Answers and Solutions: 15 – 1

Chapter 15

Capital Structure Decisions

ANSWERS TO END-OF-CHAPTER QUESTIONS

15-1 a. Capital structure is the manner in which a firm’s assets are financed; that is, the right–

hand side of the balance sheet. Capital structure is normally expressed as the

percentage of each type of capital used by the firm—debt, preferred stock, and

common equity. Business risk is the risk inherent in the operations of the firm, prior

to the financing decision. Thus, business risk is the uncertainty inherent in a total risk

sense, future operating income, or earnings before interest and taxes (EBIT).

Business risk is caused by many factors. Two of the most important are sales

variability and operating leverage. Financial risk is the risk added by the use of debt

financing. Debt financing increases the variability of earnings before taxes (but after

interest); thus, along with business risk, it contributes to the uncertainty of net income

and earnings per share. Business risk plus financial risk equals total corporate risk.

c. Reserve borrowing capacity exists when a firm uses less debt under “normal”

conditions than called for by the tradeoff theory. This allows the firm some

flexibility to use debt in the future when additional capital is needed.

15-2 Business risk refers to the uncertainty inherent in projections of future ROIC = ROEU.

15-4 Operating leverage affects EBIT and, through EBIT, EPS. Financial leverage has no

effect on EBIT—it only affects EPS, given EBIT.

15-5 If sales tend to fluctuate widely, then cash flows and the ability to service fixed charges

will also vary. Such a firm is said to have high business risk. Consequently, there is a

15-6 Public utilities place greater emphasis on long-term debt because they have more stable

sales and profits as well as more fixed assets. Also, utilities have fixed assets which can

15-7 EBIT depends on sales and operating costs. Interest is deducted from EBIT. At high debt

15-8 The tax benefits from debt increase linearly, which causes a continuous increase in the

firm’s value and stock price. However, financial distress costs get higher and higher as

Answers and Solutions: 15 – 3

SOLUTIONS TO END-OF-CHAPTER PROBLEMS

15-1 QBE = F/(P – V) = $500,000/($75 – $50) = 20,000.

15-2 If wd = 0.2, then wce = 1 – 0.2 = 0.8. So D/S = wd/we = 0.2/0.8.

15-3 If the company had no debt, its required return would be:

rs,U = rRF + bU RPM = 5.5% + 1.0(6%) = 11.5%.

15-4 S = (1 – wd)(Vop) = (1 – 0.4)($500) = $300 million.

15-7 a. Here are the steps involved:

(1) Determine the variable cost per unit at present, V:

Profit = P(Q) – FC – V(Q)

$500,000 = ($100,000)(50) – $2,000,000 – V(50)

50(V) = $2,500,000

V = $50,000.

Answers and Solutions: 15 – 4

(4) Estimate the approximate rate of return on new investment:

Return = Profit/Investment = $850,000/$4,000,000 = 21.25%.

Since the return exceeds the 15 percent cost of equity, this analysis suggests that the

firm should go ahead with the change.

c. It is impossible to state unequivocally whether the new situation would have more or

less business risk than the old one. We would need information on both the sales

probability distribution and the uncertainty about variable input cost in order to make

this determination. However, since a higher breakeven point, other things held

constant, is more risky. Also the percentage of fixed costs increases:

15-8 a. Original value of the firm (D = $0):

We are given that the book value of assets is equal to the market value of assets, so

the value is $3,000,000. Alternatively, we can calculate the value as the sum of the

debt (which is zero) and the stock (200,000 shares at a price of $15 per share):

V = D + S = 0 + ($15)(200,000) = $3,000,000.

Because growth is zero, FCF is equal to EBIT(1-T). The value of operations is:

Vop =

.286.214,348,3$

0896.0

)40.01)(000,500($

WACC

)T1)(EBIT(

WACC

FCF =

−

=

−

=

Increasing the financial leverage by adding $900,000 of debt results in an increase in

b. Using its target capital structure of 30% debt, the company must have debt of:

D = wd V = 0.30($3,348,214.286) = $1,004,464.286.

Therefore, its value of equity is:

Answers and Solutions: 15 – 6

c. The number of shares repurchased, X, is:

X = (D – D0)/P = $1,004,464.286 / $16.741 = 60,000.256 60,000.

Thus, by adding debt, the firm increased its EPS by $0.342.

d. 30% debt: TIE =

I

EBIT

=

5.312,70$

EBIT

.

Probability TIE

0.10 ( 1.42)

0.20 2.84

Answers and Solutions: 15 – 7

15-9 a. Present situation (50% debt):

WACC = wd rd(1-T) + wcers

= (0.5)(10%)(1-0.15) + (0.5)(14%) = 11.25%.

V =

1125.0

)15.01)(24.13($

WACC

)T1)(EBIT(

WACC

FCF −

=

−

=

= $100 million.

15-10 a. BEA’s unlevered beta is bU=b/(1+ (1-T)(D/S))=1.0/(1+(1-0.40)(20/80)) = 0.870.

b. b = bU (1 + (1-T)(D/S)).

At 40 percent debt: bL = 0.87 (1 + 0.6(40%/60%)) = 1.218.

rS = 6 + 1.218(4) = 10.872%

1114.0

)15.01)(24.13($

WACC

)T1)(EBIT(

WACC

FCF −

=

−

=

Answers and Solutions: 15 – 8

15-11 Tax rate = 40% rRF = 5.0%

bU = 0.8 rM – rRF = 6.0%

From data given in the problem and table we can develop the following table:

wd

wce

D/S

rd

rd(1 – T)

Levered

betaa

rsb

WACCc

0

100%

0.00

6.0%

3.60%

0.80

9.80%

9.80%

Notes:

a These beta estimates were calculated using the Hamada equation,

b = bU[1 + (1 – T)(D/S)].

b These rs estimates were calculated using the CAPM, rs = rRF + (rM – rRF)b.

0.25

7.0%

4.20%

0.92

9.26%

0.67

8.0%

4.80%

1.12

8.95%

1.50

9.0%

5.40%

1.52

8.89%

4.00

10.0%

6.00%

2.72

9.06%

Answers and Solutions: 15 – 9

SOLUTION TO SPREADSHEET PROBLEM

Mini Case: 15 – 10

MINI CASE

Assume you have just been hired as a business manager of PizzaPalace, a regional pizza

restaurant chain. The company’s EBIT was $50 million last year and is not expected to grow.

The firm is currently financed with all equity and it has 10 million shares outstanding. When you

took your corporate finance course, your instructor stated that most firms’ owners would be

financially better off if the firms used some debt. When you suggested this to your new boss, he

encouraged you to pursue the idea. As a first step, assume that you obtained from the firm’s

investment banker the following estimated costs of debt for the firm at different capital

structures:

% Financed With Debt rd

0% —

20 8.0%

30 8.5

40 10.0

50 12.0

If the company were to recapitalize, debt would be issued, and the funds received would be

used to repurchase stock. PizzaPalace is in the 40 percent state-plus-federal corporate tax

bracket, its beta is 1.0, the risk-free rate is 6 percent, and the market risk premium is 6

percent.

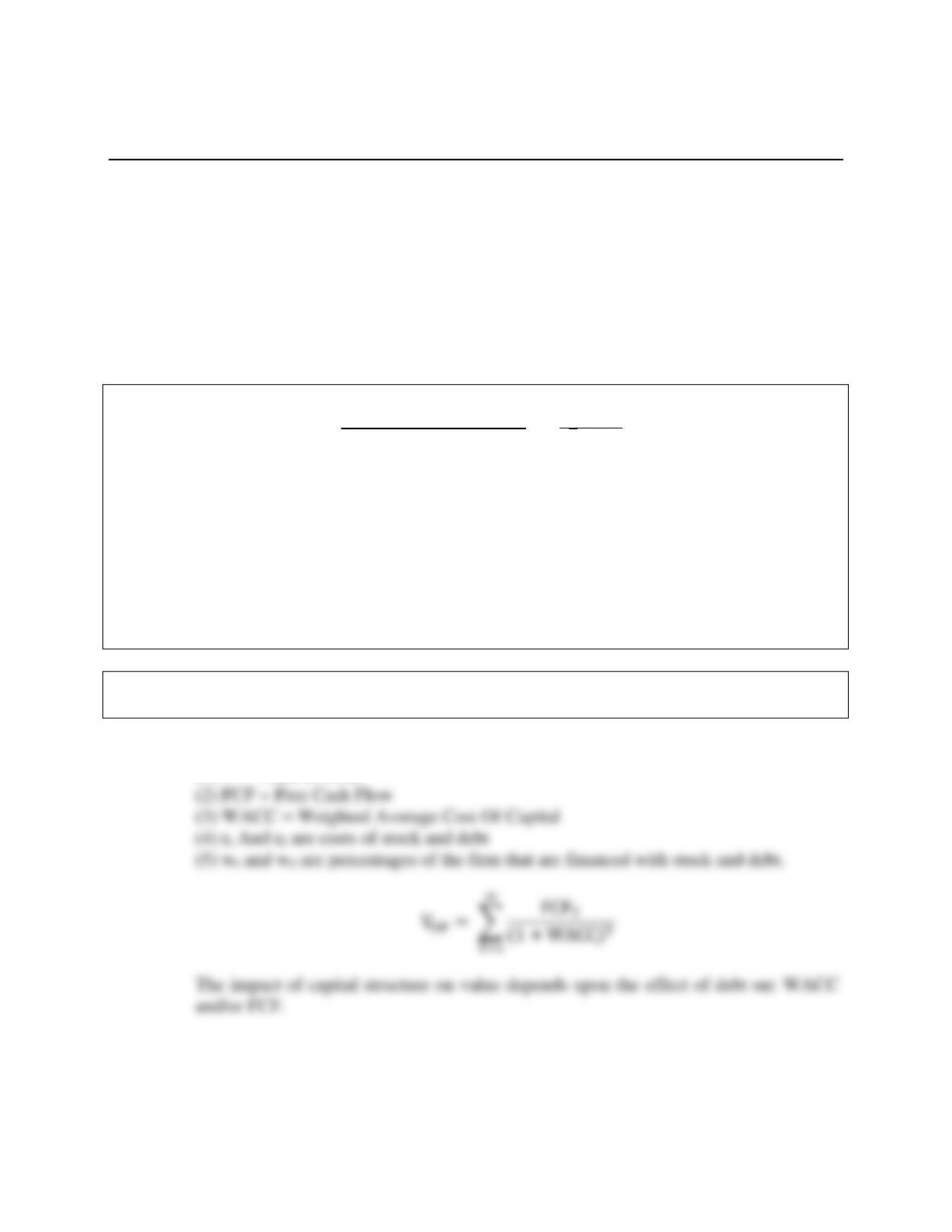

a. Using the free cash flow valuation model, show the only avenues by which

capital structure can affect value.

Answer: The basic definitions are:

(1) V = Value of Firm

Mini Case: 15 – 11

b. (1) What is business risk? What factors influence a firm’s business risk?

Answer: Business risk is uncertainty about EBIT. Factors that influence business risk include:

b. (2) What is operating leverage, and how does it affect a firm’s business risk? Show

the operating break even point if a company has fixed costs of $200, a sales price

of $15, and variables costs of $10.

Answer: Operating leverage is the change in EBIT caused by a change in quantity sold. The

higher the proportion of fixed costs within a firm’s overall cost structure, the greater

c. Now, to develop an example which can be presented to PizzaPalace’s

management to illustrate the effects of financial leverage, consider two

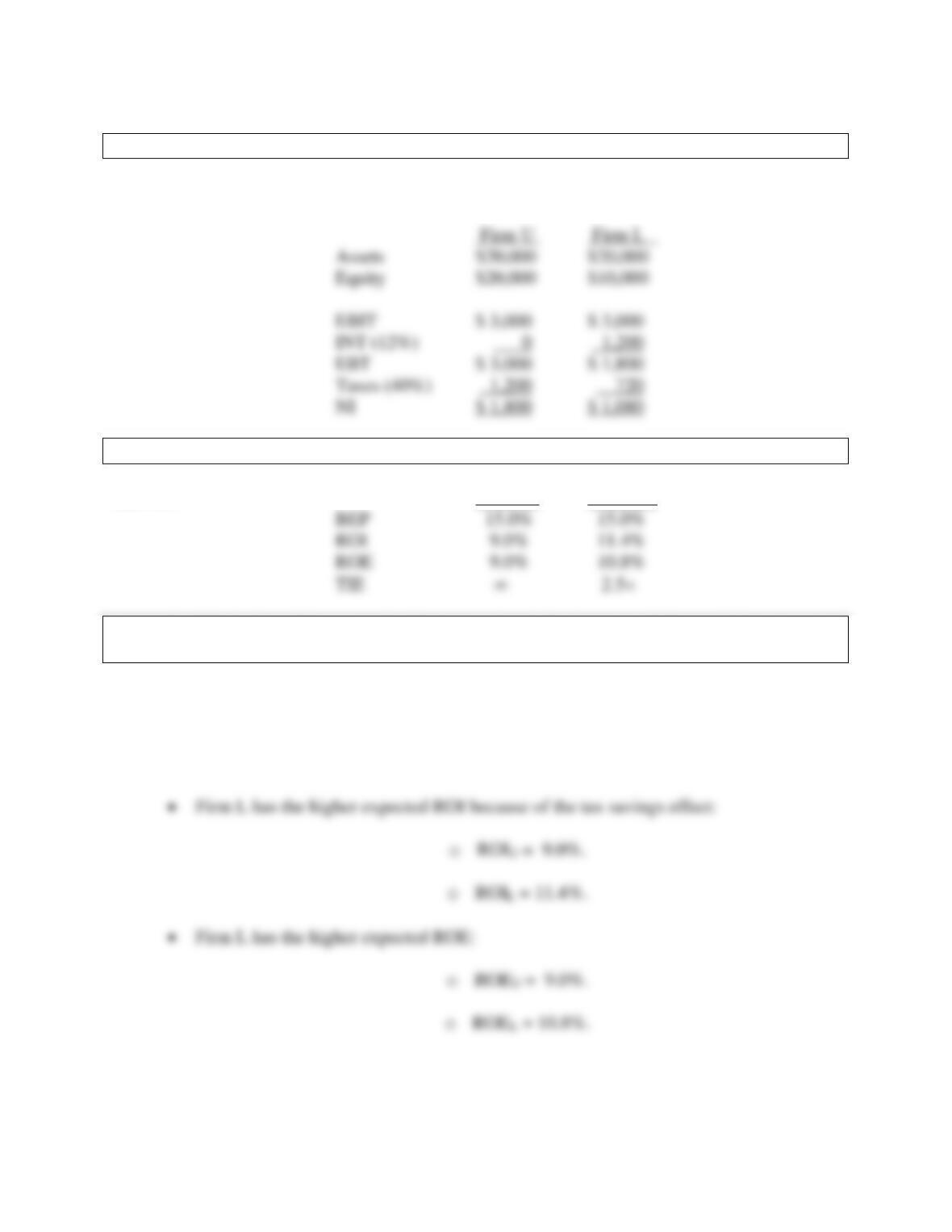

hypothetical firms: Firm U, which uses no debt financing, and Firm L, which

uses $10,000 of 12 percent debt. Both firms have $20,000 in assets, a 40 percent

tax rate, and an expected EBIT of $3,000.

Mini Case: 15 – 12

1. Construct partial income statements, which start with EBIT, for the two firms.

Answer: Here are the fully completed statements:

Firm U Firm L

c. 2. Now calculate ROE for both firms.

Answer: Firm U Firm L

c. 3. What does this example illustrate about the impact of financial leverage on

ROE?

Answer: Conclusions from the analysis:

• The firm’s basic earning power, BEP = EBIT/total assets, is unaffected by financial

leverage.

Mini Case: 15 – 13

d. Explain the difference between financial risk and business risk.

Answer: Business risk increases the uncertainty in future EBIT. It depends on business factors

e. What happens to ROE for Firm U and Firm L if EBIT falls to $2,000? What does this

imply about the impact of leverage on risk and return?

Answer:

Firm U

Firm L

EBIT

$2,000

$2,000

Interest

$1,200

EBT

$2,000

Taxes

$1,200

ROIC

ROE

Mini Case: 15 – 14

f. What does capital structure theory attempt to do? What lessons can be learned

from capital structure theory? Be sure to address the MM models.

Answer: MM theory begins with the assumption of zero taxes. MM prove, under a very

restrictive set of assumptions, that a firm’s value is unaffected by its financing mix:

VL = VU.

MM theory ignores bankruptcy (financial distress) costs, which increase as more

leverage is used. At low leverage levels, tax benefits outweigh bankruptcy costs. At

high levels, bankruptcy costs outweigh tax benefits. An optimal capital structure

exists that balances these costs and benefits. This is the trade-off theory.

Mini Case: 15 – 15

A second agency problem is the potential for “underinvestment”. Debt increases risk

of financial distress. Therefore, managers may avoid risky projects even if they have

positive NPVs.

g. What does the empirical evidence say about capital structure theory? What are

the implications for managers?

Answer: Tax benefits are important. At the optimal capital structure, $1 debt adds about $0.10

to $0.20 to value on average. For the average firm financed with 25% to 30% debt,

this adds about 3% to 6% to the total value. Bankruptcies are costly– costs can be up

Mini Case: 15 – 16

attitudes.

h. With the above points in mind, now consider the optimal capital structure for

PizzaPalace.

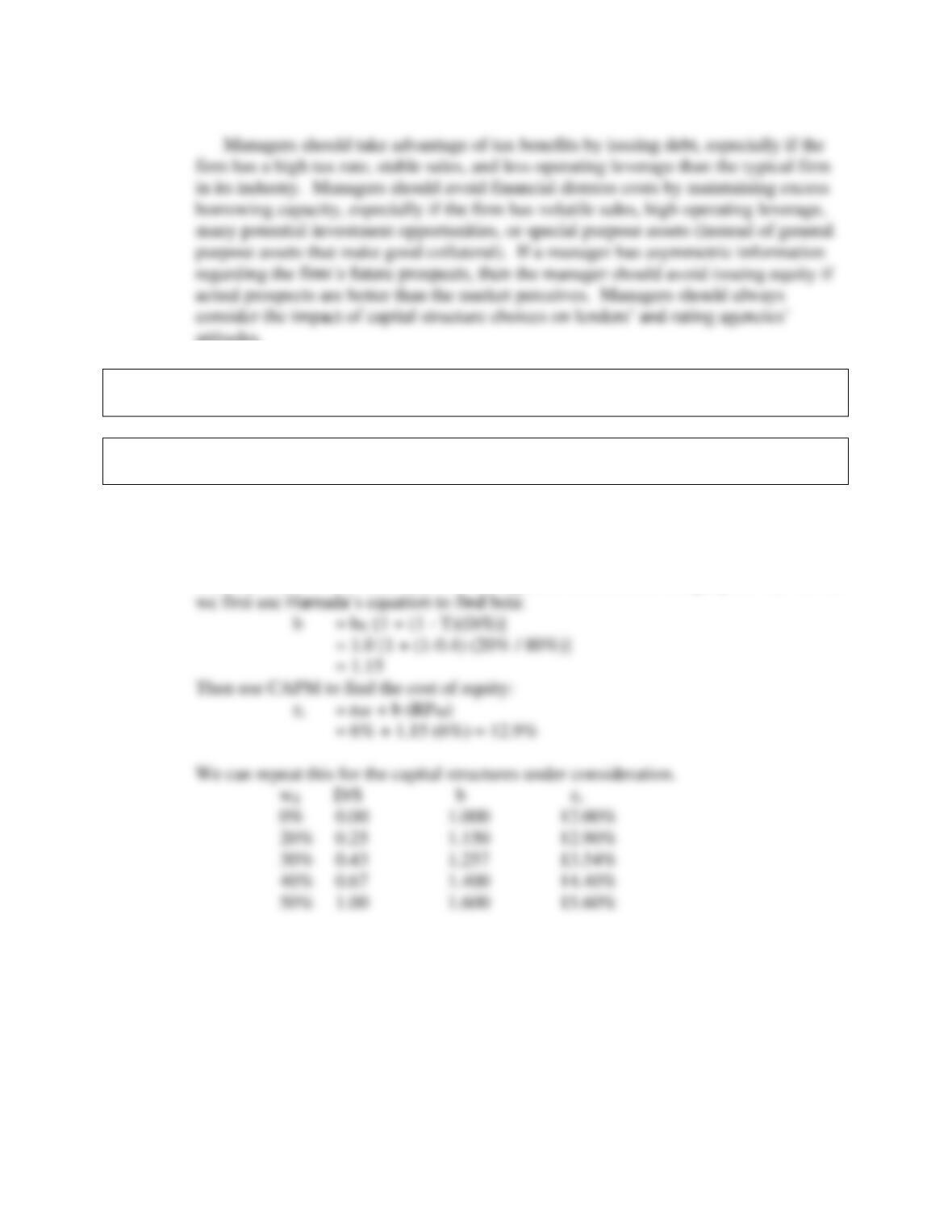

h. (1) For each capital structure under consideration, calculate the levered beta, the

cost of equity, and the WACC.

Answer: MM theory implies that beta changes with leverage. bu is the beta of a firm when it

has no debt (the unlevered beta.) Hamada’s equation provides the beta of a levered

firm: bL = bU [1 + (1 – T)(D/S)]. For example, to find the cost of equity for wd = 20%,

Mini Case: 15 – 17

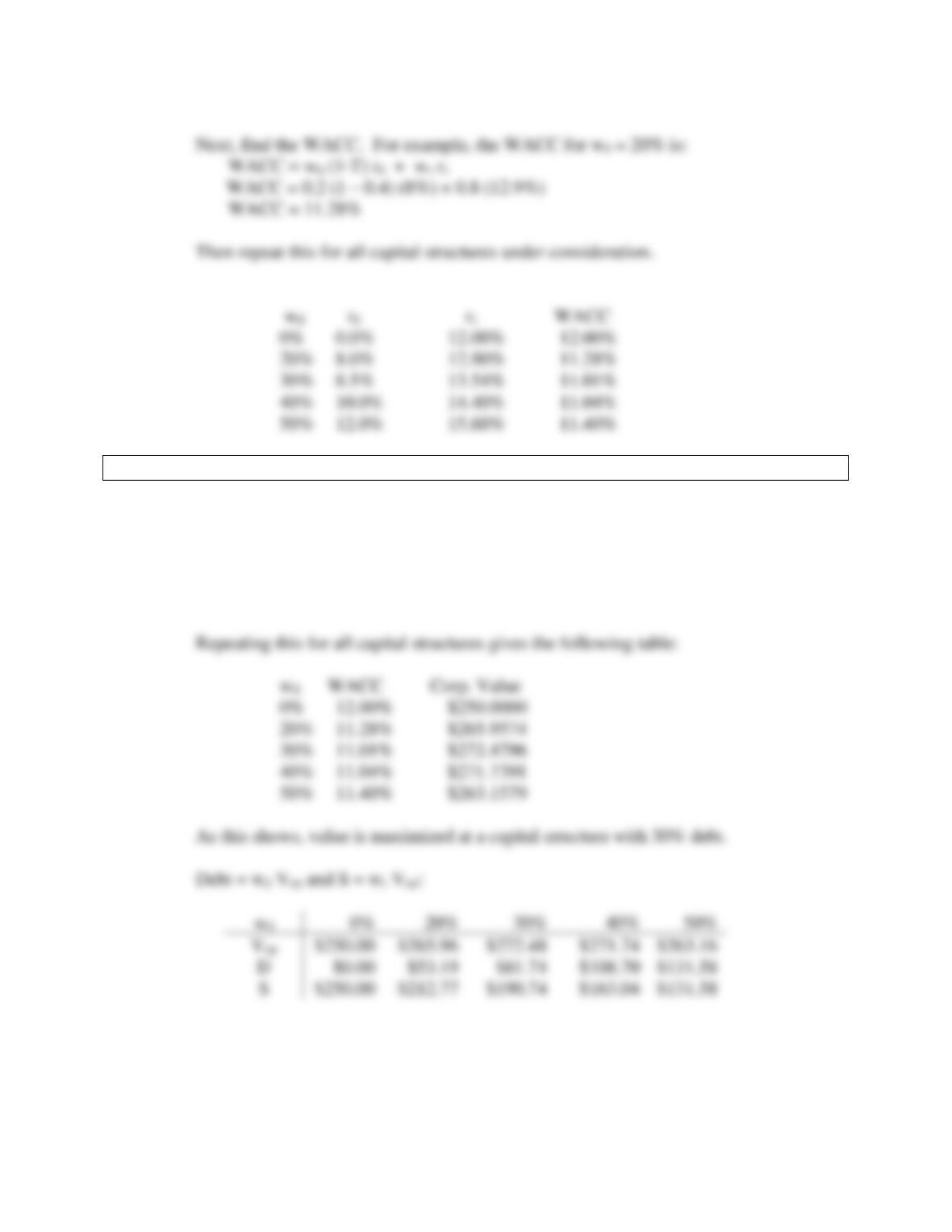

h. (2) Now calculate the corporate value.

Answer: For example the corporate value for wd = 20% is:

V = FCF(1+g) / (WACC-g)

Using these values, V = $30(1+0) / (0.1128 − 0) = $2,65.96 million.

Mini Case: 15 – 18

i. Describe the recapitalization process and apply it to PizzaPalace. Calculate the

resulting the value of the debt that will be issued, the resulting market value of

equity, the price per share, the number of shares repurchased, and the

remaining shares. Considering only the capital structures under analysis, what is

PizzaPalace’s optimal capital structure?

Answer:

First, find the dollar value of debt. For example, for wd = 20%, the dollar value of

debt is:

d = wd V = 0.2 ($2,659,574) = $53.19.

Mini Case: 15 – 19

The situation before the recap is:

The stock price is $25 and the total wealth of shareholders is $2,500,000.

Now consider the situation if the firm moves to a capital structure with wd = 20% by

issuing $53.1915 in debt but has not yet repurchased equity. The firm’s value of

operations increases because its WACC decreases. The firm also temporarily has

$531,915 in short-term investments.

Mini Case: 15 – 20

The repurchase itself will not change the stock price. If investors thought that the

repurchase would increase the stock price, they would all purchase stock the day

before, which would drive up its price. If investors thought that the repurchase would

decrease the stock price, they would all sell short the stock the day before, which

would drive down the stock price.

Before

Debt

After

Debt,

Before

Rep.

After Rep.

Vop

$250

$265.9574

$265.9574

+ ST Inv.

0

53.1915

0

$250

$319.1489

$265.9574

0

53.1915

53.1915

$250

$265.9574

$212.7660

$250

$265.9574

$212.7660

0

0

53.1915

$250

$265.9574

$265.9574

Mini Case: 15 – 21

There are some shortcuts we can take to find the values of S, P, and n after the

repurchase:

We apply these relationships for each possible capital structure:

wd

0%

20%

30%

40%

50%

rd

0.0%

8.0%

8.5%

10.0%

12.0%

ws

100%

80%

70%

60%

50%

b

1.150

13.54%

11.01%

$81.74

S

n

P

$27.25

$27.17

The optimal capital structure is for wd = 30%. This gives the highest corporate value,

the lowest WACC, and the highest stock price per share. But notice that wd = 40% is

very similar to the optimal solution; in other words, the optimal range is pretty flat.