CHAPTER 14

MONETARY POLICY AND THE BANK OF CANADA

LEARNING OBJECTIVES

I. Goals of Chapter 14

A. Look at how the money supply is determined

B. Explore the question: How should the central bank conduct monetary policy?

1. Should the central bank offset cyclical fluctuations?

2. Should the central bank follow simple rules?

3. How should policy-making institutions be designed?

II. Notes to Sixth Edition Users

TEACHING NOTES

I. Principles of Money Supply Determination (Sec. 14.1)

A. Three groups affect the money supply

1. The central bank is responsible for monetary policy

B. The money supply in an all-currency economy

1. A trading system based on barter is inconvenient

2. The creation of a central bank to print money can improve matters

a. The central bank uses money it prints to buy real assets from

the public; this gets money in circulation

3. In an all-currency economy, the money supply equals the monetary

base

C. The money supply under fractional reserve banking

270 Chapter 14

a. In this case, the consolidated balance sheet of banks has

3. The currency that banks hold is called bank reserves

a. When bank reserves are equal to deposits, the system is called

4. Rather than holding reserves that earn no interest, suppose a bank

lent some of the reserves

a. It could do this, since the flow of money in and out of the bank is

5. When all the banks catch on to this idea, they will all make loans as the

economy undergoes a multiple expansion of loans and deposits

6. The process stops only when the banks’ currency holdings (reserves)

are exactly 20% of their total deposits, with loans equal to 80% of total

deposits

a. For example, if the monetary base is $1 million, banks would

Numerical Problem 1 gives students practice dealing with bank balance sheets.

7. The money supply in this economy is equal to the total amount of bank

deposits ($5 million in the example)

8. The relationship between the monetary base and the money supply

can be shown algebraically

a. Let M = money supply, BASE = monetary base, DEP = bank

deposits, RES = bank reserves, res = banks’ desired reserve-

Monetary Policy and the Bank of Canada 271

9. Each unit of monetary base allows 1/res of money to be created

10. The monetary base is called high-powered money because each unit

of the base that is issued leads to the creation of more money

D. Bank runs

1. In the example, banks plan on never having to pay out more than 20%

of their deposits

E. The money supply with both public holdings of currency and fractional reserve

banking

1. If there is both public holding of currency and fractional reserve

banking, the picture gets more complicated

2. The money supply consists of currency held by the public and

deposits, so M = CU+ DEP (14.4)

9. The term (cu + 1)/(cu + res) is the money multiplier

a. The money multiplier is greater than 1 for res less than 1 (that

Numerical Problems 2 and 3 deal with the money multiplier.

F. Open-market operations

1. The most direct and frequently used way of changing the money

supply is by raising or lowering the monetary base through open-

market operations

2. To increase the monetary base, the central bank prints money and

272 Chapter 14

c. For a constant money multiplier, the decline or fall in the

Policy Application

Most of the use of open-market operations turns out not to be related to changes in

monetary policy at all, but rather to changes in money demand. There’s a seasonal

component to money demand, which the Bank of Canada offsets by changing money

supply so that interest rates don’t change over the seasons. There are also other factors

that affect the money supply, such as the government’s use of funds. The Bank offsets

these factors as well.

II. Monetary Control in Canada (Sec. 14.2)

A. The Bank of Canada

1. The Bank of Canada was created in 1934, partly in response to

political pressures arising from the Great Depression

2. Since 1938 the Bank has been a crown corporation with headquarters

binding directive to the Bank in the event of a disagreement

4. But in reality the Bank has more independence than the Bank of

Canada Act suggests

a. The government refrains from public criticism of the Bank’s

actions

b. It is widely accepted that if a directive were to be issued to the

B. The Bank of Canada’s Balance Sheet

1. Balance sheet of Bank

a. Largest Asset is the holdings of government securities (Table

14.2)

b. Also owns foreign currencies and makes loans to banks and

trust companies

2. The monetary base equals bank reserves plus currency in circulation

C. 1. Tools of Monetary Policy

2. Overnight Rates (the most commonly used instrument of monetary

control)

Monetary Policy and the Bank of Canada 273

a. Most money in Canada is in the form of demand deposits. To

allow cheques to clear between banks, they hold balances at

the Bank of Canada called settlement balances

b. $100 cheque written on National Bank to Royal Bank, while an

Peter Howitt of Ohio State University discusses the institutional setting of Canadian

monetary policy and the relationship between the Bank of Canada and the government

in Canada, in Michelle Fratianni and Dominick Salvatore, Monetary Policy in Developed

Economies: Handbook of Comparative Economic Policies, volume 3 (Westport, Conn:

Greenwood Press) 1993. Howitt concludes that to a large extent the governor of the

Bank of Canada solely determined Canadian monetary policy.

3. Open Market Operations

a. By open market purchase or sale of government securities, the

Bank could increase or reduce the monetary base

b. The Bank uses Special Purchase and Resale Agreements

Policy Application

In January 1999, the Bank of Canada’s operating procedures for making monetary

policy changed as a result of the introduction of the Large-Value Transfer System. The

changes are explained in Donna Howard’s article, “A Primer on the implementation of

Monetary Policy in the LVTS Environment” in Bank of Canada Review, Autumn 1998.

D. The Exchange Fund Account

a. The Bank of Canada also manages the government’s holding of

various foreign currencies (the exchange fund account) (Table

14.3)

274 Chapter 14

d. A Closer Look 14.1: The Bank of Canada’s Response to the

Financial Crisis

(1)The Bank of Canada introduced 4 extraordinary measures to

add liquidity during the financial crisis:

(i) the Bank extended beyond one business day of length of

(2) These measures were guided by 5 principles:

(i) the Bank should target distortions of systemwide

importance

(3) The general consensus is that were it not for the innovative

policies of the Bank of Canada and other major central

banks around the world, the impacts would have been

significantly worse.

E. Intermediate Targets

a. Bank faces the problem of how to use the tools it has to achieve

its desired goals

d. If most shocks are LM shocks the Bank might want to target

interest rates

(1) Without intervening, output and interest rates would be

volatile

e. A Closer Look 14.2: Making Monetary Policy

(1) Since 1991, the Bank of Canada has committed to inflation

targeting

Monetary Policy and the Bank of Canada 275

(4) After reviewing the QPM results and the final briefing by

F. Setting monetary policy in practice

2. Lags in the effects of monetary policy

a. It takes a fairly long time for changes in monetary policy to have

an impact on the economy

3. The channels of monetary policy transmission

a. Exactly how does monetary policy affect economic activity and

prices? There are two effects discussed in the textbook so far

(1) The interest rate channel: as seen in the IS–LM model, a

decline in money supply raises real interest rates, reducing

b. How important are these different channels?

(1) Suppose real interest rates are high, but the dollar has

been falling; is monetary policy tight or easy? It depends

III. The Conduct of Monetary Policy: Rules Versus Discretion (Sec. 14.3)

A. Monetarists and classical macroeconomists advocate the use of rules

1. Rules make monetary policy automatic, as they require the central

bank to set policy based on a set of simple, prespecified, and publicly

276 Chapter 14

3. The rule should be simple; there shouldn’t be much leeway for

exceptions

B. Most Keynesians economists support discretion

1. Discretion means the central bank looks at all the information about the

economy and uses its judgment as to the best course of policy

C. The monetarist case for rules

1. Monetarism is an economic theory emphasizing the importance of

monetary factors in the economy

main source of business cycles

b. Proposition 2: Despite the powerful short-run effect of money on

the economy, there is little scope for using monetary policy

actively to try to smooth business cycles

(1) First, the information lag makes it difficult to know the

current state of the economy

(2) Second, monetary policy works with a long and variable

c. Proposition 3: Even if there is some scope for using monetary

policy to smooth business cycles, the central bank cannot be

relied on to do so effectively

(1) Friedman believes the central bank responds to political

Monetary Policy and the Bank of Canada 277

d. Proposition 4: The central bank should choose a specific

monetary aggregate (such as M1 or M2) and commit itself to

making that aggregate grow at a fixed percentage rate. year in

be gradually lowered over time

D. Rules and central bank credibility

1. New arguments for rules suggest that rules are valuable even if the

central bank has a lot of information and forms policy wisely

2. Rules, commitment, and credibility

a. How does a central bank (or a dad) gain credibility?

b. One way to get credibility is by building a reputation for following

through on its promises, even if it’s costly in the short run

c. Another, less costly, way is to follow a rule that is enforced by

(4) So a rule may create unacceptable risks

3. The Taylor Rule

a. The Taylor rule is given by i = π + 0.02 +0.5y + 0.5(π–0.02)

(14.9)

b. If the economy is “overheating” with output growing more rapidly

than full-employment and inflation rising, the Taylor rule

suggests that the Bank of Canada should tighten monetary

278 Chapter 14

Policy Application

For a good description of the rules versus discretion issue applied to monetary policy,

see the article by Herb Taylor, “Time Inconsistency: A Potential Problem for

Policymakers,” Federal Reserve Bank of Philadelphia Business Review, March/April

1985, pp. 3–12.

E. Application: Shooting at targets: past, present, future

1. High unemployment and high inflation in the 1970s led central banks

worldwide to experiment with alternative strategies for monetary policy,

including targeting money growth and targeting inflation

2. Money-growth targeting

a. Germany’s Bundesbank introduced money-growth targets in

1975 and has used the strategy ever since

b. The US, Canada, the US, Switzerland, and others also adopted

d. Bank of Canada announce targets in 1975 of 10–15% growth

for M1 as part of the policy of gradualism

(1) Monetarists disagreement with Bank’s policy

(2) M1 growth rates fell substantially between 1975 and 1982

f. Most countries that used money-growth targeting (including

Data Application

Students can easily see whether the Bank of Canada is meeting its inflation targets by

inspecting a graph in the Monetary Policy Report twice each year. The graph shows the

actual inflation rate and the target range since 1990. The report can be viewed at the

Bank of Canada web site.

3. Inflation targeting

a. Since 1990, some countries have switched from targeting

money growth to targeting inflation

Monetary Policy and the Bank of Canada 279

b. Under inflation targeting, the central bank announces targets for

inflation over the next 5 years

c. Advantages of inflation targeting over money-growth targeting

(1) It avoids the problem of instability in money demand

d. Disadvantages of inflation targeting relative to money-growth

targeting

(1) Inflation responds to policy actions with a long lag, so it’s

hard to judge what policy actions are needed to hit the

4. Price level targeting

a. It provides more certainty about the long term purchasing power

of money than does inflation targeting

is that it provides the central bank with greater flexibility

F. Other ways to achieve central bank credibility

1. Appointing a “tough” central banker

a. Appointing someone who has a well-known reputation for being

tough in fighting inflation may help establish credibility for the

2. Changing central bankers’ incentives

a. People are more likely to believe a central bank is serious about

3. Increasing central bank independence (text Fig. 14.3)

a. If the executive and legislative branches of government can’t

interfere with the central bank, people are more likely to believe

280 Chapter 14

ADDITIONAL ISSUES FOR CLASSROOM DISCUSSION

1. Should There Be One Currency per Country?

There is an old literature in international finance which discusses the question of the

optimal area within which a single currency should be used. To most people a ‘single

currency area’ coincides with the nation state. However, economists have speculated

2. The Goal of Zero Inflation

The Bank of Canada’s zero inflation policy has moved Canada down the rankings from

a ‘high-inflation’ country in the 1970s and early 1980s to a ‘low inflation’ country in the

1990s. In 1998-1999, Canada’s annual inflation rate was about 1.2%. This contrasts

with inflation rates of 14 percent in the late 1970s.

Monetary Policy and the Bank of Canada 281

3. Monetary Policy in a Multi-Region Country

Canada’s different regions have very different economic cycles. In the late 1980s,

Ontario was booming, while much of the Prairies and British Columbia had not fully

ANSWERS TO TEXTBOOK PROBLEMS

Review Questions

1. The monetary base, or high-powered money, consists of the liabilities of the central

bank that are usable as money. In an all-currency economy, the money supply

equals the monetary base.

2. The money multiplier is the number of dollars of the money supply that can be

created from each dollar of monetary base. In a system of 100% reserve banking,

the reserve-deposit ratio is one and the money multiplier is one. Under fractional

3. Changes in the desire by the public for holding currency affect the currency-deposit

ratio, thus changing the money multiplier. Similarly, changes in banks’ desire to

4. Suppose the Bank lowers the operating band for the overnight rate. This

encourages banks to borrow reserves and increases the overnight rate. Since

interest rates tend to move together, the rise in the overnight rate will tend to drive

up other interest rates. This will lead to a fall in the money supply.

282 Chapter 14

7. The three channels of monetary policy transmission are the interest rate channel,

the exchange rate channel, and the credit channel. The interest rate channel arises

because tighter monetary policy raises the real interest rate, which reduces

8. The monetarist response to the argument that discretion is more flexible than

following a rule is to argue that (1) because of information lags, it is difficult for the

central bank to tell what the appropriate policy is at a particular time; (2) there are

9. The use of money-growth or inflation targets does not seem to have increased

central bank credibility significantly in any country other than Japan. In other

countries, including the United States, Germany, and Canada, disinflations based

independent.

Numerical Problems

1. Initial balance sheet of banks (all amounts in florins):

Assets Liabilities

Reserves 500 000 Deposits 500 000

Banks want to hold reserves equal to only 20% of deposits. This is 0.20 x 500 000

Monetary Policy and the Bank of Canada 283

can lend another 160 000. Of this amount, 80 000 comes back to the bank in the

form of new deposits, and the other 80 000 is held by the public in the form of

currency and half is in deposits, these are each equal to 833 1/3 thousand florins.

With a reserve-deposit ratio of 0.2, total reserves held by banks are 0.2 x 833 1/3 =

166 2/3 thousand florins. The final balance sheets are:

Central Bank

2. Dollar amounts are in millions of dollars.

a. DEP = M – CU = 6 – 2 = 4.

RES = res × DEP = 0.25 × 4 = 1.

3. a. res = 0.4 – 2(0.10) = 0.2.

multiplier = (cu + 1) / (cu + res) = (0.4 + 1) / (0.4 + 0.2) = 2 1/3.

M = multiplier x BASE = 2 1 /3 × 60 = 140.

284 Chapter 14

d. If the reserve-deposit ratio is unaffected by the real interest rate, the LM curve

is steeper than when it is affected by the real interest rate. To see why,

consider the effect of a decline in the real interest rate. If the reserve-deposit

ratio is affected by the real interest rate, the fall in the real interest rate causes

banks to hold more reserve, since they are cheaper (they have a lower

Analytical Problems

1. a. The increase in banks’ reserve-deposit ratio reduces the money multiplier,

causing the money supply to decline.

b. The increased holding of cash raises the currency-deposit ratio, reducing the

money multiplier and causing the money supply to decline.

Monetary Policy and the Bank of Canada 285

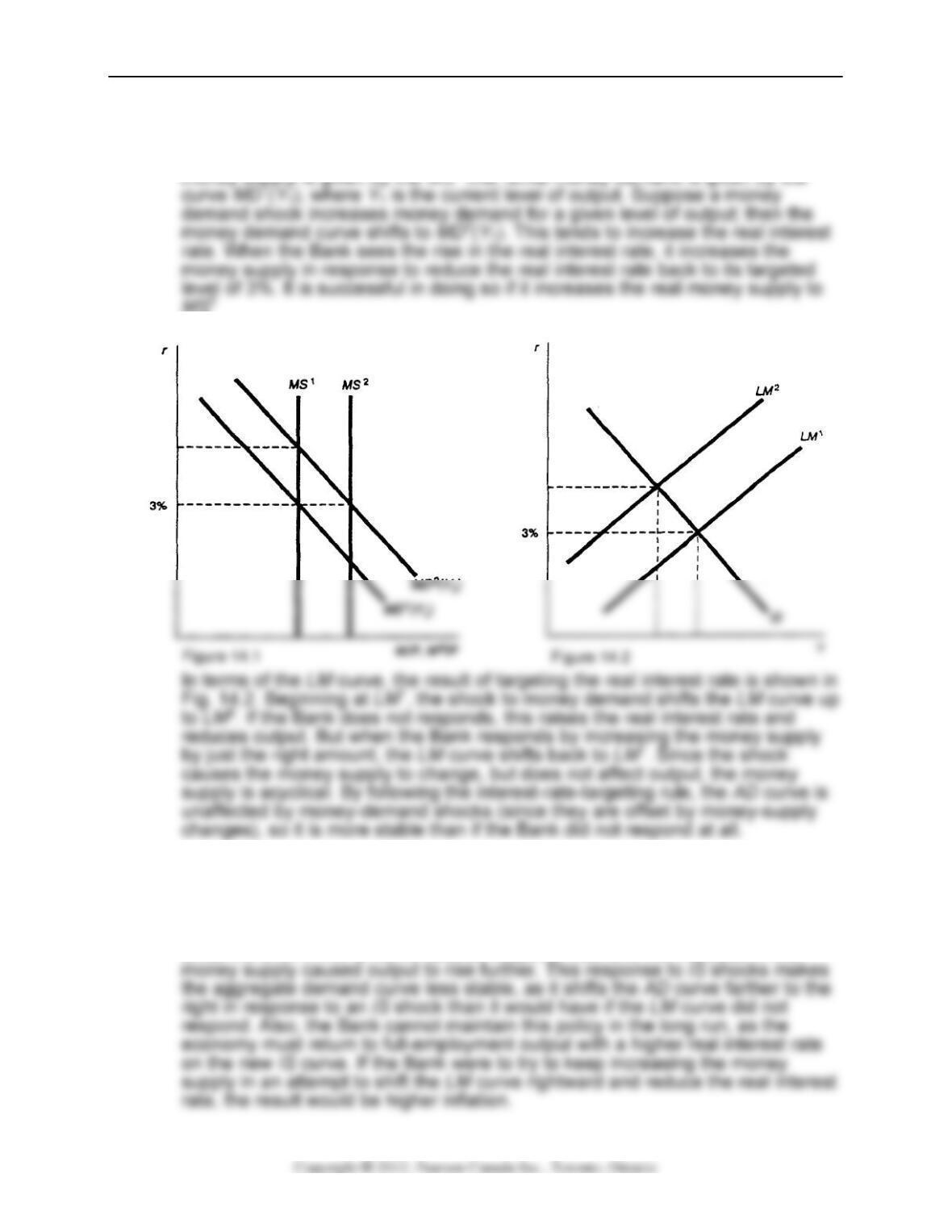

2. a. If the Bank targets the real interest rate, then money demand shocks are offset

by changes in the money supply, so the LM curve does not move. To see this,

look at Fig. 14.1, which depicts the result in a Keynesian model. Initially, real

MS2

b. When there are IS shocks, the rule does not work very well. Suppose a shock

shifts the IS curve from IS1 to IS2, as shown in Fig. 14.3. Targeting the real

interest rate requires the Bank to increase the money supply to shift the LM

curve from LM1 to LM2. While this maintains the real interest rate at its initial

level, output is above full-employment output. The money supply is procyclical,

since the shift in the IS curve caused output to rise, and the increase in the

286 Chapter 14

c. When there are aggregate supply shocks, the rule also does not work very well.

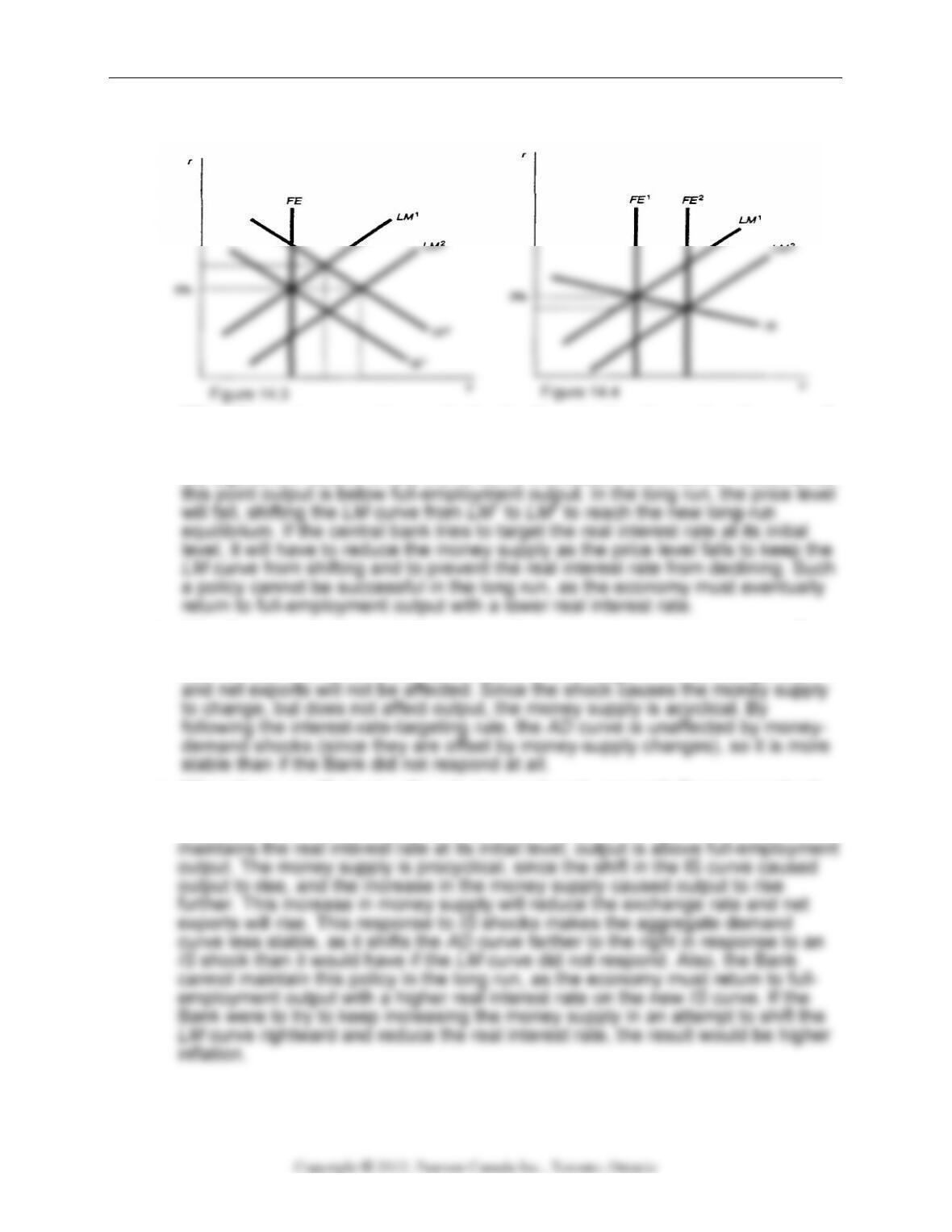

Suppose a supply shock shifts the FE line from FE1 to FE2, as shown in Fig.

14.4. In the short run, there is no effect on output or the real interest rate, since

the equilibrium occurs where the IS curve intersects the LM curve. However, at

d. If the Bank targets the real interest rate, then money demand shocks are offset

by changes in the money supply, so the LM curve does not move. Since the

real interest rate remains the same, there is no change in the exchange rate

e. When there are IS shocks, the rule does not work very well. Suppose a shock

shifts the IS curve to the right. Targeting the real interest rate requires the Bank

to increase the money supply to shift the LM curve to the right. While this

Monetary Policy and the Bank of Canada 287

3. To examine Taylor’s rule, we’ll use the classical model with misperceptions.

a. An increase in money demand causes the aggregate demand curve to shift to

the left, reducing the price level and inflation and decreasing output, if the

money supply is unchanged. In response to these changes in output and

c. An adverse supply shock causes the aggregate supply curve to shift to the left,

increasing the price level and inflation and decreasing output, if the money

supply is unchanged. Assuming that output decreases more than full-

employment output, in response to these changes, Taylor’s rule is ambiguous

about which way to move the nominal Fed funds rate, since higher inflation

increases the funds rate but lower output decreases the funds rate.