Chapter 13: Capital Structure and Leverage

Learning Objectives

363

Chapter 13

Capital Structure and Leverage

Learning Objectives

After reading this chapter, students should be able to do the following:

◆ Explain why there may be differences in a firm’s capital structure when measured on a book-value

basis, a market-value basis, or a target basis.

364

Lecture Suggestions

Chapter 13: Capital Structure and Leverage

Lecture Suggestions

This chapter is rather long, but it is also modular, hence sections can be omitted without loss of

continuity. Therefore, if you are experiencing a time crunch, you could skip selected sections.

DAYS ON CHAPTER: 4 OF 56 DAYS (50-minute periods)

Chapter 13: Capital Structure and Leverage

Answers and Solutions

365

Answers to End-of-Chapter Questions

13-1 Operating leverage is the extent to which fixed costs are used in a firm’s operations. If operating

13-2 a. The break-even point will be lowered.

b. The effect on the break-even point is indeterminant. An increase in fixed costs will increase

13-3 If sales tend to fluctuate widely, then cash flows and the ability to service fixed charges will also

13-4 An increase in the personal tax rate makes both stocks and bonds less attractive to investors

because it raises the tax paid on dividend and interest income. Changes in personal tax rates will

have differing effects, depending on what portion of an investment’s total return is expected in the

13-5 a. An increase in the corporate tax rate would encourage a firm to increase the amount of debt

in its capital structure because a higher tax rate increases the interest deductibility feature of

debt.

b. An increase in the personal tax rate would cause investors to shift from bonds to stocks due

to the attractiveness of the deferral of capital gains taxes. This would raise the cost of debt

relative to equity; thus, firms would be encouraged to use less debt in their capital

structures.

13-6 Biotechnology companies use relatively little debt because their industries tend to be cyclical,

oriented toward research, or subject to huge product liability suits. Utility companies, on the

13-7 EBIT depends on sales and operating costs that generally are not affected by the firm’s use of

financial leverage, because interest is deducted from EBIT. At high debt levels, however, firms

13-8 Expected EPS is generally measured as EPS for the coming years, and we typically do not reflect

in this calculation any bankruptcy-related costs. Also, EPS does not reflect (in a major way) the

13-9 The tax benefits from debt increase linearly, which causes a continuous increase in the firm’s

13–10 With increased competition after the breakup of AT&T, the new AT&T and the seven Bell

operating companies’ business risk increased. With this component of total company risk

13–11 The firm may want to assess the asset investment and financing decisions jointly. For instance,

the highly automated process would require fancy, new equipment (capital intensive) so fixed

costs would be high. A less automated production process, on the other hand, would be labor

intensive, with high variable costs. If sales fell, the process that demands more fixed costs might

Solutions to End-of-Chapter Problems

13-1 QBE =

VP

F

−

13-2 The optimal capital structure is that capital structure where WACC is minimized and stock price is

13-3 a. Expected EPS for Firm C:

b. According to the standard deviations of EPS, Firm B is the least risky, while C is the riskiest.

However, this analysis does not consider portfolio effects—if C’s earnings increase when most

other companies’ decline (that is, its beta is low), its apparent riskiness would be reduced.

Also, standard deviation is related to size, or scale, and to correct for scale we could calculate a

coefficient of variation (/mean):

13–4 From the Hamada equation, b = bU[1 + (1 – T)(D/E)], we can calculate bU as bU = b/[1 + (1 – T)(D/E)].

368

Answers and Solutions

Chapter 13: Capital Structure and Leverage

13-5 a. ROIC =

capital Total

)TEBIT(1−

.

b. LL: Debt/Capital = 30%; Debt = 0.3 × $20,000,000 = $6,000,000.

EBIT $4,000,000

Interest ($6,000,000 0.10) 600,000

c. LL: Debt/Capital = 60%; Debt = 0.6 × $20,000,000 = $12,000,000.

EBIT $4,000,000

Interest ($12,000,000 0.15) 1,800,000

Although LL’s return on equity is higher than it was at the 30% leverage ratio, it is lower

than the 21.0% return of HL.

13-6 a. 9,000 units 15,000 units

Sales $234,000 $390,000

Chapter 13: Capital Structure and Leverage

Answers and Solutions

369

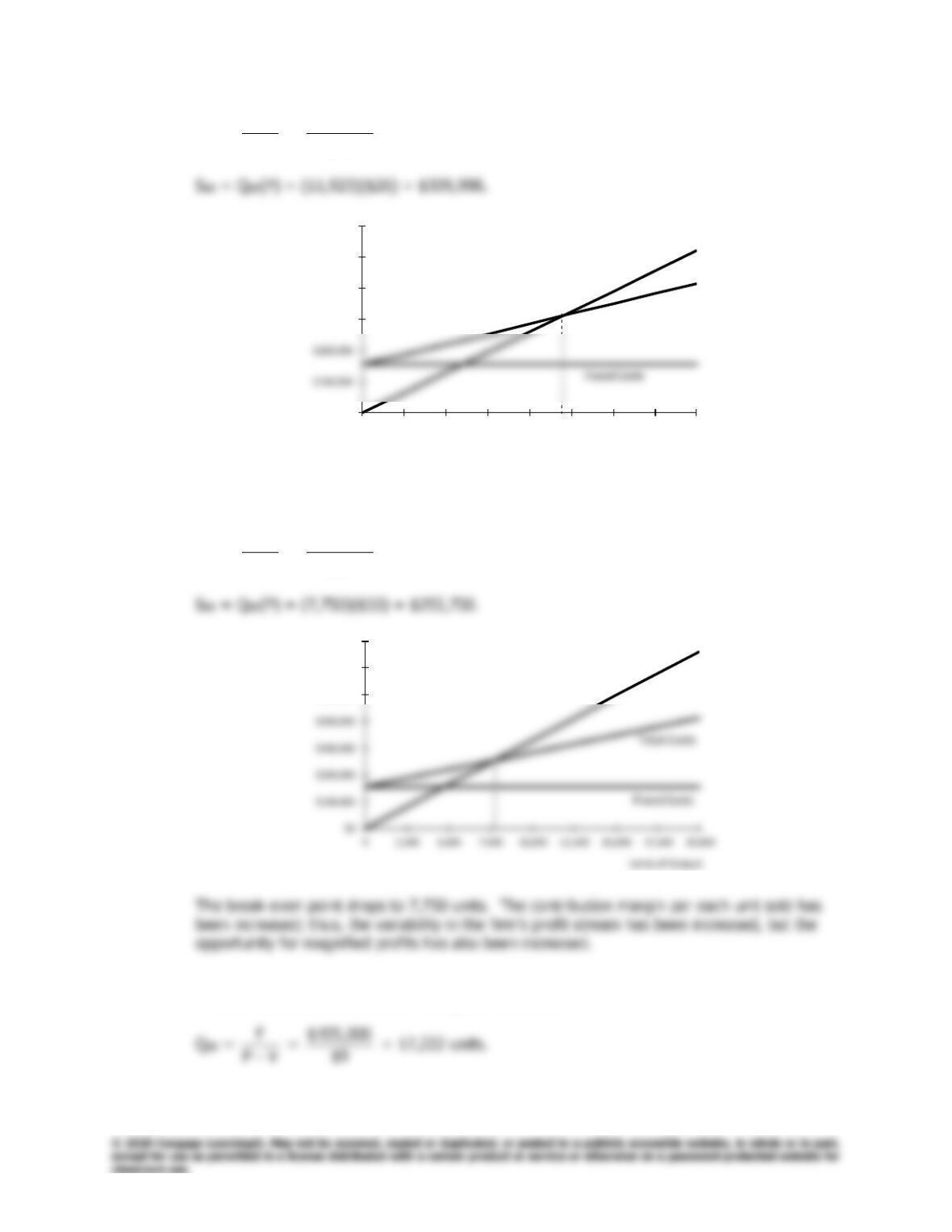

b. QBE =

V P

F

−

=

3$1

,00055$1

= 11,923 units.

$0

$300,000

$400,000

$500,000

$600,000

0 2,500 5,000 7,500 10,000 12,500 15,000 17,500 20,000

Units of Output

Revenues

Total Costs

c. If the selling price rises to $33, while the variable cost per unit remains fixed, P – V rises to

$20. The end result is that the break-even point is lowered.

QBE =

V P

F

−

=

20$

,00055$1

= 7,750 units.

$500,000

$600,000

$700,000

Revenues

d. If the selling price rises to $33 and the variable cost per unit rises to $24, P – V falls to $9.

The end result is that the break-even point increases.

,00055$1

The break-even point increases to 17,222 units because the contribution margin per each

unit sold has decreased.

$400,000

$500,000

$600,000

$700,000

Total Costs

Revenues

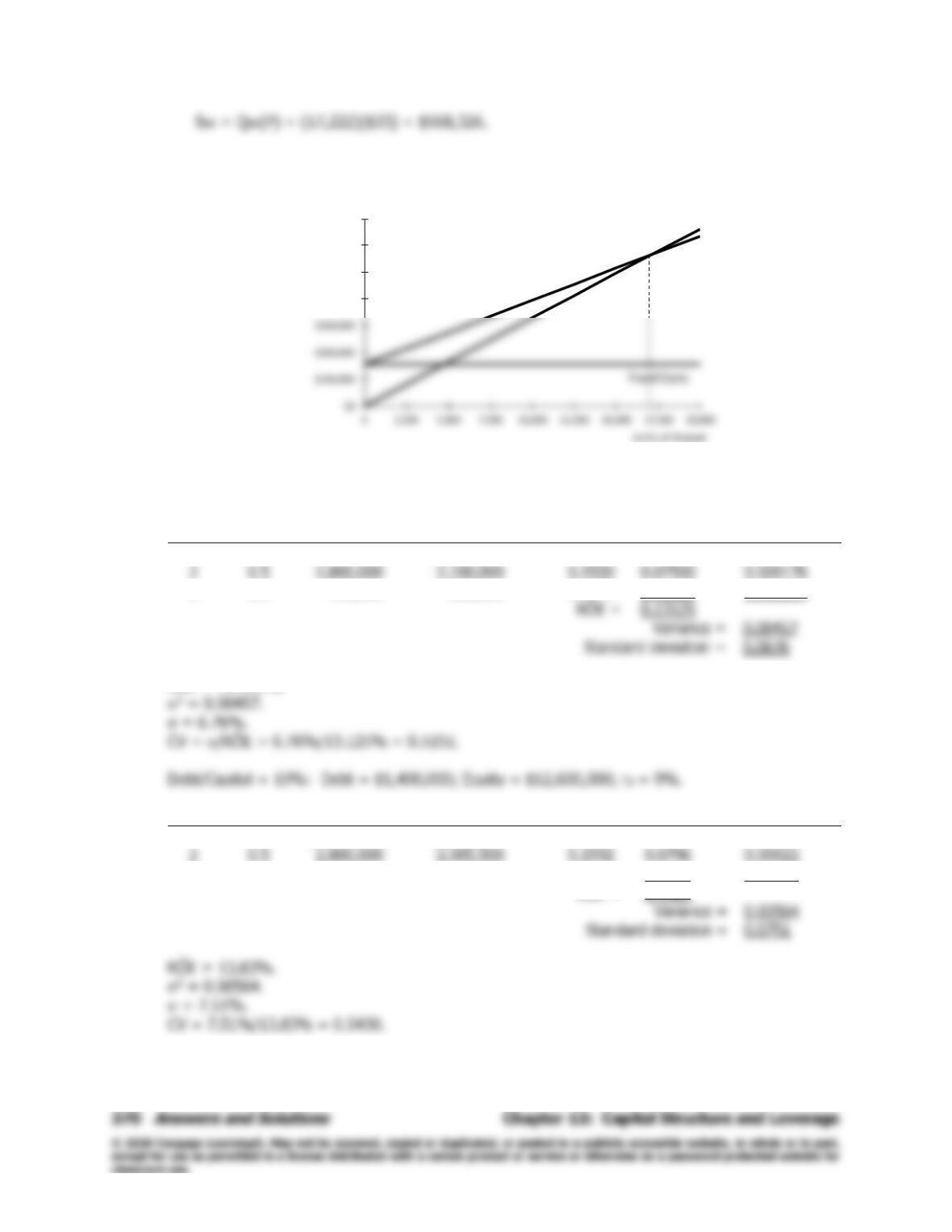

13-7 No leverage: Debt = 0; Equity = $14,000,000.

State

Ps

EBIT

(EBIT – rdD)(1 – T)

ROES

PS(ROE)

PS(ROES – RÔE)2

1

0.2

$4,200,000

$3,150,000

0.2250

0.04500

0.001758

2

0.5

2,800,000

2,100,000

0.1500

0.000176

3

0.3

700,000

525,000

0.0375

0.01125

0.002637

RÔE =

0.13125

0.00457

RÔE = 13.125%.

State

Ps

EBIT

(EBIT – rdD)(1 – T)

ROES

PS(ROE)

PS(ROES – RÔE)2

1

0.2

$4,200,000

$3,055,500

0.2425

0.0485

0.00217

2

0.5

2,800,000

2,005,500

0.1592

0.0796

0.00022

3

0.3

700,000

430,500

0.0342

0.0102

0.00326

RÔE =

0.1383

0.00564

Chapter 13: Capital Structure and Leverage

Answers and Solutions

371

Debt/Capital = 50%: Debt = $7,000,000; Equity = $7,000,000; rd = 11%.

State

Ps

EBIT

(EBIT – rdD)(1 – T)

ROES

PS(ROE)

PS(ROES – RÔE)2

1

0.2

$4,200,000

$2,572,500

0.3675

0.0735

0.00703

2

0.5

2,800,000

0.2175

0.1087

0.00070

3

0.3

700,000

(52,500)

(0.0075)

(0.0022)

0.01055

0.1800

0.01828

RÔE = 18.0%.

2 = 0.01828.

Debt/Capital = 60%: D = $8,400,000; E = $5,600,000; rd = 14%.

State

Ps

EBIT

(EBIT – rdD)(1 – T)

ROES

PS(ROE)

PS(ROES – RÔE)2

1

0.2

$4,200,000

$2,268,000

0.4050

0.0810

0.01099

2

0.5

2,800,000

1,218,000

0.2175

0.1087

0.00110

3

0.3

700,000

(357,000)

(0.0638)

(0.0191)

0.01648

0.1706

0.02856

RÔE = 17.06%.

As leverage increases, the expected return on equity rises up to a point. But as the risk increases

13-8 Facts as given: Current capital structure: 25% debt, 75% equity; rRF = 4%; rM – rRF = 5%;

T = 25%; rs = 12%.

Step 1: Determine the firm’s current beta.

rs = rRF + (rM – rRF)b

372

Answers and Solutions

Chapter 13: Capital Structure and Leverage

Step 2: Determine the firm’s unlevered beta, bU.

bU = bL/[1 + (1 – T)(D/E)]

Step 3: Determine the firm’s beta under the new capital structure.

bL = bU[1 + (1 – T)(D/E)]

= 1.92.

Step 4: Determine the firm’s new cost of equity under the changed capital structure.

rs = rRF + (rM – rRF)b

13-9 a. Dividends = 0.4 × $1,000,000 = $400,000. So, the current dividend per share, D0, =

b. Step 1: Calculate EBIT before the recapitalization:

EBIT = $1,000,000/(1 – T) = $1,000,000/0.75 = $1,333,333.

Note: The firm is 100% equity financed, so there is no interest expense.

13-10 a. Firm A

1. Fixed costs = $80,000.

Chapter 13: Capital Structure and Leverage

Answers and Solutions

373

Firm B

1. Fixed costs = $120,000.

sales even–Break

$240,000

b. Firm B has the higher operating leverage due to its larger amount of fixed costs.

c. Operating profit = (Selling price)(Units sold) – Fixed costs – (Variable costs/unit)(Units sold).

Check:

13-11 a. Using the standard formula for the weighted average cost of capital, we find:

b. The firm’s current levered beta at 25% debt can be found using the CAPM formula.

374

Answers and Solutions

Chapter 13: Capital Structure and Leverage

c. To “unlever” the firm’s beta, the Hamada equation is used.

bL = bU[1 + (1 – T)(D/E)]

d. To determine the firm’s new cost of common equity, one must find the firm’s new beta under

its new capital structure. Consequently, you must “relever” the firm‘s beta using the Hamada

equation:

The firm’s cost of equity, as stated in the problem, is derived using the CAPM equation.

rs = rRF + (rM – rRF)b

e. Again, the standard formula for the weighted average cost of capital is used. Remember, the

WACC is a marginal, after-tax cost of capital and hence the relevant before-tax cost of debt is

now 10.5% and the cost of equity is 16.20%.

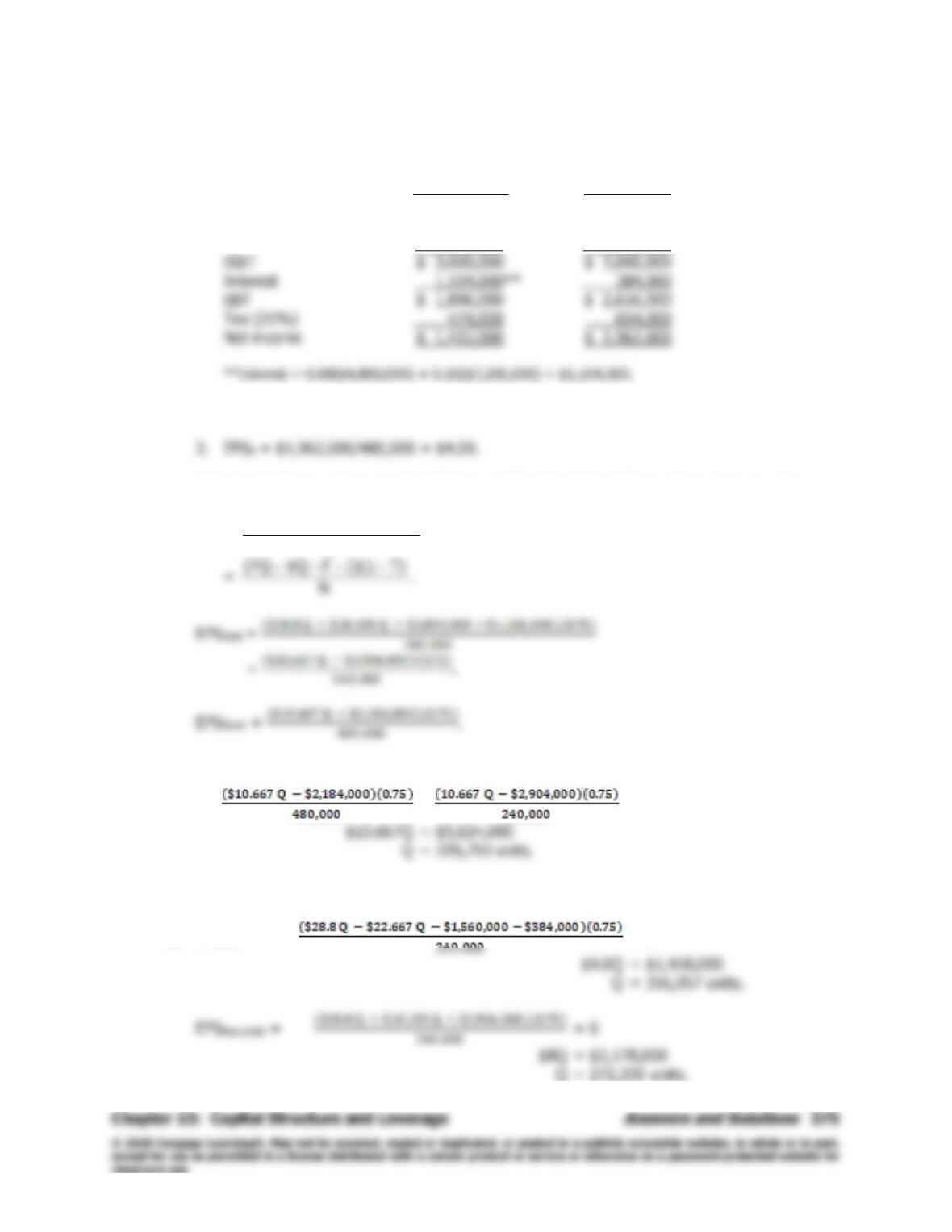

13-12 a. Without new investment:

Sales $12,960,000 ($28.80 × 450,000 units)

VC 10,200,000 (Given in problem)

1. EPSOld = $612,000/240,000 = $2.55.

With new investment:

Debt Stock

Sales $12,960,000 $12,960,000

VC (0.8)($10,200,000) 8,160,000 8,160,000

FC 1,800,000 1,800,000

2. EPSD = $1,422,000/240,000 = $5.93.

EPS should improve, but expected EPS is significantly higher if financial leverage is used.

b. EPS =

N

T) I)(1 F VC (Sales −−−−

Therefore,

=

This is the “indifference” sales level, where EPSdebt = EPSstock.

c. EPSOld = = 0

376

Answers and Solutions

Chapter 13: Capital Structure and Leverage

d. At the expected sales level, 450,000 units, we have these EPS values:

EPSOld Setup = $2.55. EPSNew,Debt = $5.93. EPSNew,Stock = $4.09.

Chapter 13: Capital Structure and Leverage

Answers and Solutions

377

13–13 Use of debt (millions of dollars):

Probability 0.3 0.4 0.3

Sales $2,250.00 $2,700.00 $3,150.00

EBIT (15% of sales) 337.50 405.00 472.50

Interest* 83.63 83.63 83.63

*Interest on debt = ($270 0.09) + Current interest expense

= $24.30 + $59.33 = $83.63.

Standard deviation of EPS if debt financing is used:

Use of stock (millions of dollars):

Probability 0.3 0.4 0.3

Sales $2,250.00 $2,700.00 $3,150.00

capital Total

Debt

=

270$50.397$50.697$00.255$

50.697$ + 00.255$

+++

=

00.620,1$

50.952$

= 58.8%.

Under debt financing the expected EPS is $4.02, the standard deviation is $0.65, the CV is 0.16,

and the debt-to-capital ratio increases to 75.5%. (The debt-to-capital ratio had been 70.6%.)

Chapter 13: Capital Structure and Leverage

Comprehensive/Spreadsheet Problem

379

Comprehensive/Spreadsheet Problem

Note to Instructors:

The solution to this problem is not provided to students at the back of their text. Instructors

can access the

Excel

file on the textbook’s website.

13–14 Tax rate = 25%; rRF = 5.0%; bU = 1.2; rM – rRF = 6.0%

Levered

wd wc D/E rd rd(1 – T) betaa rsb WACCc

0.20 0.80 0.2500 8.00 6.00 1.43 13.55 12.04

0.60 0.40 1.5000 12.00 9.00 2.55 20.30 13.52

Notes:

a These beta estimates were calculated using the Hamada equation, bL = bU[1 + (1 – T)(D/E)].

b These rs estimates were calculated using the CAPM, rs = rRF + (rM – rRF)b.

380

Comprehensive/Spreadsheet Problem

Chapter 13: Capital Structure and Leverage

d.

25%

30%

35%

40%

0% 20% 40% 60% 80% 100%

Capital Costs Vs. D/(D+E)

rs

25%

30%

35%

40%

0.00 1.00 2.00 3.00 4.00

Capital Costs Vs. D/E

rs

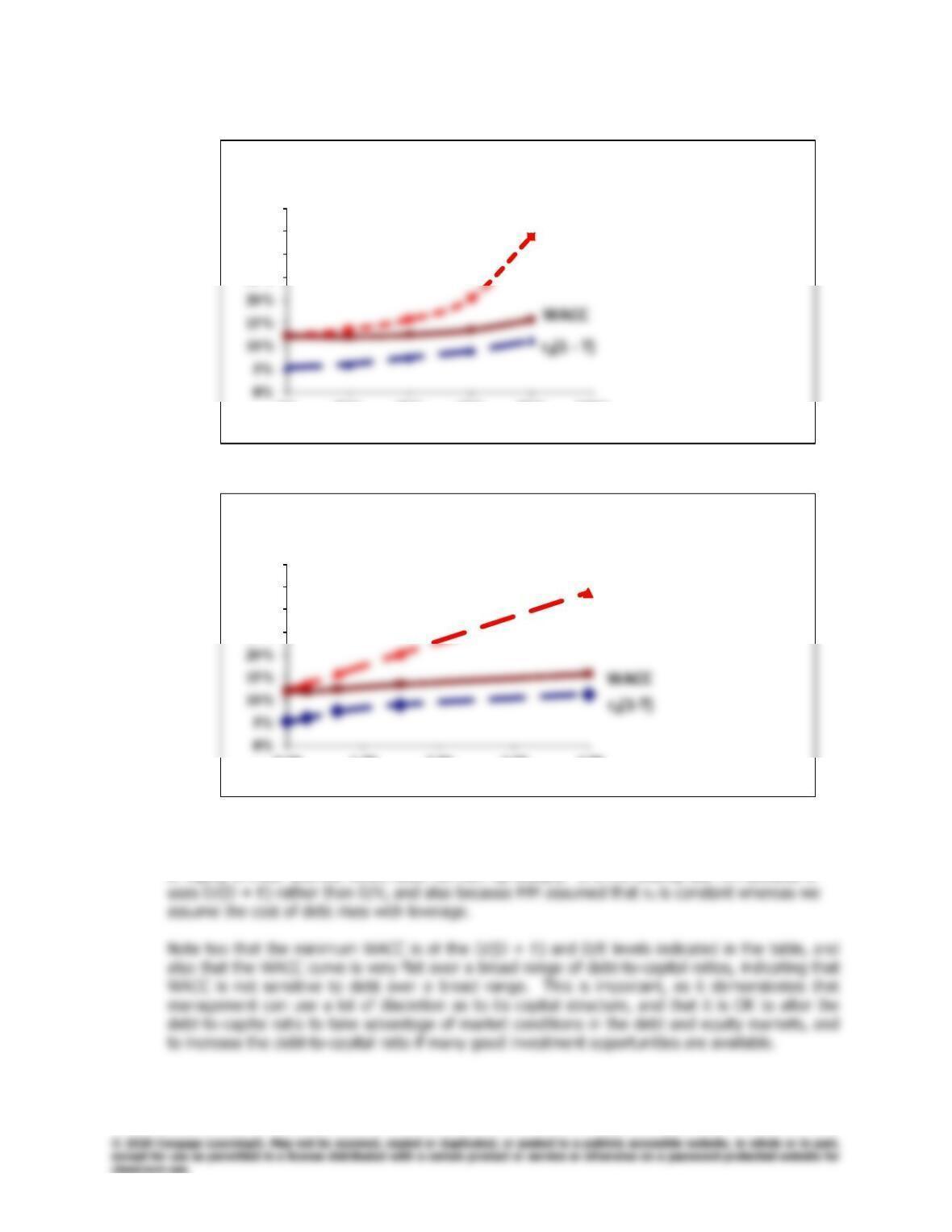

The top graph is like the one in the textbook, because it uses the D/(D +E) ratio on the

horizontal axis. The bottom graph is a bit like MM showed in their original article in that the cost

of equity is linear and the WACC does not turn up sharply. It is not exactly like MM because it

13-15

Campus Deli Inc.

Optimal Capital Structure

Assume that you have just been hired as business manager of Campus Deli

(CD), which is located adjacent to the campus. Sales were $1,100,000 last

year, variable costs were 60% of sales, and fixed costs were $40,000.

CD currently has no debt—it is an all-equity firm—and its 80,000 shares

outstanding sell at a price of $25 per share, which is also the book value.

The firm’s federal-plus-state tax rate is 25%. On the basis of statements

In today’s market, the risk-free rate, rRF, is 7.5%, and the market risk

premium, RPM, is 6%. CD’s unlevered beta, bU, is 1.25. CD currently has no

debt, so its cost of equity (and WACC) is 15%. If the firm was recapitalized,