Chapter 15: Working Capital Management

Learning Objectives

427

Chapter 15

Working Capital Management

Learning Objectives

After reading this chapter, students should be able to do the following:

◆ Explain how different amounts of current assets and current liabilities affect firms’ profitability and

thus their stock prices.

◆ Explain how companies decide on the proper amount of each current asset—cash, marketable

securities, accounts receivable, and inventory.

428

Lecture Suggestions

Chapter 15: Working Capital Management

Lecture Suggestions

We have never found working capital an interesting topic to students; hence it is, to us, a somewhat

more difficult subject to teach than most. Perhaps that’s because it comes near the end of the course,

when everyone is tired. More likely, though, the problem is that working capital management is really

more a matter of operating efficiently than thinking conceptually correctly—i.e., it is more practice than

DAYS ON CHAPTER: 4 OF 56 DAYS (50-minute periods)

Chapter 15: Working Capital Management

Answers and Solutions

429

Answers to End-of-Chapter Questions

15-1 The DuPont equation is: ROE = Profit margin on sales x Total assets turnover x Leverage factor.

A relaxed current assets investment policy means that relatively large amounts of cash,

15-2 The cash conversion cycle is the length of time funds are tied up in working capital, or the length

of time between paying for working capital and collecting cash from the sale of the working

15-3 When most of us use the term cash, we mean currency (paper money and coins) plus bank

demand deposits. However, when corporate treasurers use the term, they often mean currency

15-4 Firms need to forecast their cash flows. If they will need additional cash, they should line up

funds well in advance, while if they will generate surplus cash, they should plan for its productive

use. The primary forecasting tool is the cash budget.

Cash budgets can be of any length, but firms typically develop a monthly cash budget for the

coming year and a daily cash budget at the start of each month. The monthly budget is good for

long-range planning, while the daily budget gives a more precise picture of the actual cash flows.

If cash inflows and outflows do not occur uniformly during each month, then the actual funds

needed might be quite different from the indicated monthly amounts.

15-5 The four key factors in a firm’s credit policy are: (1) credit period, the length of time buyers are

given to pay for their purchases; (2) discounts, price reductions given for early payment; (3)

credit standards, the required financial strength of acceptable credit customers; and (4) collection

policy, procedures used to collect past due accounts. A relaxed credit policy would call for a

430

Answers and Solutions

Chapter 15: Working Capital Management

15-6 The maturity matching, or “self–liquidating,” approach calls for matching asset and liability

maturities. All of the fixed assets plus the permanent current assets are financed with long-term

capital, but temporary current assets are financed with short-term debt. A more aggressive

financing approach would involve financing some of its permanent assets with short-term debt.

The reason for adopting the aggressive policy is to take advantage of the fact that the yield curve

15-7 Trade credit is the debt arising from credit sales and recorded as an account receivable by the

seller and as an account payable by the buyer. Free trade credit is the credit received during the

discount period, while the costly trade credit is the credit taken in excess of free trade credit,

15-8 The prime rate is the published interest rate charged by commercial banks to large, strong

borrowers. The commercial paper rate is the interest rate charged on unsecured, short-term

promissory notes of large firms, usually issued in denominations of $100,000 or more. The

commercial paper rate would be somewhat below the prime rate. The simple interest rate is the

rate charged on a bank loan that is paid monthly, and the principal is payable on demand. The

Chapter 15: Working Capital Management

Answers and Solutions

431

15-9 Accruals are continually recurring short-term liabilities, especially accrued wages and accrued

taxes. Accruals arise automatically, or spontaneously, from a firm’s operations, hence they are

15–10 A/R Sales Profit

a. The firm restricts its credit standards. – – 0

b. The terms of trade are changed from 2/10, net 30, to 3/10, net 30. 0 + 0

c. The terms are changed from 2/10 net 30, to 3/10, net 40. 0 + 0

d. The credit manager gets tough with past-due accounts. – – 0

Explanations:

Solutions to End-of-Chapter Problems

15-1 1. Sales = $12,000,000; Inventory = $3,000,000; A/R = $3,250,000; A/P = $1,250,000; COGS

= 0.75(Sales); Interest on bank loan = 8%; CCC = ?

CCC = Inventory conversion period + Average collection period – Payables deferral period.

Inventory conversion period =

dayper sold goods ofCost

Inventory

Payables deferral period =

sold/365 goods ofCost

Payables

2. Lower inventories and receivables by 10% each and increase payables by 10%. Sales and

COGS remain the same.

Inventory = $3,000,000 0.9 = $2,700,000.

Calculate new CCC:

000,700,2$

= 109.50 days.

000,925,2$

Chapter 15: Working Capital Management

Answers and Solutions

433

000,375,1$

3. Cash freed up:

Inventory = (121.67 – 109.50) $24,657.53 = $300,082.19.

4. Impact on pretax profits: $750,000 0.08 = $60,000 increase in pretax profits.

15-2 Sales = $12,000,000; A/R = $1,500,000; DSO = ?

DSO =

Sales/365

sReceivable

If all customers paid on time (assuming that it makes no sense for customers to pay earlier than

30 days), then the firm’s DSO = 30 days. If customers paid on time, the firm’s A/R = 30

15-3 Purchases = $8,000,000; terms = 3/5 net 55; currently pays on Day 5 and takes discounts.

Forgoes discounts; additional credit = ?

$8,000,000/365 50 days = $1,095,890.41 $1,095,890.

434

Answers and Solutions

Chapter 15: Working Capital Management

15-4 a.

cy cle

conversion

Cash

=

period

deferral

Payables

period

collection

sReceivable

period

conversion

Inventory

−+

c. Step 1: Calculate inventory balance from inventory conversion period:

64 =

365

235,578,2$

75.0

Inventory

15-5 a. 0.4(10) + 0.6(70) = 46 days.

Customers who do not take the discount and pay on Day 30:

1. Nominal cost: 3/97 365/20 = 56.44%.

d. Customers who do not take the discount and pay on Day 70:

1. Nominal cost: 3/97 365/60 = 18.81%.

e. 0.4(10) + 0.6(30) = 22 days. $1,921,000/365 = $5,263.0137 sales per day.

15-6 a. Cash conversion cycle = 22 + 40 – 30 = 32 days.

15-7 a. Calculate inventory:

Inventory turnover ratio = Sales/Inventory

Receivables collection period = DSO = 37 days.

Cash

Payables

sReceivable

Inventory

b. Total assets = Inventory + Receivables + Fixed assets

c. 9.9 =

Inventory

000,121$

436

Answers and Solutions

Chapter 15: Working Capital Management

12,222.22$

15-8 a. Return on equity may be computed as follows:

Restricted Moderate Relaxed

Current assets

(% of sales Sales) $ 900,000 $1,000,000 $1,200,000

Fixed assets 1,000,000 1,000,000 1,000,000

b. No, this assumption would probably not be valid in a real-world situation. A firm’s current

asset policies, particularly regarding accounts receivable, such as discounts, collection period,

c. As the answers to part a indicate, the restricted policy leads to a higher expected return.

However, as the current asset level is decreased, presumably some of this reduction comes

from accounts receivable. This can be accomplished only through higher discounts, a shorter

collection period, and/or tougher collection policies. As outlined above, this would in turn

15-9 a. Presently, FGC has 7 days of collection float; under the lockbox system, this would drop to 5

days.

$2,300,000 7 days = $16,100,000

FGC can reduce its cash balances by the $4,600,000 reduction in negative float. This would

be a one-time cash flow, unless the firm grows. Then cash flow would increase by the

differential growth in collections.

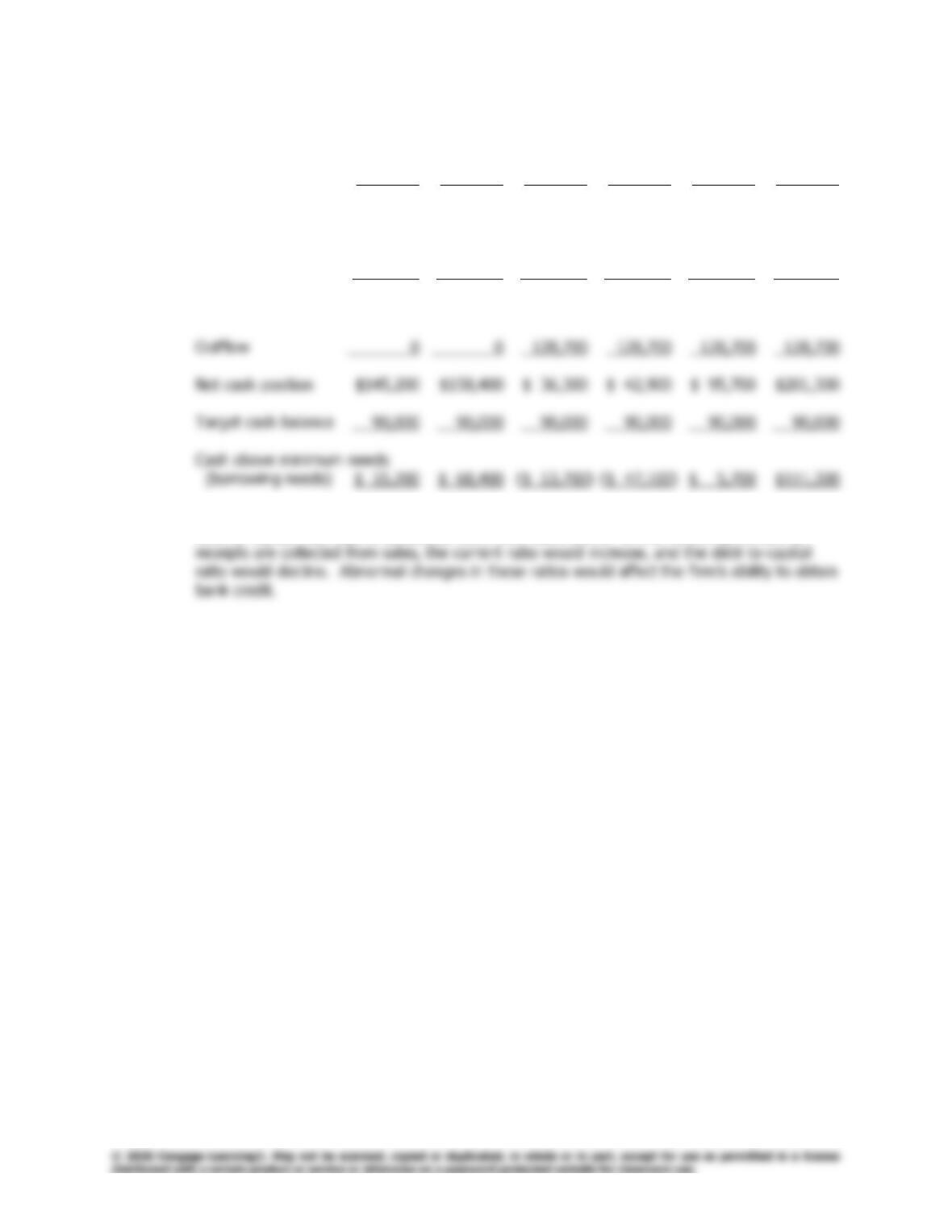

15-10 a.

May June July August September October November December January

Collections and purchases worksheet

Sales (gross) $180,000 $180,000 $360,000 $540,000 $720,000 $360,000 $360,000 $90,000 $180,000

Collections

During month of sale 18,000 18,000 36,000 54,000 72,000 36,000 36,000 9,000

During 1st month after sale 135,000 135,000 270,000 405,000 540,000 270,000 270,000

Cash gain or loss for month

Collections $198,000 $351,000 $531,000 $657,000 $414,000 $333,000

Payments for labor and raw materials 90,000 126,000 882,000 306,000 234,000 162,000

General and administrative salaries 27,000 27,000 27,000 27,000 27,000 27,000

Design studio payment 180,000

Total payments $128,700 $164,700 $983,700 $524,700 $272,700 $263,700

Loan requirement or cash surplus

Cash at start of month $132,000 $201,300 $387,600 ($65,100) $67,200 $208,500

Cumulative cash $201,300 $387,600 ($65,100) $67,200 $208,500 $277,800

b. The cash budget indicates that Helen will have surplus funds available during July, August,

November, and December. During September the company will need to borrow $155,100.

c. In a situation such as this, where inflows and outflows are not synchronized during the

month, it may not be possible to use a cash budget centered on the end of the month. The

cash budget should be set up to show the cash positions of the firm on the 5th of each

438

Answers and Solutions

Chapter 15: Working Capital Management

have offset the outflows, and by July 30 we see that the monthly totals agree with the cash

budget developed earlier in part a.

7/2/19 7/4/19 7/5/19 7/6/19 7/14/19 7/30/19

Opening balance $132,000 132,000 132,000 $132,000 $132,000 $132,000

Cumulative inflows

(1/30 receipts

no. of days) 13,200 26,400 33,000 39,600 92,400 198,000

Total cash available $145,200 $158,400 $165,000 $171,600 $224,400 $330,000

d. The months preceding peak sales would show a decreased current ratio and an increased

debt-to-capital ratio due to additional short-term bank loans. In the following months as

Chapter 15: Working Capital Management

Comprehensive/Spreadsheet Problem

439

Comprehensive/Spreadsheet Problem

Note to Instructors:

The partial solution for parts a and b of this problem are provided at the back of the text;

however, the solutions to parts c and d are not. Instructors can access the

Excel

file on the

textbook’s website.

15–11 See problem 15-10 parts a through d on the preceding two pages.

The “Sales adjustment factor” can be used to cause sales to vary from the base levels. Similarly,

we can change the percentage of late-paying customers. Here is the relevant data table:

Change

in Sales

$155,100 0% 15% 30% 45% 60% 75% 90%

–100% $ 2,296,200 $ 2,296,200 $ 2,296,200 $ 2,296,200 $ 2,296,200 $ 2,296,200 $ 2,296,200

–50% $ 1,040,700 $ 1,054,200 $ 1,067,700 $ 1,081,200 $ 1,094,700 $ 1,108,200 $ 1,121,700

Maximum Loan Required

% Collections in 2nd month

440

Integrated Case

Chapter 15: Working Capital Management

Integrated Case

15-12

Ski Equipment Inc.

Managing Current Assets

Dan Barnes, financial manager of Ski Equipment Inc. (SKI), is excited, but

apprehensive. The company’s founder recently sold his 51% controlling block

of stock to Kent Koren, who is a big fan of EVA (Economic Value Added). EVA

is found by taking the after-tax operating profit and subtracting the dollar cost

of all the capital the firm uses:

If EVA is positive, the firm is creating value. On the other hand, if EVA is

negative, the firm is not covering its cost of capital and stockholders’ value is

being eroded. Koren rewards managers handsomely if they create value, but

those whose operations produce negative EVAs are soon looking for work.

Koren frequently points out that if a company can generate its current level of