(2.) What is operating leverage, and how does it affect a firm’s business risk? Answer: See Chapter 15 Mini

1

2

3

4

5

6

7

8

12

13

14

15

16

17

18

19

20

21

22

23

24

25

26

27

28

29

30

33

36

37

38

39

40

A B C D E F G H I

12/10/2012

Situation

Percent Financed

with debt, wdrd

0% 0.0%

20% 8.0%

30% 8.5%

40% 10.0%

50% 12.0%

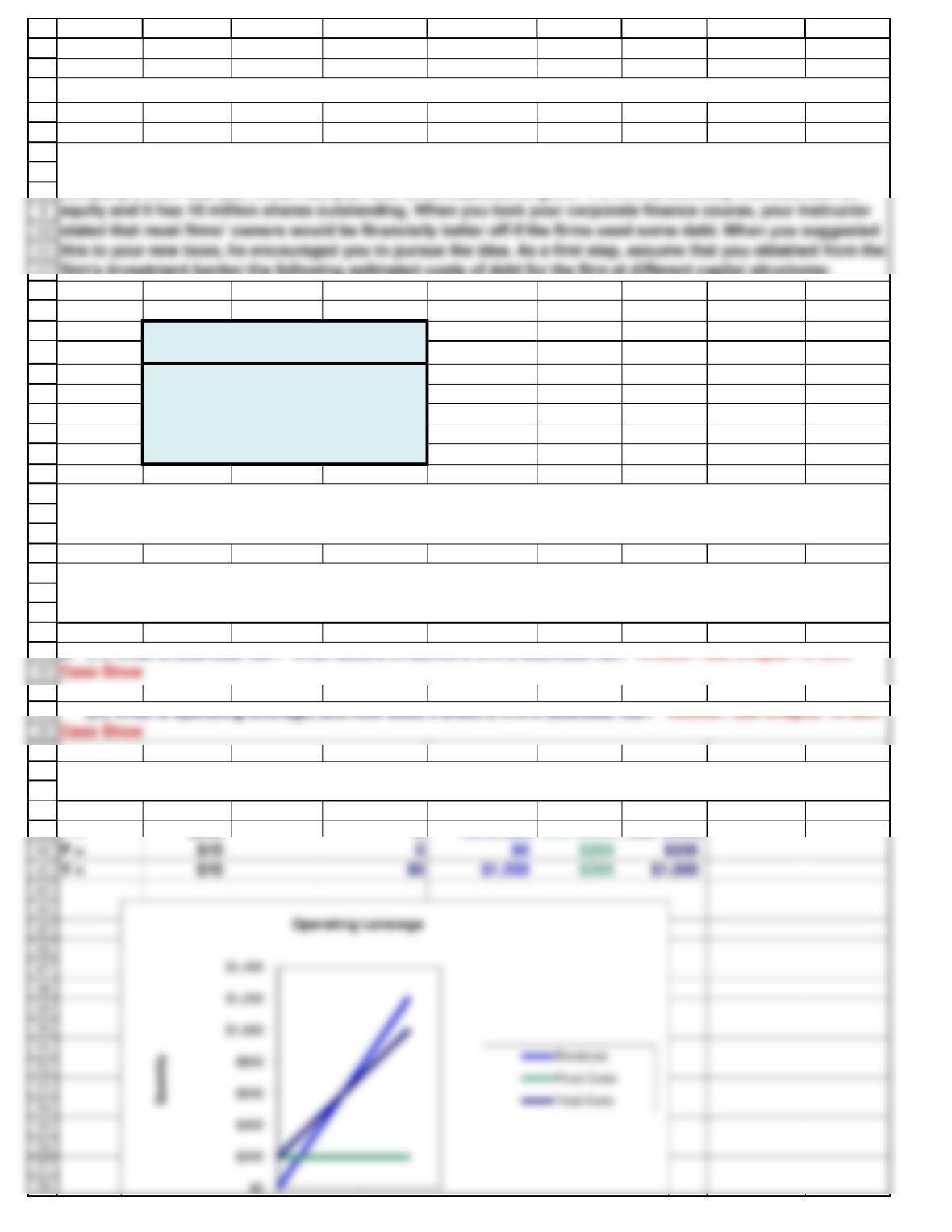

F = $200 QRevenues

Fixed Costs

Total Costs

Chapter 15. Mini Case

If the company were to recapitalize, debt would be issued, and the funds received would be used to repurchase

stock. Pizza Palace is in the 40% state-plus-federal tax bracket, the risk-free rate is 6 percent, and the market

risk premium is 6 percent.

a. Provide a brief overview of capital structure effects. Be sure to identify the ways in which capital structure

can affect the weighted average cost of capital and free cash flows. Answer: See Chapter 15 Mini Case Show

b. (1.) What is business risk? What factors influence a firm’s business risk? Answer: See Chapter 15 Mini

(3.) Show the operating break even point if a company has fixed costs of $200, a sales price of $15, and

variables costs of $10.

Assume you have just been hired as a business manager of PizzaPalace, a regional pizza restaurant chain. The

company’s EBIT was $50 million last year and is not expected to grow. The firm is currently financed with all

firm’s investment banker the following estimated costs of debt for the firm at different capital structures:

050 100

this to your new boss, he encouraged you to pursue the idea. As a first step, assume that you obtained from the

59

60

61

62

63

64

70

71

72

73

74

75

76

77

83

84

85

86

87

88

89

95

96

97

98

99

100

102

103

104

105

106

107

108

109

110

A B C D E F G H I

Q BE = FC / (P – VC)

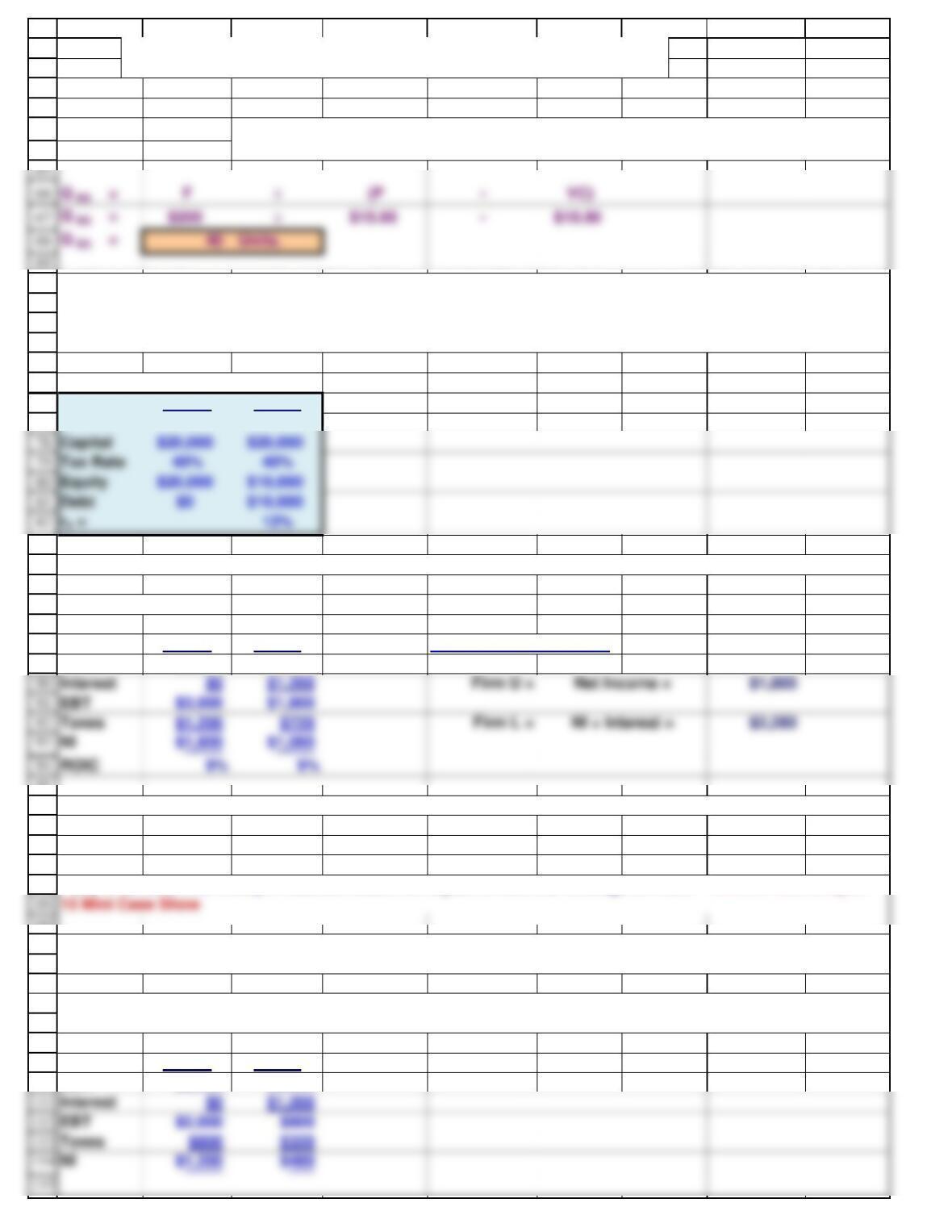

Two Hypothetical Firms

Firm U Firm L

Impact of Leverage

Firm U Firm L Distribution to Investors

EBIT $3,000 $3,000

ROE 9% 10.8%

Firm U Firm L

EBIT $2,000 $2,000

e. What happens to ROE for Firm U and Firm L if EBIT falls to $2,000? What does this imply about the impact of

leverage on risk and return?

In words, the quantity at which a firm breaks even is found as the difference between

Price and Variable costs divided by Fixed costs.

c. Now, to develop an example which can be presented to PizzaPalace’s management to illustrate the effects of

financial leverage, consider two hypothetical firms: Firm U, which uses no debt financing, and Firm L, which

uses $10,000 of 12 percent debt. Both firms have $20,000 in assets, a 40 percent tax rate, and an expected EBIT

of $3,000.

(1.) Construct partial income statements, which start with EBIT, for the two firms.

(2.) Now calculate ROE for both firms.

(3.) What does this example illustrate about the impact of financial leverage on ROE? Answer: See Chapter

d. Explain the difference between financial risk and business risk. Answer: See Chapter 15 Mini Case Show

$0 050 100

managers? Answer: See Chapter 15 Mini Case Show

135

rRF = 6.0%

116

117

118

119

120

122

123

125

126

127

128

129

130

131

136

137

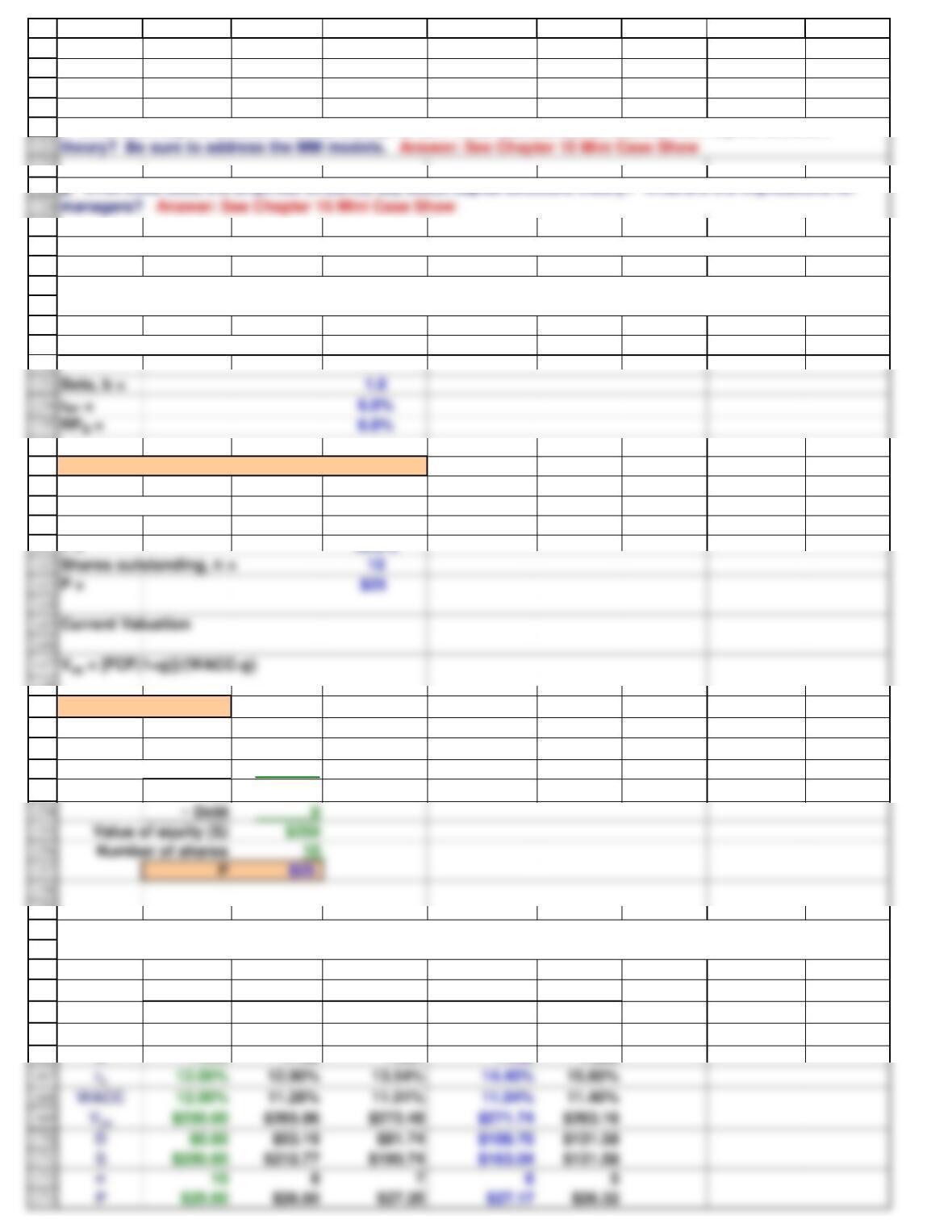

Vop = [FCF(1+g)]/(WACC-g)

rs12.00% 12.90% 13.54% 14.40% 15.60%

138

139

140

141

148

149

150

151

152

153

159

160

161

162

163

164

165

166

A B C D E F G H I

ROIC 6.0% 6.0%

ROE 6.0% 4.8%

Data for Recapitalization

rs= rRF + b(RPM) = 12%

Expected FCF = $30

g in FCF = 0%

T = 40.0%

Vop = $250

Vop $250

+ ST investments

0

VTotal $250

wd0% 20% 30% 40% 50%

rd0.0% 8.0% 8.5% 10.0% 12.0%

ws100% 80% 70% 60% 50%

b1.000 1.150 1.257 1.400 1.600

f. What does capital structure theory attempt to do? What lessons can be learned from capital structure

(1.) For each capital structure under consideration, calculate the levered beta, the cost of equity, and the

WACC.

h. With the above points in mind, now consider the optimal capital structure for PizzaPalace.

g. What does does the empirical evidence say about capital structure theory? What are the implications for

Investment bankers provided estimates of the cost of debt for different capital structures, as shown below.

Other rows are explained below the table.

theory? Be sure to address the MM models. Answer: See Chapter 15 Mini Case Show

rs= rRF + b(RPM) = 12.90%

Vop = $265.96

174

175

176

177

178

179

180

181

182

183

188

189

190

191

192

193

194

199

200

201

202

203

204

205

206

207

215

216

217

218

219

220

221

A B C D E F G H I

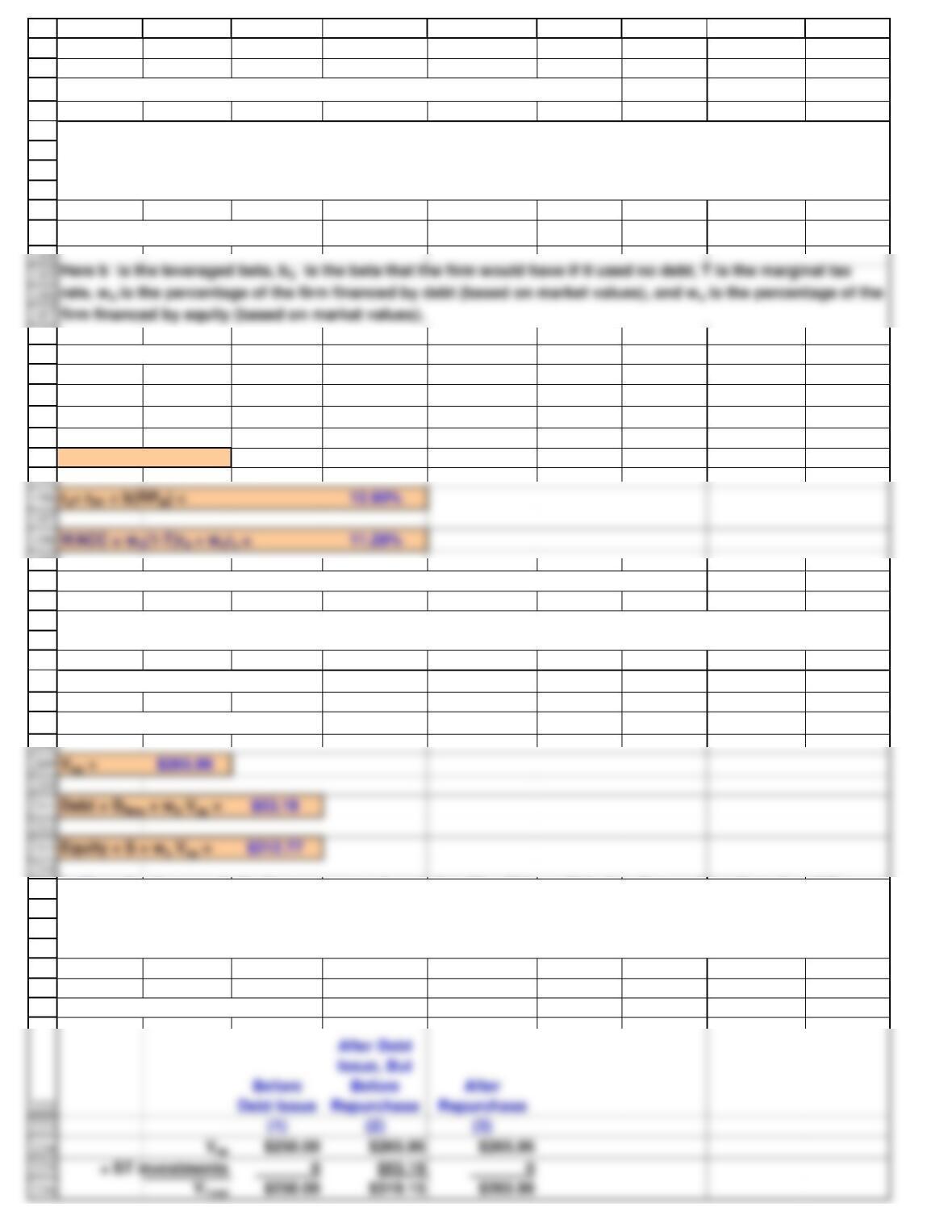

Estimating the Cost of Equity for Different Capital Structures

b = bU [1 + (1-T)(wd/ws)]

For example:

wd = 20%

ws = 80%

b = 1.15

The betas, cost of equity, and WACC at each debt level are shown in the table above.

Corporate Value for wd = 20%

Vop = [FCF(1+g)]/(WACC-g)

Consider a recap to 20% debt.

(2.) Now calculate the corporate value, the value of the debt that will be issued, and the resulting market value

of equity.

i. Describe the recapitalization process and apply it to PizzaPalace. Calculate the resulting the value of the

debt that will be issued, the resulting market value of equity, the price per share, the number of shares

repurchased, and the remaining shares. Considering only the capital structures under analysis, what is

PizzaPalace’s optimal capital structure?

Hamada developed his equation by merging the CAPM with the Modigliani-Miller model. We use the model to

determine beta at different amount of financial leverage, and then use the betas associated with different debt

ratios to find the cost of equity associated with those debt ratios. Here is the Hamada equation:

firm financed by equity (based on market values).

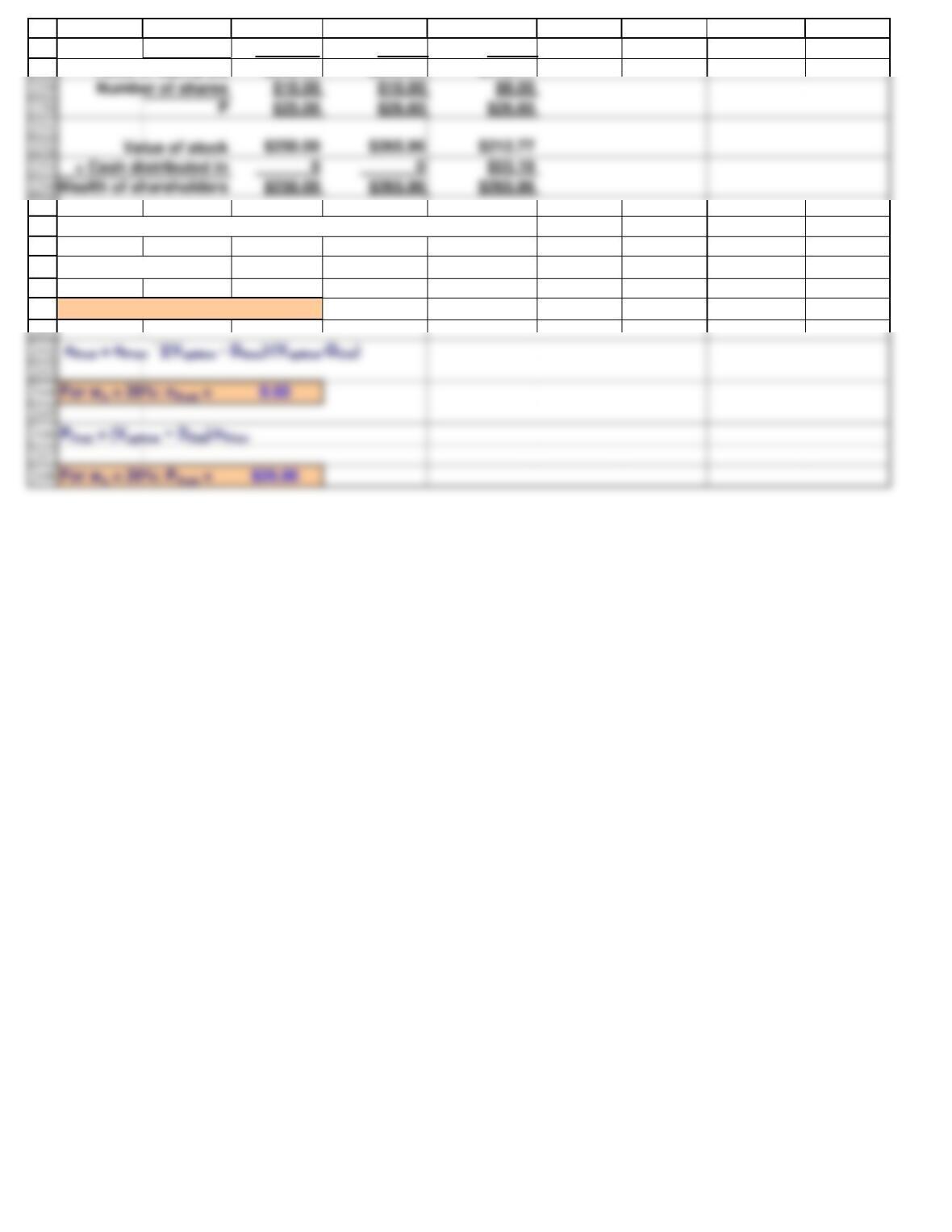

For wd = 20%: nPost = 8.00

PPost = (VopNew − DOld)/nPrior

For wd = 20%: PPost = $26.60

227

228

235

236

237

238

239

240

A B C D E F G H I

− Debt 0 $53.19 $53.19

Value of equity (S)

$250.00 $265.96 $212.77

Shortcuts for finding results after the repurchase:

S =(1- wd) (VopNew)

For wd = 20%: S = $212.77