LECTURE SUPPLEMENT

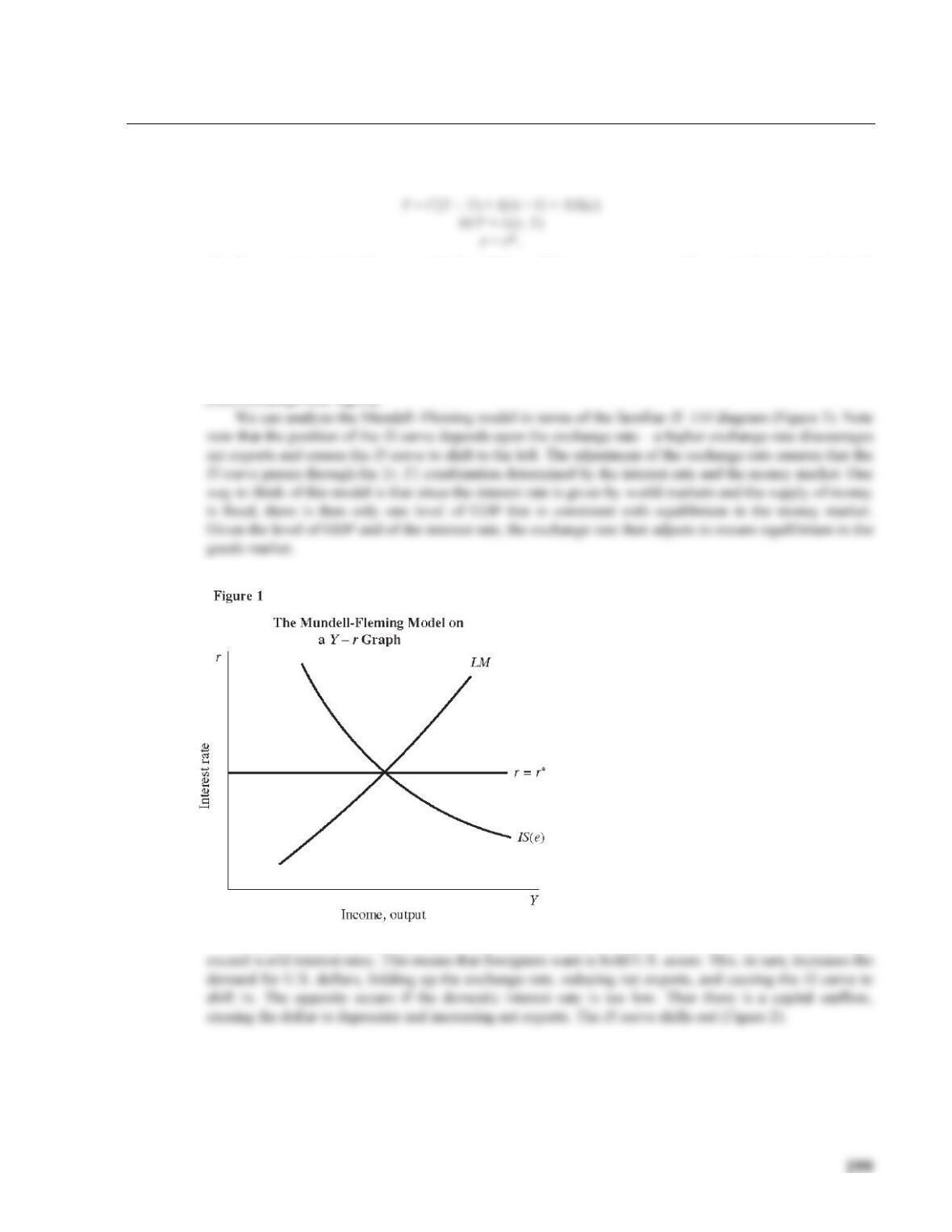

13–6 The Mundell–Fleming Model in Y–r Space

We analyze the open economy in the short run using the Mundell–Fleming model. The basic equations are

The first equation is the IS curve, with the addition of the net exports term. The equivalent loanable–funds

representation is

S(Y) – I(r) = NX(e).

The second equation is the LM curve, and the third is the small–open–economy restriction that the domestic

interest rate must equal the world interest rate. We first think about the model under a flexible– (or

floating) exchange–rate regime and then examine how the conclusions of the model are altered under a

fixed–exchange–rate regime.

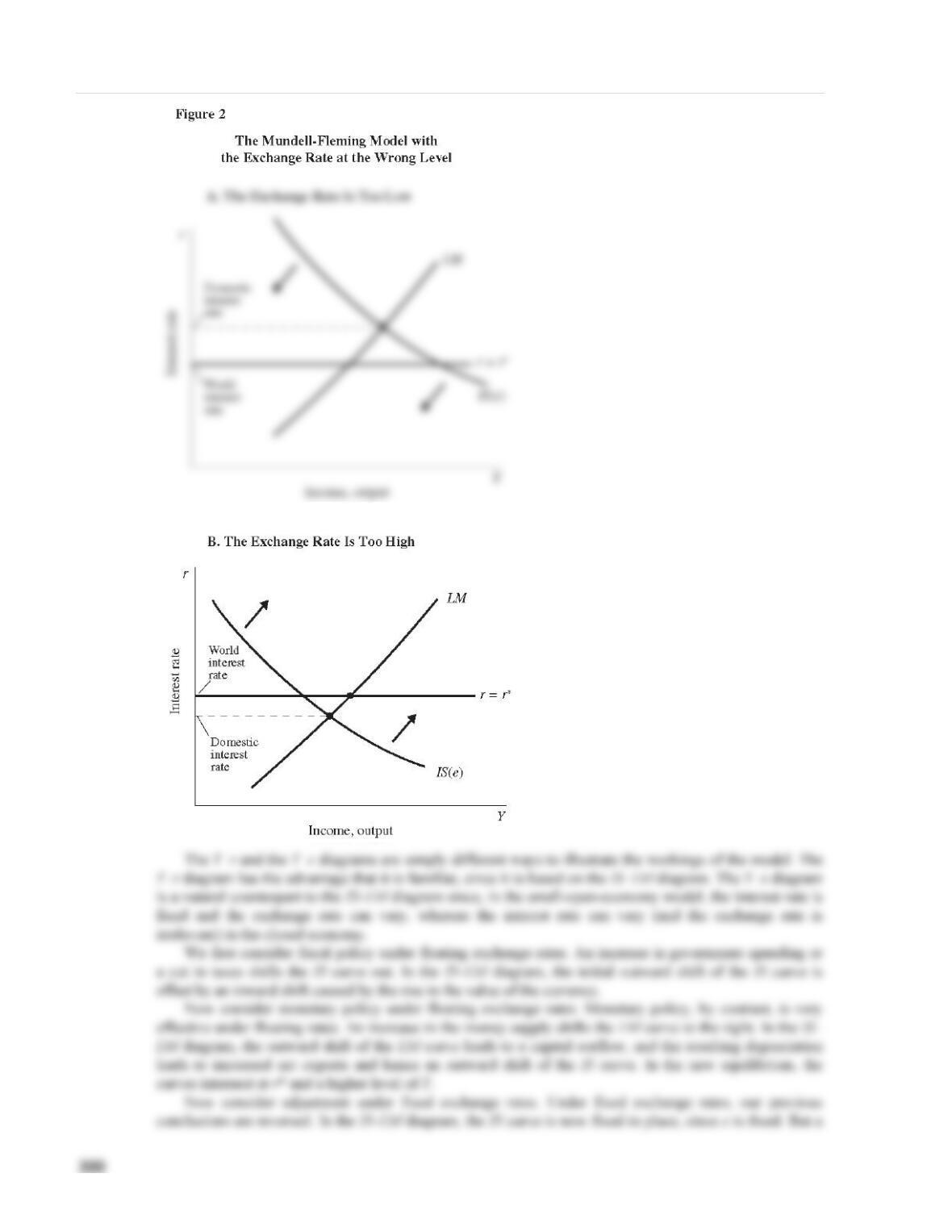

What is the economics behind this? If the IS and LM curves intersect above r*, then U.S. interest rates

300 | CHAPTER 13 The Open Economy Revisited: The Mundell–Fleming Model and the Exchange

Rate Regime

301

greater demand for dollars—caused, for example, by high interest rates—simply leads to a greater supply

of dollars. So now, if r > r*, the LM curve shifts out, and conversely.

An expansionary fiscal policy under fixed exchange rates shifts the IS curve to the right and puts

pressure on interest rates to rise. The demand for U.S. dollars thus increases. Whereas previously this led

to an appreciation of the dollar, now the Fed stands willing to supply the extra dollars that are demanded.

The money supply thus expands to meet the demand, leading to increased output.

ADVANCED TOPIC

13–7 Uncovered Interest Parity

The Mundell–Fleming model assumes that the interest rate in a small open economy must equal the world

interest rate. Yet interest rates often differ in different countries. The reason is that something is missing in

the Mundell–Fleming story: exchange rate expectations.

Think about someone with $1 to invest. She could invest it in the United States and earn the (nominal)

Multiplying out and subtracting 1 from each side gives

∆e/e + i + i(∆e/e) = i*.

We can neglect the term i(∆e/e) since it is the product of two small numbers, so we get1

i – i* = –∆e/e.

This equation is the UIP condition. It tells us that if the domestic interest rate exceeds the world

exchange–rate risk.

All of this analysis is in nominal terms. Exactly the same conclusion holds if we measure variables in

real terms. To see this, remember that the Fisher equation tells us that

i = r + π and i* = r* + π*.

If we substitute these into the UIP condition, we get

303

ADDITIONAL CASE STUDY

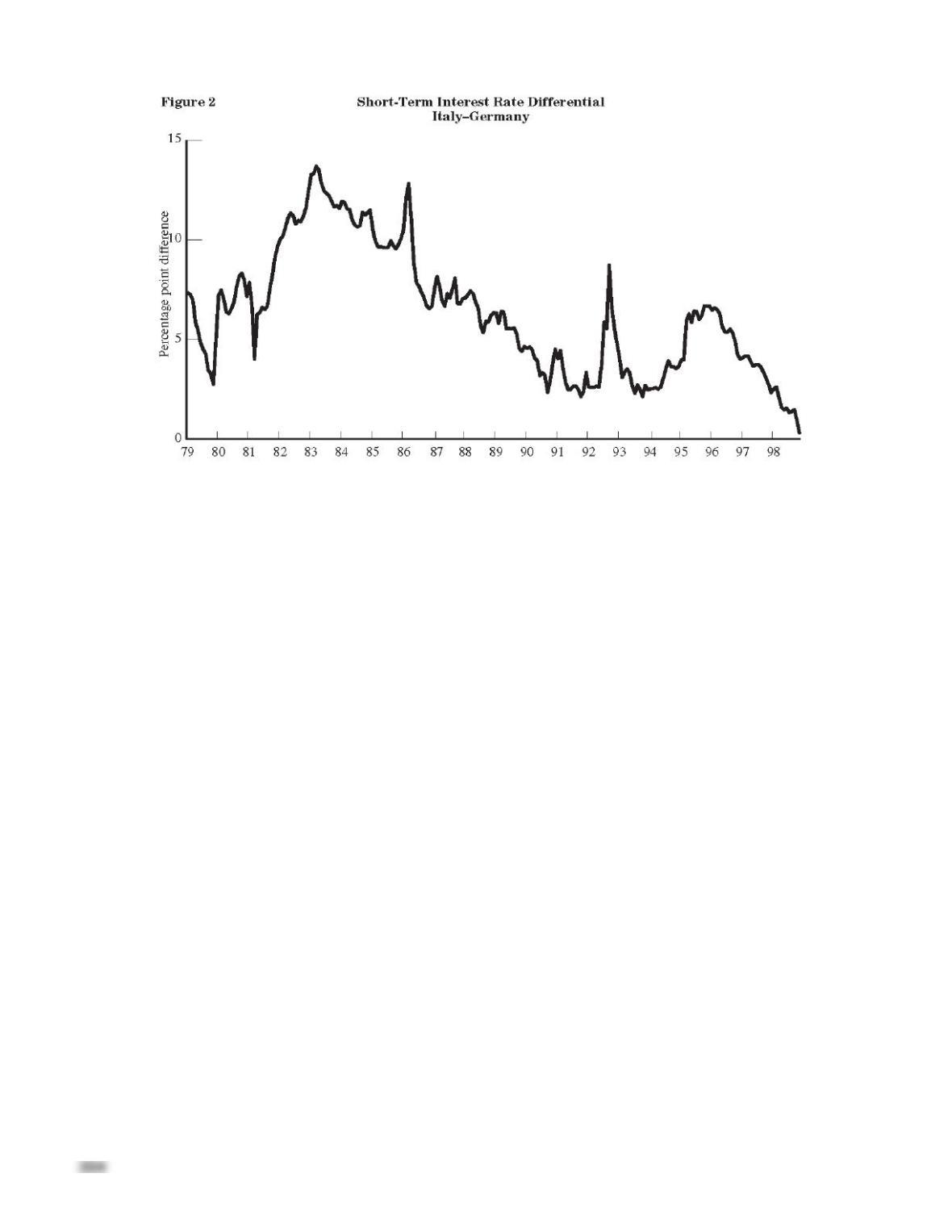

13–8 Interest Rate Differentials in the European Monetary System

To the extent that interest–rate differences across countries reflect expectations about changes in exchange

rates, these differences can provide information about the credibility of a fixed–exchange–rate system. If

two countries fix the rate at which their currencies can be exchanged for each other and if individuals

believe that the exchange rate will not change, then interest rates in the two countries should be identical.

In 1979 several members of the European Union fixed their exchange rates. Each country’s currency

was allowed to fluctuate only within narrow bands against the currencies of the other members of the

exchange–rate mechanism of the European Monetary System. Interest–rate differences between the

countries indicate changes in the credibility of the exchange–rate system. Figures 1 and 2 show the

differences between short–term (three–month) interest rates in France and Germany and short–term interest

rates in Italy and Germany. Throughout the 1980s the exchange rate system became more credible, and

individuals became increasingly convinced that the exchange rates would be maintained. By the beginning

of 1991, for example, French and German interest rates differed by less than 1 percentage point. In 1992

and 1993, however, interest rates in France and Italy rose relative to German rates, reflecting the crisis in

the European Monetary System during those years.11

305

ADVANCED TOPIC

13–9 The Dornbusch Overshooting Model

Exchange rates have proved to be very volatile under the floating–rate system. One possible explanation of

this volatility was provided by the international economist Rudiger Dornbusch. He showed, using the

Mundell–Fleming model, that the nominal exchange rate might overshoot its long–run value in response to

monetary shocks.1 To explain Dornbusch’s argument, we first consider how to introduce uncovered

interest parity (UIP) into the Mundell–Fleming model.2

The key insight of UIP is that the domestic interest rate can diverge from the world interest rate if

investors anticipate changes in the exchange rate. Specifically, arbitrage should ensure that

r – r* = –∆e/e;

that is, the domestic interest exceeds the world interest rate if the domestic currency is expected to

depreciate.33 Following Dornbusch, we assume that expectations about movements in the exchange rate

depend upon where the current exchange rate is relative to its long–run value. Thus, if e is the long–run

level of the nominal exchange rate, we write

∆e/e=–

θ

e–e

( )

.

This tells us that if the actual exchange rate is above its long–run equilibrium level, the exchange rate is

expected to depreciate. (The parameter θ indicates how responsive the exchange rate is to deviations from

its long–run value.)

Putting these two equations together, we get

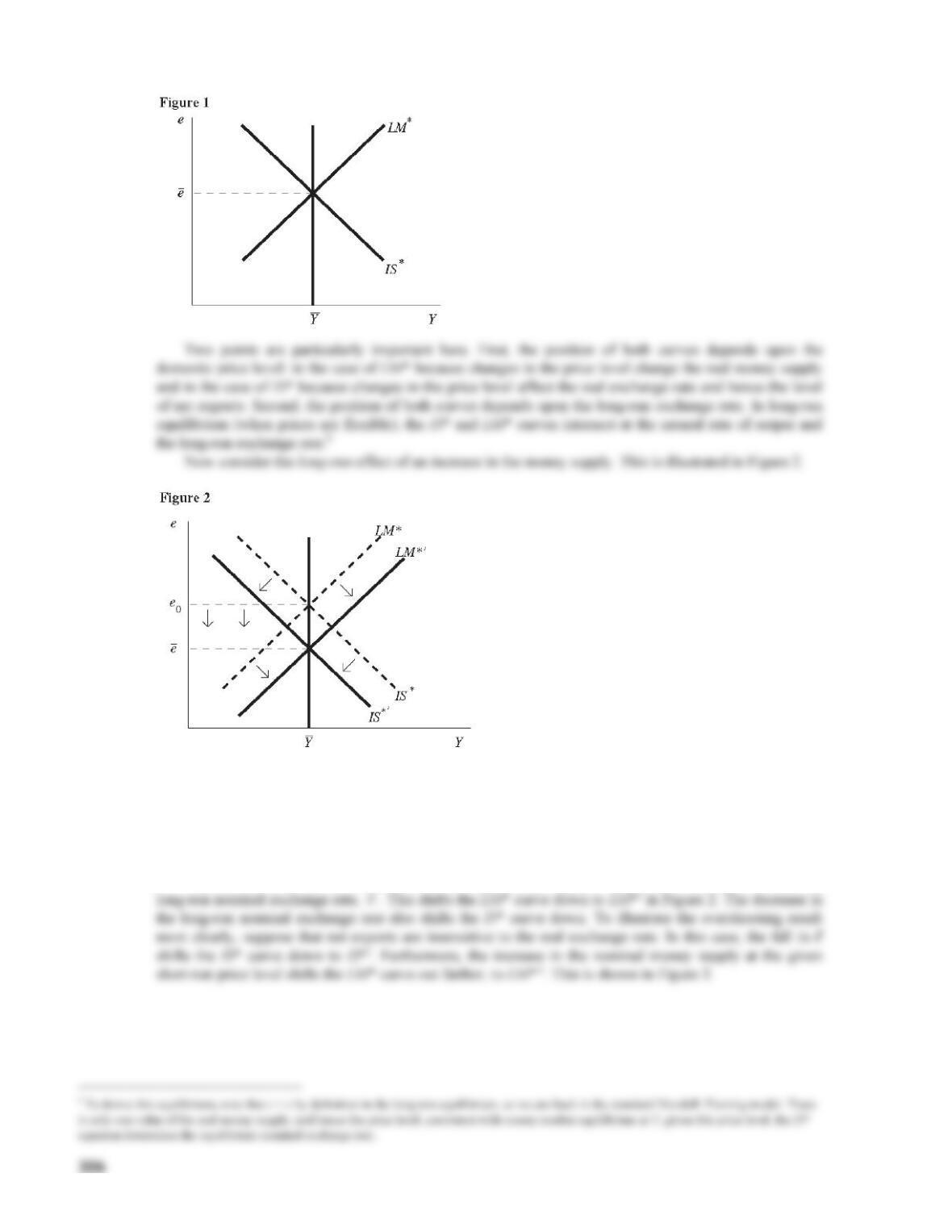

In the long run, after all price adjustment has taken place, the IS* and LM* curves both shift down (recall

that the position of both curves depends upon the price level). Money is neutral in the long run: The price

level increases in proportion to the increase in the money supply, so that the real money supply is

unchanged; and the exchange rate depreciates by an amount proportionate to the rise in prices so that the

real exchange rate is unchanged. For example, if M is increased by 10 percent, then P is 10 percent higher

and e is 10 percent lower in the long run.

What are the short–run effects of an increase in the money supply? People know that this decreases the

308

CASE STUDY EXTENSION

13–10 Mexico’s Foreign Exchange Reserves

Figure 1 shows the decline in Mexico’s foreign exchange reserves during 1994. In February 1994 Mexico

had $29 billion in reserves. In March and April reserves fell as pressure mounted on the peso following the

assassination of the leading presidential candidate, Luis Donaldo Colosio. Although reserves fell by nearly

40 percent between February and April, they remained stable throughout the rest of the spring and into the

summer. In the late fall the Mexican central bank had to return to buying pesos and selling its foreign

309

ADDITIONAL CASE STUDY

13–11 Exchange Rate Volatility

Since the world economies abandoned the Bretton Woods system of fixed exchange rates in 1973,

exchange rates have turned out to be very volatile. A broad illustration of this is the dollar’s major

appreciation during the early 1980s and depreciation in the second half of the decade. For example, in

1980, $1 bought 4.2 French francs, 227 Japanese yen, and 1.8 German marks. In 1985, $1 bought 9.0

francs, 238 yen, and 2.9 marks; at the end of 1992, it bought 5.3 francs, 123 yen, and 1.6 marks.1 Not

surprisingly, such large changes in nominal exchange rates also imply substantial fluctuations in real

exchange rates.

1 Economic Report of the President, 1993, Table B–107:470.

2 Supplements 17–3 to 17–8 discuss asset pricing.

CASE STUDY EXTENSION

13–12 The Federal Reserve and the European Central Bank

The structure of the European System of Central Banks is similar to that of the Federal Reserve System.

The Federal Reserve System is composed of 12 regional banks and the Board of Governors. The president

of each regional bank is chosen by the board of directors of that bank and must be approved by the Board

of Governors. The Board of Governors consists of seven members who are appointed by the President of

voting members; only five presidents have voting rights at any one time. The president of the Federal

Reserve Bank of New York is a permanent voting member. The other four positions rotate annually

among the remaining Federal Reserve Banks.1

The Governing Council is the primary monetary decision–making body of the European System of

Central Banks. It consists of the Executive Board (6 members) and the governors of the central banks of

LECTURE SUPPLEMENT

13-13 Additional Readings

The debate over exchange–rate regimes arises frequently in international macroeconomics. The American

Economic Review, Papers and Proceedings included a session in May 1987 on “Reforming the

International Monetary System” and one in May 1989 on “Exchange Rate Policy.” In each issue John

Williamson makes a case for exchange–rate stabilization. He (and Rudiger Dornbusch) also comment on