382

Integrated Case

Chapter 13: Capital Structure and Leverage

A. (1) What is business risk? What factors influence a firm’s business

risk?

Answer: [Show S13-1 through S13-4 here.] Business risk is the riskiness

inherent in the firm’s operations if it uses no debt. A firm’s

business risk is affected by many factors, including these: (1)

A. (2) What is operating leverage, and how does it affect a firm’s

business risk?

Answer: [Show S13-5 through S13-7 here.] Operating leverage is the

extent to which fixed costs are used in a firm’s operations. If a

A. (3) What is the firm’s return on invested capital (ROIC)?

Answer: [Show S13-8 here.]

ROIC =

capital invested Total

)T 1(EBIT −

Chapter 13: Capital Structure and Leverage

Integrated Case

383

B. (1) What do the terms financial leverage and financial risk mean?

Answer: [Show S13-9 here.] Financial leverage refers to the firm’s decision

to finance with fixed-income securities, such as debt and preferred

B. (2) How does financial risk differ from business risk?

Answer: [Show S13-10 here.] As we discussed above, business risk

depends on a number of factors such as sales and cost variability

C. To develop an example that can be presented to CD’s management

as an illustration, consider two small hypothetical firms: Firm U

with zero debt financing and Firm L with $10,000 of 12% debt.

Both firms have $20,000 in invested capital and a 25% federal-

plus-state tax rate, and they have the following EBIT probability

distribution for next year:

Probability EBIT

0.50 3,000

(1) Complete the partial income statements and the firms’ ratios in

Table IC 13.1.

384

Integrated Case

Chapter 13: Capital Structure and Leverage

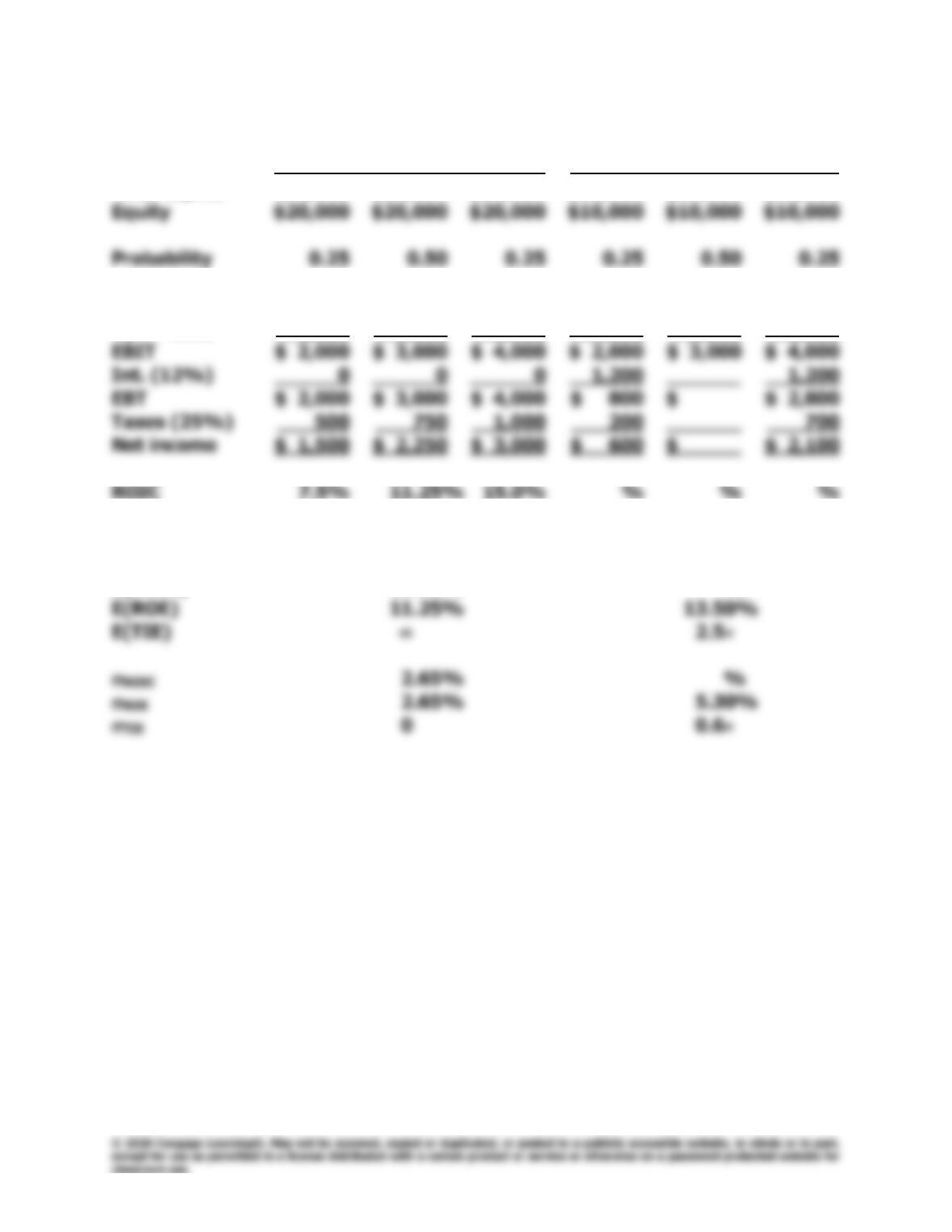

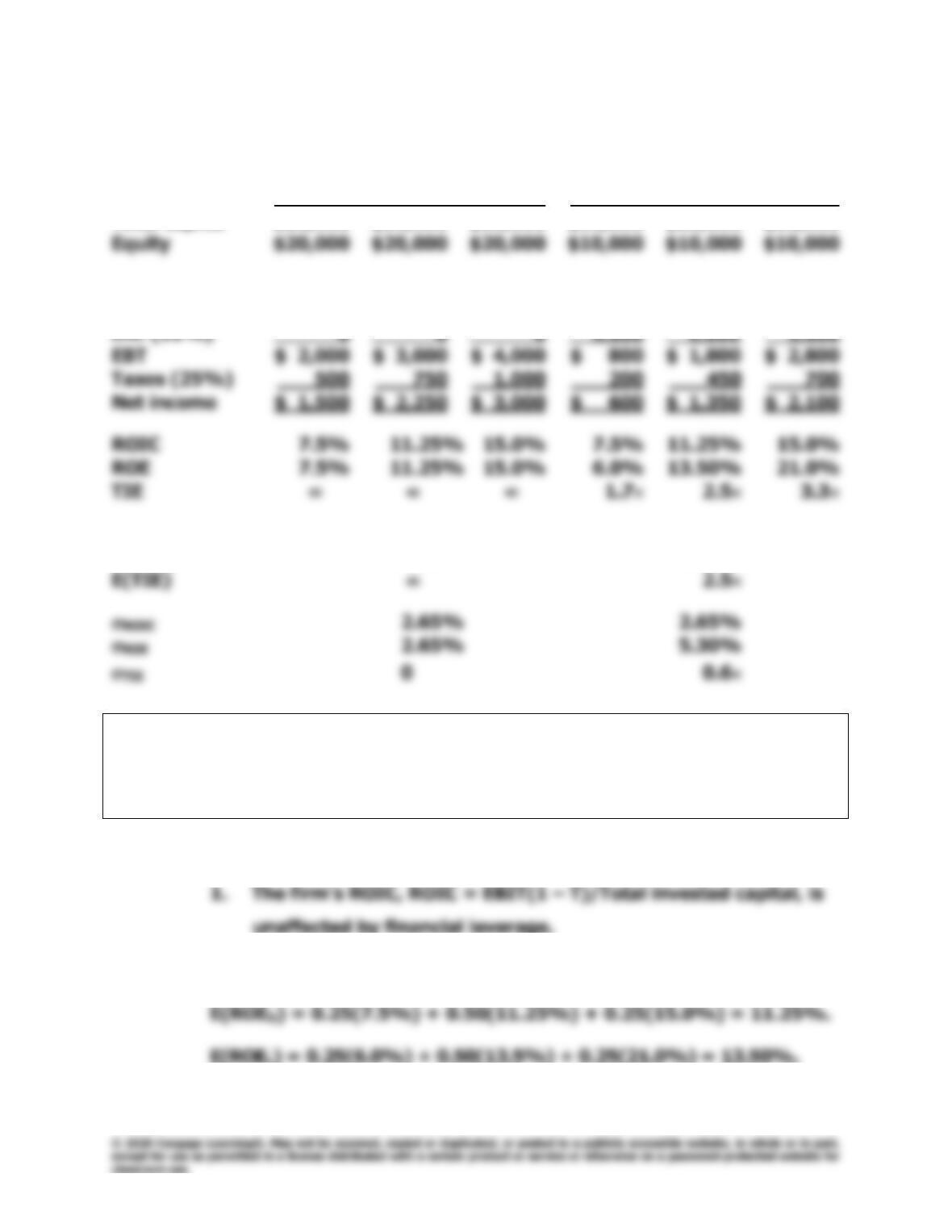

Table IC 13.1. Income Statements and Ratios

Firm U Firm L

Total capital $20,000 $20,000 $20,000 $20,000 $20,000 $20,000

Sales $ 6,000 $ 9,000 $12,000 $ 6,000 $ 9,000 $12,000

Oper. costs 4,000 6,000 8,000 4,000 6,000 8,000

ROE 7.5% 11.25% 15.0% 6.0% % 21.0%

TIE 1.7 3.3

E(ROIC) 11.25% %

Chapter 13: Capital Structure and Leverage

Integrated Case

385

Answer: [Show S13-11 through S13-15 here.] Here are the fully completed

statements:

Firm U Firm L

Total capital $20,000 $20,000 $20,000 $20,000 $20,000 $20,000

Probability 0.25 0.50 0.25 0.25 0.50 0.25

EBIT $ 2,000 $ 3,000 $ 4,000 $ 2,000 $ 3,000 $ 4,000

E(ROIC) 11.25% 11.25%

E(ROE) 11.25% 13.50%

C. (2) Be prepared to discuss each entry in the table and to explain how

this example illustrates the effect of financial leverage on expected

rate of return and risk.

Answer: [Show S13–16 and S13-17 here.] Conclusions from the analysis:

2. Firm L has the higher expected ROE:

386

Integrated Case

Chapter 13: Capital Structure and Leverage

Therefore, the use of financial leverage has increased the

3. Firm L has a wider range of ROEs, and a higher standard

deviation of ROE, indicating that its higher expected return is

accompanied by higher risk. To be precise:

4. When EBIT = $2,000, ROEU > ROEL, and leverage has a

5. Leverage will always boost expected ROE if expected ROIC

6. Finally, note that the TIE ratio is huge (undefined, or infinitely

large) if no debt is used, but it is relatively low if 50% debt is

Chapter 13: Capital Structure and Leverage

Integrated Case

387

D. After speaking with a local investment banker, you obtain the

following estimates of the cost of debt at different debt levels (in

thousands of dollars):

Amount Debt/Capital Debt/Equity Bond

Borrowed Ratio Ratio Rating rd

$ 0 0.000 0.0000 — —

250 0.125 0.1429 AA 8.0%

500 0.250 0.3333 A 9.0

750 0.375 0.6000 BBB 11.5

1,000 0.500 1.0000 BB 14.0

Now consider the optimal capital structure for CD.

(1) To begin, define the terms optimal capital structure and target

capital structure.

Answer: [Show S13-18 here.] The optimal capital structure is the capital

structure at which the tax-related benefits of leverage are exactly

offset by debt’s risk–related costs. At the optimal capital structure,

D. (2) Why does CD’s bond rating and cost of debt depend on the amount

of money borrowed?

Answer: [Show S13-19 here.] Financial risk is the additional risk placed on the

common stockholders as a result of the decision to finance with debt.

388

Integrated Case

Chapter 13: Capital Structure and Leverage

D. (3) Assume that shares could be repurchased at the current market price

of $25 per share. Calculate CD’s expected EPS and TIE at debt levels

of $0, $250,000, $500,000, $750,000, and $1,000,000. How many

shares would remain after recapitalization under each scenario?

Answer: [Show S13–20 through S13-26 here.] The analysis for the debt

levels being considered (in thousands of dollars and shares) is

shown below:

At D = $0:

EPS =

goutstandin Shares

)T1)](D(rEBIT[ d−−

= [$400,000(0.75)]/80,000 = $3.75.

Chapter 13: Capital Structure and Leverage

Integrated Case

389

At D = $500,000:

Shares repurchased = $500,000/$25 = 20,000.

At D = $750,000:

Shares repurchased = $750,000/$25 = 30,000.

At D = $1,000,000:

Shares repurchased = $1,000,000/$25 = 40,000.

D. (4) Using the Hamada equation, what is the cost of equity if CD

recapitalizes with $250,000 of debt? $500,000? $750,000?

$1,000,000?

390

Integrated Case

Chapter 13: Capital Structure and Leverage

rRF = 7.5% rM – rRF = 6.0%

Amount Debt/Capital Debt/Equity Levered

Borroweda Ratiob Ratioc Betad rse

$ 0 0.00% 0.00% 1.25 15.00%

250 12.50 14.29 1.38 15.80

Notes:

a Data given in problem.

b Calculated as amount borrowed divided by total capital.

c Calculated as amount borrowed divided by equity (total capital

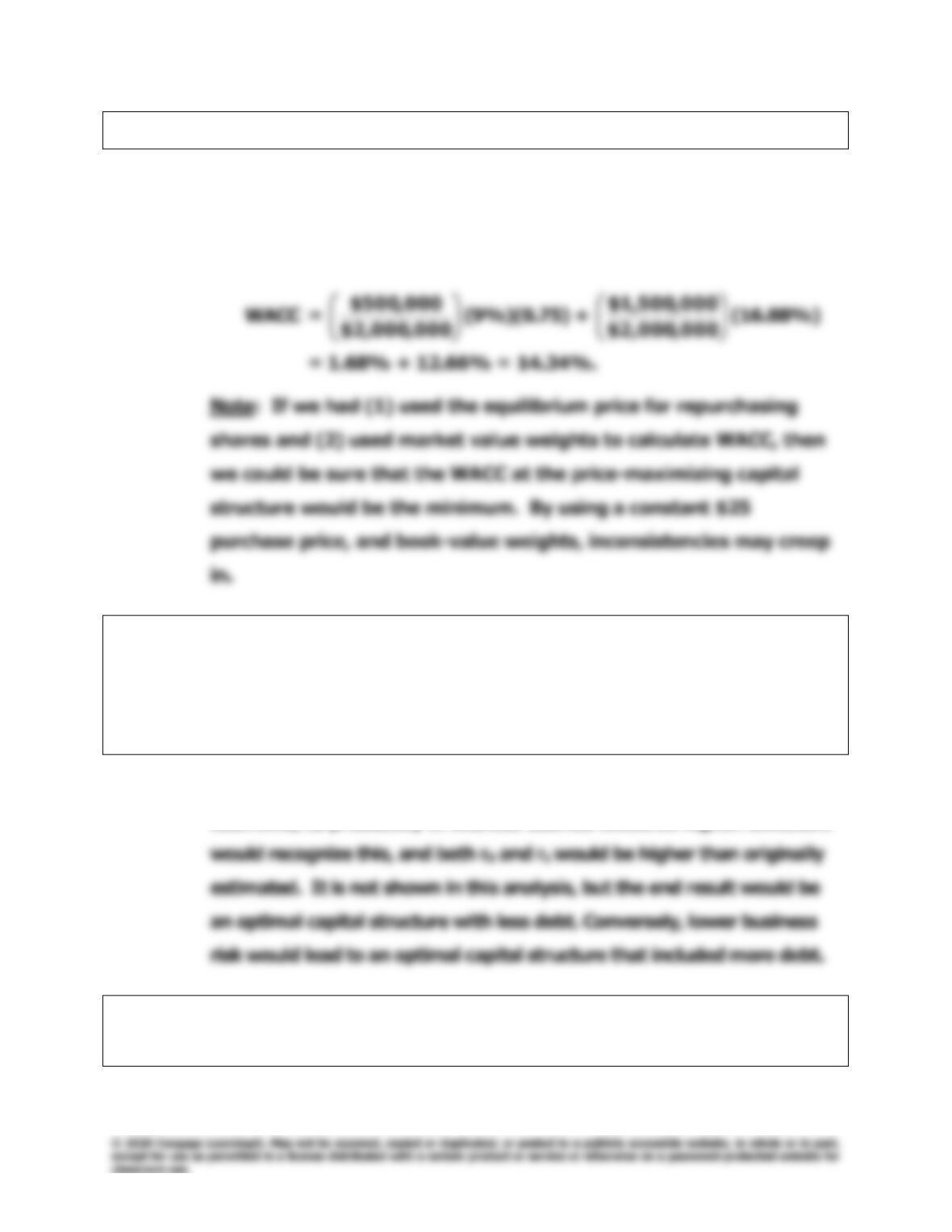

D. (5) Considering only the levels of debt discussed, what is the capital

structure that minimizes CD’s WACC?

Chapter 13: Capital Structure and Leverage

Integrated Case

391

rRF = 7.5% rM – rRF = 6.0%

Tax rate = 25.0%

Amount

Borroweda

Debt/Capital

Ratiob

Equity/Capital

Ratioc

Debt/Equity

Ratiod

Levered

Betae

rsf

rda

rd(1 – T)

WACCg

$ 0

0.00%

100.00%

0.00%

1.25

15.00%

0.0%

0.00%

15.00%

250

87.50

14.29

1.38

15.80

8.0

6.00

14.58

500

25.00

75.00

33.33

1.56

16.88

9.0

6.75

14.34

750

62.50

60.00

1.81

18.38

8.63

14.72

50.00

2.19

15.56

Notes:

a Data given in problem.

b Calculated as amount borrowed divided by total capital.

c Calculated as 1 – D/(D + E).

d Calculated as amount borrowed divided by equity (total capital less

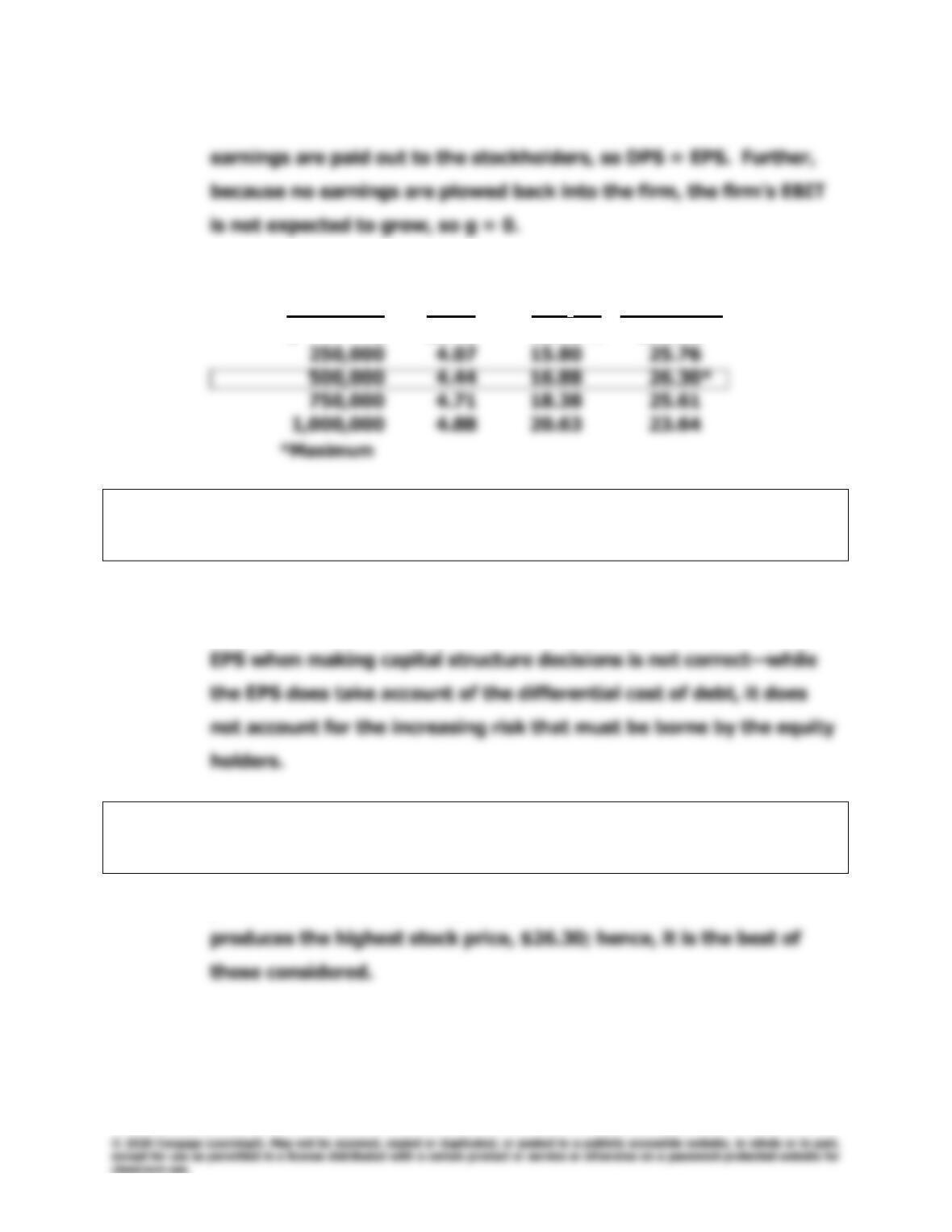

D. (6) What would be the new stock price if CD recapitalizes with

$250,000 of debt? $500,000? $750,000? $1,000,000? Recall that

the payout ratio is 100%, so g = 0.

Answer: [Show S13-34 and 13-35 here.] We can calculate the price of a

constant growth stock as DPS divided by rs minus g, where g is the

392

Integrated Case

Chapter 13: Capital Structure and Leverage

expected growth rate in dividends: P0 = D1/(rs – g). In this case all

Here are the results:

Debt Level DPS rs Stock Price

$ 0 $3.75 15.00% $25.00

D. (7) Is EPS maximized at the debt level that maximizes share price?

Why or why not?

Answer: [Show S13-36 here.] We have seen that EPS continues to increase

beyond the $500,000 optimal level of debt. Therefore, focusing on

D. (8) Considering only the levels of debt discussed, what is CD’s optimal

capital structure?

Answer: [Show S13-37 here.] A capital structure with $500,000 of debt

Chapter 13: Capital Structure and Leverage

Integrated Case

393

D. (9) What is the WACC at the optimal capital structure?

Answer: Initial debt level:

Debt/Total capital = 0%, so Total capital = Initial equity = $25

80,000 shares = $2,000,000.

E. Suppose you discovered that CD had more business risk than you

originally estimated. Describe how this would affect the analysis.

How would the analysis be affected if the firm had less business

risk than originally estimated?

Answer: [Show S13–38 here.] If the firm had higher business risk, then, at any

debt level, its probability of financial distress would be higher. Investors

F. What are some factors a manager should consider when

establishing his or her firm’s target capital structure?

394

Integrated Case

Chapter 13: Capital Structure and Leverage

Answer: [Show S13-39 here.] Since it is difficult to quantify the capital

structure decision, managers consider the following judgmental

factors when making capital structure decisions:

2. Pro forma TIE ratios at different capital structures under

different scenarios.

4. Reserve borrowing capacity.

6. Asset structure.

8. Management attitudes.

10. Firm’s internal conditions.

12. Firm’s growth rate.

Chapter 13: Capital Structure and Leverage

Integrated Case

395

Optional Question

Modigliani and Miller proved, under a very restrictive set of assumptions, that

the value of a firm will be maximized by financing almost entirely with debt.

Why, according to MM, is debt beneficial?

Answer: MM argued that using debt increases the value of the firm because

interest is tax deductible. The government, in effect, pays part of the

interest, and this lowers the cost of debt relative to the cost of

396

Integrated Case

Chapter 13: Capital Structure and Leverage

Optional Question

What assumptions underlie the MM theory? Are these assumptions realistic?

Answer: MM’s key assumptions are as follows:

2. There are no taxes.

4. Investors have the same information as managers about the

firm’s future investment opportunities.

6. EBIT is not affected by the use of debt.

These assumptions are obviously unrealistic—investors do incur

Chapter 13: Capital Structure and Leverage

Integrated Case

397

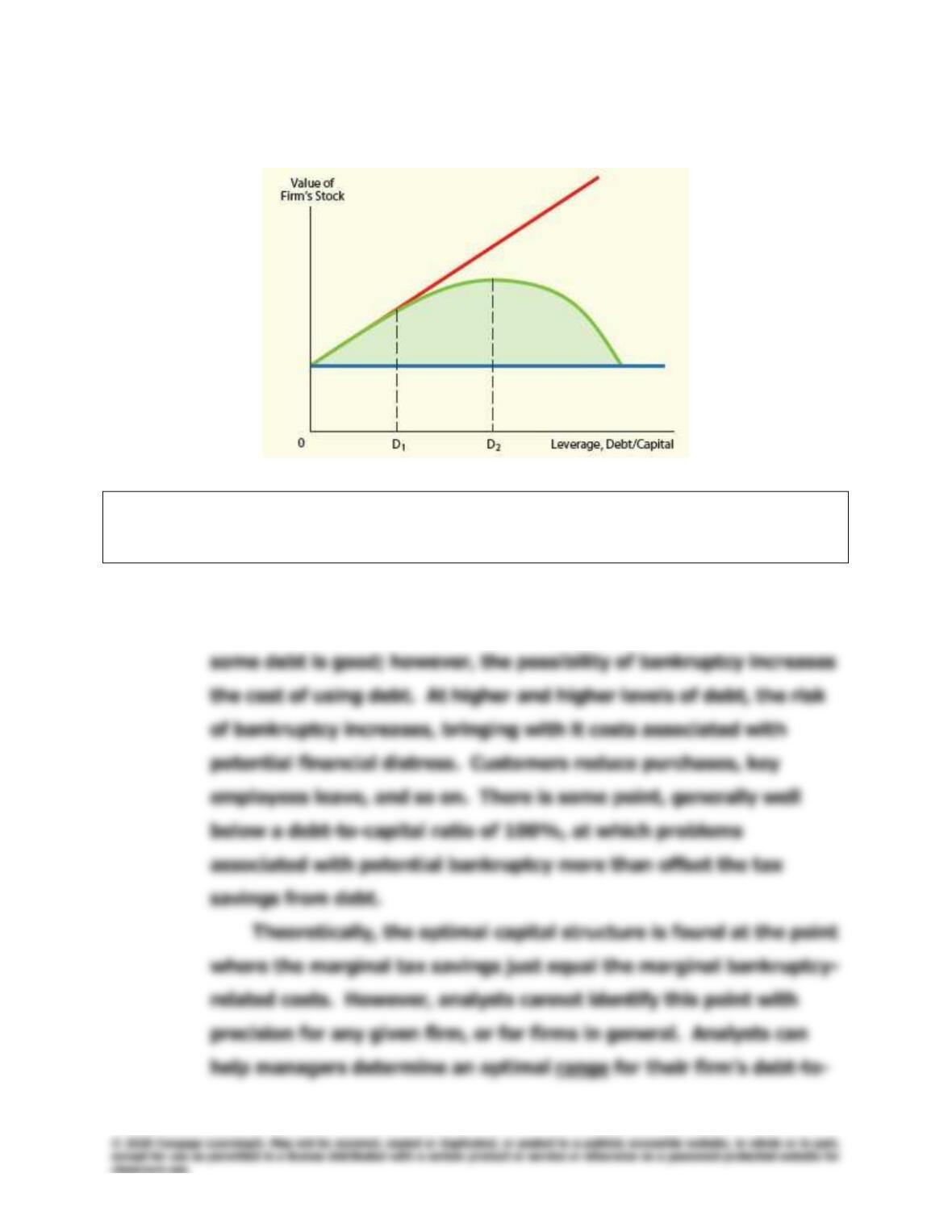

Figure IC 14.1. Relationship Between Capital Structure and Stock Price

G. Put labels on Figure IC 13.1 and then discuss the graph as you might

use it to explain to your boss why CD might want to use some debt.

Answer: [Show S13–40 and S13-41 here.] The use of debt permits a firm to

obtain tax savings from the deductibility of interest. So the use of

398

Integrated Case

Chapter 13: Capital Structure and Leverage

H. How does the existence of asymmetric information and signaling

affect capital structure?

Answer: [Show S13-42 through S13-45 here.] The asymmetric information

concept is based on the premise that management’s choice of

Chapter 13: Capital Structure and Leverage

Integrated Case

399

Optional Question

You might expect the price of a mature firm’s stock to decline if it announces a

stock offering. Would you expect the same reaction if the issuing firm were a

young, rapidly growing company?

Answer: If a mature firm sells stock, the price of its stock would probably

decline. A mature firm should have other financing alternatives, so