1

2

3

4

5

6

7

8

9

13

14

15

19

20

16

17

21

22

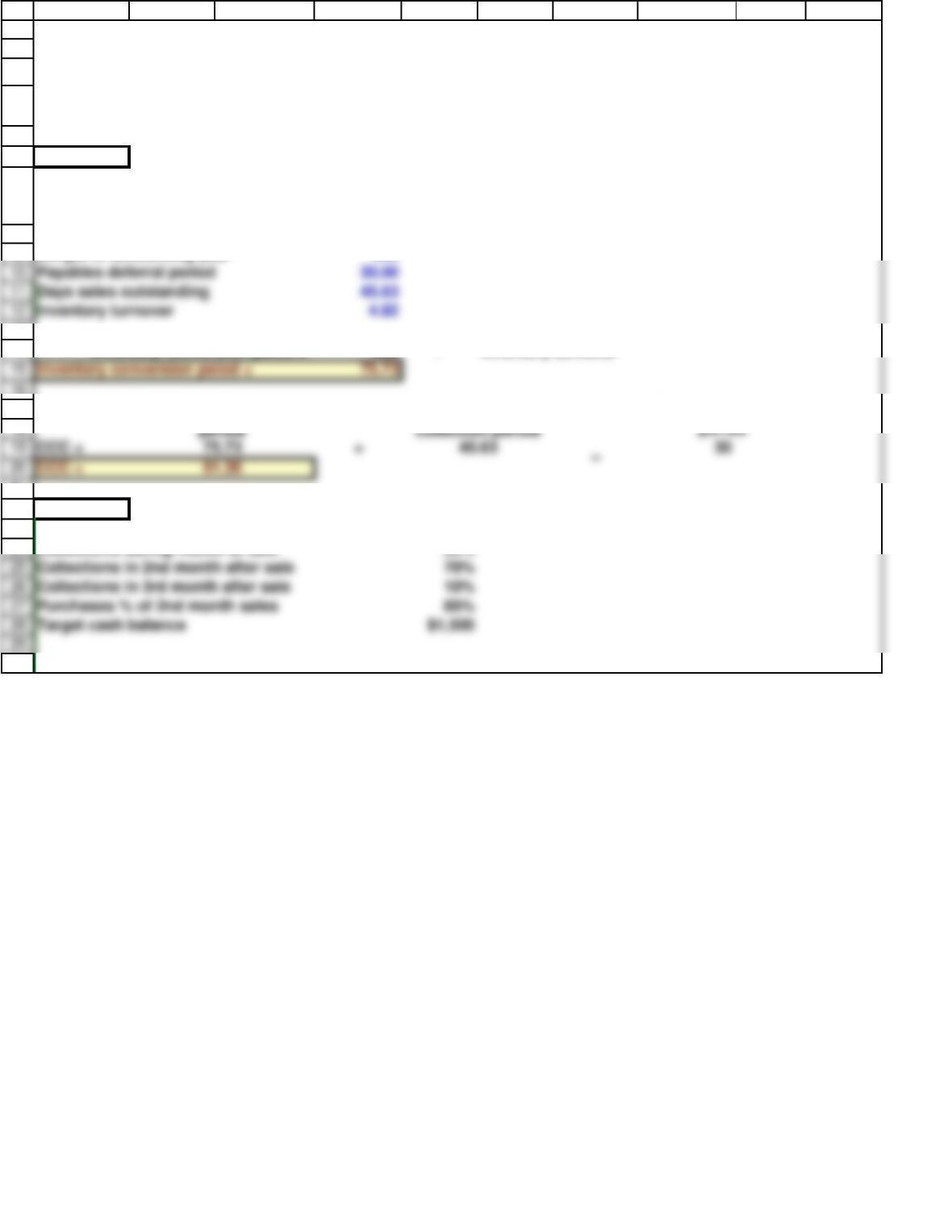

Collections in 2nd month after sale 70%

Collections in 3rd month after sale 10%

Purchases % of 2nd month sales 85%

Target cash balance $1,500

23

24

30

A B C D E F G H I J

15 Case model

PART D

Length of accounting year 365

365 / Inventory turnover

PARTS F & G

Discount given on sales (2/10) 2%

Collections during month of sale 20%

Inventory conversion peiod =

Chapter 15. Working Capital Management

9/12/2022 17:22

Assume that SKI’s payables deferral period is 30 days. Now calculate the firm’s cash conversion cycle estimating

the inventory conversion period as 365/Inventory turnover.

12/9/2018

This spreadsheet model is designed to be used in conjunction with the chapter’s integrated case and the related

PowerPoint slide presentation.

−

Payables deferral

CCC =

Inventory conversion

+

Receivables

Payables deferral period 30.00

Days sales outstanding 45.63

Inventory turnover 4.82

31

32

33

34

35

36

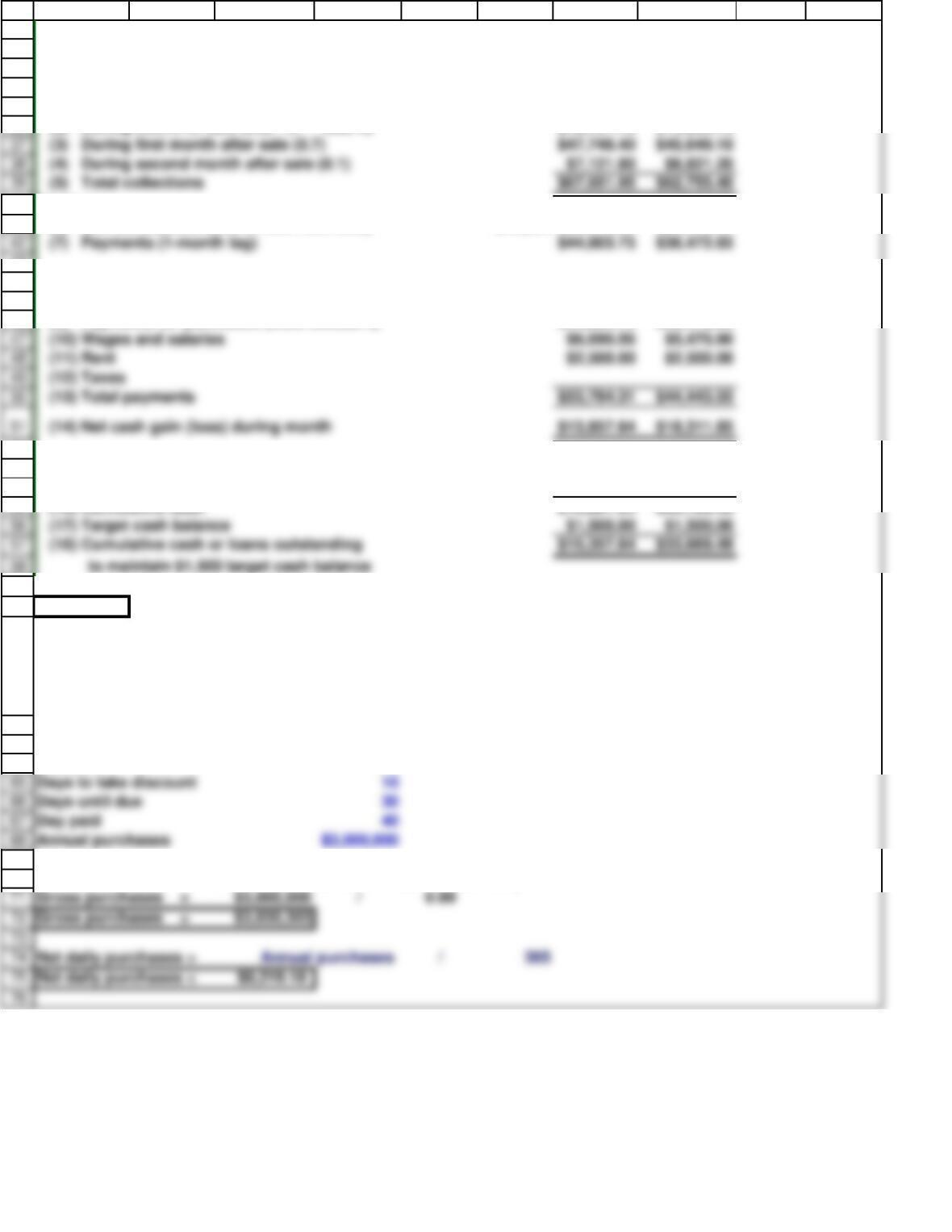

(7) Payments (1-month lag) $44,603.75 $36,472.65

(10) Wages and salaries $6,690.56 $5,470.90

(11) Rent $2,500.00 $2,500.00

(12) Taxes

(13) Total payments $53,794.31 $44,443.55

57

(17) Target cash balance $1,500.00 $1,500.00

40

41

43

44

45

46

52

53

54

55

59

60

Days to take discount 10

Days until due 30

Day paid 40

Annual purchases $3,000,000

61

62

63

64

69

70

71

72

74

75

A B C D E F G H I J

TABLE IC 16.2 Cash Budget for January and February

Nov Dec Jan Feb March April

I. Collections and purchases worksheet

(1) Sales (gross) $71,218 $68,212 $65,213.00 $52,475.00 $42,909 $30,524

Collections

(2) During month of sale (0.2) × (1 – disc%) $12,781.75 $10,285.10

Purchases

(6) 0.85 (forecasted sales 2 mos from now) $44,604 $36,472.65 $25,945.40

II. Cash gain or loss for month

(8) Total collections (from Section I) $67,651.95 $62,755.40

(9) Payments for purchases (from Section I) $44,603.75 $36,472.65

III. Cash surplus or loan requirement

(15) Cash at beginning of month $3,000.00 $16,857.64

(16) Cumulative cash

$16,857.64 $35,169.49

PART M

Length of accounting year 365

Discount 1%

Gross purchases = Annual purchases / (1 – Discount%)

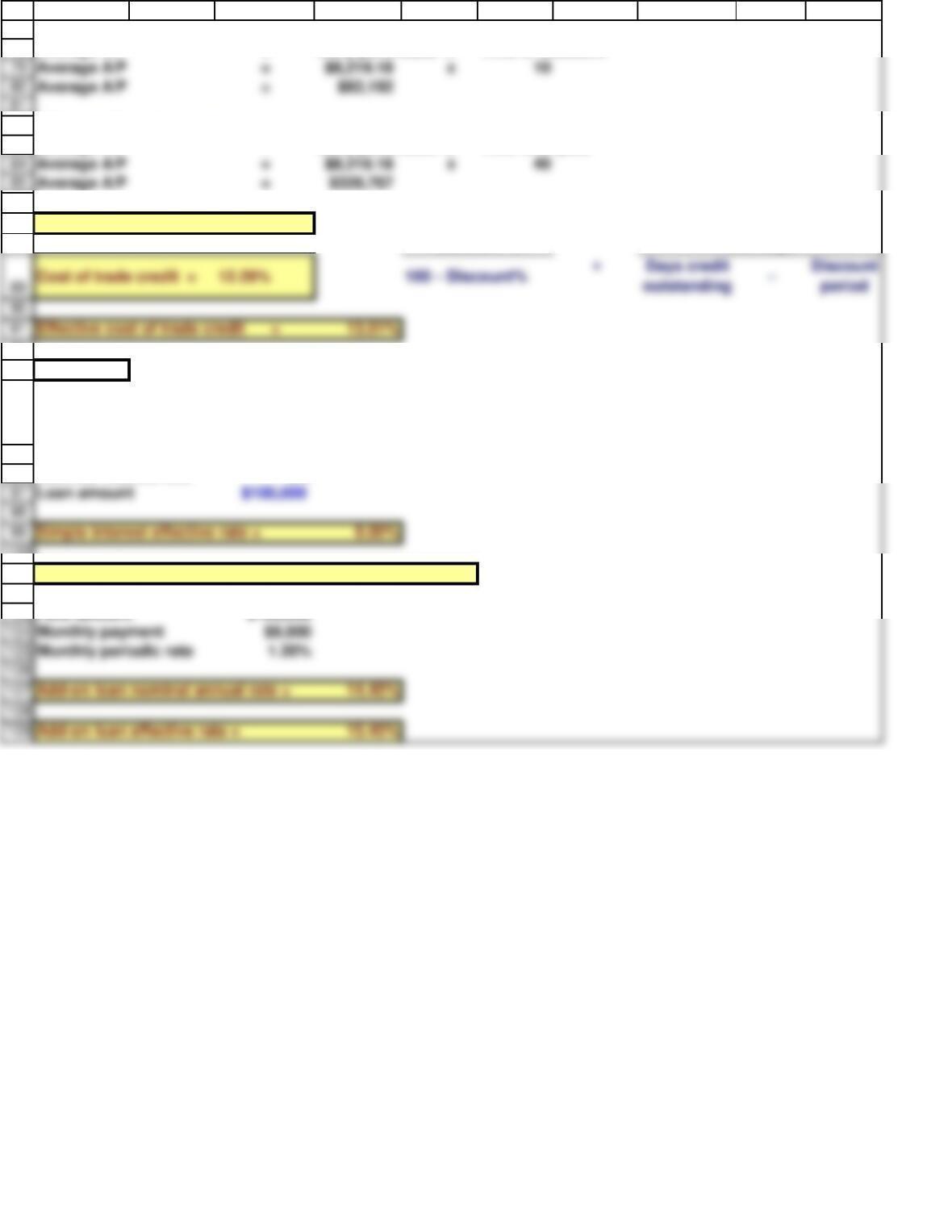

Assume that SKI buys on terms of 1/10, net 30, but that it can get away with paying on the 40th day if it chooses

not to take discounts. Also assume that it purchases $3 million of components per year, net of discounts. How

much free trade credit can the company get, how much costly trade credit can it get, and what is the percentage

cost of the costly credit? Should SKI take discounts? Why or why not?

39

(3) During first month after sale (0.7) $47,748.40 $45,649.10

(4) During second month after sale (0.1) $7,121.80 $6,821.20

Average A/P = $8,219.18 x 40

Average A/P = $328,767

77

78

82

83

86

87

88

90

91

Effective cost of trade credit = 13.01%

92

93

98

99

Loan amount $100,000

Simple interest effective rate = 8.00%

94

95

96

100

101

106

107

108

109

Monthly payment $9,000

Monthly periodic rate 1.20%

Add-on loan nominal annual rate = 14.45%

Add-on loan effective rate = 15.45%

102

103

A B C D E F G H I J

Average A/P = Daily purchases x Time of discount

Average A/P = Daily purchases x Time until paid

Costly trade credit = $246,575

PART N

Nominal interest rate 8%

Approximate annual rate of add-on loan = 16.00%

Face amount $108,000

Take discounts:

Without taking discounts:

Suppose SKI decided to raise an additional $100,000 as a 1-year loan from its bank, for which it was quoted a rate

of 8%. What is the effective annual cost rate assuming simple interest and add-on interest on a 12-month

installment loan?

Discount %

365 Days

Average A/P = $8,219.18 x 10

Average A/P = $82,192