CHAPTER 15

A Dynamic Model of Economic

Fluctuations

Notes to the Instructor

Chapter Summary

Part V of the text presents some advances in macroeconomic theory that clarify our

understanding of the economy. This part of the text begins with Chapter 15, which extends the

analysis of short–run fluctuations to consider the response over time of key macroeconomic

variables. The chapter does this by constructing a dynamic model of aggregate demand and

Comments

The material presented in this chapter is more difficult than the AD–AS, IS–LM models analyzed

in earlier chapters. But because many of the building blocks have already been discussed,

instructors should have a relatively easy time motivating the approach, and students should

readily see the connections to what they have already learned. The model consists of five

equations—a relatively large number for undergraduates to work with—but the discussion

surrounding the model requires only basic algebra. Dynamic solution of the model is done

through simulation exercises, with figures illustrating the time paths of different variables.

Faculty who don’t feel comfortable with going through the algebra of the model’s details can

still use the chapter effectively by relying on the simulation figures to discuss how various

shocks and changes in policy affect the economy over time.

Use of the Dismal Scientist Web Site

Go to the Dismal Scientist Web site and download annual data on the federal funds rate, real

GDP, and the GDP price index over the past 30 years. Compute the trend level of real GDP over

time by graphing it and choosing as endpoints 1979 and 2006 (cyclical peaks). Now construct a

GDP gap series by subtracting your trend GDP from actual GDP. Compute the inflation rate

using the GDP price index. Using the specification of the Taylor rule discussed in Chapter 15,

compute predictions for the federal funds rate over this time period. Now compare your

predictions with the actual federal funds rate. When are they similar and when are they different?

Does the rule fit better after the shift in 1984 to interest–rate targeting and away from monetary–

aggregate targeting by the Federal Reserve? Assess whether your findings suggest that monetary

344 | CHAPTER 15 A Dynamic Model of Economic Fluctuations

Chapter Supplements

This chapter includes the following supplements:

15-2 The Microeconomics of Labor Supply

15-4 Involuntary Unemployment and Overqualification

15-6 Real Business Cycles and Random Walks

15-8 Volatility and Growth

15-9 How Long Is the Long Run? Part Four

15–10 Additional Readings

Lecture Notes | 345

Lecture Notes

Introduction

The chapter builds on the earlier development of the AD–AS, IS–LM models by developing a

dynamic model of aggregate demand and aggregate supply. This model is another way to study

15–1 Elements of the Model

Many of the variables in the model are familiar from previous chapters, but now we will use a

“t” subscript to denote the time period. Thus, total output and national income in period “t” will

be given as Yt and, similarly, in period “t–1” it is given as Yt–1. The model is composed of five

equations, which we describe below.

Output: The Demand for Goods and Services

The demand for goods and services in the economy is determined by:

consumption spending by households, with the response depending on the size of the parameter

α

(a higher interest rate might also appreciate the real exchange rate, dampening net exports).

The demand for goods and services grows with the natural level of output. This feature allows us

to consider long–run economic growth in this model. Finally, the demand shock represents

The Real Interest Rate: The Fisher Equation

We define the real interest as equal to the nominal rate minus expected inflation:

rt = it – Et

π

t+1

which is similar to the Fisher equation. The variable Et

π

t+1 represents the period t expectation of

inflation for period t + 1. Notation and timing reflect the convention of dating variables by when

they are known. Accordingly, the ex ante real interest rate rt and the nominal interest rate it are

Inflation: The Phillips Curve

The model uses a standard Phillips curve, similar to the one derived in Chapter 14:

346 | CHAPTER 15 A Dynamic Model of Economic Fluctuations

Expected Inflation: Adaptive Expectations

Expectations of inflation are formed adaptively, so that last period’s inflation rate is used as the

expectation for inflation in the current period:

Et−1

π

t=

π

t−1.

The Nominal Interest Rate: The Monetary Policy Rule

The last equation of the model is a rule for monetary policy in which the central bank sets a

target for the nominal interest rate based on inflation and output:

it=

π

t+

ρ

+

θπ

(

π

t–

π

t

*)+

θ

YYt−Yt

( )

.

The policy rule assumes that the central bank responds to deviation in inflation from its

target inflation rate

π

t

* and to deviations in output relative to its natural level

Yt

Yt

Yt

. Policy

parameters,

θπ

and

θ

Y, determine how much the central bank responds to these deviations. In the

instrument for the central bank, here the policy instrument is the interest rate. The implicit

assumption here is that the central bank adjusts the money supply as necessary to achieve its

target for the interest rate. Choosing the interest rate as the policy instrument is more realistic as

it closely matches the practice of central banks around the world.

Case Study: The Taylor Rule

funds rate rises by the same amount—0.5 percent. If instead inflation falls below 2 percent or

GDP falls below its natural rate, the federal funds rate falls accordingly. John Taylor’s monetary

rule may be the rule that the Fed implicitly follows in setting policy.

According to the Taylor rule, if inflation and output are low enough, then the nominal

interest rate should be negative. This situation occurred during the financial crisis of 2008–2009.

Lecture Notes | 347

Figure 1: The Unemployment Rate and the Natural Rate of Unemployment in the United States.

15–2 Solving the Model

The five equations presented above determine the paths of the model’s five endogenous

variables: output Yt, the real interest rate rt, inflation πt, expected inflation Et–1πt, and the nominal

interest rate it. Before using the model to analyze the economy’s response to economic shocks,

we first describe the model’s long–run equilibrium.

π

t-1

Parameters

α

The responsiveness of the demand for goods and services to

the real interest rate

ρ

The natural rate of interest

ϕ

The responsiveness of inflation to output in the Phillips curve

π

π

ε

υ

348 | CHAPTER 15 A Dynamic Model of Economic Fluctuations

The Long–Run Equilibrium

Long–run equilibrium for the model is the situation in which there are no shocks and inflation is

constant over time. Applying this to the five equations of the model gives output and the real

The Dynamic Aggregate Supply Curve

To analyze the economy in the short run, we need to derive two equations that are the analogues

of the AD and AS equations of Chapter 14. The dynamic aggregate supply equation is the

Phillips curve, with lagged inflation substituted for expected inflation:

Figure 2

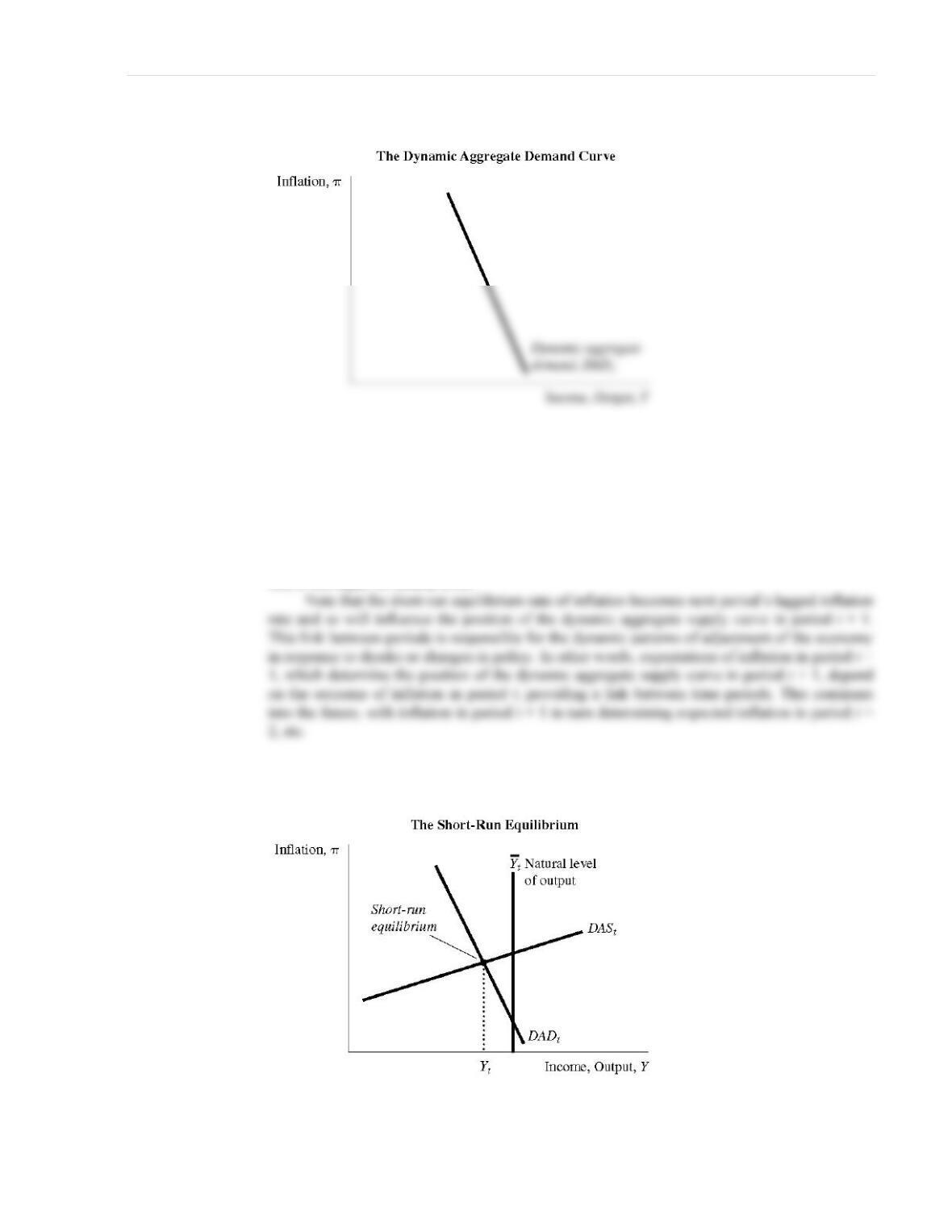

The Dynamic Aggregate Demand Curve

To derive the dynamic aggregate demand curve, start with the demand for goods and services

equation and substitute for the real interest rate using the Fisher equation. Next, eliminate the

nominal interest rate by using the monetary policy equation and substitute for expected inflation

using the equation for inflation expectations. Finally, cancel terms and rearrange the equation to

yield:

Yt=Yt– [

αθ π

/ (1+

αθ

Y)](

π

t–

π

t

*)+[1/ (1+

αθ

Y)]

ε

t.

(DAD)

This equation is represented as a downward–sloping schedule called the dynamic aggregate

demand curve when plotted with inflation on the y–axis and output plotted on the x–axis. Its slope

Lecture Notes | 349

Figure 3

The Short–Run Equilibrium

The intersection of the dynamic aggregate demand curve and the dynamic aggregate supply

curve determines the economy’s short–run equilibrium. These two relationships determine two

endogenous variables (inflation and output in period t), given the five other exogenous (or

predetermined) variables. These are the natural level of output, the target inflation rate, the

demand shock, the supply shock, and the previous period’s inflation rate. The short–run

equilibrium level of output can be less than, equal to, or greater than its natural level. In the long

run, it will equal its natural level.

Figure 4

15–3 Using the Model

We can use the model to assess the effects of change in the exogenous variables. To simplify the

analysis, we assume the economy is initially at its long–run equilibrium.

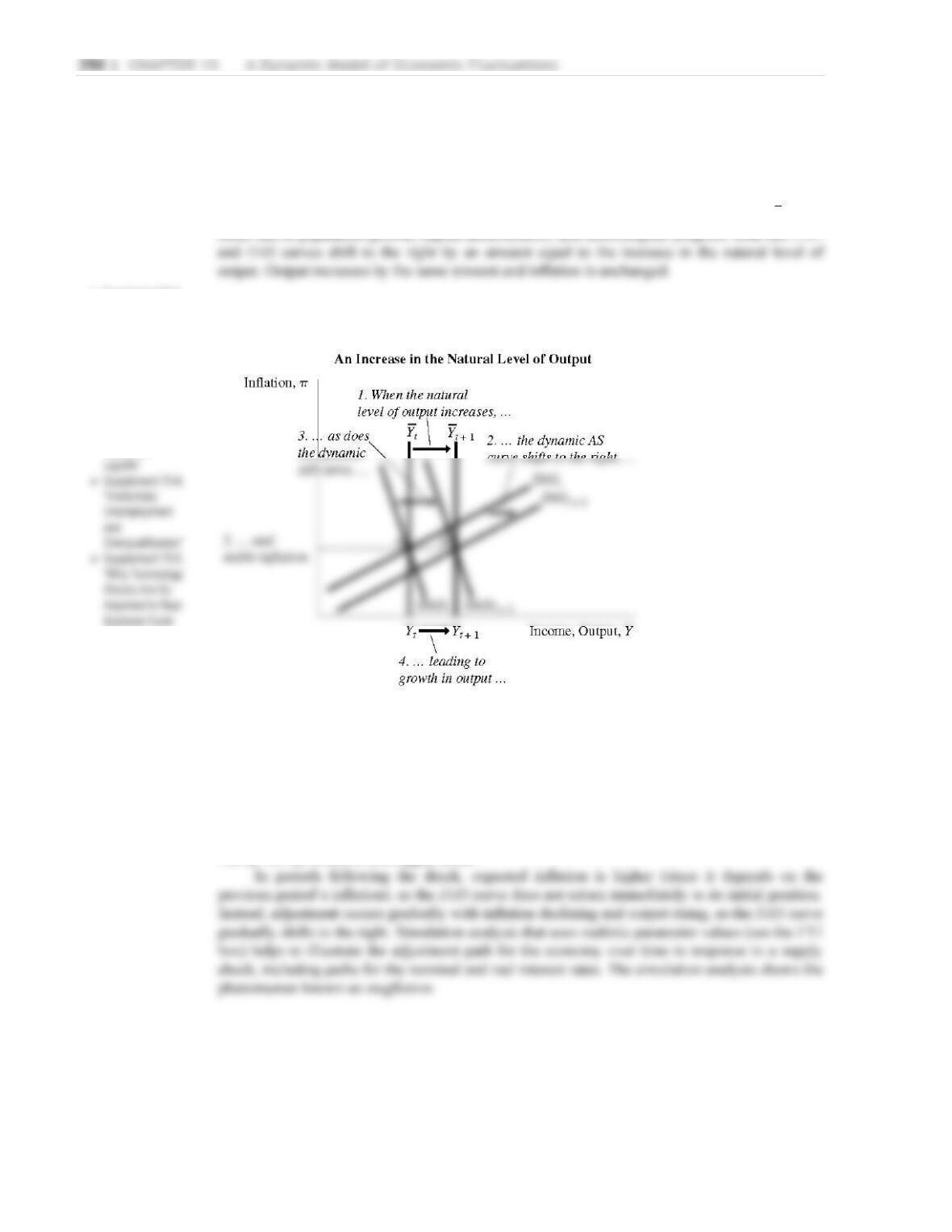

Long–Run Growth

As discussed in Chapters 8 and 9, increases over time in the natural level of output,

Yt

, may

occur due to population growth, capital accumulation, and technological progress. Both the DAD

Figure 5

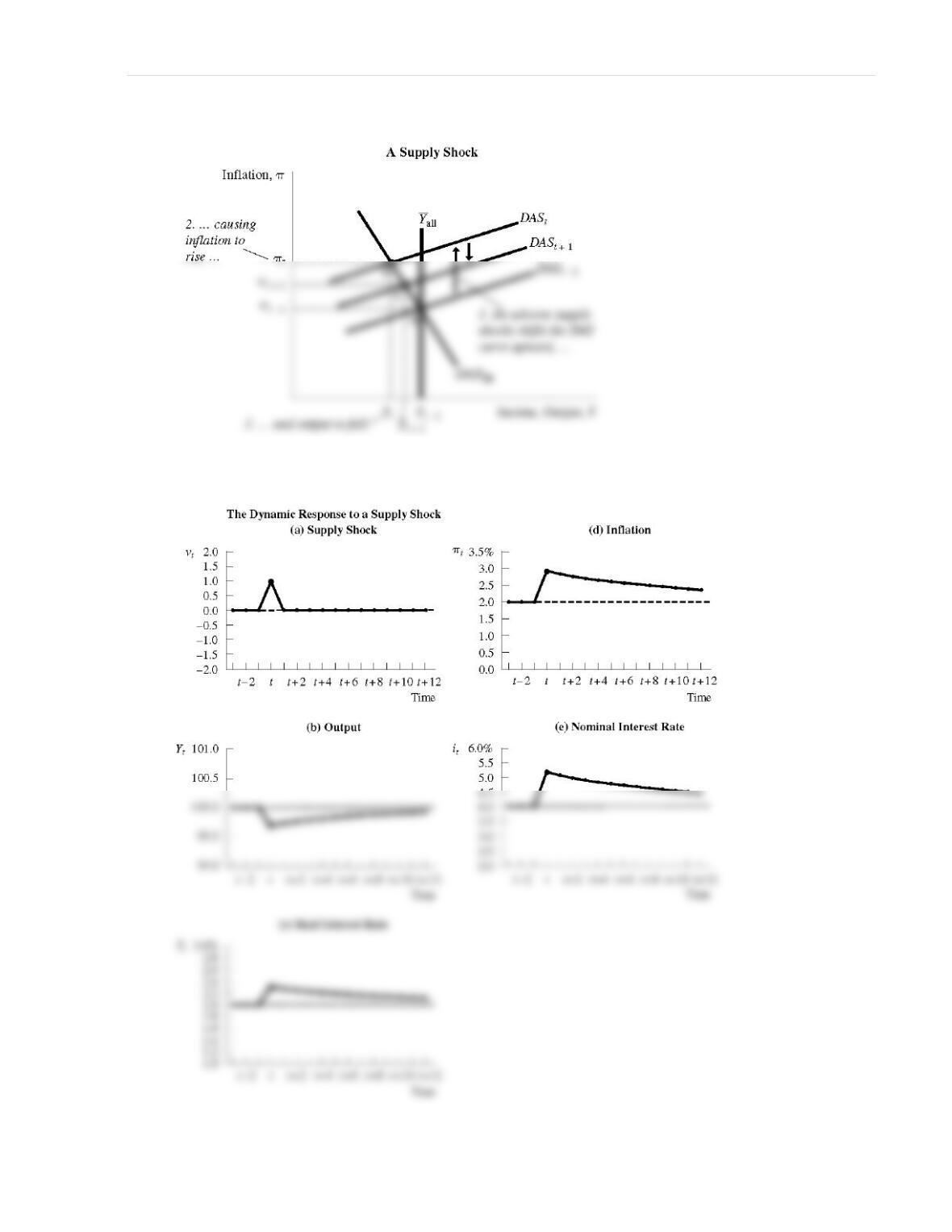

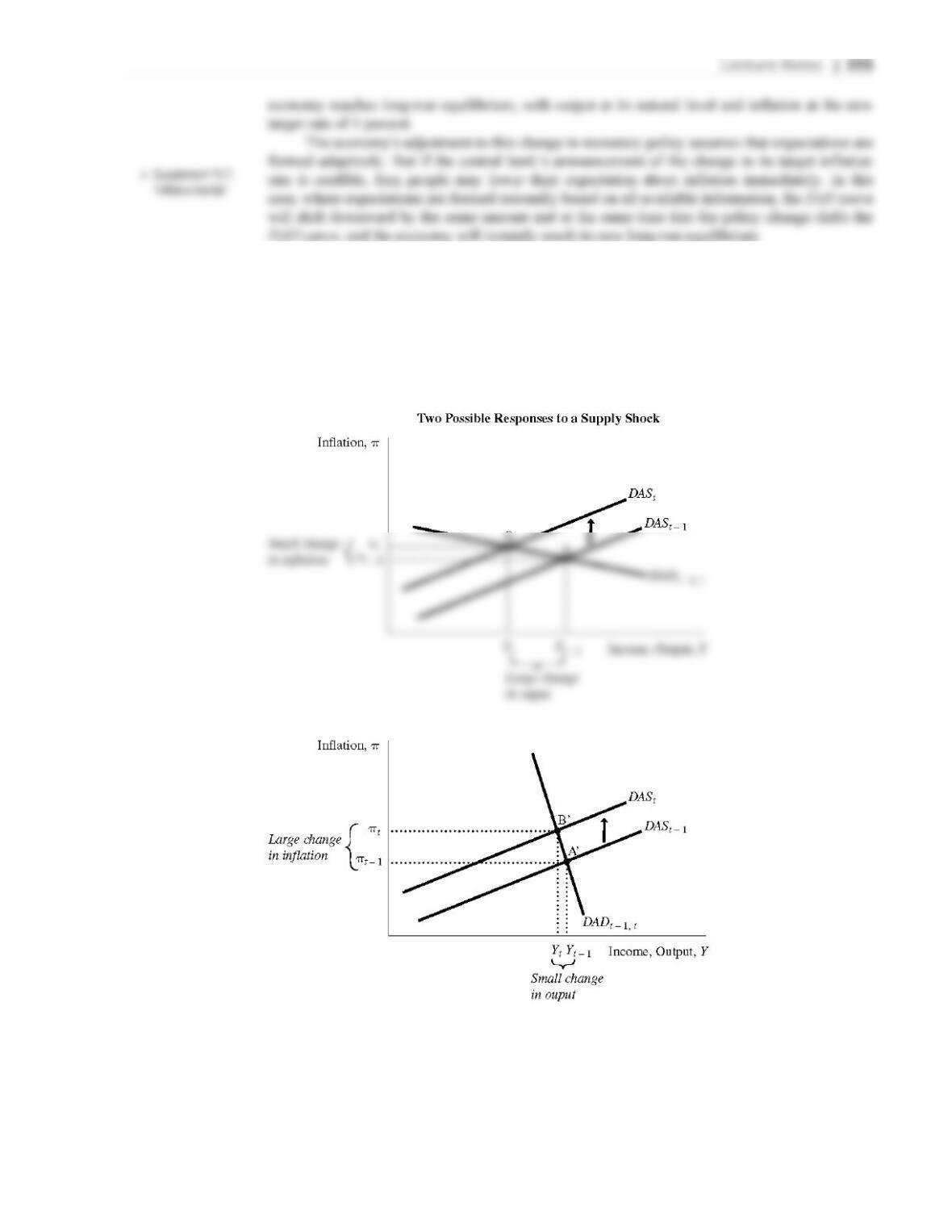

A Shock to Aggregate Supply

Suppose that the aggregate supply shock variable ut increases to 1 percent for one period of time

and then returns to zero. The DAS curve will shift up in period t by exactly the amount of the

shock. The DAD curve will remain unchanged. Inflation rises and output falls in period t. These

effects reflect in part the response of the central bank through its policy rule that leads to higher

nominal and real interest rates, which in turn reduces demand for goods and services and pushes

output below its natural level. Lower output dampens inflationary pressure, so inflation does not

rise by the full extent of the supply shock.

!Supplement 15–1,

“How a Real

Business Cycle

Model Is

Constructed”

!Supplement 15–2,

“The

Microeconomics

of Labor Supply”

!Supplement 15–3,

“Quits and

Models”

!Supplement 15–6,

“Real Business

Cycles and

Random Walks”

Lecture Notes | 351

Figure 6

Figure 7

352 | CHAPTER 15 A Dynamic Model of Economic Fluctuations

FYI: The Numerical Calibration and Simulation

The textbook uses simulation analysis to explore the adjustment of the economy to various

shocks and changes in policies. Each period is best thought of as one year in length. The model

is calibrated using numerical values for the parameters of the model and some of the exogenous

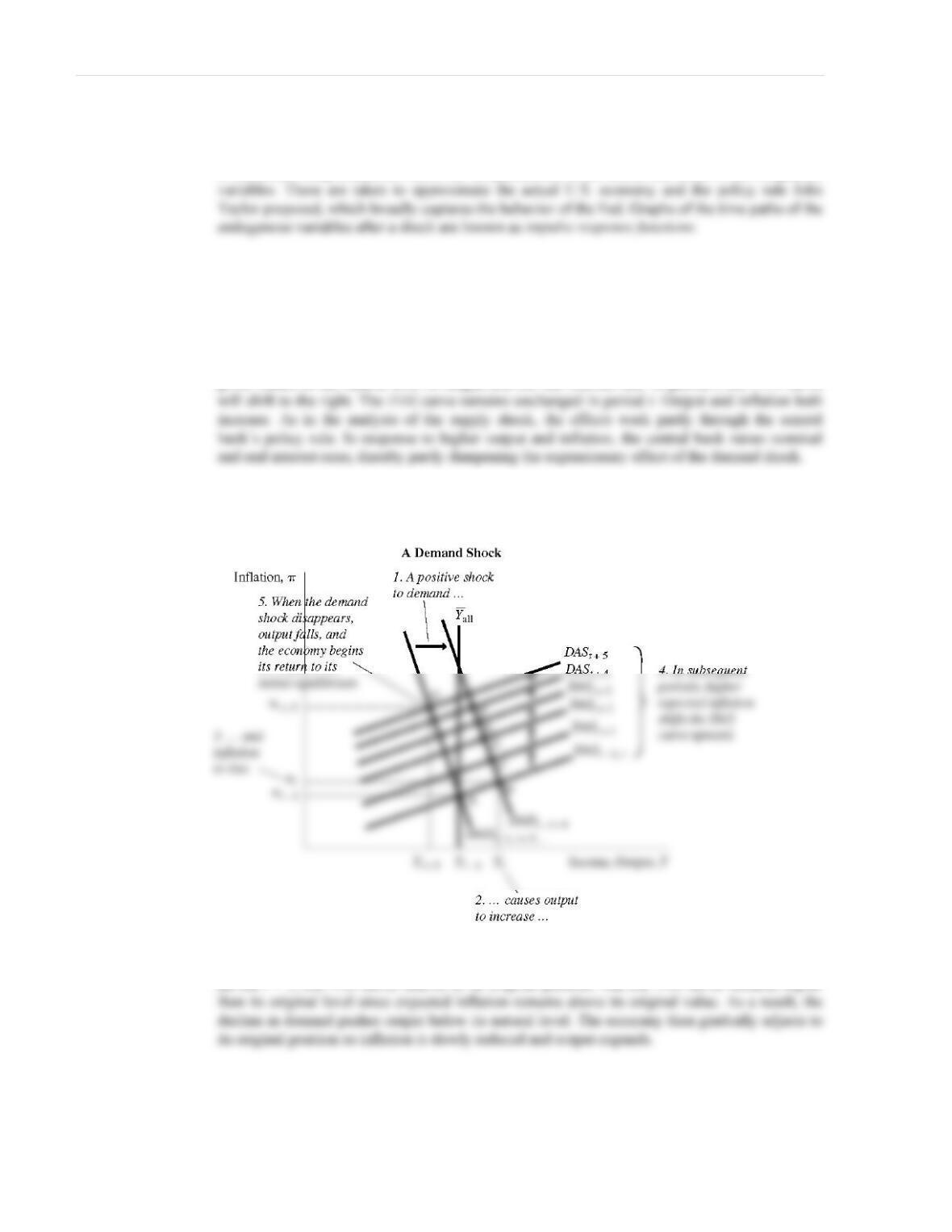

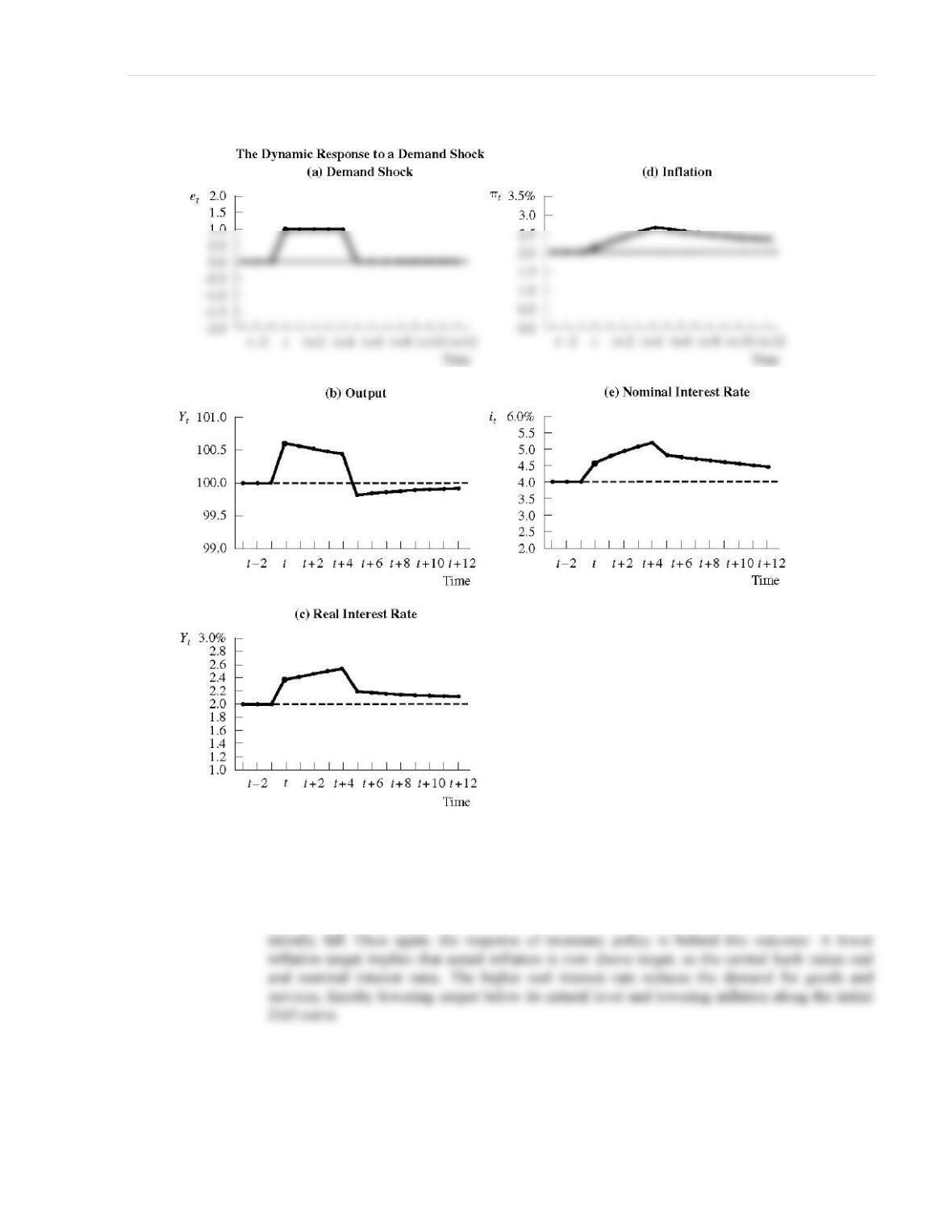

A Shock to Aggregate Demand

Suppose that the aggregate demand shock variable equals one for five periods and then returns to

its normal value of zero. This positive shock might reflect a war that increases government

purchases or a stock–market boom that raises wealth and consumption. More generally, a

demand shock could represent any event that changes the demand for goods and services at

given values of the natural level of output and the real interest rate. In period t, the DAD curve

Figure 8

In subsequent periods, expected inflation is higher, and so the DAS curve shifts upward

continually, reducing output and increasing inflation. When the demand shock disappears in

period t + 5, the DAS curve returns to its original position. But the DAS curve remains higher

Lecture Notes | 353

Figure 9

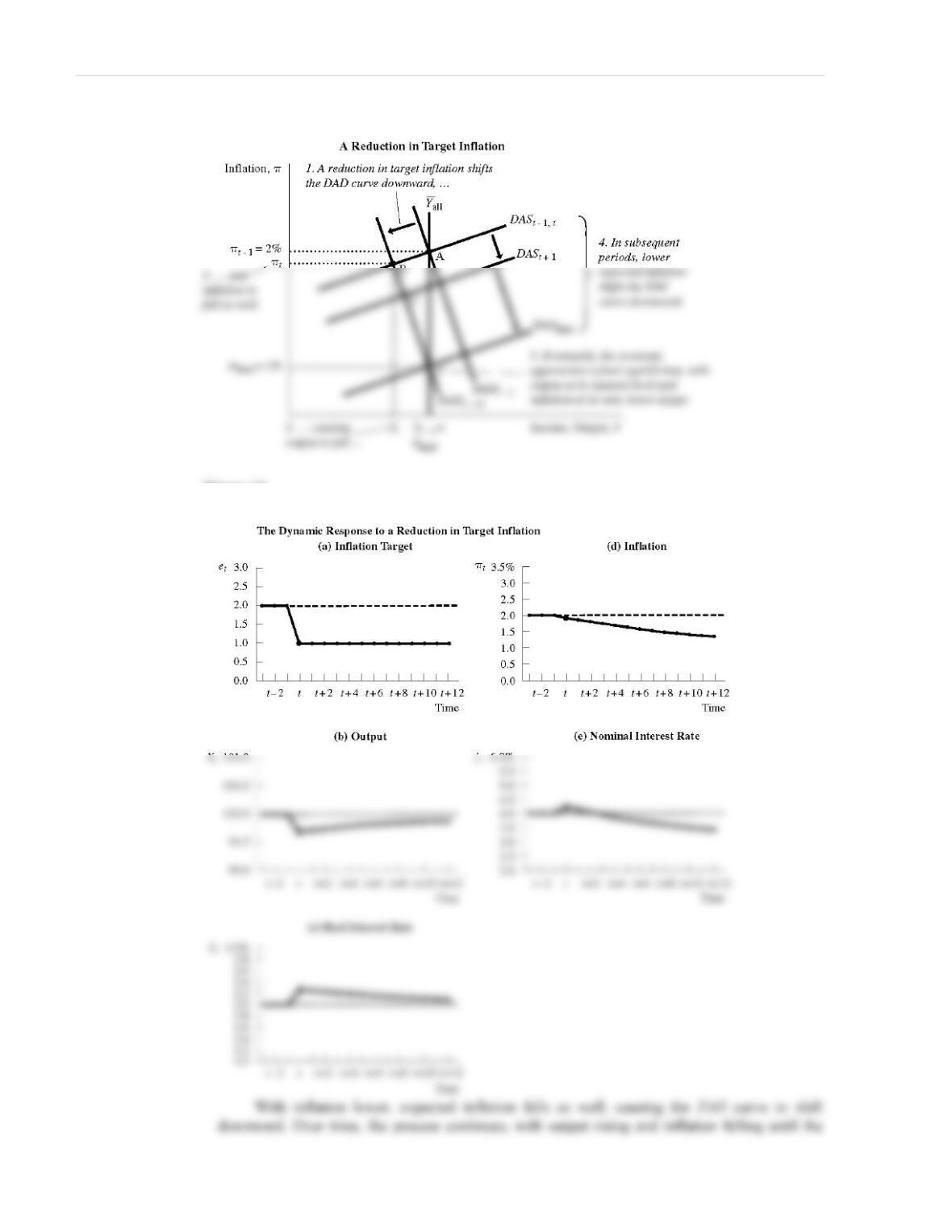

A Shift in Monetary Policy

Suppose that the central bank lowers its target for inflation from 2 percent to 1 percent and keeps

it at the lower value from then on. This will cause the DAD curve to shift to the left (and, to be

exact, downward by one percentage point). Since the target for inflation does not enter the

dynamic aggregate supply equation, the DAS curve does not shift initially. Output and inflation

354 | CHAPTER 15 A Dynamic Model of Economic Fluctuations

Figure 10

Figure 11

15–4 Two Applications: Lessons for Monetary Policy

The model developed in the previous sections can be used to motivate a discussion about the

design of monetary policy. In particular, we can consider how the values of the parameters of the

monetary policy rule influence the effectiveness of monetary policy.

Figure 12

The Tradeoff Between Output Variability and Inflation

Variability

Consider the effect of a supply shock on the economy. As shown earlier, the initial response is

for output to fall below its natural level and inflation to rise above the central bank’s target. But

356 | CHAPTER 15 A Dynamic Model of Economic Fluctuations

the extent to which output declines or inflation rises depends on the slope of the DAD curve.

When the slope is steep, inflation rises relatively more and output declines relatively less,

whereas when the slope is flat, inflation rises relatively less and output declines relatively more.

Because the slope of the DAD curve depends on the parameters of the monetary policy

rule, the central bank can affect the slope by choosing whether to respond more or less strongly

to deviations from target inflation or the natural level of output. In particular, when 8r is large

Case Study: Different Mandates, Different Realities: The Fed

Versus the ECB

The legislation that created the Federal Reserve gave it the dual mandate of stabilizing both

employment and prices, whereas the European Central Bank (ECB) is charged with the primary

objective of maintaining price stability, defined as inflation close to 2 percent over the medium

term. These differences in mandates can be interpreted in our model as being reflected in

different parameters in the monetary policy rule. For the ECB compared to the Fed, more weight

is given to inflation stability and less to output stability. The events of 2008, when oil prices rose

sharply and the world economy headed into recession, support this interpretation: The Fed

lowered interest rates from 5 percent to a range of 0 to 0.25 percent, while the ECB cut interest

rates by much less. In 2011, as the global economy recovered, the ECB began to raise interest

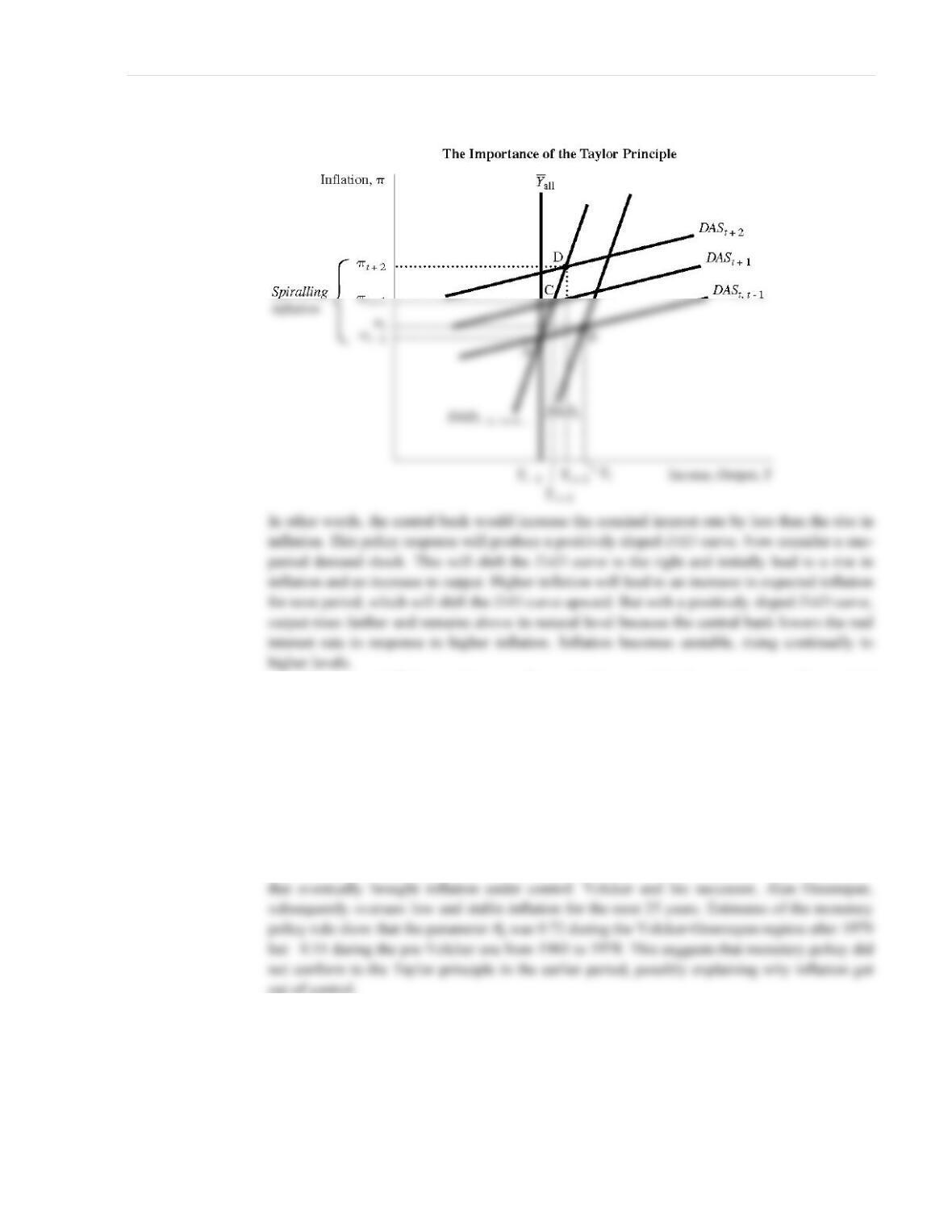

The Taylor Principle

Suppose that the central bank responded to a rise in inflation above its target by cutting the real

interest rate. From the monetary policy equation, this would imply that the parameter 8r is less

than zero:

it=

π

t+

ρ

+

θπ

(

π

t–

π

t

*)+

θ

YYt–Yt

( )

.

Lecture Notes | 357

Figure 13

To prevent inflation getting out of control, the central bank must increase the nominal

interest by more than the rise in inflation (8r must be greater than zero), thereby increasing the

real interest rate, so that the DAD curve is negatively sloped. The requirement that the central

bank respond to inflation by raising the nominal interest more than one–for–one is sometimes

called the Taylor principle, after economist John Taylor, who highlighted it as a key

consideration in the design of monetary policy.

Case Study: What Caused the Great Inflation?

Inflation during the 1970s in the United States reached high levels. Paul Volcker, who was

appointed chairman of the Fed in 1978, instituted a change in monetary policy beginning in 1979

out of control.

15–5 Conclusion: Toward DSGE Models

Advanced courses in macroeconomics develop a class of models known as dynamic, stochastic,

general equilibrium (DSGE) models. The dynamic AD–AS model discussed in this chapter is a

simpler version of these more advanced DSGE models. The model of this chapter illustrates how

the key macroeconomic variables (output, inflation, and real and nominal interest rates) respond

!Supplement 15–9,

“How Long Is the

Long Run?”