Concise10e

THE CASH CONVERSION CYCLE

Cash

conversion

cycle

=

Inventory

conversion

period (ICP)

+

Receivables

collection

period (ACP)

–

Payables

deferral

period (PDP)

EXAMPLE

Sales $1,216,666

COGS $1,013,889

CCC =ICP +ACP –PDP

= Inv / (COGS/365) +AR/(Sales/365) – AP/(COGS/365)

Calculate the cash conversion cycle for the Great Fashions Inc. (GFI). Annual sales are $1,216,666, and the annual cost of goods

sold is $1,013,889. The average levels of inventory, receivables, and accounts payable are $250,000, $300,000, and $150,000,

respectively. GFI uses a 365-day accounting year.

It takes 90 days to make and then sell golf outfits, and another 90 days to collect cash after the sale, or a total of 180 days

between spending money and collecting cash. However, the company can delay payment for supplies and labor for 54 days.

Therefore, the net days the firm must finance its labor and purchases is 180 – 54 = 126 days, which is the cash conversion cycle.

This chapter deals with working capital management. Two useful tools for working capital management are (1) the cash

conversion cycle and (2) the cash budget. This spreadsheet model shows how these tools are used to help manage current

assets.

The cash conversion cycle focuses on the length of time between when the company must make payments and when it receives

cash inflows. The cash conversion cycle is determined by three factors: (1) The inventory conversion period, which is the

average time required to convert materials into finished goods and then to sell those goods. (2) The receivables collection

period, which is the length of time required to convert the firm’s receivables into cash, or how long it takes to collect cash from a

sale. (3) The payables deferral period, which is the average length of time between the purchase of materials and labor and

payment for them. The cash conversion cycle is determined by the following formula:

12/12/2018

Chapter 15. Model for Managing Current Assets

1

2

3

4

5

6

7

8

A B C D E F G H I J K L M N

15 Chapter model 12/12/2018

THE CASH BUDGET

Input Data

Collections during month of sale 20% Assumed constant. Don’t change.

Collections during 1st month after sale 70% Assumed constant. Don’t change.

Collections during 2nd month after sale 10% Equal to 100% – (20% + 70%) – Bad debt %

The cash budget is a statement that shows expected cash flows over a specified period of time. Generally, firms use

a monthly cash budget for the coming year, plus a daily cash budget for the coming month. The monthly cash

budgets are used for long-range planning, and the daily budget for actual cash control. The following monthly cash

budget examines Allied Food for the last 6 months of 2020.

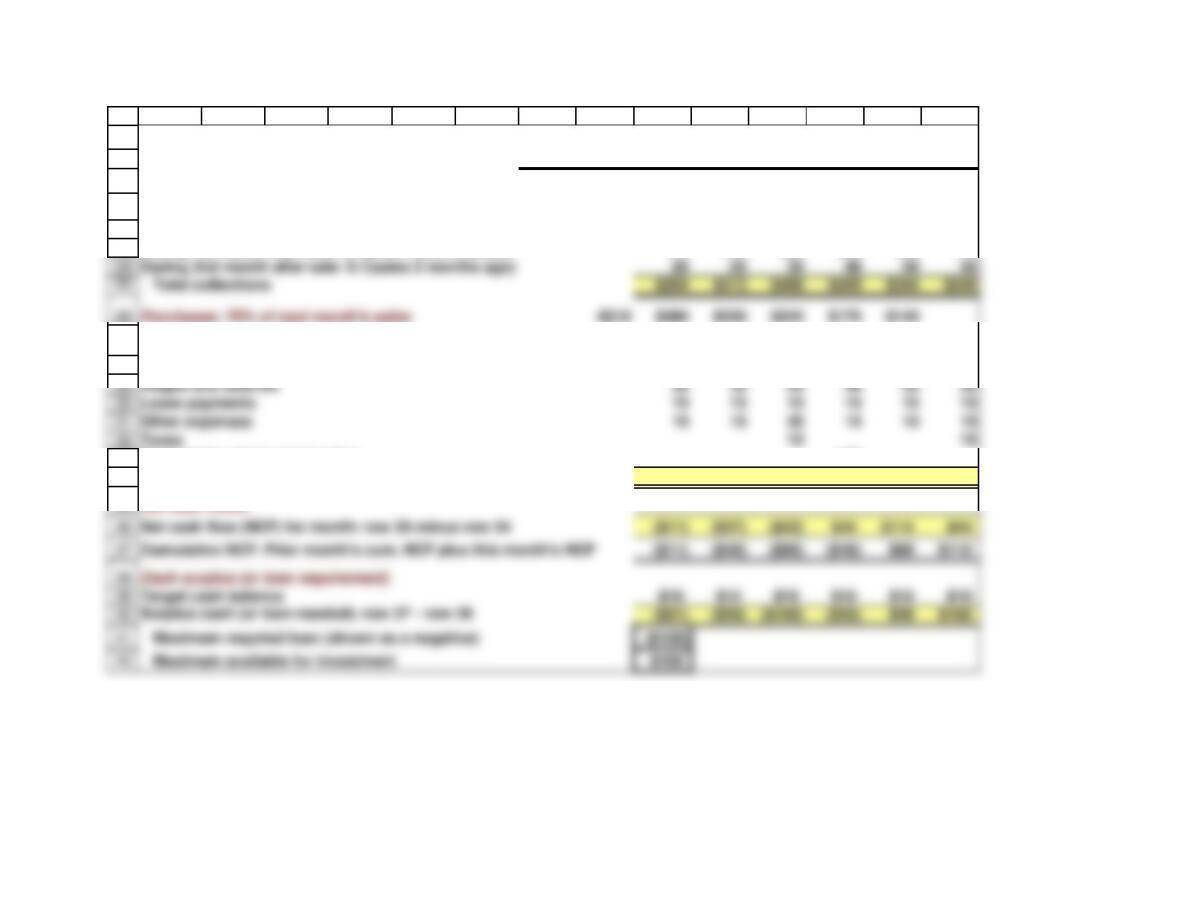

Table 15.1 Allied Food Products 2020 Cash Budget (Dollars in Millions)

Percent bad debts 0% Can change to see effects

Discount on first month collections

Purchases as a % of next month’s sales 70% Can change to see effects

Lease payments 15$ Can change to see effects

Construction cost for new plant (Oct) 100$ Can change to see effects

Target cash balance 10$ Can change to see effects

Sales adjustment factor (change from base) 0% % increase or decrease from base to see effects

18

19

20

21

22

23

Lease payments 15 15 15 15 15 15

Other expenses 10 15 20 15 10 10

27

28

33

34

40

42

Target cash balance $10 $10 $10 $10 $10 $10

35

A B C D E F G H I J K L M N

THE CASH BUDGET

May June July August Sept Oct Nov Dec

Sales (gross) $200 $250 $300 $400 $500 $350 $250 $200

Collections

During month of sale: 0.2(Sales)(0.98) $59 $78 $98 $69 $49 $39

During 1st month after sale: 0.7(prior month’s sales) 175 210 280 350 245 175

Payments

Payment for materials: Last month’s purchases $210 $280 $350 $245 $175 $140

Payment for plant construction 100

Total payments

$265 $350 $450 $415 $230 $205

Net cash flows:

25

During 2nd month after sale: 0.1(sales 2 months ago) 20 25 30 40 50 35

43

44

45

46

47

48

2.00% $ 115

4.00% $ 130

6.00% $ 145

7.00% $ 152

9.00% $ 167

50

52

54

57

59

60

61

62

63

65

A B C D E F G H I J K L M N

% bad Max Req’d Loan

debts $ 100

1.00% $ 107

3.00% $ 122

5.00% $ 137

8.00% $ 160

10.00% $ 175

Question: If the percent of customers who end up as bad debts increases, how would this

affect the maximum required loan?

Answer: Do a sensitivity

analysis.

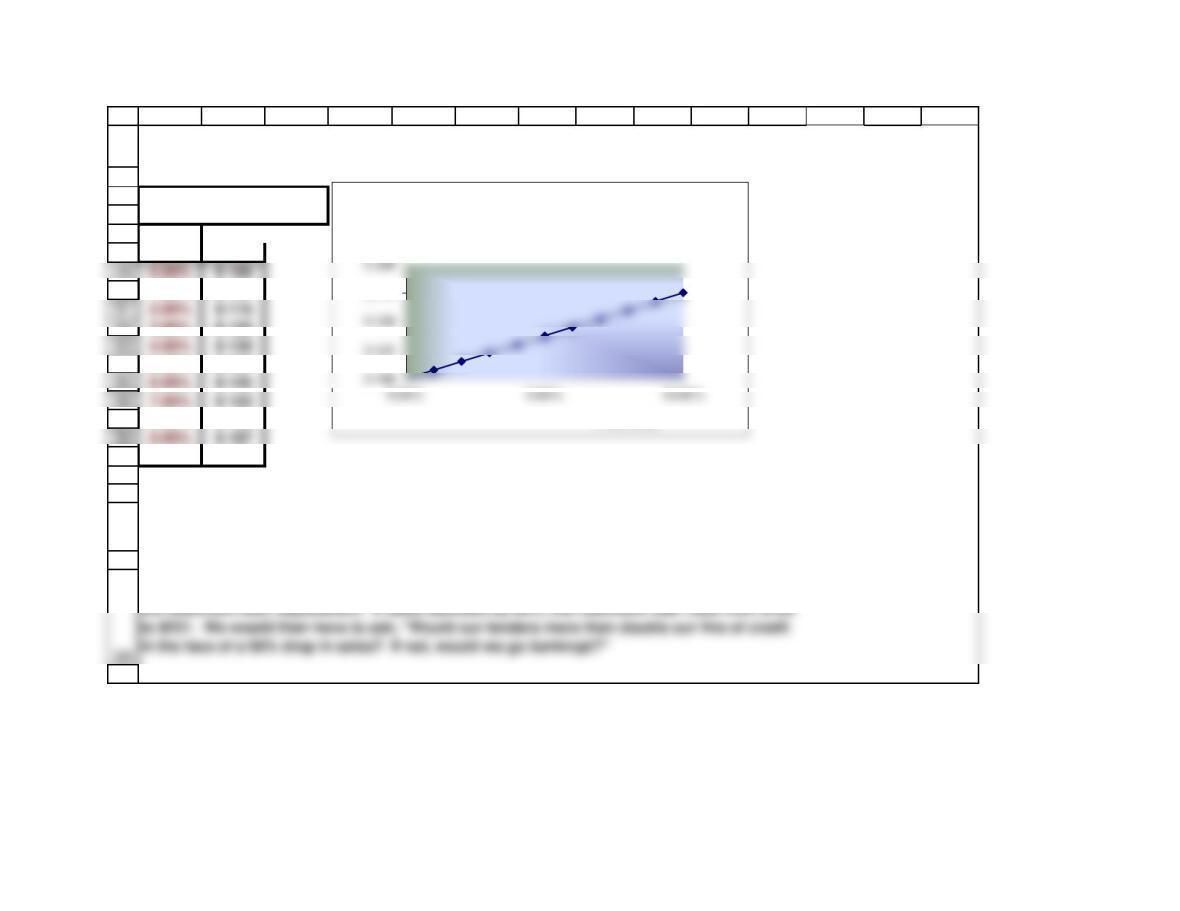

You could do all sorts of “What if” analyses. For example, assume sales declined by 50%.

How would that affect the maximum loan requirement?

Answer: Just change the sales adjustment factor from 0% to -50% and observe the change in

$ 175

Loan

Requirement

% Bad Debts

Effect of Bad Debts on Loan Requirements

0.00% $ 100

66

67

68

69

70

71

81

82

83

84

85

86

87

88

89

94

98

-50% $ 231 $ 236 $ 242 $ 248 $ 254 $ 262 $ 272 $ 282

90

91

99

A B C D E F G H I J K L M N

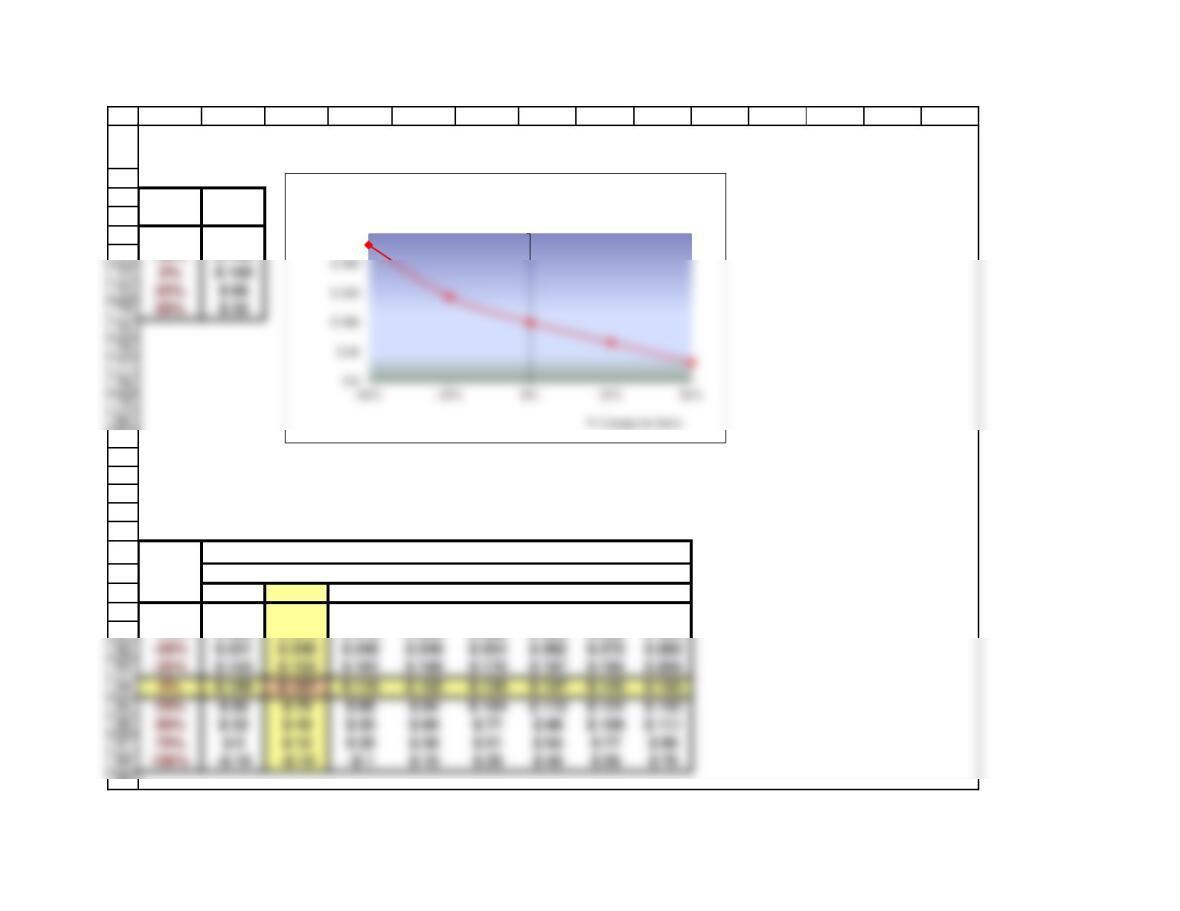

% Change

Max Loan

in Sales

$ 100

-50% $ 231

-25% $ 143

Q: If both sales and collections change, what will happen to the maximum loan requirement?

Answer: Do a sensitivity analysis.

Change

in Sales

$100 0% 1% 2% 3% 4% 5% 6% 7%

-100% $ 525 $ 525 $ 525 $ 525 $ 525 $ 525 $ 525 $ 525

-75% $ 368 $ 373 $ 378 $ 383 $ 388 $ 393 $ 398 $ 403

Maximum Loan Required

Bad Debt %

Here’s a sensitivity analysis for the effect of changes in sales on the maximum loan

requirement:

$ 250

Max Loan

Required

Max Loan Vs. Change in Sales

74

100

101

102

A B C D E F G H I J K L M N

The model could be used to analyze the effects of other variables, such as changing the

You can see from the table that, from the base case (Bad Debt % = 0, change in sales = 0), an

increase in late payers increases the loan requirement, as does a decline in sales.

15 Chapter model 12/12/2018

Calculation of APR and Effective Interest Rate on Add-on loan (Section 15-10d)

Amount received

$10,000.00

Rate per year

3.000%

Months

12

Banks and other lenders typically use add-on interest for automobiles and other types of installment

loans. The term add-on means that the interest is calculated and then added to the amount borrowed

to determine the loan’s face value. Suppose you borrow $10,000 on an add-on basis at a nominal rate

of 3.0% to purchase a car, with the loan to be repaid in 12 monthly installments. What are the

approximate rate of interest, the annual percentage rate, and the effective rate on your loan?

SECTION 15-10 12/12/2018

SOLUTIONS TO SELF-TEST QUESTIONS

4a. If a firm borrowed $500,000 at a rate of 10% simple interest with monthly interest payments

and a 365-day year, what would be the required interest payment for a 30-day month?

Nominal rate

10%

Amount borrowed

$500,000.00

Days/year

365

4b. If interest must be paid monthly, what would be the effective annual rate?

If interest had to be paid daily, the effective rate would be found as follows:

Effective rate = (1 + nom rate/365)^365 –1.0 = 0.10515578 or 10.52%

However, interest must be paid monthly, so the effective rate is lower, found as follows:

5a. If this loan had been made on a 10% add-on basis payable in 12 end-of-month

installments, what would be the monthly payments?

Find the total interest:

0.1 × $500,000 = $50,000.00

Find the total amount of the loan: $500,000 + $50,000 = $550,000

5b. What is the annual percentage rate?

5c. What is the effective annual rate?

Simple interest loan

Add-on Loan

Rate/day = nominal rate / 365 = (fraction, not %) 0.00027397