CASE STUDY EXTENSION

14–4 Anticipated and Unanticipated Money

Robert Barro pioneered another test of the imperfect–information model.1 An implication of that model is

that anticipated changes in the money supply affect the price level, not output, because anticipated

changes in the money supply increase the expected price level and cause the aggregate supply curve to

shift upward. Unanticipated changes in the money supply affect output.

329

ADVANCED TOPIC

14–5 Is Price Flexibility Stabilizing?

The basic aggregate demand–aggregate supply model suggests that fluctuations in output arise because

shocks cause aggregate demand to fluctuate along an upward–sloping aggregate supply curve. The

aggregate supply curve may slope upward because of price or wage stickiness. This suggests that output

fluctuations will be smaller if prices are more flexible. In particular, if there is a negative shock to

aggregate demand, output will generally fall less, and prices fall more, depending on how steep the

aggregate supply curve is.

There are circumstances, however, in which price flexibility may not make the economy more

stable.11 The basic idea comes from the Fisher equation, which tells us that the real rate of interest equals

the nominal rate minus the expected inflation rate and the fact that aggregate demand depends upon the

real interest rate. Suppose that a fall in aggregate demand leads to a fall in prices, and suppose that falling

prices lead in turn to expectations that prices will fall further in the future. Then falling prices lead to a

decrease in expected inflation and hence an increase in the real interest rate. This leads to a further fall in

aggregate demand. As discussed in Chapter 12, some economists believe that this destabilizing effect of

330

LECTURE SUPPLEMENT

14–6 How Long Is the Long Run? Part Three

Earlier chapters discussed the meaning of the long run in terms of the classical model of Chapter 3 and the

Solow growth model of Chapters 8 and 9. The classical model is a long–run model because prices are

flexible and adjust to ensure that all markets are in equilibrium. The short–run models of Part IV of the

textbook, by contrast, assume some price stickiness, implying that the long run is however long it takes for

prices to be flexible. In the short run, therefore, the aggregate supply curve slopes upward; in the long run,

it is vertical.

ADVANCED TOPIC

14–7 Policy Ineffectiveness

The imperfect–information model of aggregate supply was very influential in the 1970s. One reason is that

it provided a basis for a radical reexamination of the ability of the Federal Reserve to influence the

economy. In particular, two new classical economists, Thomas Sargent and Neil Wallace, put forward a

policy–ineffectiveness argument to the effect that, if people had rational expectations, monetary policy

could not be used to stabilize the economy.11

The basic idea is that people’s expectations about the price level are influenced by their expectations

about the Fed’s actions. Rational individuals understand that if the Fed wishes to stimulate aggregate

demand, it will increase the money supply. They understand further that a higher money supply will raise

where y is output,

y

is the natural rate of output, p is the price level, pe is the expected price level, and we

assume that all variables are in logarithmic terms. Second, we have a simple aggregate demand equation:

y=y+

θ

m−p

( )

+u.

(2)

This equation says that demand depends upon the real money supply (m – p) and a random shock (u). We

suppose for the moment that this shock is observed by everybody, so both the Fed and the private sector

can react to it. The equation is written so that if u = 0, output is at its natural rate when p = m. Finally, we

suppose that the Fed may try to set monetary policy on the basis of the shock to aggregate demand. We

write this as

m = m(u). (3)

The first thing we do is to eliminate p between equations (1) and (2) to get a solution for y. Equation (2)

implies that

p=m–y–y

( )

/

θ

+u/

θ

.

(4)

Substituting (4) into (1) gives

y=y+

α

m−y−y

( )

/

θ

+u/

θ

−pe

( )

,

(5)

332

p

(since this implies y =

y

).

Sargent and Wallace, however, suggested that it wasn’t correct to think about people’s expectations of

the price level as being independent of their expectations of the money supply, for the reasons argued

earlier. They assumed that people had rational expectations. This means that their expectation of the price

is their best possible guess, given the information they have. We write this as pe = E(p), where E( ) is the

symbol for a mathematical expectation. In this case, our first task is to find out what determines people’s

price expectations.

To do so, we go back to equation (4):

p=m–y–y

( )

/

θ

+u/

θ

.

(4)

Using this, we find that

pe=E p

( )

=E m

( )

−E y

( )

−E y

( )

( )

/

θ

+E u

( )

/

θ

(9)

( )

( )

( )

( )

( )

( )

=y.

(10)

This uses the fact that the best guess of a best guess is just the best guess, so the second term equals zero.

The aggregate supply equation, in other words, tells us that, on average, output is at its natural rate. So,

from equations (9) and (10),

pe = E(m) + u/θ. (11)

We have now solved for price expectations. Plugging this into the solution for y [equation (7)], we get

p

pe

AS (pe)

AD (m, u)

yy

Figure 1

p

333

What happens if the Fed thinks that people have static expectations, but they actually have rational

expectations? The Fed wishes to stabilize output and so sets the money supply according to the rule

determined in equation (8):

m=p−u/

θ

.

(8)

But people have rational expectations about the Fed and can infer its rule. Thus

E m

( )

=p−u/

θ

=m.

(13)

y=y+

α

/

θ

+

α

( )

( )

u.

(14)

Neither the Fed nor the private sector could do anything about this uncertainty.

Now suppose, however, that the private sector does not observe u, but the Fed does. Then pe = E(m) =

p

. In this case the Fed is able to offset the u shocks by means of monetary policy. When the Fed has an

information advantage, there is room for countercyclical stabilization policy in this model, but not

otherwise.

The policy–ineffectiveness proposition is an example of the Lucas critique, which is discussed in

Chapter 14 of the textbook. The point is that people’s expectations of economic variables are not

independent of the actions of policymakers, since those actions will in general affect the variables. It is

therefore a mistake to suppose that people’s expectations, or more generally their behavior, will remain

unchanged in the face of changes in government policies.

p

334

CASE STUDY EXTENSION

14–8 Did the NAIRU Decline in the 1990s?

As the economy expanded during the 1990s, the unemployment rate fell, dropping below 5 percent in

1997 and reaching a 30–year low of 3.9 percent in 2000. At the same time, inflation remained well

behaved and showed no sign of rising in response to tight labor markets. Many economists believed that

the natural rate of unemployment—or the NAIRU—was about 5 to 6 percent, and so the quiescence of

inflation seemed puzzling when unemployment remained well below this threshold for several years.1

335

Although favorable supply shocks contributed to the fortuitous combination of low unemployment

and low price inflation, the relationship between unemployment and wage inflation also appears to have

shifted during the 1990s. Accordingly, a more complete explanation requires understanding possible

changes in labor markets that may have lowered the NAIRU.3 Here a major factor often highlighted is the

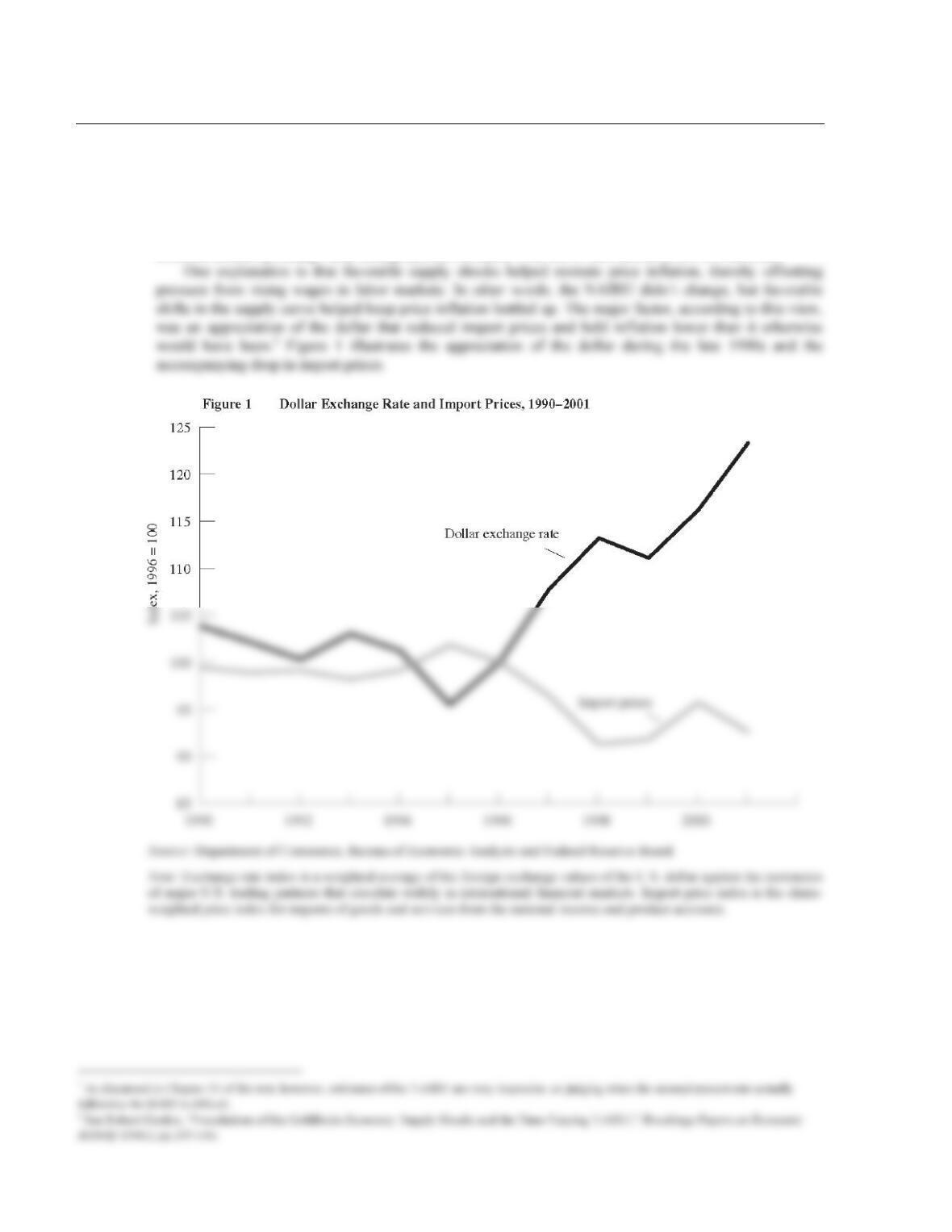

Source: Department of Labor, Bureau of Labor Statistics.

Note: Workers aged 16–24 as a share of labor force aged 16 and over.

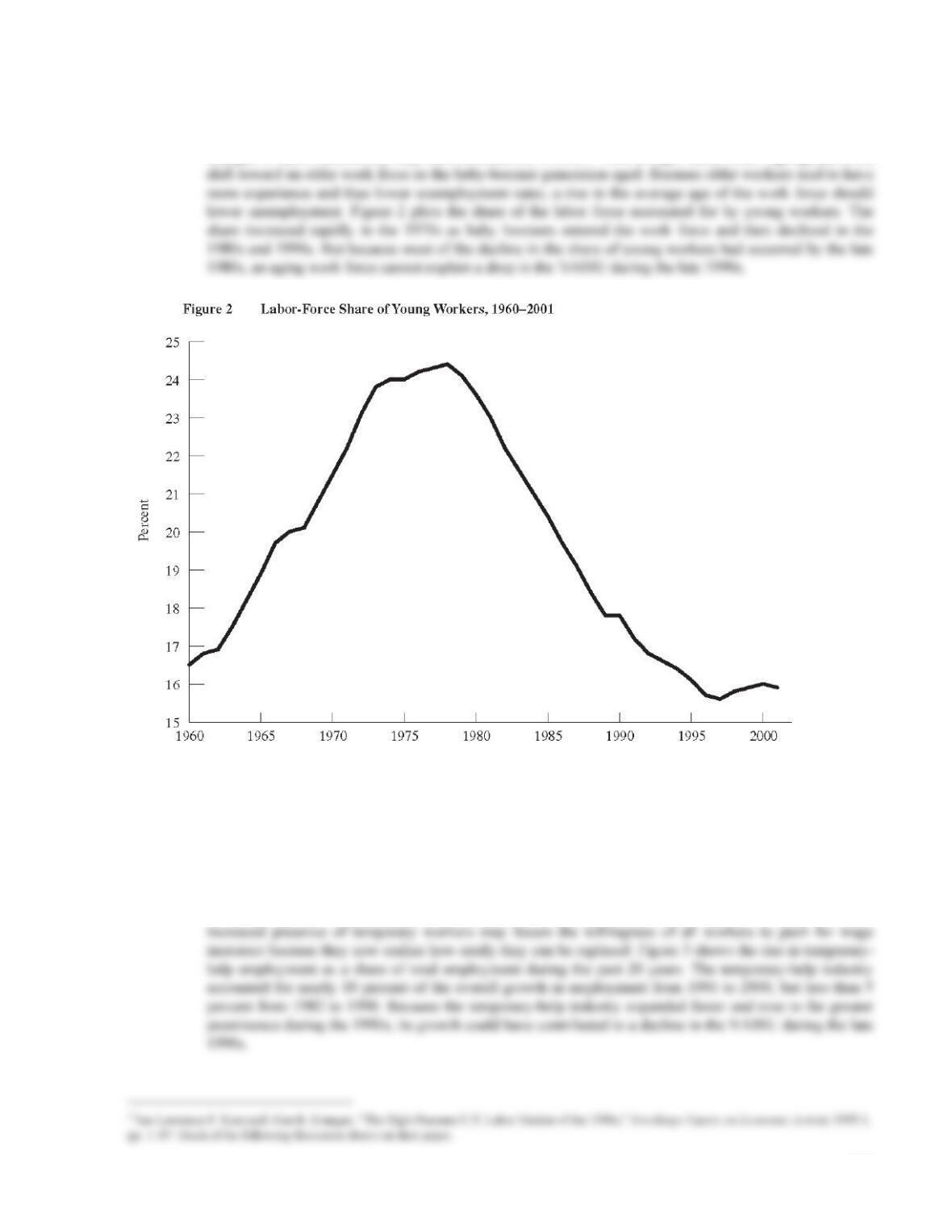

Another factor that could have contributed to a decline in the NAIRU is the recent rapid expansion of

the temporary–help industry. Businesses may be more willing to hire “temps” rather than permanent

employees because the costs associated with hiring permanent employees are greater than those for

temporary help. In particular, temporary–help agencies provide screening and other services, thereby

lowering the cost of hiring and possibly improving the efficiency of job matching. Such improved

efficiency in matching would lead to lower frictional unemployment (see Chapter 6). Furthermore, the

336

Source: Department of Labor, Bureau of Labor Statistics.

Note: Data are employment in the temporary help industry as a share of total nonfarm payroll employment.

Other less important factors that also may have contributed to a decline in the NAIRU include the

continuing erosion of the power of labor unions (see Chapter 7) and the enormous increase in the prison

population since the early 1980s. Because people in prison tend on average to have higher unemployment

CASE STUDY EXTENSION

14–9 Costs of Disinflation

To evaluate the desirability of tight monetary policies aimed at controlling inflation, we really need to

compare the costs of inflation with the costs of disinflation. Analysis of the welfare cost of inflation

suggests that the gain (in reduced “shoe–leather” costs) from reducing the inflation rate by 1 percentage

point is somewhere between $2 billion and $4 billion.1 The textbook suggests that the sacrifice ratio is

about 5, meaning that reducing inflation by 1 percentage point costs about 5 percent of one year’s GDP, or

about $750 billion.

Recession imposes a one–time cost, but the gains from permanently lower inflation persist year after

year. Even without any discounting of the future, however, these estimates suggest it would take literally

hundreds of years before the long–run gain from lower inflation outweighed the cost of the implied

CASE STUDY EXTENSION

14–10 The Unequal Costs of Disinflation

The sacrifice ratio illustrates the cost of reducing inflation in terms of output lost for the economy as a

whole. During the disinflation from 1982 to 1985, the sacrifice ratio is estimated to have been 3.3

percentage points of GDP lost for each percentage–point reduction in inflation. In terms of unemployment,

the cost was a cumulative total of 10 percentage points of cyclical unemployment (unemployment above

the economy–wide natural rate of 6.0). This cost was somewhat lower than might have been expected

given previous estimates of the sacrifice ratio. Even so, it still varied greatly across different demographic

groups of the labor force.

Table 1 Cyclical Unemployment Rate by Age and Race in the Disinflation of 1982–1985

White

Black

Male

Female

Male

Female

“Natural Rate” (1979 value)

4.5%

5.9%

11.4%

13.3%

1982

8.8

8.3

20.1

17.6

1983

8.8

7.9

20.3

18.6

1984

6.4

6.5

16.4

15.4

1985

6.1

6.4

15.3

14.9

Cumulative cyclical

10.1

5.5

26.5

13.3

ADDITIONAL CASE STUDY

14–11 “The Poincaré Miracle”

The estimates of the sacrifice ratio mentioned in the textbook evidently cannot always be right; otherwise

stopping hyperinflations would cost hundreds of years’ worth of GDP. Bringing a hyperinflation to an end,

as discussed in Chapter 5 of the textbook, involves policymakers’ taking strong measures to balance the

government’s budget and convince the public that policymakers will not again resort to printing money to

1925 and 1926, by about 23 percent.3 Prices were relatively stable for the first three months of 1926 but

grew more rapidly in the following months, rising by over 13 percent between June and July.4 France had

been running budget deficits both during and after World War I, partly in anticipation of paying its deficits

off using reparations from Germany. After Germany was provided with relief from reparations, France had

to either increase its tax revenues or effectively default on its debt by reducing its real value through

Indexation (Cambridge, Mass.: MIT Press, 1983). The following account is based on this article.

3 January–to–January changes in the wholesale price index, calculated from Table 4–1 in Sargent, “Stopping Moderate Inflations.”

4 Not surprisingly, this inflation was accompanied by depreciation of the French franc. See Chapter 6 of the text for the relationship between the

exchange rate and the inflation rate.

5 Sargent, “Stopping Moderate Inflations,” 62.

LECTURE SUPPLEMENT

14–12 Hysteresis and the Long–Run Phillips Curve

Economists used to believe that the Phillips curve reflected a long–run tradeoff between inflation and

unemployment. Policymakers could choose either high inflation and low unemployment or low inflation

and high unemployment. More sophisticated theories of the Phillips curve then incorporated inflation

ADDITIONAL CASE STUDY

14–13 Unemployment in the United Kingdom in the 1980s

Doubts about the natural–rate hypothesis and interest in hysteresis arose largely in response to the

experience in the 1980s of several European countries, especially the United Kingdom. In the 1970s, U.K.

unemployment averaged 3.4 percent, whereas in the 1980s it averaged 9.4 percent. This rise presented a

LECTURE SUPPLEMENT

14–14 Additional Readings

Chapter 14 of the textbook deals with many of the advances in macroeconomics of the last 30 years. Any

short list of readings must be very incomplete. A good place to start is with three of the “Schools Briefs”

published by The Economist: “Paradigm Lost” (November 3, 1990), “Tales of the Expected” (November