Game Theory and Competitive Strategy 451

prohibition, potential conspirators face practical problems in any overt or tacit attempt

at collusion. To illustrate the problems encountered, consider the following profit

payoff matrix faced by two potential conspirators in a one-shot, simultaneous-move

game. The first number in each cell is firm A’s profit payoff; the second number is the

profit payoff to firm B.

Firm B

Pricing

Strategy

Low Price

(“Left”)

High Price

(“Right”)

A. Is there a dominant strategy and a Nash equilibrium strategy for each firm? If so,

what are they?

B. If the firms agreed to collude and charge high prices, both would earn $25 million

and joint profits of $50 million would be maximized. However, the joint high-

price strategy is not a stable equilibrium. Explain.

P14.6 SOLUTION

A. In this problem, the low-price strategy is a dominant strategy for both firms. If firm B

charged low prices, firm A will also choose to charge low prices because the $5 million

452 Chapter 14

B. If the firms agreed to collude and charge high prices, both would earn $25 million and

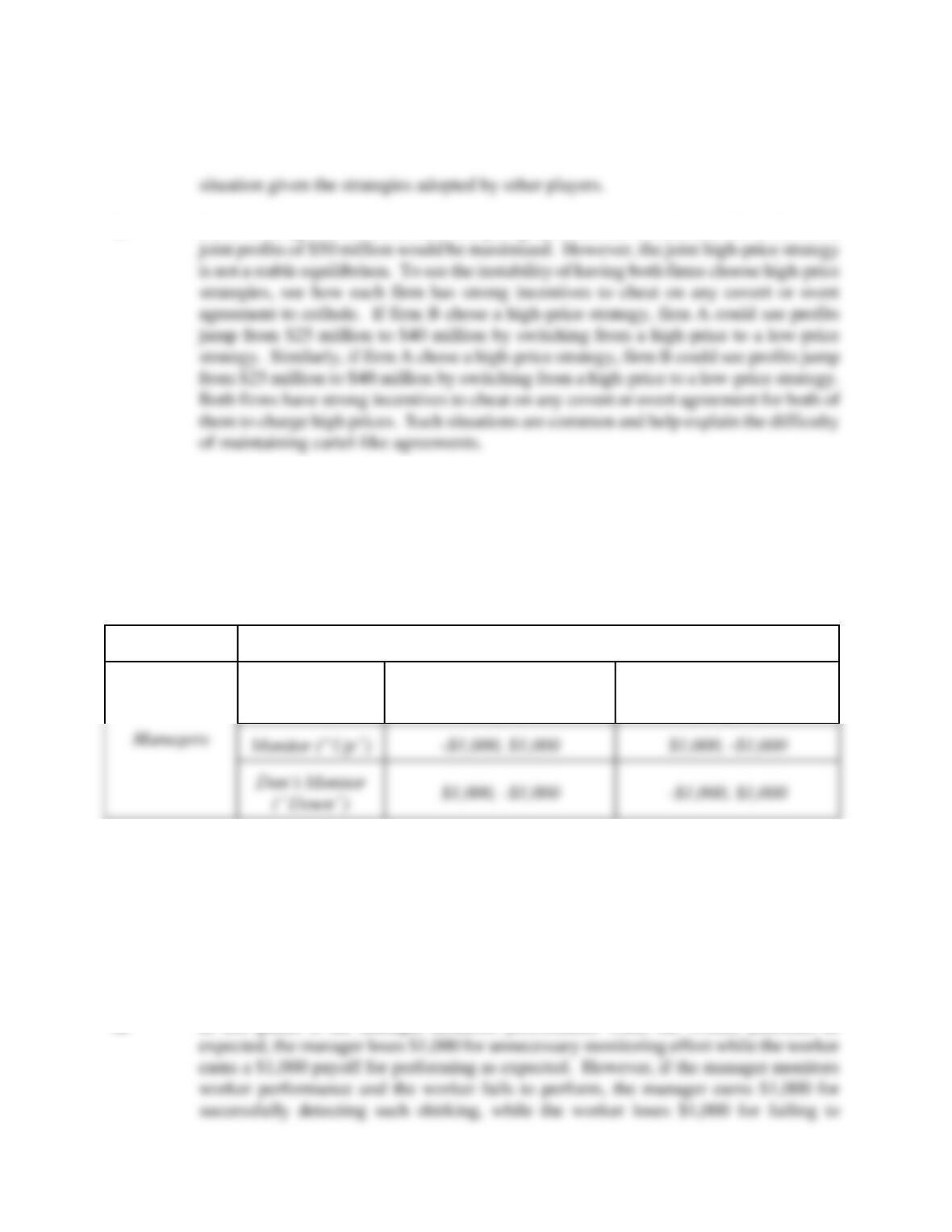

P14.7 Randomized Strategies. Game theory can be used to analyze conflicts that arise

between managers and workers. Managers can choose to monitor worker performance,

or not monitor worker performance. For their part, workers can choose to perform the

requested task within the time frame requested, or fail to perform as requested. The

resulting payoff matrix for this one-shot, simultaneous move game shows the payoff to

managers (first number) and workers (second number).

Workers

Work

Strategy

Perform

(Left”)

Fail to Perform

(“Right”)

A. Document the fact that there is no Nash equilibrium strategy for each player.

B. Explain how each player will have a preference for secrecy in the absence of a

Nash equilibrium and how randomized strategies might be favored in such

circumstances.

P14.7 SOLUTION

A. In this game, if the manager monitors performance while the worker performs as

Game Theory and Competitive Strategy 453

B. In the absence of Nash equilibrium, each player will have a preference for secrecy to

mask moves and preferences. In the absence of a Nash equilibrium, workers might

P14.8 Predatory Pricing. Prohibitions against predatory pricing stem from big business

conspiracy theories popularized in the late nineteenth century by journalists such as Ida

Tarbell, author of an influential book titled History of the Standard Oil Company. In

that book, Tarbell condemned Standard Oil’s allegedly predatory price cutting.

Business historians assert that Tarbell vilified John D. Rockefeller because of personal

reasons, and not only because of an interest in reshaping public policy. Standard Oil’s

low prices had driven the employer of Tarbell’s brother, the Pure Oil Company, out of

the petroleum-refining business.

According to predatory pricing theory, the predatory firm sets price below

marginal cost, the relevant cost of production. Competitors must then lower their price

below marginal cost, thereby losing money on each unit sold. If competitors failed to

match the predatory firm’s price cuts, they would continue to lose market share until

they were driven out of business. If competitors follow the lead of the predatory pricing

firm and cut price below marginal cost, they will incur devastating losses, and

eventually go bankrupt. Either way, the “deep pockets” of the predatory firm give it the

financial muscle and staying power necessary to drive smaller, weaker competitors out

of business. After competition has been eliminated from the market, the predatory firm

raises prices to compensate for money lost during its price war against smaller

competitors, and earns monopoly profits forever thereafter.

A. The ban against predatory pricing is one of the most controversial U. S. antitrust

454 Chapter 14

policies. Explain why this ban is risky from a public policy perspective, and why

predatory pricing strategy can be criticized as irrational from a game theory

perspective.

B. Explain why the prohibition against predatory pricing might be politically popular

even if predatory pricing is implausible from an economic perspective.

P14.8 SOLUTION

A. The antitrust ban on predatory pricing is risky from a public policy perspective because,

like any limit on price competition, a ban on predatory pricing can retard beneficial price

competition among firms. The theory of predatory pricing has long held appeal for

From a game theory perspective, predatory pricing strategy seems irrational

because it is based upon output and pricing assumptions that are not credible. For

B. Predatory pricing theory gets virtually no respect from economists, but is still a popular

legal and political theory for several reasons. Huge sums of money are involved in

predatory pricing litigation and that fact guarantees that the antitrust bar will be fond of

Game Theory and Competitive Strategy 455

P14.9 Non-price Competition. General Cereals, Inc. (GCI), produces and markets Sweeties!,

a popular ready-to-eat breakfast cereal. In an effort to expand sales in the Secaucus,

New Jersey, market, the company is considering a one-month promotion whereby GCI

would distribute a coupon for a free daily pass to a local amusement park in exchange

for three box tops, as sent in by retail customers. A 25% boost in demand is anticipated,

even though only 15% of all eligible customers are expected to redeem their coupons.

Each redeemed coupon costs GCI $6, so the expected cost of this promotion is 30¢ (=

0.15 × $6 ÷ 3) per unit sold. Other marginal costs for cereal production and

distribution are constant at $1 per unit.

Current demand and marginal revenue relations for Sweeties! are

A. Calculate the profit-maximizing price/output and profit levels for Sweeties! prior

to the coupon promotion.

B. Calculate these same values subsequent to the Sweeties! coupon promotion and

following the expected 25% boost in demand.

P14.9 SOLUTION

A. The profit-maximizing price/output combination is found by setting MR = MC and

solving for Q:

B. The profit-maximizing price/output combination is found by setting the new relevant

and, because:

Game Theory and Competitive Strategy 457

P14.10 Variability of Business Profits. Near the checkout stand, grocery stores and

convenience stores prominently display low-price impulse items like candy, gum and

soda that customers crave. Despite low prices, such products generate enviable profit

margins for retailers and for the companies that produce them. For example, Hershey

Foods Corp. is the largest U.S. producer of chocolate and nonchocolate confectionary

(sugared) products. Major brands include Hershey’s, Reese’s, Kit Kat, Almond Joy, and

Milk Duds. While Hershey’s faces increasing competition from other candy companies

and snack-food producers of energy bars, the company is extremely profitable.

Hershey’s rate of return on stockholder’s equity, or net income divided by book value

per share, routinely exceeds 30% per year, or about three times the publicly-traded

company average. Profit margins, or net income per dollar of sales revenue, generally

exceed 13%, and earnings grow in a predictable fashion by more than 10 percent per

year.

A. Explain how the failure to reflect intangible assets, like the value of brand names,

might cause Hershey’s accounting profits to overstate Hershey’s economic profits.

B. Explain why high economic profit rates are a necessary but not sufficient

condition for the presence of monopoly profits.

P14.10 SOLUTION

A. Business profit is often measured in dollar terms or as a percentage of sales revenue,

called profit margin. The economist’s concept of a normal rate of profit is typically

458 Chapter 14

B. In economic terms, monopoly profits are the unwarranted payoff received by firms for

the raw exercise of pricing power. Implicit in the concept of monopoly profits is the

business, the economic value of brand name advertising is not reflected in accounting

value of the firm. In an economic sense, advertisers like Hershey’s have a right to

expect to earn a fair return on risky intangible assets derived from advertising and

product promotion. Accounting rates of return for advertising-intensive firms should be

higher than average to compensate brand name leaders for high-risk promotional

Game Theory and Competitive Strategy 459

CASE STUDY FOR CHAPTER 14

Time Warner, Inc., Is Playing Games with Stockholders

Time Warner, Inc., the world’s largest media and entertainment company, is best known as the

publisher of magazines such as Fortune, Time, People, and Sports Illustrated. The Company is a

media powerhouse comprised of Internet technologies and electronic commerce (America Online),

cable television systems, filmed entertainment and television production, cable and broadcast

television, recorded music and music publishing, magazine publishing, book publishing and direct

marketing. Time Warner has the potential to profit whether people go to theaters, buy or rent

videos, watch cable or broadcast TV, or listen to records.

Time Warner is also famous for introducing common stockholders to the practical use of

game theory concepts. In 1991, the company introduced a controversial plan to raise new equity

capital through use of a complex “contingent” rights offering. After months of assuring Wall Street

that it was close to raising new equity from other firms through strategic alliances, Time Warner

instead asked its shareholders to ante up more cash. Under the plan, the company granted holders

of its 57.8 million shares of common stock the rights to 34.5 million shares of new common, or 0.6

rights per share. Each right enabled a shareholder to pay Time Warner $105 for an unspecified

number of new common shares. Because the number of new shares that might be purchased for

$105 was unspecified, so too was the price per share. Time Warner’s Wall Street advisers

structured the offer so that the new stock would be offered at cheaper prices if fewer shareholders

chose to exercise their rights.

In an unusual arrangement, the rights from all participating shareholders were to be

460 Chapter 14

exercise their rights.

The terms of the offer were designed to make Time Warner shareholders feel compelled

ground in terms of Wall Street experience. Disgruntled shareholders noted that a similar contingent

rights offering by Bass PLC of Britain involved a fee of only 2.125% of the proceeds to the company,

despite the fact that the lead underwriter Schroders PLC agreed to buy and resell any new stock that

wasn’t claimed by rights holders. This led to charges that Time Warner’s advisers were charging

underwriters’ fees without risking any of their own capital.

Proceeds from the offering were earmarked to help pay down the $11.3 billion debt Time

Inc. took on to buy Warner Communications Inc. Time Warner maintained that it was in intensive

Stockholder reaction to the Time Warner offering was immediate and overwhelmingly

negative. On the day the offering was announced, Time Warner shares closed at $99.50, down

$11.25, in New York Stock Exchange composite trading. This is in addition to a decline of $6

suffered the previous day on the basis of a report in The Wall Street Journal that some form of equity

offering was being considered. After trading above $120 per share in the days prior to the first

reports of a pending offer, Time Warner shares plummeted by more than 25% to $88 per share

within a matter of days. This is yet one more disappointment for the company’s long-suffering

A. Was Paramount’s above-market offer for Time, Inc. consistent with the notion that the

prevailing market price for common stock is an accurate reflection of the discounted net

Game Theory and Competitive Strategy 461

present value of future cash flows? Was management’s rejection of Paramount’s above–

market offer for Time, Inc. consistent with the value-maximization concept?

B. Assume that a Time Warner shareholder could buy additional shares at a market price

of $90 or participate in the company’s rights offering. Construct the payoff matrix that

correspond to a $90 per share purchase decision versus a decision to participate in the

rights offering with subsequent 100%, 80%, and 60% participation by all Time Warner

shareholders.

CASE STUDY SOLUTION

A. These are, of course, controversial questions designed to spur debate on the issues of

capital market efficiency and the convergence or divergence between shareholder and

managerial interests. Paramount’s 1989 above-market offer for Time, Inc. is consistent

with the notion that the prevailing market price for common stock is an accurate

B. The payoff matrix that corresponds to a $90 per share purchase decision versus a

462 Chapter 14

Decision

States of Nature

60% Participation

80% Participation

100% Participation

C. A secure strategy, sometimes called the maximin strategy, guarantees the best possible

outcome given the worst possible scenario. In this case, the worst possible scenario for

D. The price of Time Warner common stock fell subsequent to the announcement of the

adversarial rather than cooperative relationship between management and stockholders.

Interestingly, in light of the furor caused by its contingent rights offering, Time

Warner decided to withdraw the offer a few weeks after it had been announced. In its

place, the company decided to offer current shareholders the right to purchase up to