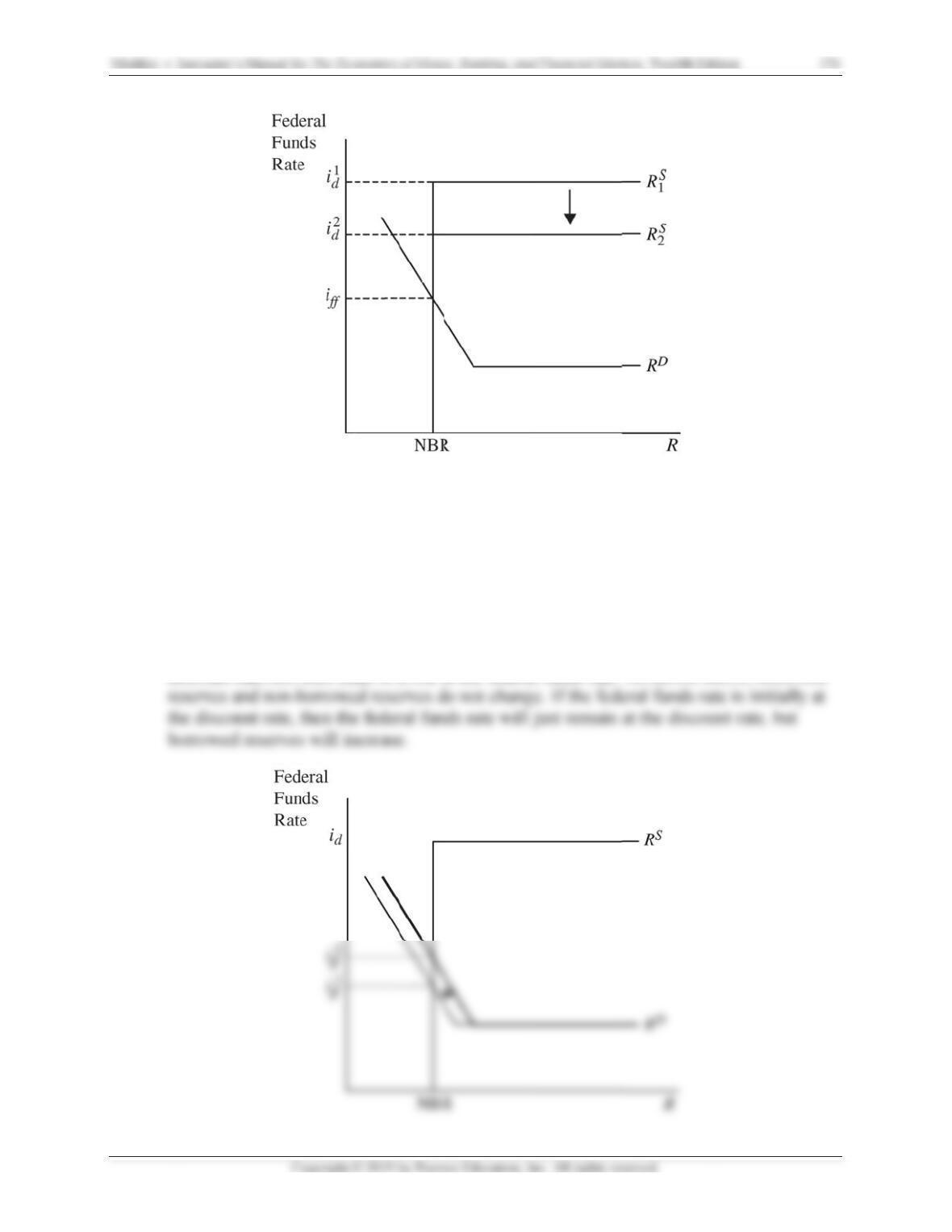

T

he Fed rais

e

T

o raise the t

a

e

curities, w

h

a

te will incr

e

i

scount rate

,

T

he Fed rais

e

a

te.

R

aising the i

n

n

ual for The Ec

o

an unusual

l

e

ct that an u

n

e

s the targe

t

a

rget fed fu

n

h

ich will shi

f

e

ase, and as

,

borrowed r

e

s the intere

s

n

terest rate o

n

o

nomics of Mon

e

l

y large inc

r

n

usually lar

g

t

federal fun

d

n

ds rate, the

f

t the suppl

y

long as the

e

eserves will

s

t rate on r

e

n

reserves a

b

e

y, Banking, an

d

r

ease in with

g

e increase i

n

d

s rate.

Fed will ha

v

y

of non-

b

or

r

e

quilibrium

remain the

s

e

serves abov

e

b

ove the cur

r

d

Financial Mar

k

h

drawals fro

m

n

withdraw

a

v

e to condu

c

r

owed reser

v

fed funds r

a

same.

e the curren

r

ent fed fun

d

k

ets, Twelfth E

d

m

checking

d

a

ls will occu

r

c

t an open

m

v

es to the le

f

a

te remains

b

n

t equilibriu

m

d

s rate mean

s

d

ition

d

eposit acc

o

r in the futu

r

m

arket sale o

f

t. The fed f

u

b

elow the

m

federal fu

n

s

that the flo

175

o

unts

r

e,

f

u

nds

n

ds

or of

h

n

n

n

n

o

n

o

e

e

e

t

f

t

f

f

e

f

,

Mishkin •

e.

T

A

i

n

u

n

f.

T

m

W

I

nstructor’s Ma

n

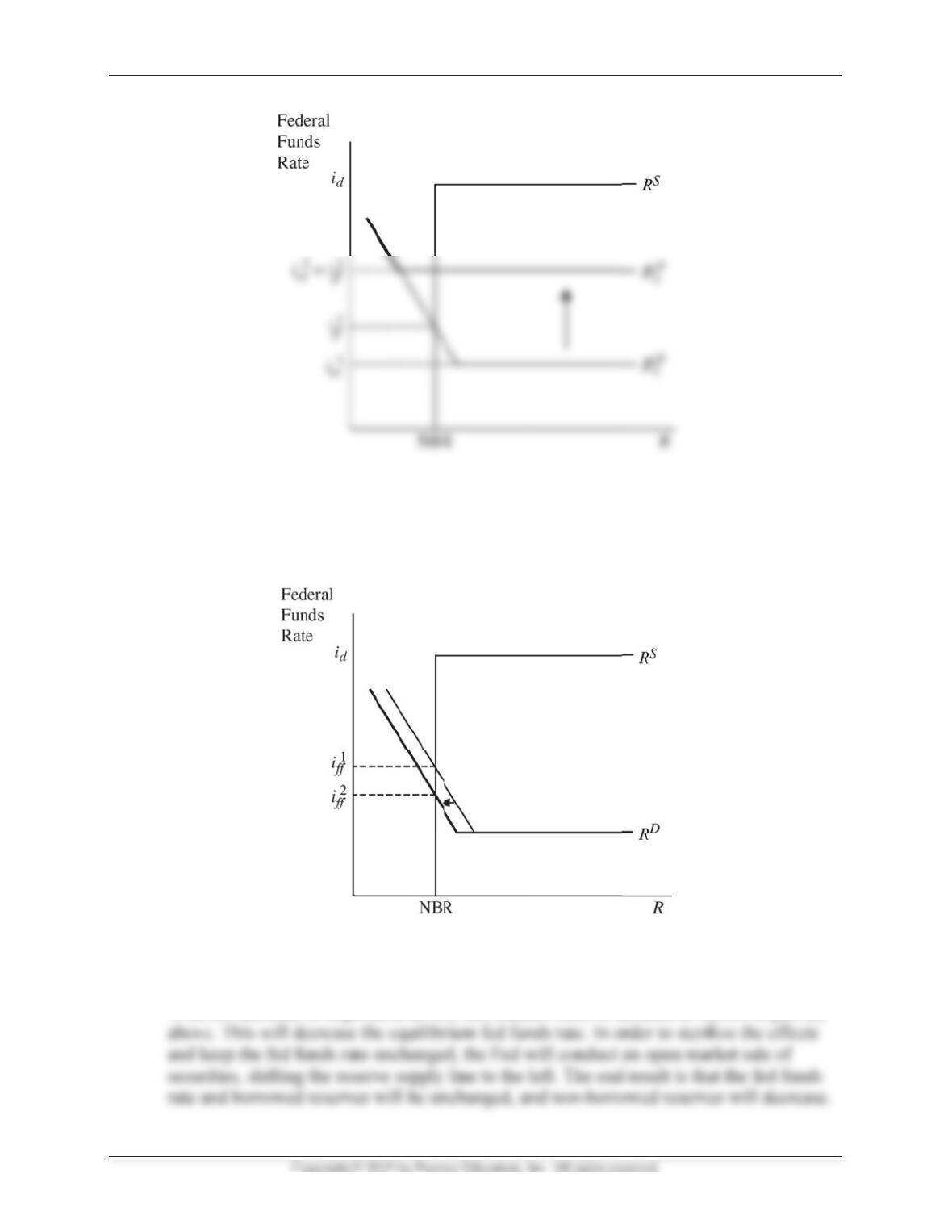

T

he Fed red

u

A

decrease i

n

n

terest rate.

T

n

changed.

T

he Fed red

u

m

arket sale

of

W

ith the dec

r

n

ual for The Ec

o

u

ces reserve

n

required re

s

T

he result is

u

ces reserve

of

securities.

r

ease in req

u

o

nomics of Mon

e

requiremen

t

s

erves shifts

that the fed

requiremen

t

u

ired reserv

e

e

y, Banking, an

d

t

s.

the demand

funds rate

d

t

s and then

o

e

s, this redu

c

d

Financial Mar

k

for reserves

d

ecreases, a

n

o

ffsets this a

c

es reserve

d

k

ets, Twelfth E

d

line to the l

e

n

d NBR and

a

ction by co

n

d

emand as s

h

d

ition

e

ft, at any gi

v

BR remain

n

ducting an

o

h

own in par

t

176

v

en

o

pen

t

(e)

w

w

e

e

r

o

Mishkin •

ANSW

E

1.

Go t

o

(NO

N

a.

C

i

n

m

b.

Is

W

N

f

u

m

a

m

s

a

n

s

h

o

h

n

o

w

n

e

e

n

n

2.

I

n D

e

(and

Fede

I

nstructor’s Ma

n

E

RS TO D

A

o

the St. Lou

N

BORRES)

a

C

alculate th

e

n

the federa

l

m

onth a year

s

your answ

e

W

hy or why

n

N

onborrowe

d

u

nds rate in

c

e

cember 20

0

it’s possibl

e

r

al Reserve

n

ual for The Ec

o

A

TA ANAL

Y

is Federal

R

a

nd the fede

r

e

percent ch

a

l

funds rate

f

earlier.

e

r to part (a

)

n

ot?

d

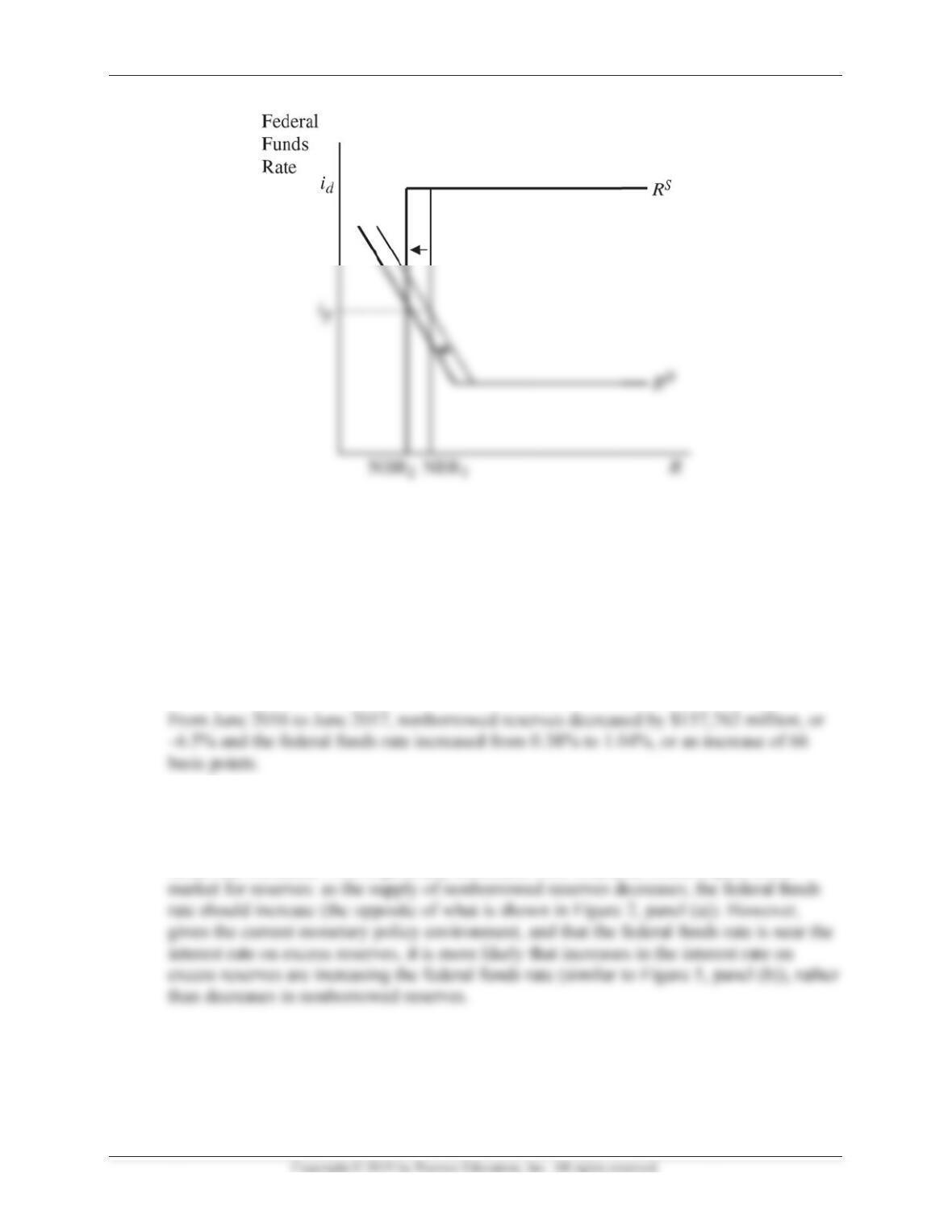

reserves d

e

c

reased. Thi

s

0

8, the Fed

s

e

that it will

s

FRED data

b

o

nomics of Mon

e

Y

SIS PRO

B

R

eserve FR

E

r

al funds ra

t

a

nge in non

b

f

or the most

)

consistent

w

e

creased mo

d

s

is generall

y

s

witched fro

m

s

witch back

b

ase, and fi

n

e

y, Banking, an

d

B

LEMS

E

D database,

t

e (FEDFU

N

b

orrowed re

s

recent mon

t

w

ith what y

o

d

estly over

t

y

consistent

m

a point fe

d

to a point t

a

n

d data on t

h

d

Financial Mar

k

,

and find d

a

N

DS).

s

erves and t

h

t

h of data a

v

o

u expect fr

o

t

he one yea

r

with what

y

d

eral funds

t

a

rget in the

f

h

e federal f

u

k

ets, Twelfth E

d

a

ta on nonb

o

h

e percenta

g

v

ailable and

f

o

m the mar

k

r

pe

r

iod, wh

i

y

ou would e

x

t

arget to a r

a

f

uture). Go

t

u

nds targets

/

d

ition

o

rrowed res

e

g

e point ch

a

f

or the sam

e

k

et for reser

v

i

le the feder

a

x

pect in the

a

nge target

t

o the St. Lo

u

/

ranges

177

e

rves

a

nge

e

v

es?

a

l

u

is

Mishkin • Instructor’s Manual for The Economics of Money, Banking, and Financial Markets, Twelfth Edition 178

(DFEDTAR, DFEDTARU, DFEDTARL) and the effective federal funds rate (DFF).

Download into a spreadsheet the data from the beginning of 2006 through the most current

data available.

a. What is the current federal funds target/range, and how does it compare to the effective

federal funds rate?

b. When was the last time the Fed missed its target or was outside the target range? By how

much did it miss?

The last time the Fed missed its target was when it switched from a target of between

c. For each daily observation, calculate the “miss” by taking the absolute value of the

difference between the effective federal funds rate and the target (use the abs(.) function).

For the periods in which the rate was a range, calculate the absolute value of the “miss”

as the amount by which the effective federal funds rate was above or below the range.

What was the average daily miss between the beginning of 2006 and the end of 2007?

What was the average daily miss between the beginning of 2008 and December 15,

2008? What is the average daily miss for the period from December 16, 2008, to the most

current date available? Since 2006, what was the largest single daily miss? Comment on

the Fed’s ability to control the federal funds rate during these three periods.

From the beginning of 2006 to the end of 2007, the average daily miss was 0.05, or 5

basis points. From the beginning of 2008 to December 15, 2008, the average daily miss

was 0.22, or 22 basis points. From December 16, 2008 through July 13, 2017, the federal