CHAPTER 14

New Keynesian Economics: Sticky Prices

CHAPTER KEY IDEAS

2. In the New Keynesian model, the price level is fixed, and firms will satisfy whatever

3. The central bank is modelled as setting an interest rate and then supplying the

appropriate quantity of money to support that interest rate target.

4. In the short run, the goods market and labour market do not clear. The demand for

5. Money is not neutral in the New Keynesian model. A decrease in the central bank’s

6. The New Keynesian model is not consistent with all the business cycle facts. Average

8. New Keynesian models do not fit the data as well as we might hope, and the

NEW IN THE FOURTH EDITION

1. New Section: “The Liquidity Trap and Sticky Prices”

3. All tables and charts have been updated to reflect new data.

4. End-of-chapter problems have been added.

Instructor’s Manual for Macroeconomics, Fourth Canadian Edition

TEACHING GOALS

It is straightforward to teach this material without making a large investment in doing

IS/LM AD/AS analysis. The model is just a simple extension of the monetary

intertemporal model, with a fixed price and an interest rate rule for monetary policy. It is

important for the students to recognize that the central bank’s interest rate target needs to

be supported with the appropriate supply of money (which may vary, if there are money

demand shocks). Emphasize the concepts “output gap” and “natural rate of interest,”

particularly as these enter policy discussions.

This model should be subjected to the same rigour as the equilibrium models in

Chapter 11. Does it fit the data? Does it make sense? Keynesian thinking is quite

Students should learn how policy works in the New Keynesian model. Policy works

because of a market failure—the inability of private markets to clear in the short run. If

policymakers are smart, quick, and have good information, they can do better—maybe a

lot to ask. There are important differences between fiscal and monetary policy as

stabilization tools, particularly in terms of what they imply for the allocation of resources.

CLASSROOM DISCUSSION TOPICS

You might start the discussion by getting students to think about why prices might be

sticky in practice. What do we observe about market prices? Which prices seem to be

sticky and which are not? Goods are sold in different ways, for example for some goods

prices are posted and we cannot bargain, but for other goods we are expected to haggle.

Why might prices be sticky? Are there costs to changing prices? What would these costs

be? Why do gasoline prices change frequently while the prices of motor oil (sold at the

same gas station) do not? What about sales?

Students are indoctrinated with Keynesian economics at an early stage, and this is

reinforced by how much of the media thinks about the economy. We typically blame

Chapter 14: New Keynesian Economics

An important avenue for discussion would be to consider the financial crisis and the

responses of fiscal and monetary policy to it. The crisis appears to have had little to do

with sticky prices, but nevertheless policymakers use Keynesian beliefs to justify their

actions. Was the 2008–09 downturn the result of downward stickiness in prices? Were

firms going out of business because they could not bear to reduce the prices of their

products?

OUTLINE

1. The New Keynesian Model

a) Menu Costs

2. The Non-Neutrality of Money in the New Keynesian Model

a) Output, Employment Increase with a Fall in Target Interest Rate

3. Government Policy

a) Stabilization Policy

b) Fiscal Policy

c) Monetary Policy

d) Macroeconomics in Action 12.1: 1981/82 Recession

e) Macroeconomics in Action 12.2: Policy Lags

4. Total Factor Productivity Shocks in the New Keynesian Model

5. Criticisms

a) Theory Weak

b) Model Does Not Fit the Data Well

c) Prices Change Frequently in Practice—Every Four Months on Average

d) Macroeconomics in Action 12.3: How Sticky Are Nominal Prices?

TEXTBOOK QUESTION SOLUTIONS

Problems

1. An increase in G shifts the output demand curve to the right. With a fixed interest rate

target, output increases, investment stays constant, consumption increases,

2. a) This acts to shift the output demand curve to the left (just the reverse of what

happens in question 1. Output decreases, investment falls, consumption falls,

employment falls, and the real wage falls. The output gap rises.

b) The central bank can lower its interest rate target, supported by decreasing the

3. Given some level of government spending, G1, this determines the positions of the

output demand and supply curves, and determines the equilibrium level of output Y1,

and the equilibrium real interest rate r1. The central bank would like to keep the price

4. Under the assumption that Ricardian equivalence holds, so that the timing of taxes is

irrelevant, the deficit does not matter. What matters in the basic New Keynesian

model is the level of government spending. If fiscal policy is the only stabilization

5. a) There should be no change in the target rate. The money supply changes with the

shift in money demand, with the target rate unchanged. The output gap therefore

is unaffected by the money demand shift.

b) This shifts the demand for investment goods, and shifts the output demand curve

6. Under this monetary policy, whenever TFP increases, the central bank increases its

target interest rate to accommodate it. All aggregate variables move just as they

7. a) No problem. The shift in money demand is accommodated by a movement in the

money supply in the same direction. The output gap stays at zero.

b) Output demand shifts to the right, but the central bank holds its interest rate target

8. Recall from Chapter 13 that liquid financial assets can be expressed as

()

B

akr

P

=+ ,

with the key difference here being that P is fixed in the New Keynesian sticky price

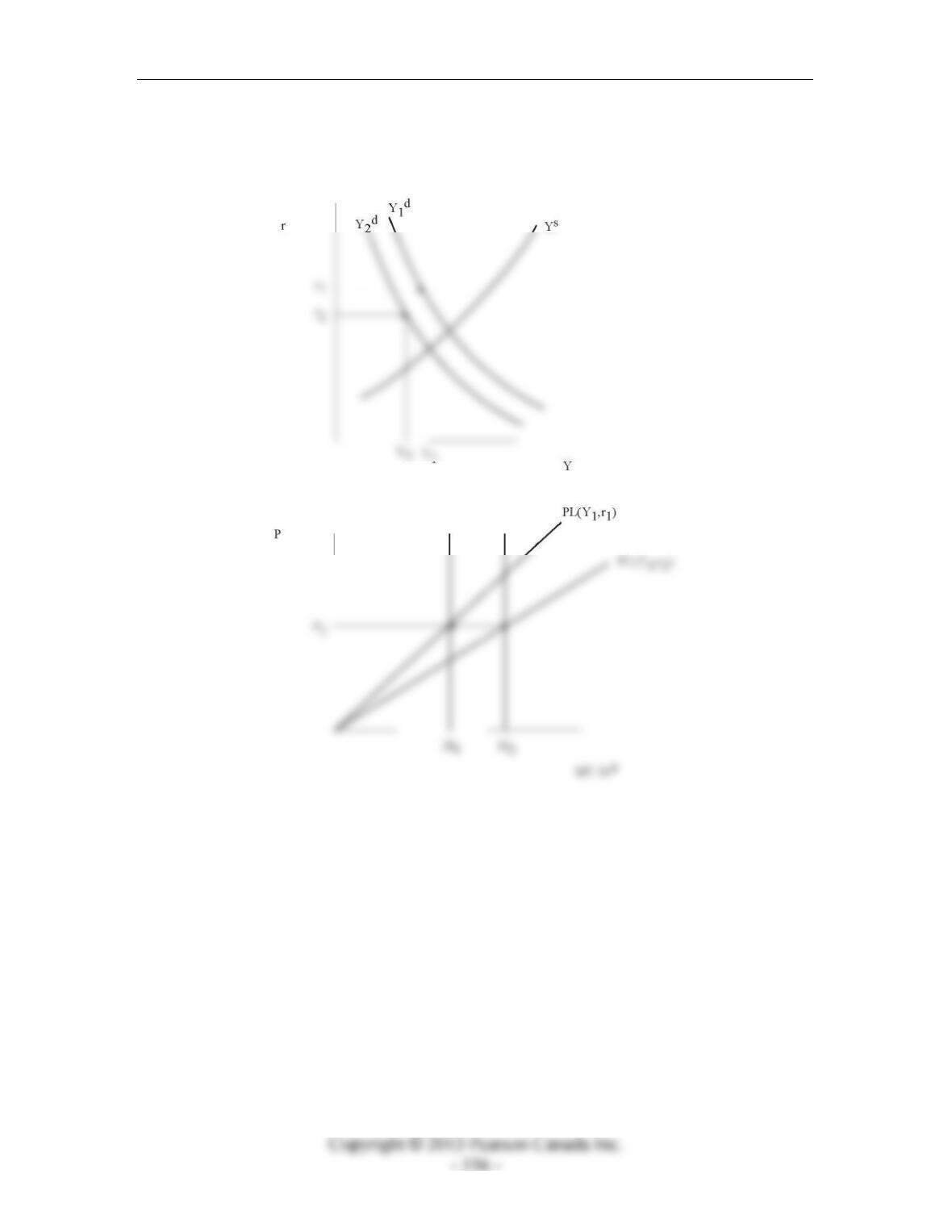

14.1, output can actually decline under what would conventionally think is

accommodative monetary policy. In Figure 14.1, the output gap increases, and the

deficiency in financial liquidity is aggravated. However, in Figure 14.2, we depict the

case where output increases, so that the the output gap falls, but this case could

Instructor’s Manual for Macroeconomics, Fourth Canadian Edition

correct both inefficiencies (the output gap and the deficiency in financial liquidity), as

the central bank essentially only has one policy instrument.

Figure 14.1

Chapter 14: New Keynesian Economics

Figure 14.2

9. If consumption and investment expenditures are very inelastic with respect to the real

interest rate. This implies that the output demand curve is steeper, which implies that

output will increase a smaller amount in response to a decrease in the real interest