13 Chapter model 12/12/2018

BUSINESS RISK AND FINANCIAL RISK (Section 13-2)

OPERATING LEVERAGE

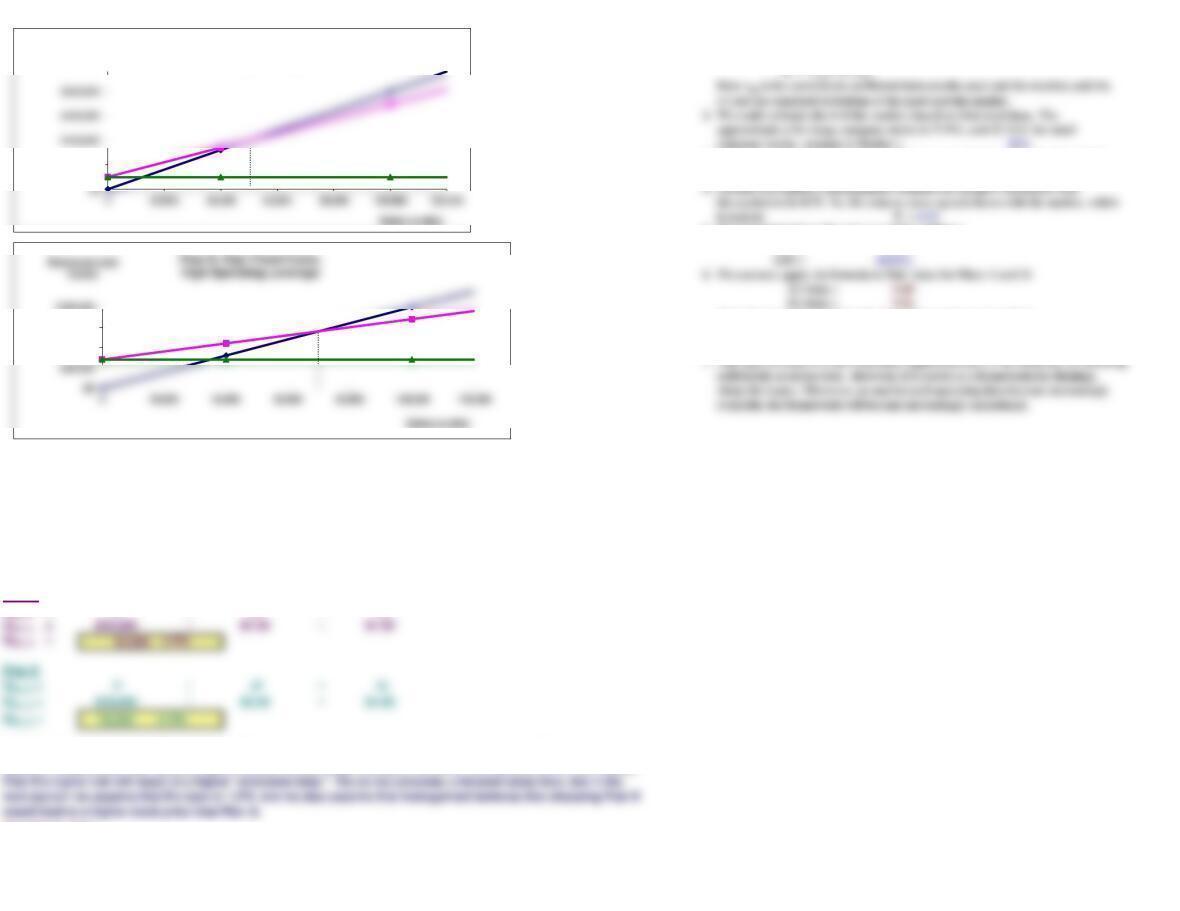

A‘s break-even units = 50,000. B’s break-even units = 70,000.

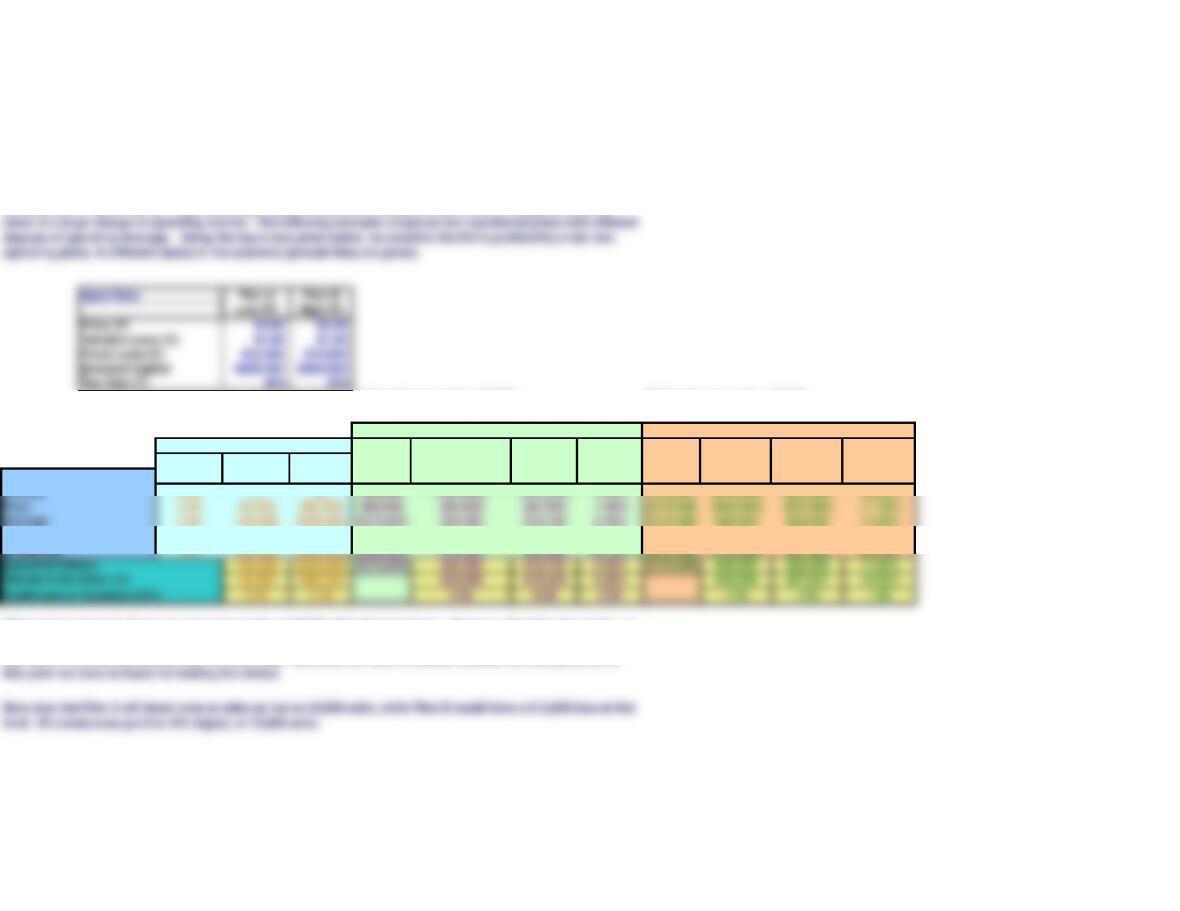

Operating Performance

Units Dollar Operating Operating

Demand Probability Sold Sales Costs EBIT EBIT(1 – T) ROIC Costs EBIT EBIT (1 – T) ROIC

Good 0.20 160,000 $320,000 $265,000 $55,000 $41,250 20.63% $230,000 $90,000 $67,500 33.75%

Which plan is better? Based on expected profits and ROIC, Plan B looks better. However, Plan B is also riskier, as

measured by the standard deviation (s) and the coefficient of variation (CV). So, we face a tradeoff between risk

and return–B is more profitable, but A is less risky. Someone will have to choose between the two plans, but at

Plan B: High Fixed, Low Variable Costs

In this chapter, we introduce two new dimensions of risk, business risk and financial risk. Business risk is the risk

inherent in the firm’s operations, and it would be there even if the firm used no debt. Financial risk is the

additional risk borne by the stockholders as a result of the use of debt.

Operating leverage reflects the degree to which fixed costs are embedded in a firm’s operations. Thus, if a high

percentage of a firm’s costs are fixed, then the firm is said to have high operating leverage because these costs are

incurred even if sales decline. High operating leverage produces a situation where a small change in sales can

Data Applicable to Both Plans

Chapter 13. Capital Structure and Leverage

Plan A: Low Fixed, High Variable Costs

Further discussion of Operating Leverage (Beyond the scope of Concise FFM, but interesting)

1. The beta of the ith asset can be found using this equation:

bi = r i,m ( si / sm )

3. We could calculate the historical R between some traded assets and the market,

and make an educated guess about R for non-traded assets, like Bigbee’s project.

5. We calculated above the s for A and B as follows:

s(A) = 9.26%

s(B) = 18.52%

These betas could be used in the Hamada equation as described

below to bring in financial risk and thus to get an idea of total risk with

different operating and financial plans.

QBE = F / (P − V)

Plan A

QBE, A = F / (P −V)

FINANCIAL RISK

The results generated in the table above are graphed here:

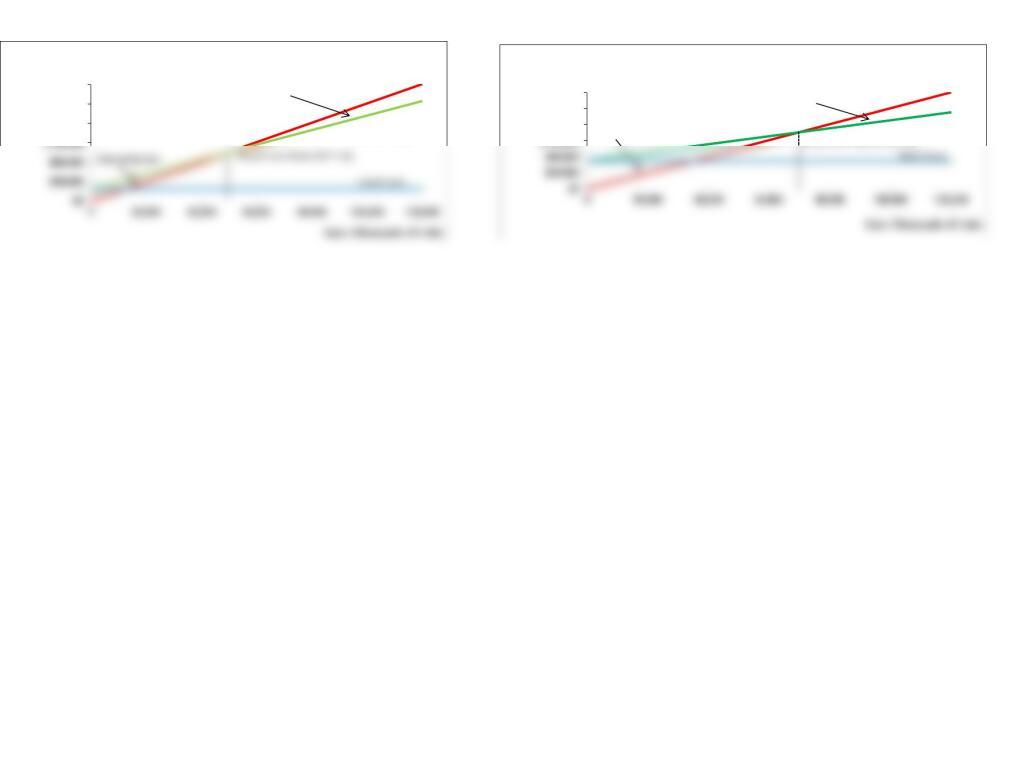

(1) B has a much higher break-even point, and (2) B has more operating leverage in the sense that a given change

in sales leads to a larger change in profits than for A.

We can see from the graph that A‘s break-even point is between 40,000 and 60,000 units and that B’s break-even

point is between 60,000 and 80,000 units, but we cannot tell the exact points. However, we can use the following

formula to find the exact break-even point for both plans:

At this point, we know that Plan B has a higher expected rate of return, but it is also more risky. Our analysis is

based on stand-alone risk. However, given a positive correlation between the firm’s returns and that on the market,

$100,000

$150,000

$200,000

$50,000

Revenues and

Costs

Plan A: Low Fixed Costs,

Low Operating Leverage

2. We could estimate the s of the market, based on historical data. The

approximate s for large company stocks is 27.9%, and 25.76% for small

company stocks. Assume s Market = 25%

Amount Cost of

Borrowed Debt

0% $0 4.0%

10% $20,000 4.0%

The risk of the stock is reflected in the stock’s beta coefficient, and, as we discuss below, beta rises with the use of

debt–the more debt, the higher the beta. The lowest beta is the one that would exist if no debt were used–this is

the “unlevered beta,” and it reflects the firm’s business risk.

Discussions with its bankers indicate that Bigbee can borrow different amounts, but the more it borrows, the

higher the cost of its debt as shown in the table below:

Debt/Capital

Ratio

Financial leverage refers to the use of fixed-income securities (preferred stock and debt) in the capital structure.

The firm has a certain amount of business risk as discussed above in connection with operating leverage. This

business risk is measured by the firm’s “unlevered beta,” which is the beta it would have if it had no debt. If the

Debt Cost Schedule

20% $40,000 4.3%

OPTION 1: Finance Plan B entirely with common equity (Equity = 100%, Debt = 0%)

Invested capital $200,000

Debt/Capital ratio 0%

Demand for Net Income =

Product Probability EBIT EBIT(1 − T) ROIC Interest (EBIT − Int)(1 − T) ROE EPS

Terrible

0.05 ($70,000) ($52,500) -26.25% $0 ($52,500) -26.25% ($5.25)

Poor

0.20 ($30,000) ($22,500) -11.25% $0 ($22,500) -11.25% ($2.25)

Expected value $30,000 $22,500 11.25% $0 $22,500 11.25% $2.25

Standard deviation 18.52% $3.70

Coefficient of variation 1.65 1.65

OPTION 2: Finance Plan B with $100,000 of debt and $100,000 of equity (50% equity, 50% debt)

Invested capital $200,000

Debt/Capital ratio 50%

Equity/Capital ratio 50%

Interest rate 7.2% Interest rate from debt cost schedule above.

Tax rate 25%

Shares outstanding 5,000 Assumes stock can be repurchased at the current price.

Demand for Net Income =

Product Probability EBIT EBIT(1 − T) ROIC Interest (EBIT − Int)(1 − T) ROE EPS

Terrible 0.05 ($70,000) ($52,500) -26.25% $7,200 ($57,900) -57.90% ($11.58)

Poor 0.20 ($30,000) ($22,500) -11.25% $7,200 ($27,900) -27.90% ($5.58)

Expected value $30,000 $22,500 11.25% $7,200 $17,100 17.10% $3.42

Standard deviation 37.05% $7.41

Coefficient of variation 2.17 2.17

Equity/Capital ratio 100%

Interest rate 4.00% Interest rate from debt cost schedule above.

Tax rate 25%

Shares outstanding 10,000

Debt/Capital

Ratio

Exp. EPS SD of EPS CV of EPS

50% $3.42 $7.41 2.17

0% $2.25 $3.70 1.65 Minimum risk

10% $2.43 $4.12 1.69

60% $3.38 $9.26 2.74

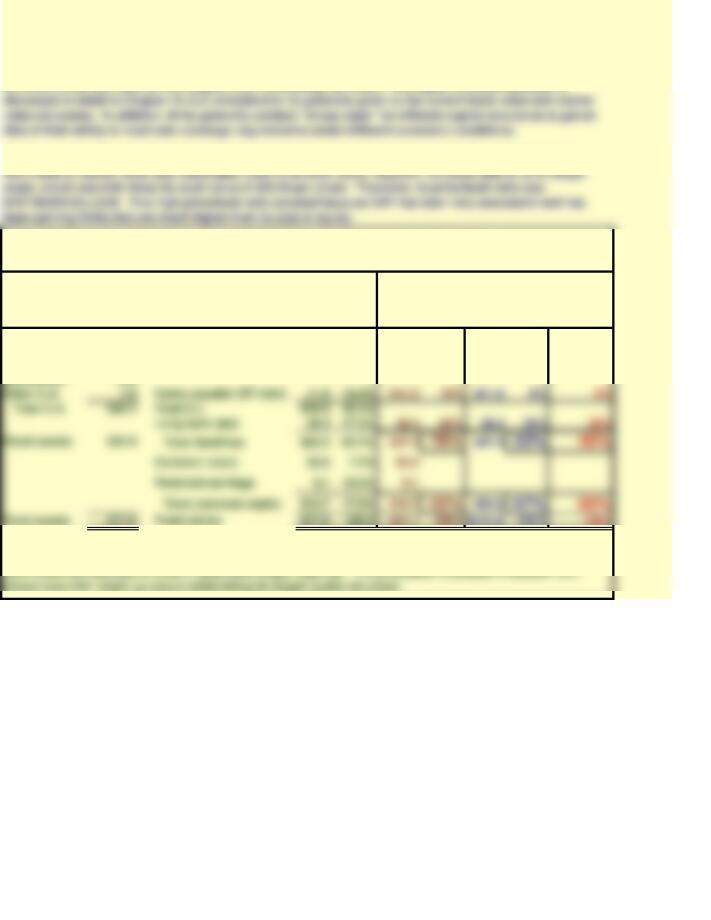

DETERMINING THE OPTIMAL CAPITAL STRUCTURE (Section 14-3)

THE HAMADA EQUATION

bU1.375

Tax rate 25%

Debt/Capital D/E

bL

0.0 0.00 1.375

0.3 0.43 1.817

0.4 0.67 2.063

0.6 1.50 2.922

Hamada developed his equation by merging the CAPM with the Modigliani-Miller model. We use the model to

determine beta at different amounts of financial leverage, and then use the betas associated with different

debt/capital ratios to find the cost of equity associated with each of those debt/capital ratios. Here is the Hamada

equation:

In the table below, we apply the Hamada equation to Bigbee Electronics, given its unlevered beta and tax rate.

The optimal capital structure is the one that maximizes the stock price, and this is the same one that minimizes the

WACC. To find–or, really, estimate–the optimal capital structure, we need information on how capital structure

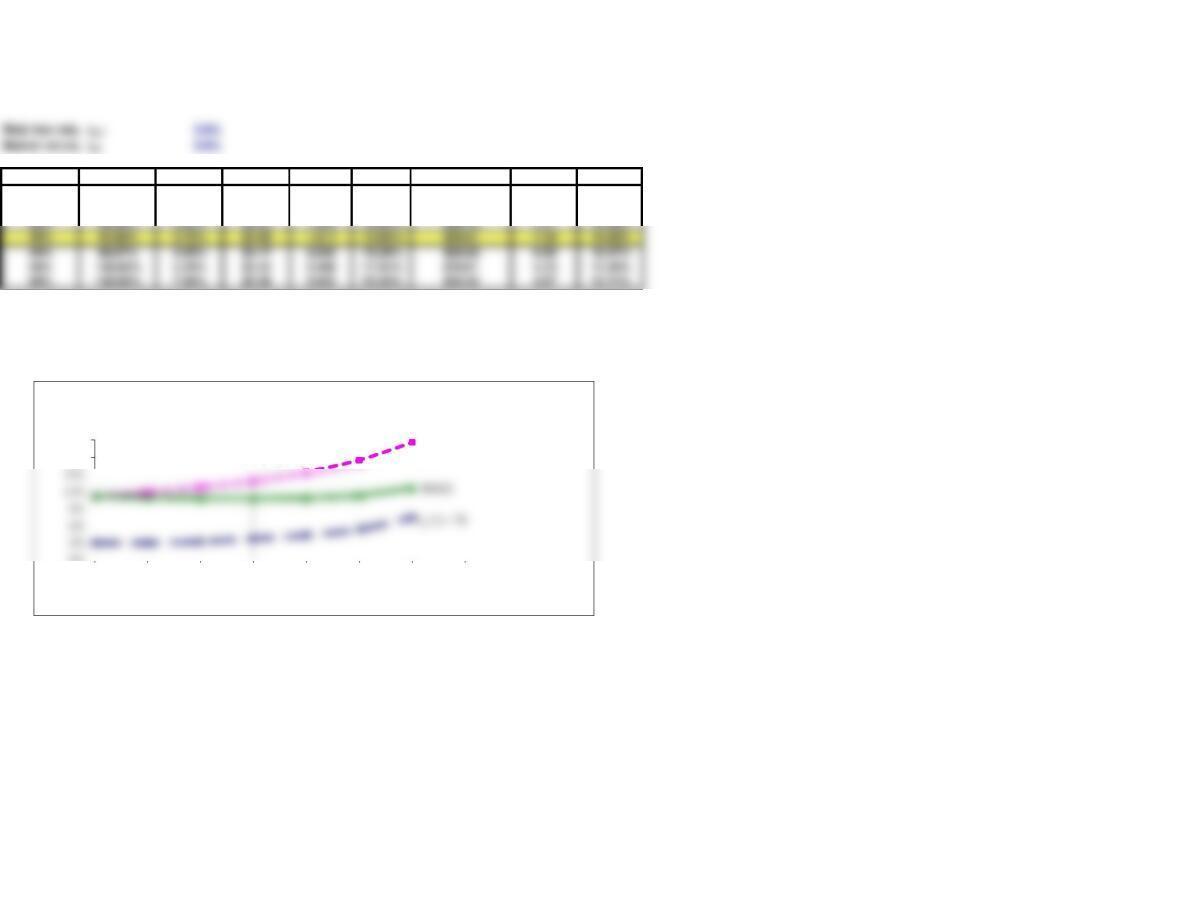

In the tables just above, we calculated the expected EPS and risk measures at zero debt and at 50% debt. We can

use an Excel Data Table to calculate these values at a number of different debt/capital ratios, as shown below.

There’s a conflict between risk and return so we must decide what the appropriate tradeoff is, i.e., we must decide

the optimal capital structure.

20% $2.65 $4.63 1.75

Debt/Capital D/E

rd(1 – T) EPS = DPS Est. beta rsEst. Price P/E Ratio WACC

0% 0.00% 3.00% $2.25 1.375 11.25% $20.00 8.89 11.25%

10% 11.11% 3.00% $2.43 1.490 11.94% $20.38 8.38 11.04%

40% 66.67% 4.35% $3.17 2.063 15.38% $20.62 6.50 10.97%

We see that the stock price is maximized, and the WACC is minimized, if the firm finances with 30% debt and 70%

equity. This is the optimal capital structure.

Below, we graph the key data from the table above.

As the table shows, beta rises with financial leverage. With beta specified, we can determine the effects of

leverage on the cost of equity and then on the WACC. Here we assume that the risk-free rate is 3%, the required

return on the market is 9%, and, therefore, the market risk premium is 6%. We also assume that Bigbee pays out all

of its earnings as dividends, hence its earnings and dividends are not expected to grow. Therefore, its stock price

can be found by using the perpetuity equation, Price = Dividend/rs.

0%

18%

21%

0% 10% 20% 30% 40% 50% 60% 70%

Cost of Capital

Debt/Capital Ratio

Effects of Capital Structure on the Cost of Capital

rs

13 Chapter model 12/12/2018

Section 13-1. Book, Market, or Target Weights?

Assets Target %

Cash $8.3 Accounts payable $10.2 13.2% – – – – –

Receivables 16.1 Accruals 5.7 7.4% – – – – –

Inventories 10.0

CAT had 597.63 million shares outstanding, its book value per share was $23.03, and its year-end market price

was $157.58 per share. We do not know its management-determined target capital structure. The 40% debt

We can think about a firm’s capital structure in three ways: (1) in book value terms, (2) in market value terms,

or (3) as a target capital structure that is not tied directly to either book or market data. The target capital

structure is the one used for the weights when calculating the WACC. The capital structure decision is

We show below, in columns A-H, an abbreviated balance sheet of Caterpillar Inc.(CAT) as of 12/31/17. The

Table 13.1 Caterpillar Inc.’s Book Value, Market Value, and Target Capital Structure

(Dollars in Billions)

Condensed Balance Sheet

Assets and Claims Against Assets At Book Values

Investor supplied capital: Payables and

accruals are excluded because they come

from operations, not from investors

Claims

Book Value

Market Value

2. In CAT‘s case, as is often true, we assume that the market value of the debt is

approximately equal to its book value, but the common stock’s market price differs from

its book value.

3. The stock sells at a price of $157.58 per share versus a book value of $23.03, and the firm

has 597.63 million shares outstanding. Therefore, the market value of the common equity is

4. No distinction is made between common equity raised by issuing stock vs. retaining

earnings when establishing the target capital structure.

5. For illustrative purposes, we assume that CAT has the same cost for long-term bonds and

short-term notes payable, hence it can lump the two together and use a 40% weight for

all investor-supplied debt, i.e., for all debt other than accounts payable and accruals. If

the interest rates varied, then the firm could treat long- and short-term debt separately or

6. If CAT used preferred stock, the market value of that stock would be calculated in the

same way as we calculated the market value of its common equity.

7. Assume that the average interest rate on both short- and long-term new debt is 5%, the

firm’s tax rate is 25%, and its cost of equity is 11%. Here are the WACCs based on book,

market, and target weights:

calculated WACC. The greater the difference between the book and market values of the

stock, and the greater the difference between the costs of debt and equity, the greater

the difference in the calculated WACCs.

8. Generally, a firm’s managers take into account its current and recent past book and

market value structures, as well as those of firms used as benchmarks, when they

like the one we do in the remainder of the chapter.

Accounts payable and accruals come in as a result of operations, not from investors,

so they are not considered to be capital as the term is used here. The capital structure

13 Chapter model 12/12/2018

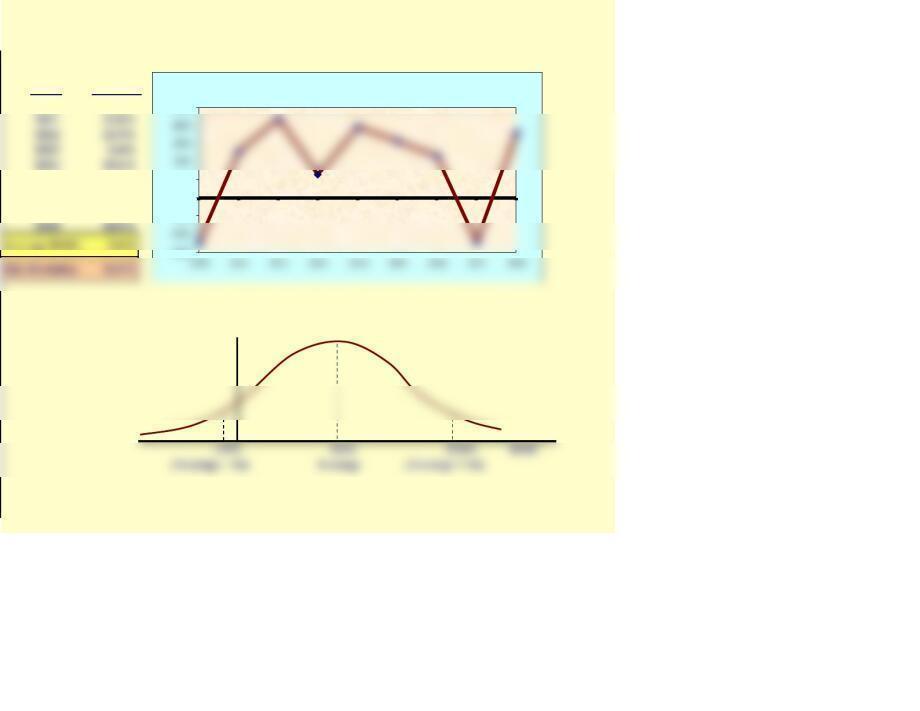

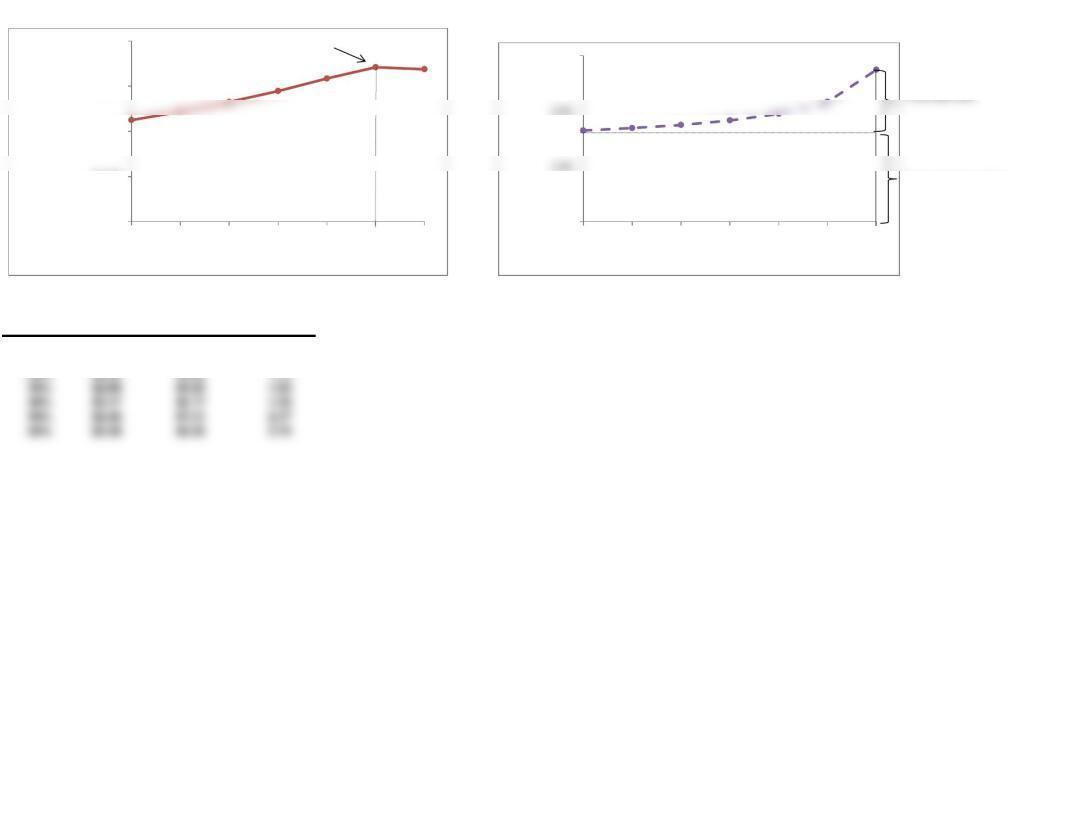

Figure 13.1 Return on Invested Capital (ROIC), 2010−2018

a. ROIC Over Time: An Indicator of Business Risk

Year

ROIC

2010 -12.4%

2015 15.7%

2016 11.5%

2017 -12.2%

b. Probability Distribution of ROIC: Another Indicator of Business Risk

Probability

Since Bigbee has no debt, its ROIC is equal to its ROE, hence we could replace the term

ROIC with ROE. Note, though, that as soon as debt is issued, ROE and ROIC will differ.

-15%

-5%

0%

5%

25%

ROIC

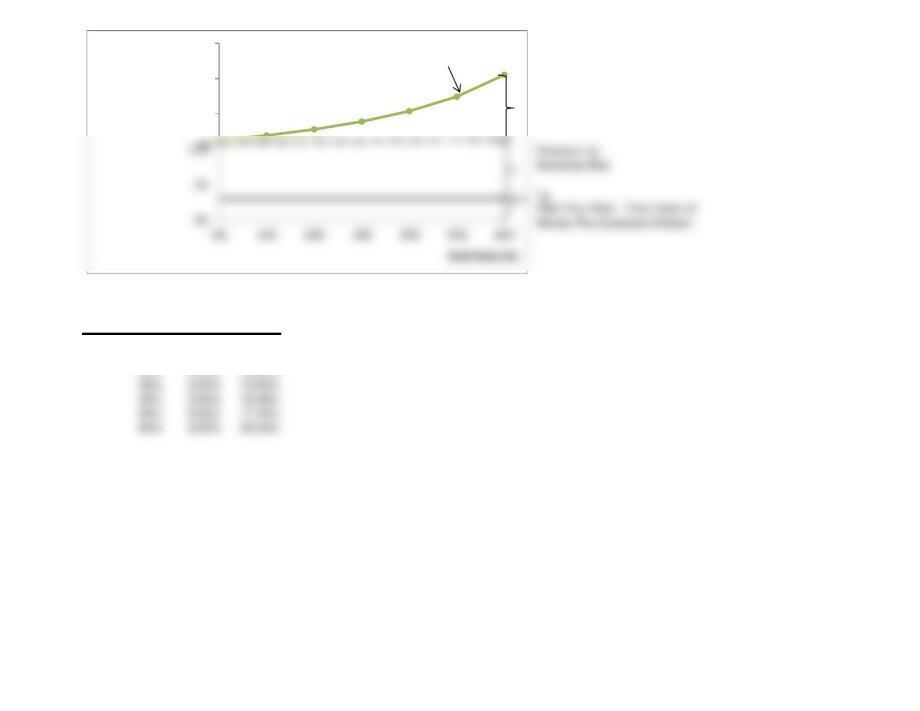

Figure 13.2 Illustration of Operating Leverage 12/12/2018

Plan A Plan B

$160,000

$200,000

$240,000

Revenues and Costs

(Thousands of

Dollars)

Total Operating Costs

Sales Revenues

Operating Profit (EBIT)

$120,000

$160,000

$200,000

$240,000

Revenues and Costs

(Thousands of

Dollars)

Sales Revenues

Total Operating Costs

Break-Even Point (EBIT = 0)

Operating Loss

Operating Profit (EBIT)

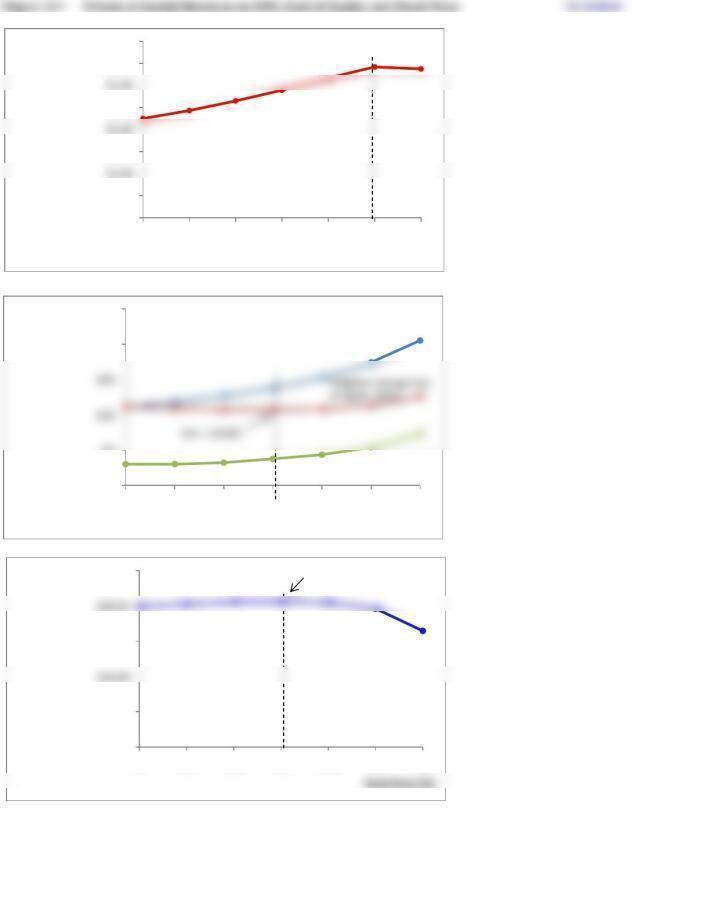

Figure 13.5 Relationships among Expected EPS, Risk, and Financial Leverage

Debt/Capital

Expected

EPS

Standard

Deviation of EPS

Coefficient

of Variation

0% $2.25 $3.70 1.65

10% $2.43 $4.12 1.69

20% $2.65 $4.63 1.75

Basic Business Risk

Additional Risk to Stockholders

from Use of Financial Leverage:

Financial Risk

12/12/2018

$0.00

$1.00

$2.00

$3.00

$4.00

0% 10% 20% 30% 40% 50% 60%

Expected EPS

Debt Ratio (%)

Peak EPS = $3.42

0.00

3.00

0% 10% 20% 30% 40% 50% 60%

Risk

(CVEPS)

Debt Ratio (%)

Figure 13.6 Bigbee’s Required Rates of Return on Equity at Different Debt Levels 12/12/2018

Premium for

Financial Risk

Debt/Capital

rRF rs

0% 3.00% 11.25%

10% 3.00% 11.94%

15%

20%

25%

Required Return

on Equity (%)

rS

$0.00

$0.50

$1.50

$2.50

$3.50

$4.00

0% 10% 20% 30% 40% 50% 60%

Expected EPS ($)

Debt Ratio (%)

Maximum EPS = $3.42

0%

5%

20%

25%

0% 10% 20% 30% 40% 50% 60%

Cost of Capital

(%)

Debt Ratio (%)

Cost of Equity, rs

After-Tax Cost of

$0.00

$5.00

$15.00

$25.00

0% 10% 20% 30% 40% 50% 60%

Stock Price ($)

Maximum = $20.81

Debt/Capital D/E

rd(1 – T) EPS = DPS Est. beta rsEst. Price P/E Ratio WACC

0.00% 0.00% 3.00% $2.25 1.375 11.25% $20.00 8.89 11.25%

50.00% 100.00% 5.40% $3.42 2.406 17.44% $19.61 5.73 11.42%

SECTION 13-3 12/12/2018

SOLUTIONS TO SELF-TEST QUESTIONS

bL1.25

Tax rate 25%

bU0.8101

Equity/Capital ratio (Case 1) 1.00

EquityCapital ratio (Case 2) 0.58

4. Use the Hamada equation to calculate the unlevered beta for Firm X with the following data: bL

= 1.25; T = 25%; Debt/Capital = 0.42; Equity/Capital = 0.58.

5a. What would the cost of equity be for Firm X at an Equity/Capital ratio of 1.0 (no debt), assuming

that rRF = 5% and RPM = 4%?

5b. What would the cost of equity be for Firm X at an Equity/Capital ratio of 0.58, assuming that rRF

= 5% and RPM = 4%?

Debt/Capital ratio 0.42

Equity/Capital ratio 0.58