1

2

3

4

5

6

7

8

9

15

16

17

18

19

20

21

25

26

27

28

29

30

31

38

39

42

43

44

A B C D E F G H I

13 Case model

PART A

EBIT $400,000

PART C

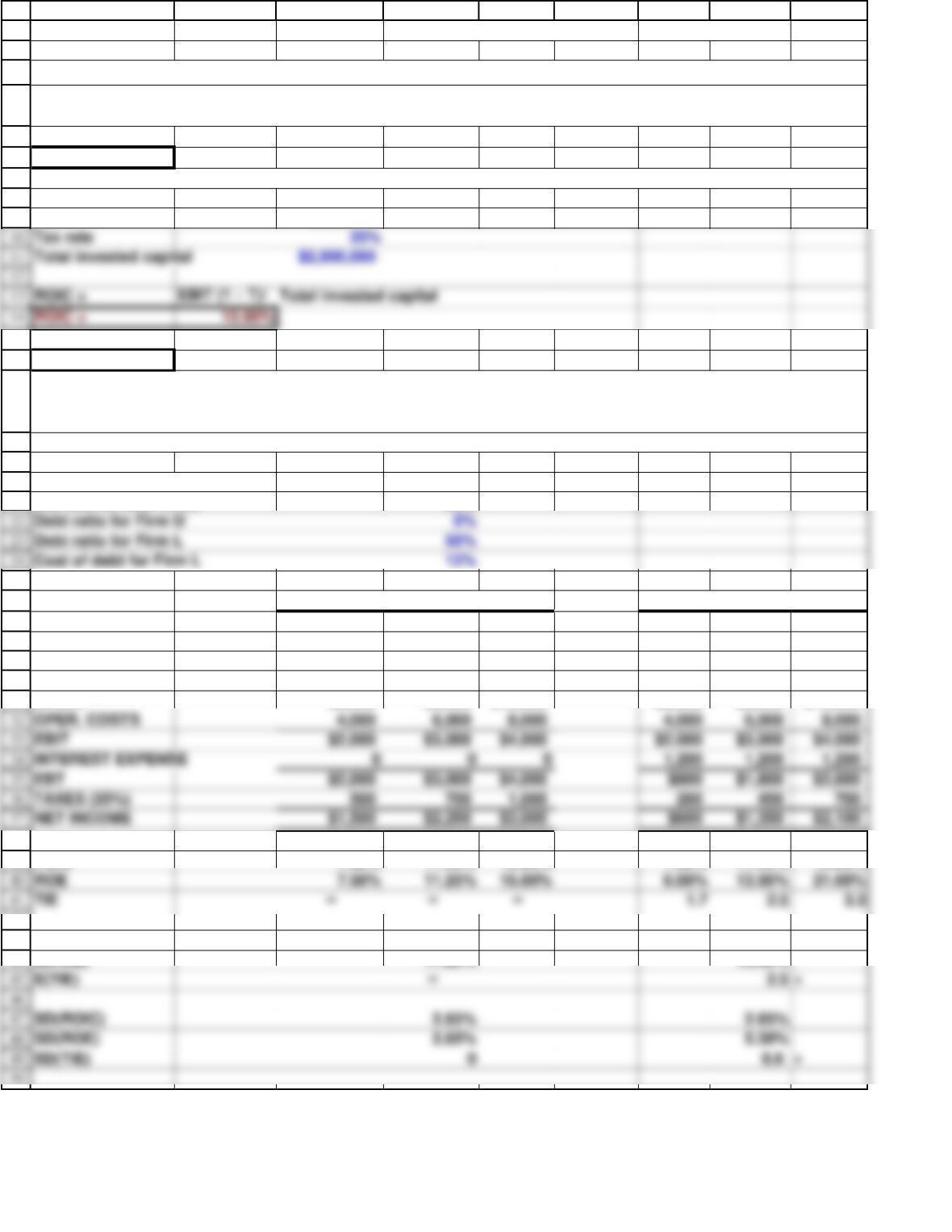

Total capital for both firms $20,000

Tax rate for both firms 25%

TOTAL CAPITAL $20,000 $20,000 $20,000 $20,000 $20,000 $20,000

EQUITY $20,000 $20,000 $20,000 $10,000 $10,000 $10,000

PROBABILITY 0.25 0.50 0.25 0.25 0.50 0.25

SALES $6,000 $9,000 $12,000 $6,000 $9,000 $12,000

ROIC 7.50% 11.25% 15.00% 7.50% 11.25% 15.00%

E(ROIC) 11.25% 11.25%

E(ROE) 11.25% 13.50%

Chapter 13. Capital Structure and Leverage

Consider two small hypothetical firms, Firm U, with zero debt financing, and Firm L, with $10,000 of 12% debt.

Both firms have $20,000 in invested capital and a 25% federal-plus-state tax rate.

9/12/2022 17:20

FIRM U

12/9/2018

(3) What is the firm’s return on invested capital (ROIC)?

FIRM L

This spreadsheet model is designed to be used in conjunction with the chapter’s integrated case and the related

PowerPoint slide presentation.

(1) Complete the partial income statements and the firms’ ratios.

51

52

53

54

55

56

57

61

62

63

64

65

66

76

77

78

79

80

81

82

85

86

87

88

89

92

93

94

95

96

A B C D E F G H I

PART D

The cost of debt at different debt levels :

Amount D / Capital D / E Bond

Borrowed Ratio Ratio Rating

rd

$0 0.0000 0.0000 — —

$250,000 0.1250 0.1429 AA 8.0%

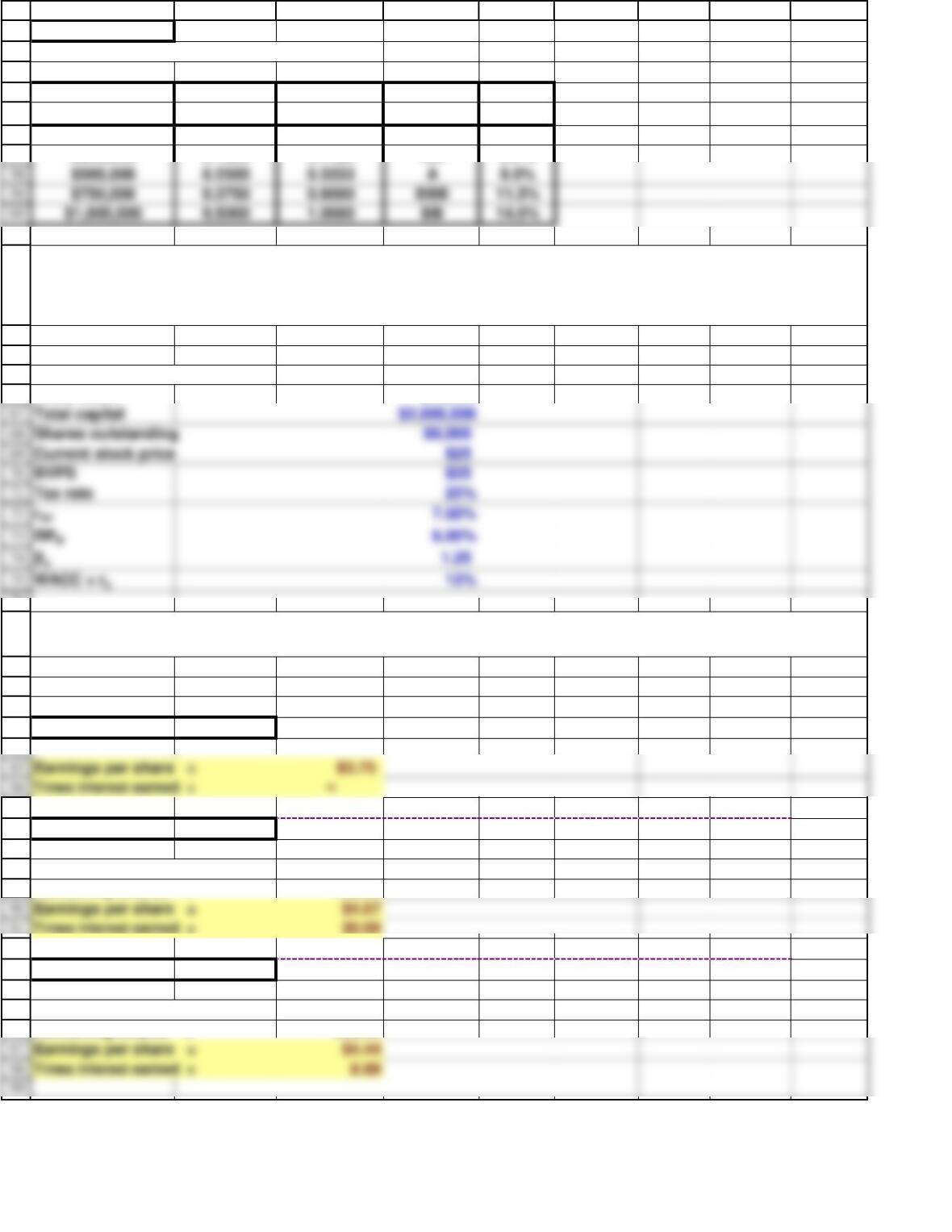

Sales (last year) $1,100,000

Variable costs as a % of sales 60%

Fixed costs $40,000

EBIT $400,000

At D = $0

At D = $250,000

Shares repurchased = 10,000

Remaining shares = 70,000

At D = $500,000

Shares repurchased = 20,000

Remaining shares = 60,000

(3) Assume that shares could be repurchased at the current market price of $25 per share. Calculate CD’s

expected EPS and TIE at debt levels of $0, $250,000, $500,000, $750,000, and $1,000,000. How many shares

would remain after recapitalization under each scenario?

The analysis for each debt level being considered (in thousands of dollars and shares) is shown below:

100

101

102

108

109

110

113

114

115

116

117

118

119

120

121

122

123

124

129

130

131

132

133

134

135

139

140

141

142

143

144

A B C D E F G H I

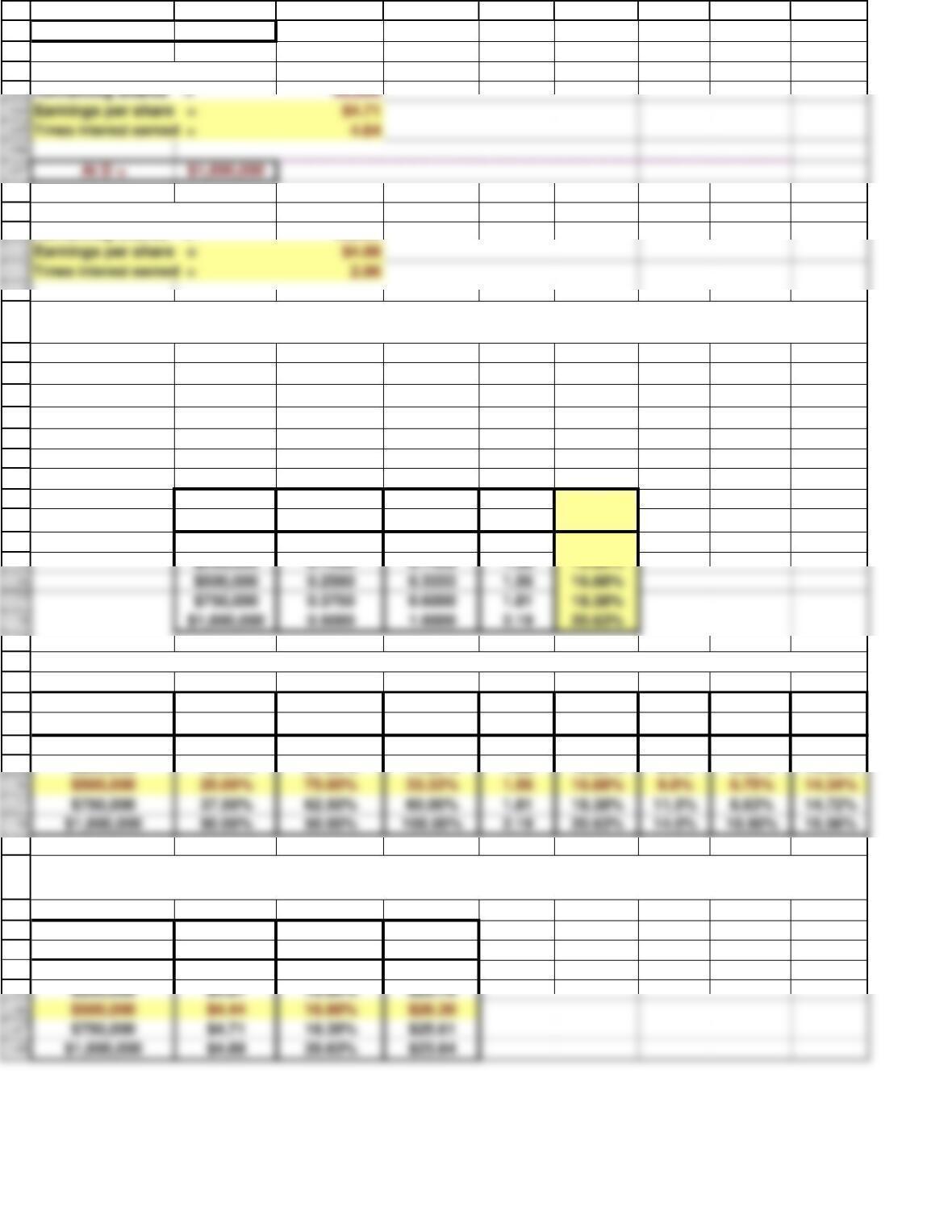

At D = $750,000

Shares repurchased = 30,000

Shares repurchased = 40,000

Remaining shares = 40,000

rRF 7.5%

RPM6.0%

βu1.25

Total capital $2,000,000

Tax rate 25%

Amount D / Capital D / E Levered

Borrowed Ratio Ratio Beta

rs

$0 0.0000 0.0000 1.25 15.00%

Amount D / Capital E / Capital D / E Levered

Borrowed Ratio Ratio Ratio Beta

rsrdrd (1 – T) WACC

$0 0.00% 100.00% 0.00% 1.25 15.00% — — 15.00%

$250,000 12.50% 87.50% 14.29% 1.38 15.80% 8.0% 6.00% 14.58%

Amount Stock

Borrowed DPS rsprice

$0 $3.75 15.00% $25.00

(4) Using the Hamada equation, what is the cost of equity if CD recapitalizes with $250,000 of debt? $500,000?

$750,000? $1,000,000?

(5) What is the capital structure that minimizes CD’s WACC?

(6) What would be the new stock price if CD recapitalizes with $250,000 of debt? $500,000? $750,000?

$1,000,000? Recall that the payout ratio is 100%, so g = 0.

At D = $1,000,000