Chapter 14: Capital Structure and Leverage

Learning Objectives

371

Chapter 14

Capital Structure and Leverage

Learning Objectives

After reading this chapter, students should be able to:

◆ Explain why there may be differences in a firm’s capital structure when measured on a book-value

basis, a market-value basis, or a target basis.

372

Lecture Suggestions

Chapter 14: Capital Structure and Leverage

Lecture Suggestions

This chapter is rather long, but it is also modular, hence sections can be omitted without loss of

continuity. Therefore, if you are experiencing a time crunch, you could skip selected sections.

What we cover, and the way we cover it, can be seen by scanning the slides and Integrated Case

DAYS ON CHAPTER: 3 OF 56 DAYS (50-minute periods)

Chapter 14: Capital Structure and Leverage

Answers and Solutions

373

Answers to End-of-Chapter Questions

14-1 Operating leverage is the extent to which fixed costs are used in a firm’s operations. If operating

14-4 An increase in the personal tax rate makes both stocks and bonds less attractive to investors

because it raises the tax paid on dividend and interest income. Changes in personal tax rates will

b. An increase in the personal tax rate would cause investors to shift from bonds to stocks due

374

Answers and Solutions

Chapter 14: Capital Structure and Leverage

14-6 Biotechnology companies use relatively little debt because their industries tend to be cyclical,

14-7 EBIT depends on sales and operating costs that generally are not affected by the firm’s use of

14-8 Expected EPS is generally measured as EPS for the coming years, and we typically do not reflect

in this calculation any bankruptcy-related costs. Also, EPS does not reflect (in a major way) the

14-9 The tax benefits from debt increase linearly, which causes a continuous increase in the firm’s

14–10 With increased competition after the breakup of AT&T, the new AT&T and the seven Bell

operating companies’ business risk increased. With this component of total company risk

14–11 The firm may want to assess the asset investment and financing decisions jointly. For instance,

Chapter 14: Capital Structure and Leverage

Answers and Solutions

375

Solutions to End-of–Chapter Problems

14-2 The optimal capital structure is that capital structure where WACC is minimized and stock price is

14-3 a. Expected EPS for Firm C:

b. According to the standard deviations of EPS, Firm B is the least risky, while C is the riskiest.

14–4 From the Hamada equation, b = bU[1 + (1 – T)(D/E)], we can calculate bU as bU = b/[1 + (1 – T)(D/E)].

376

Answers and Solutions

Chapter 14: Capital Structure and Leverage

)TEBIT(1−

b. LL: Debt/Capital = 30%.

EBIT $4,000,000

c. LL: Debt/Capital = 60%.

EBIT $4,000,000

Chapter 14: Capital Structure and Leverage

Answers and Solutions

377

b. QBE =

V P

F

−

=

$10

$140,000

= 14,000 units.

c. If the selling price rises to $31, while the variable cost per unit remains fixed, P – V rises to

$16. The end result is that the break-even point is lowered.

V P

F

−

$16

$140,000

d. If the selling price rises to $31 and the variable cost per unit rises to $23, P – V falls to $8.

The end result is that the break-even point increases.

$140,000

Dollars

800,000

378

Answers and Solutions

Chapter 14: Capital Structure and Leverage

The break-even point increases to 17,500 units because the contribution margin per each

unit sold has decreased.

14-7 No leverage: Debt = 0; Equity = $14,000,000.

State

Ps

EBIT

(EBIT – rdD)(1 – T)

ROES

PS(ROE)

PS(ROES – RÔE)2

1

0.2

$4,200,000

$2,520,000

0.18

0.036

0.00113

2

0.5

2,800,000

1,680,000

0.12

0.060

0.00011

3

0.3

700,000

420,000

0.03

0.009

0.00169

RÔE =

0.105

0.00293

RÔE = 10.5%.

State

Ps

EBIT

(EBIT – rdD)(1 – T)

ROES

PS(ROE)

PS(ROES – RÔE)2

1

0.2

$4,200,000

$2,444,400

0.039

0.00138

3

0.3

700,000

344,400

0.008

0.00212

RÔE =

Sales

Dollars

800,000

Chapter 14: Capital Structure and Leverage

Answers and Solutions

379

Debt/Capital = 50%: Debt = $7,000,000; Equity = $7,000,000; rd = 11%.

State

Ps

EBIT

(EBIT – rdD)(1 – T)

ROES

PS(ROE)

PS(ROES – RÔE)2

State

Ps

EBIT

(EBIT – rdD)(1 – T)

ROES

PS(ROE)

PS(ROES – RÔE)2

Step 1: Determine the firm’s current beta.

380

Answers and Solutions

Chapter 14: Capital Structure and Leverage

Step 3: Determine the firm’s beta under the new capital structure.

14-9 a. Dividends = 0.4 × $1,000,000 = $400,000. So, the current dividend per share, D0, =

b. Step 1: Calculate EBIT before the recapitalization:

14–10 a. Firm A

1. Fixed costs = $80,000.

Chapter 14: Capital Structure and Leverage

Answers and Solutions

381

Firm B

1. Fixed costs = $120,000.

Check:

14–11 a. Using the standard formula for the weighted average cost of capital, we find:

382

Answers and Solutions

Chapter 14: Capital Structure and Leverage

c. To “unlever” the firm’s beta, the Hamada equation is used.

bL = bU[1 + (1 – T)(D/E)]

d. To determine the firm’s new cost of common equity, one must find the firm’s new beta under

its new capital structure. Consequently, you must “relever” the firm’s beta using the Hamada

e. Again, the standard formula for the weighted average cost of capital is used. Remember, the

14–12 a. Without new investment:

Chapter 14: Capital Structure and Leverage

Answers and Solutions

383

1. EPSOld = $489,600/240,000 = $2.04.

With new investment:

Debt Stock

Sales $12,960,000 $12,960,000

b. EPS =

N

T) I)(1 F VC (Sales −−−−

Therefore,

)(0.6)$2,184,000 Q($10.667 −

)(0.6)$2,904,000 Q(10.667 −

0.6)$384,000)( $1,560,000 Q$22.667 Q($28.8 −−−

384

Answers and Solutions

Chapter 14: Capital Structure and Leverage

d. At the expected sales level, 450,000 units, we have these EPS values:

Chapter 14: Capital Structure and Leverage

Answers and Solutions

385

14–13 Use of debt (millions of dollars):

Probability 0.3 0.4 0.3

Sales $2,250.00 $2,700.00 $3,150.00

Use of stock (millions of dollars):

Probability 0.3 0.4 0.3

Sales $2,250.00 $2,700.00 $3,150.00

386

Answers and Solutions

Chapter 14: Capital Structure and Leverage

Chapter 14: Capital Structure and Leverage

Comprehensive/Spreadsheet Problem

387

Comprehensive/Spreadsheet Problem

Note to Instructors:

The solution to this problem is not provided to students at the back of their text. Instructors

can access the

Excel

file on the textbook’s website.

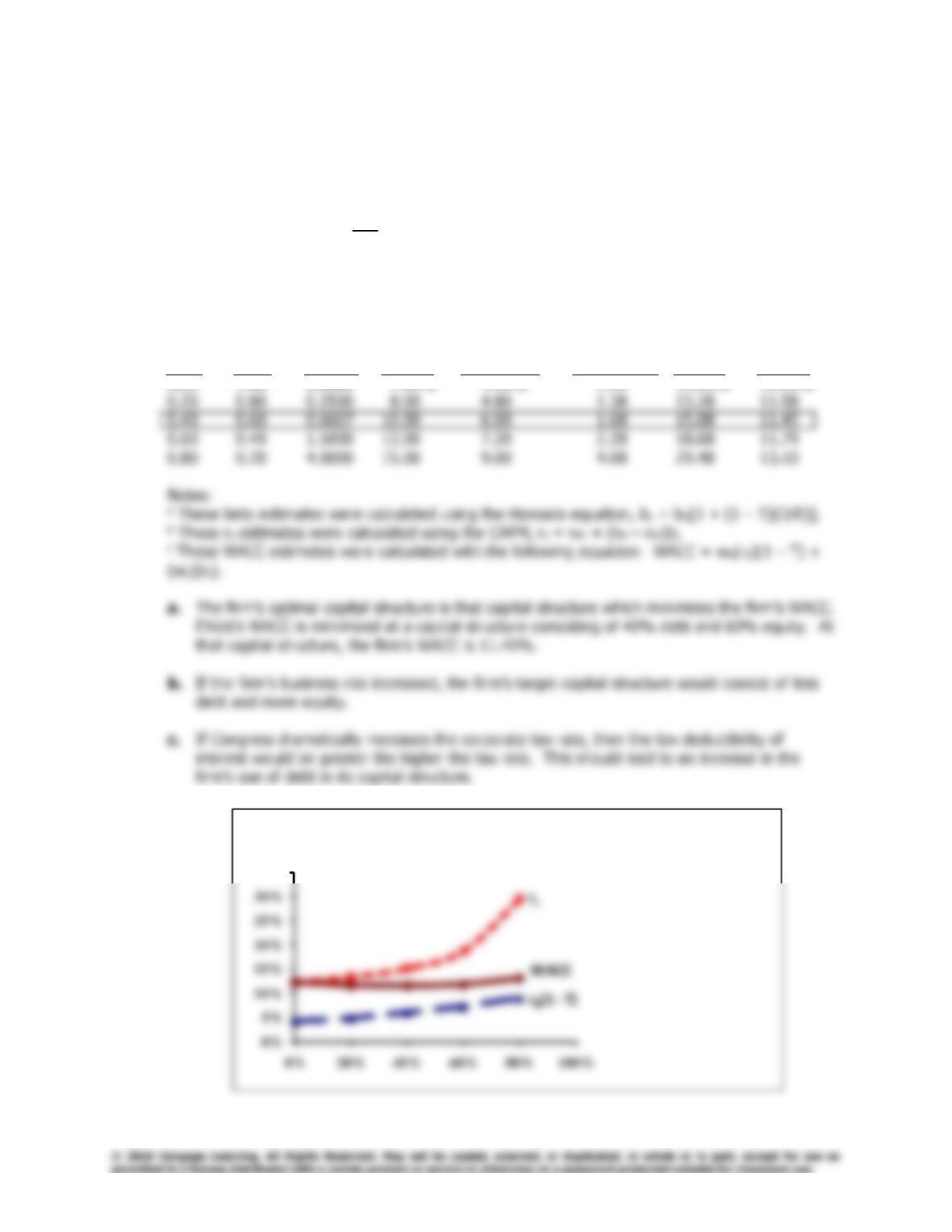

14–14 Tax rate = 40%; rRF = 5.0%; bU = 1.2; rM – rRF = 6.0%

From data given in the problem and table we can develop the following table:

Levered

wd wc D/E rd rd(1 – T) betaa rsb WACCc

d.

35%

Capital Costs Vs. D/(D+E)

388

Comprehensive/Spreadsheet Problem

Chapter 14: Capital Structure and Leverage

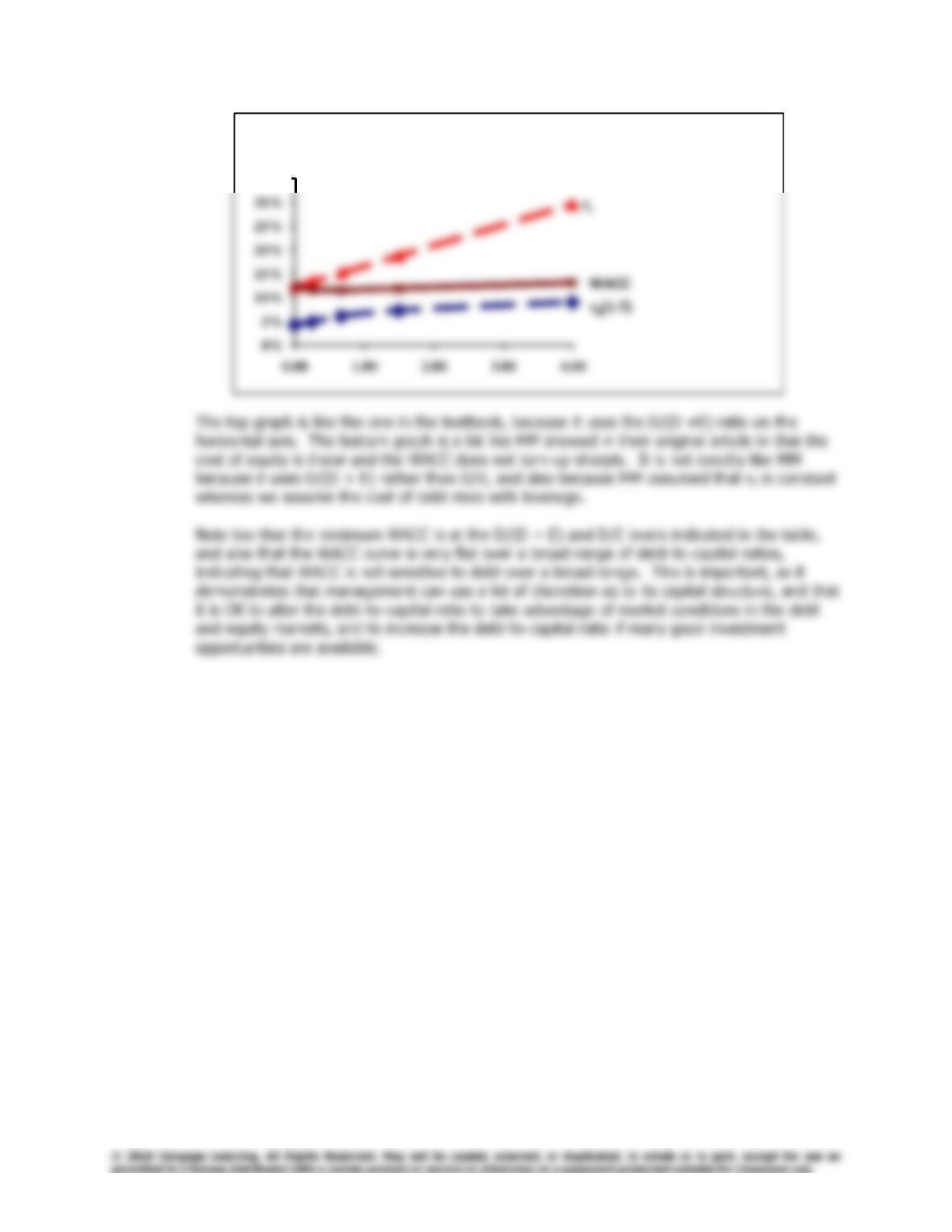

35%

Capital Costs Vs. D/E