Chapter 14

The Financial System and Economic Growth

◼ Chapter Outline, Overview, and Teaching Tips

Chapter Outline

The Role of the Financial System

Direct Finance

Indirect Finance

Information Challenges and the Financial System

Application: The Tyranny of Collateral

Government Regulation and Supervision of the Financial Sector

Financial Development and Economic Growth: The Evidence

Application: Is China a Counter-Example to the Importance of Financial Development to Economic

Growth?

Chapter 14 Web Appendix: Free Trade, Financial Globalization, and Growth

Chapter Overview and Teaching Tips

With the financial crisis that overwhelmed the world economy from 2007–2009, the public has become

more aware of the interaction between finance and economics. This part of the book provides an analytical

Chapter 14 The Financial System and Economic Growth 153

The next part of the chapter discusses why it is not easy to get the financial system to channel funds to

households and businesses with productive investment opportunities. The key barrier to getting this to

happen is asymmetric information, the fact that one party to a financial contract has different information

than the other party. There are three key concepts that students need to master to understand the material in

the rest of the chapter: adverse selection, moral hazard, and the free-rider problem. Because these three

concepts are so important, it is worth asking students in class to come up with examples of these problems

from their daily lives. This not only solidifies understanding of these concepts but also shows them how

relevant these concepts are to real-world issues. The chapter then uses these concepts to explain why

financial intermediaries like banks are so important in a financial system and why collateral is so prevalent

in debt contracts. The application, “The Tyranny of Collateral,” then provides graphic examples of how

barriers to having property serve as collateral helps keep some countries poor.

The final section of the chapter discusses the empirical evidence on the link between financial

development and economic growth. Although the evidence is quite strong that financial development plays

a key role in promoting economic growth, one economy that looks like a counterexample is China’s,

because its financial sector is relatively undeveloped and yet the economy has had very rapid growth in

recent years. Discussing this example in class, which appears as an application at the end of the chapter,

raises not only fascinating issues but also interests students because they want to better understand the rise

of China economically and possible pitfalls that China will face in the future.

◼ Answers to End of Chapter Review Questions and Problems

Answers to Review Questions

The Role of the Financial System

1. The financial system matches savers (those who have surplus funds) with borrowers who may have

good investment opportunities but no savings of their own to invest. Without a well-functioning

154 Mishkin • Macroeconomics: Policy and Practice, Second Edition

2. In direct finance, borrowers get funds from savers by selling them financial instruments (securities)

such as stocks or bonds. These securities give the lenders (savers) a claim to the borrowers’ future

Information Challenges and the Financial System

3. With both direct and indirect finance, the borrower generally has more information than the lender

does about the risk involved. This asymmetric (unequal) information creates two problems for

4. Investors in financial instruments who engage in information collection face a free-rider problem,

which means other investors may be able to benefit from their information without paying for it.

5. To overcome asymmetric information problems, banks screen potential borrowers before making

loans (to lessen adverse selection problems), monitor borrowers’ financial conditions and how they

6. Developing countries likely have weaker accounting and reporting standards, so accurate information

about private firms is more difficult to come by and also more difficult to analyze because of limited

Government Regulation and Supervision of the Financial Sector

7. The government can produce information about borrowers and provide it to investors free of charge,

it can require borrowers to report honest information about themselves to investors, and it can set and

8. Even though banks are well suited to overcome the adverse selection and moral hazard problems

inherent in lending because they make private loans and have incentives to invest in information

production about the borrowers to whom they lend, bank depositors face an asymmetric information

Chapter 14 The Financial System and Economic Growth 155

9. Governments provide safety nets to reduce the likelihood of bank runs and contagions because these

have adverse effects on the financial system and the economy. Deposit insurance and government’s

assurance that it will make funds available to troubled financial institutions are two forms that a

Financial Development and Economic Growth: The Evidence

10. Financial deepening refers to a country developing the institutions necessary to have a well-

functioning financial system. Where it has occurred, the benefits include increasing the rate of

Answers to Problems

The Role of the Financial System

1. A situation in which entrepreneurs cannot get credit to fund their investment projects is not a

desirable one from an efficiency point of view. Although it is true that many ideas will not result in

2. Funds were definitely not allocated to their most productive use. Funds are allocated to their most

productive use when considerations about which individual or firm should receive these funds are

based on risk and expected returns associated with the investment. The situation in which funds are

Information Challenges and the Financial System

3. a. The loan officer is trying to assess your credit risk by gathering information about your income (past

and current employment) and credit history to avoid the adverse selection problem. The loan office

is essentially making sure that you will have the ability and willingness to pay back your car loan.

156 Mishkin • Macroeconomics: Policy and Practice, Second Edition

b. By putting a lien on your car title, the bank solves (or reduces) the moral hazard problem. The bank

wants to make sure you will use your loan to buy a car (a problem that is sometimes solved by

4. During your visit at the bank you will probably realize that your will receive an annual interest rate of

1 percent or 2 percent if you buy a certificate of deposit, while an individual asking for a car loan will

be required to pay an annual interest rate of 7 percent or 8 percent. At the beginning, it seems

tempting for you to offer an interest rate of 4 percent, which would make both of you better off.

However, you would probably like to know that individual better, in particular his net worth (to

assess his ability to pay you back), or his credit history (has he or she defaulted on a loan before?).

5. Information asymmetries are also present in government bond markets. Usually investors resort to

many information sources about the characteristics of particular governments to assess their ability or

6. Financial intermediaries operating in countries with relatively weak property rights and legal systems

usually require a lot of collateral when making loans. The rationale for that behavior is that in the event

that the borrower defaults, the bank knows that it will be quite difficult and expensive to recover its

loan. Therefore, requesting extra collateral might help the bank speed up the process. In practice, a

Government Regulation and Supervision of the Financial Sector

7. In the U. S. financial system, trading in derivatives is concentrated in five large banks and

transactions are kept relatively private, for the same reason that banks do primarily private loans (to

Chapter 14 The Financial System and Economic Growth 157

8. Although it might seem a good idea to “copy and paste” regulatory frameworks that ensure the

soundness of a financial system from one country to the other, this is usually not a good idea.

Financial Development and Economic Growth: The Evidence

9. As more individuals and firms participate in the financial system, monetary policy becomes more

effective. When more firms and borrowers rely on financial intermediaries, monetary policy tools

have a more immediate effect on monetary aggregates. Monetary policy tools affect financial

10. Microcredit programs were very effective in defining a set of incentives that helped to deal with

asymmetric information problems. As a result, microcredit loans usually exhibit higher repayment

rates (the percentage of loans that are actually repaid) than regular loans made by financial intermediaries.

Solving the adverse selection problem was never the intention of microcredit schemes because the

◼ Answers to Data Analysis Problems

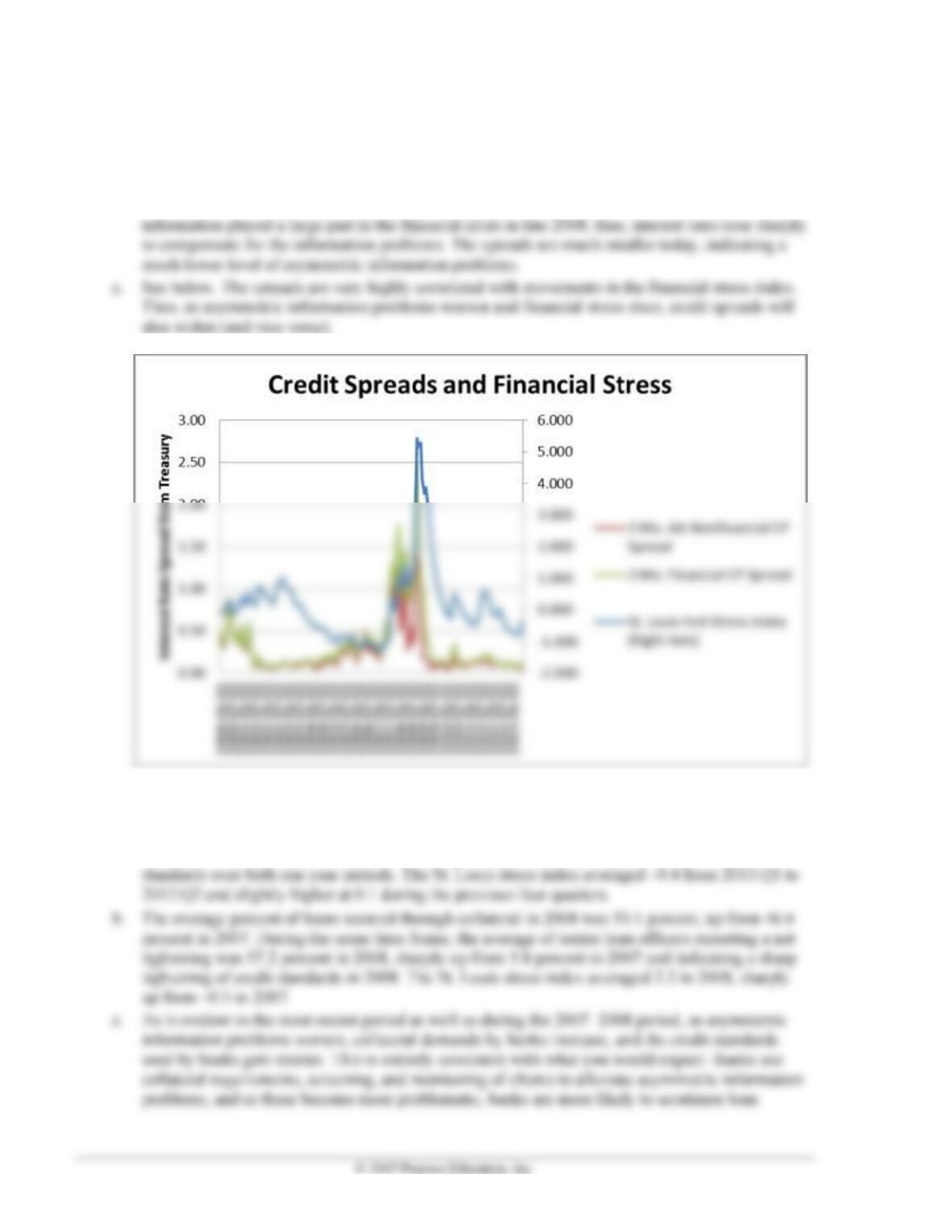

1. a. For June 2013, the AA nonfinancial commercial paper spread was 0.05, and the AA financial

commercial paper spread was 0.09. These are relatively small margins over the treasury rate and

158 Mishkin • Macroeconomics: Policy and Practice, Second Edition

fairly close to each other, indicating relatively low risk between commercial paper and the risk–

free (treasury) rate.

b. In June 2012, both AA nonfinancial commercial and the AA financial commercial paper spread

was 0.12, slightly higher than the most recent reading and indicating slightly higher risk. In

October 2008, these spreads widened significantly to 1.40 and 2.52, respectively. Asymmetric

2. a. From 2013:Q1 to 2012:Q2, the average percent of loans secured through collateral was 51.3

percent, down from 58.4 percent from the previous four quarters. During the same time frame,

the average of senior loan officers reporting a net tightening was –7.9 percent during the recent

period and –9.7 percent in the previous four quarter period, indicating an easing of credit

Chapter 14 The Financial System and Economic Growth 159

3. a. See table below.

b. See table below. There is a clear relationship between financial/investment freedom and per

capita growth in the data: from 1995 to 2005, the top three countries grew by 2.9 percent, while

the bottom three grew by only 1.62 percent. From 2005 to 2011, the top three grew by almost 1

percent, while the bottom three shrank slightly with a –0.12 percent growth rate

to 2011 period than the bottom three.

USA

Italy

France

Czech

Republic

United

Kingdom

Australia

1995 to 2005

2.28

1.05

1.53

3.19

2.99

2.53

2005 to 2011

0.19

1.89

0.98

Top 3

1995 to 2005

2.90

1.62

2005 to 2011

0.94

-0.12

◼ Answers to Review Questions and Problems in Appendix, “Free

Trade, Financial Globalization, and Growth”

1. Financial repression refers to efforts to impede the development of financial markets and institutions

2. Financial repression is supported by government officials and rich elites in developing countries.

Government officials profit from expropriating private property and promoting state-owned banks for

3. Free trade increases competition that reduces the revenues and profits of firms in developing

economies and makes it more likely that they will need to seek external sources of financing. This

4. Financial globalization opens markets to flows of foreign capital and competition from foreign financial

institutions. This gives domestic financial institutions incentives to become more efficient and adopt

160 Mishkin • Macroeconomics: Policy and Practice, Second Edition

◼ Data Sources, Related Articles, and Discussion Questions

A. For Information About Application: The Tyranny of Collateral

Data Source

De Mel, Suresh et al., “Who Are the Microenterprise Owners? Evidence from Sri Lanka on Tokman v. De

Related Article

Darlington, Shasta (CNN), “Rio slum transformed into canvas bursting with color”:

America: Rio de Janeiro. This is mainly a consequence from the lack of collateral needed to get a

mortgage loan (note especially picture 8).

Discussion Question

During the most virulent phase of the 2007–2009 financial crises, the U.S. government enacted measures

to prevent the increase in foreclosures, as many families were losing their homes. Many people criticized

this action, arguing that seizing collateral in the event of default was part of the mortgage contract. Explain

how this situation exemplifies the role played by collateral in solving asymmetric information problems.

Answer: Critics of the government’s actions defended that contracts must be properly enforced. Otherwise,

B. For Information About Application: Is China a Counter-Example to the

Importance of Financial Development to Economic Growth?

Data Source

Federal Reserve Bank of St. Louis data base (FRED):

Related Article

Yin, Y.P. et al., “Decomposition of the Efficiency of the Chinese State-Owned Commercial Banks at the

Chapter 14 The Financial System and Economic Growth 161

Discussion Questions

Assuming China does not reform its financial system and keeps relying on state-owned banks to channel

funds from savers to borrowers, which do you think would be the consequences in term of efficiency? Can

you identify a potential benefit from state-owned banks channeling funds?

Answer: As empirical evidence suggests, a state-owned financial system tends to be less efficient than a