Chapter 13

Macroeconomic Policy and Aggregate

Demand and Supply Analysis

◼ Chapter Outline, Overview, and Teaching Tips

Chapter Outline

The Objectives of Macroeconomic Policy

Stabilizing Economic Activity

Establishing Hierarchical Versus Dual Mandates

The Relationship Between Stabilizing Inflation and Stabilizing Economic Activity

Monetary Policy and the Equilibrium Real Interest Rate

Policy and Practice: The Federal Reserve’s Use of the Equilibrium Real Interest Rate, r*

Response to an Aggregate Demand Shock

How Actively Should Policy Makers Try to Stabilize Economic Activity?

Lags and Policy Implementation

Policy and Practice: The Activist/Nonactivist Debate Over the Obama Fiscal Stimulus Package

The Taylor Rule

The Taylor Rule Equation

Policy and Practice: The Fed’s Use of the Taylor Rule

Inflation: Always and Everywhere a Monetary Phenomenon

Causes of Inflationary Monetary Policy

High Employment Targets and Inflation

Chapter 13 Macroeconomic Policy and Aggregate Demand and Supply Analysis 137

Quantitative Easing Versus Credit Easing

Management of Expectations

Policy and Practice: Abenomics and the Shift in Japanese Monetary Policy in 2013

Chapter Overview and Teaching Tips

Chapter 13 shifts the perspective by bringing a new set of actors into the AD/AS framework: policy

makers. We look at how they react to shocks to the economy in order to stabilize both inflation and economic

For students to understand what policy makers do, they first need to understand what the objectives of

policy makers are, which is the first issue discussed in the chapter. Once they understand that policy

makers focus on two objectives, stabilizing economic activity and stabilizing inflation (price stability), the

next step is to see how policy makers respond to shocks to aggregate demand or aggregate supply to

achieve these objectives. The analysis in the chapter makes clear that stabilizing inflation stabilizes

economic activity, so there is no policy tradeoff, only when there are shocks to aggregate demand or

permanent shocks to aggregate supply. On the other hand, temporary shocks to aggregate supply do

involve a policy tradeoff because in this case stabilizing inflation does not stabilize economic activity.

The next section of the chapter discusses one of the most famous adages in macroeconomics, coined by

Milton Friedman: “Inflation is always and everywhere a monetary phenomenon.” Although this phrase was

discussed in Chapter 5 in a long-run context, it is important to show that it is also valid in the AD/AS

framework because the monetary authorities do have the ability to control inflation. If inflation is a monetary

phenomenon, there is still an issue as to why monetary policy makers allow it to happen. The AD/AS model

shows that overly expansionary monetary policy that leads to high inflation can occur when the policy makers

try to achieve high employment targets. The application on the Great Inflation shows students that this is not

just a theoretical possibility but actually occurred from the late 1960s to the early 1980s.

138 Mishkin • Macroeconomics: Policy and Practice, Second Edition

◼ Answers to End of Chapter Review Questions and Problems

Answers to Review Questions

The Objectives of Monetary Policy

1. Stabilizing economic activity and price stability are the two primary objectives of macroeconomic

stabilization policy. Stabilizing economic activity requires keeping unemployment at the natural rate

2. Policy makers should not strive to achieve zero rates of unemployment and inflation. Even at full

employment, unemployment is not zero because of the existence of frictional and structural

unemployment. Frictional unemployment is beneficial to the economy as it arises from the search

3. A hierarchical mandate gives top priority to the objective of price stability. Under this mandate,

policy makers may pursue the goal of stabilizing economic activity only if it does not compromise

The Relationship Between Stabilizing Inflation and Stabilizing Economic Activity

4. The equilibrium real interest rate is the real interest rate that keeps the quantity of aggregate output

demanded equal to potential output. Thus, it keeps the economy in long-run equilibrium and the

5. Stabilization policy is conducted more frequently using monetary policy rather than fiscal policy

6. The divine coincidence exists when policies that are appropriate to achieve price stability also

stabilize economic activity. When it prevails, policy makers have easier jobs because there is no

tradeoff between policy objectives and they do not have to choose between them. They can, in other

words, have their cake and eat it, too. The divine coincidence prevails when the economy is beset

Chapter 13 Macroeconomic Policy and Aggregate Demand and Supply Analysis 139

How Actively Should Policy Makers Try to Stabilize Economic Activity?

7. Activists see the process of price and wage adjustments that move the economy to long-run

equilibrium as working very slowly. They argue that instead of waiting for these slow adjustments to

8. Activists argue that wages are inflexible and, in particular, that they are not likely to fall as would be

needed for the self-correcting mechanism to adjust to long-run equilibrium if the economy suffers

9. The data lag is the time it takes to collect and process the quarterly, monthly, and other data that tell

policy makers how well or poorly the economy is performing. The recognition lag is the time

policymakers may wait for additional data to come in to be more confident of their interpretations of

The Taylor Rule

10. The Taylor rule advises the Fed to raise the real federal funds rate target when the inflation gap or the

output gap rises, and to lower this target rate when those gaps shrink. Inasmuch as it recommends

11. There are a number of reasons why this would not be a good idea. There is no guarantee that the

Taylor rule coefficients are stable across time and no one, policy makers included, knows the size of

inflation and output gaps at any given time. Even if policy makers did have accurate information

140 Mishkin • Macroeconomics: Policy and Practice, Second Edition

Inflation: Always and Everywhere a Monetary Phenomenon

12. Monetary policy makers can target any inflation rate they want to simply by implementing autonomous

monetary policy easing (to target a higher inflation rate) or tightening (to target a lower one). However,

Causes of Inflationary Monetary Policy

13. Cost-push and demand-pull inflation result when policy makers in pursuit of high targets for output

and employment (and hence low targets for the unemployment rate) implement policies that raise

aggregate demand when their targets are not met. The two types of inflation both arise from events

that move the economy away from long-run equilibrium, but their initiating causes differ. Cost-push

inflation starts with temporary negative supply shocks or wage increases in excess of productivity

Monetary Policy at the Zero Lower Bound

14. When the zero lower bound is hit, a lower inflation rate leads to a higher real interest rate because the

15. A negative output gap leads to a fall in the short-run aggregate supply curve, which lowers inflation,

16. All unconventional policies work by lowering the interest rate for investments and so stimulate

investment spending and shift the aggregate demand curve to the right. Liquidity provision helps to

heal impaired financial markets, thereby lowering financial frictions and, hence, the real interest rate

Chapter 13 Macroeconomic Policy and Aggregate Demand and Supply Analysis 141

Answers to Problems

The Objectives of Macroeconomic Policy

1. a. According to Section 8 of the Reserve Bank of New Zealand Act of 1989, the Central Bank of

New Zealand has a clear hierarchical mandate to achieve low and stable inflation. The idea

The Relationship Between Stabilizing Inflation and Stabilizing Economic Activity

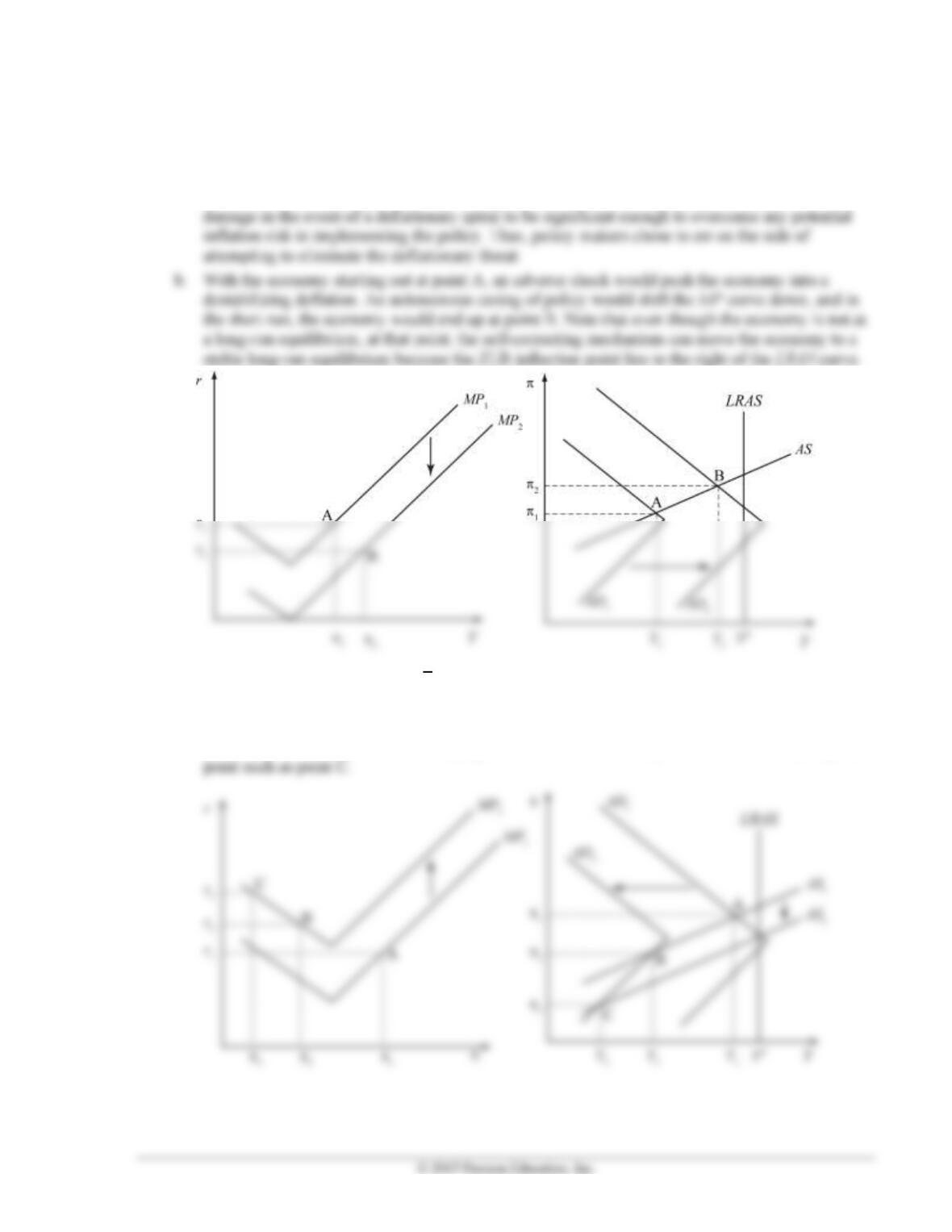

2. a. According to aggregate demand and supply analysis, the decrease in government expenditures

results in a shift to the left in the aggregate demand curve, as aggregate expenditure decreases at

every inflation rate. As a result, the new intersection point with the short-run aggregate supply

3. According to aggregate supply and demand analysis, a less efficient economy will end up in a new

long-run equilibrium at a lower level of output. Depending on the monetary policy response, the

inflation rate might be higher than before the implementation of reforms that made the economy less

4. a. Changes described by data suggest that policy makers decided to stabilize inflation in the short

run, with the corresponding decrease in output, during period 3.

b. Labeled arrows in the graph refer to the table time periods.

142 Mishkin • Macroeconomics: Policy and Practice, Second Edition

How Actively Should Policy Makers Try to Stabilize Economic Activity?

5. Evidence that shows that the welfare gains from stabilizing output and unemployment are relatively

small, which supports the nonactivist case. This is actually a major topic in macroeconomics, which

6. In panel (A) the short-run aggregate supply curve has a steeper slope, meaning that wages and prices

The Taylor Rule

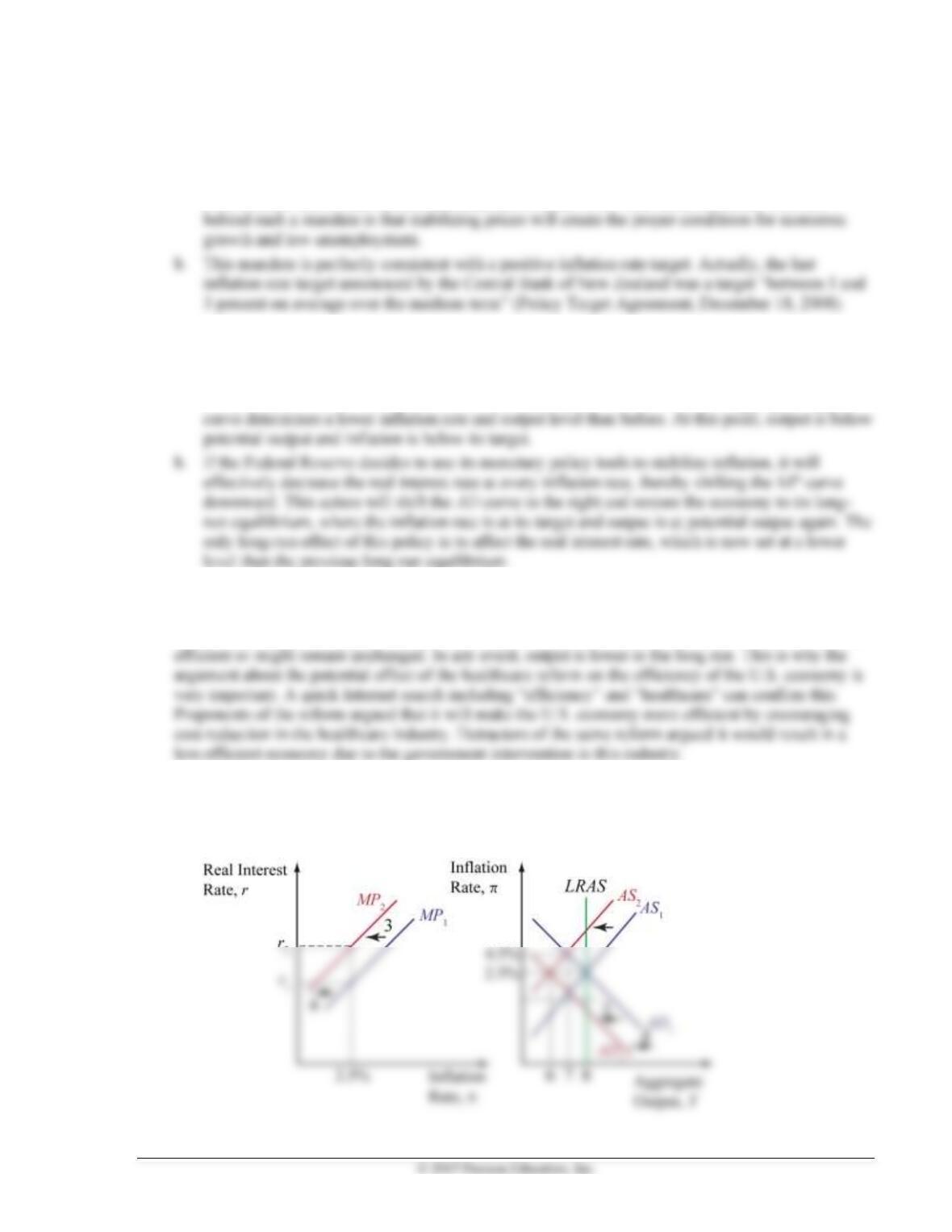

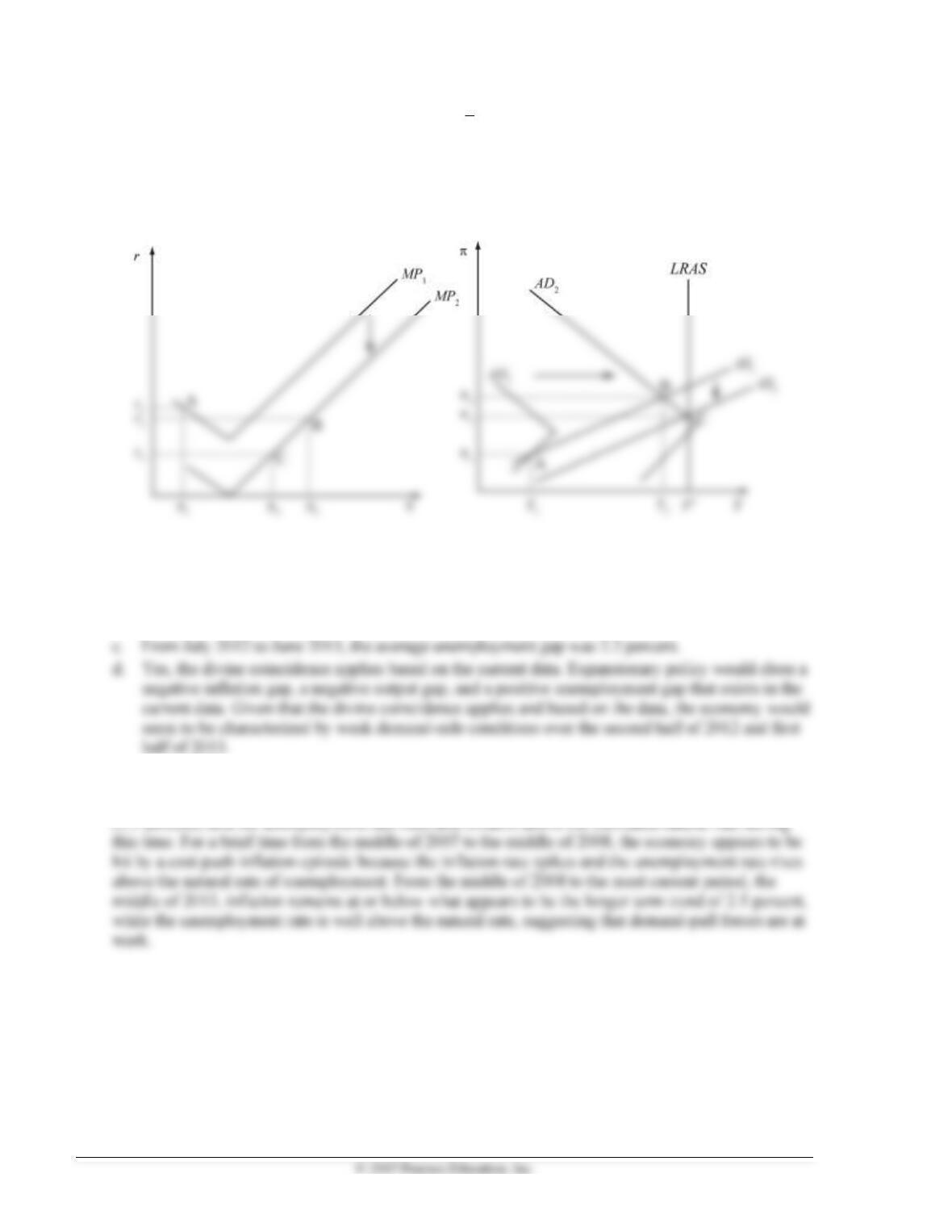

7.

a.

The decline in potential output shifts the LRAS

curve to the left. The lower potential output

increases the output gap, prompting an

autonomous tightening of policy and a shift of

the MP curve to MP2. In the short-run, the

Chapter 13 Macroeconomic Policy and Aggregate Demand and Supply Analysis 143

b. A decline in the target inflation rate increases the inflation gap, prompting an increase in the real

interest rate and shift upwards in the MP curve to MP2. As a result of the autonomous tightening

policy, aggregate demand decreases to AD2, and the economy is in recession at point B in the

short run. The self-correcting mechanism will result in a decline in the AS curve to AS3 until the

economy reaches the new long-run equilibrium at point C. In the long-run, the economy will

have permanently lower inflation with the real interest rate and output unchanged.

144 Mishkin • Macroeconomics: Policy and Practice, Second Edition

Causes of Inflationary Monetary Policy

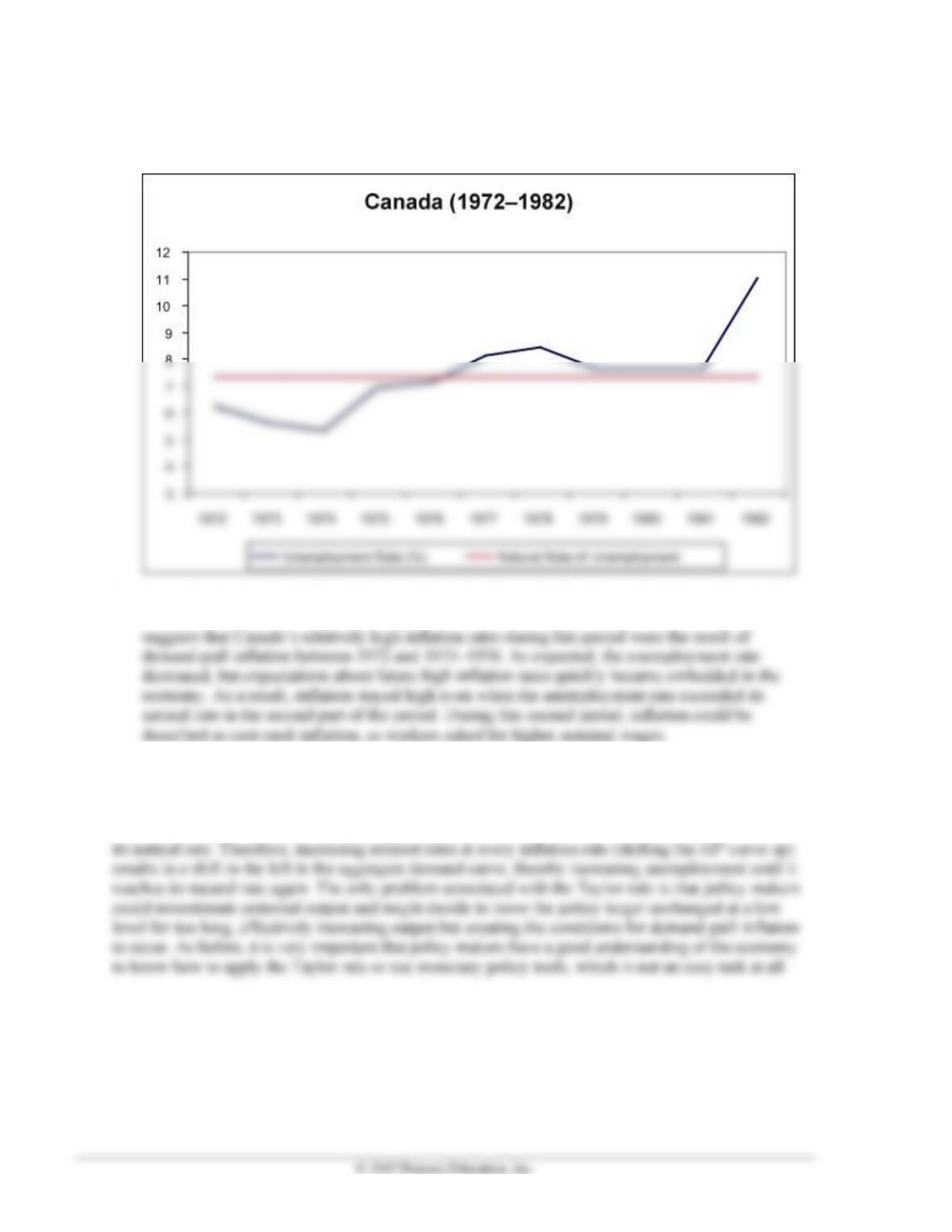

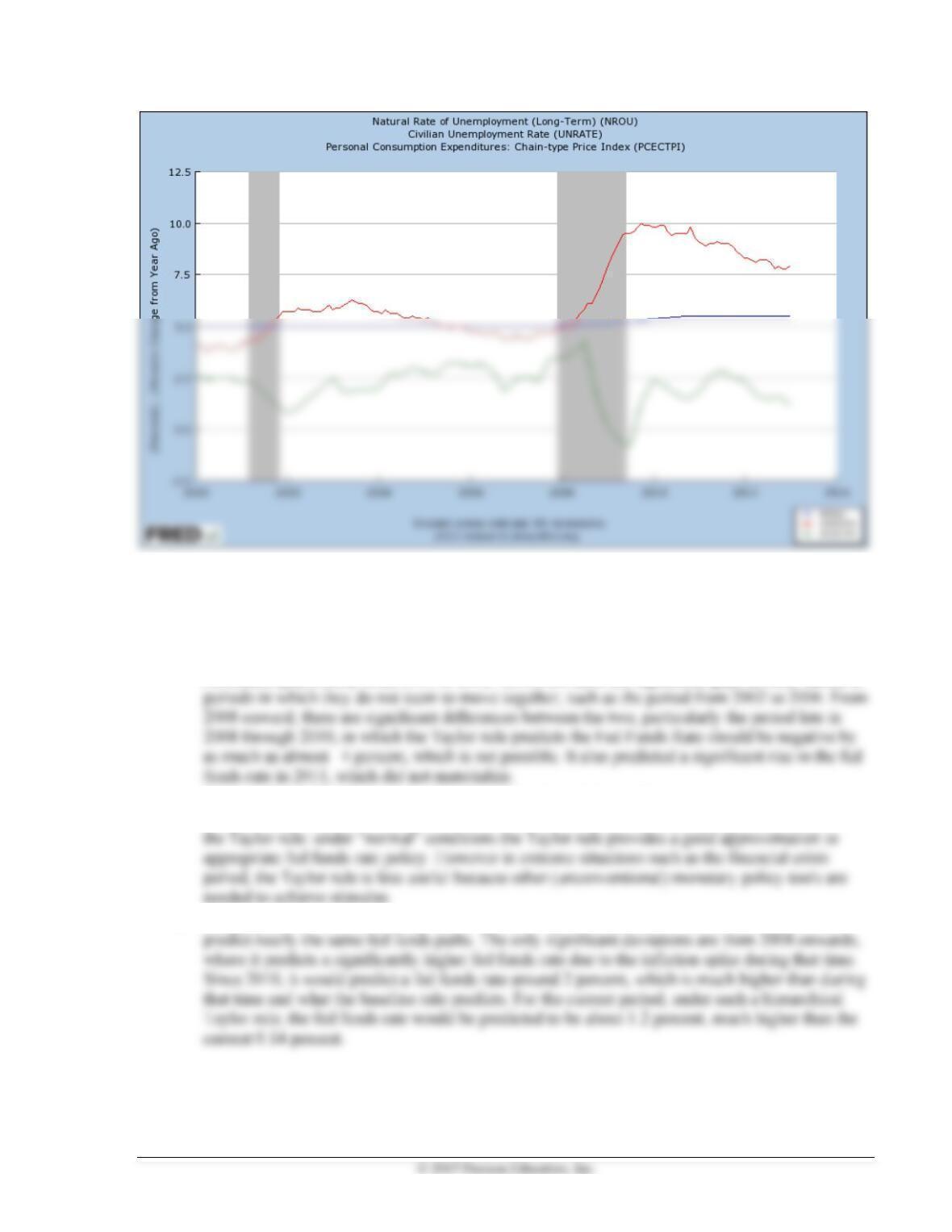

8. a.

b. According to the graph, Canada’s unemployment rate was below the estimated natural rate of

unemployment for the first part of the period, and then it was above the natural rate. This

9. The Taylor rule suggests that the policy rate target should be increased when the output gap is

positive. This rule is perfectly consistent with avoiding demand-pull inflation. The natural rate of

unemployment is the unemployment rate at which output is at its potential level. A positive output

gap means that the economy is producing more output, a situation in which unemployment is below

Chapter 13 Macroeconomic Policy and Aggregate Demand and Supply Analysis 145

Monetary Policy at the Zero Lower Bound

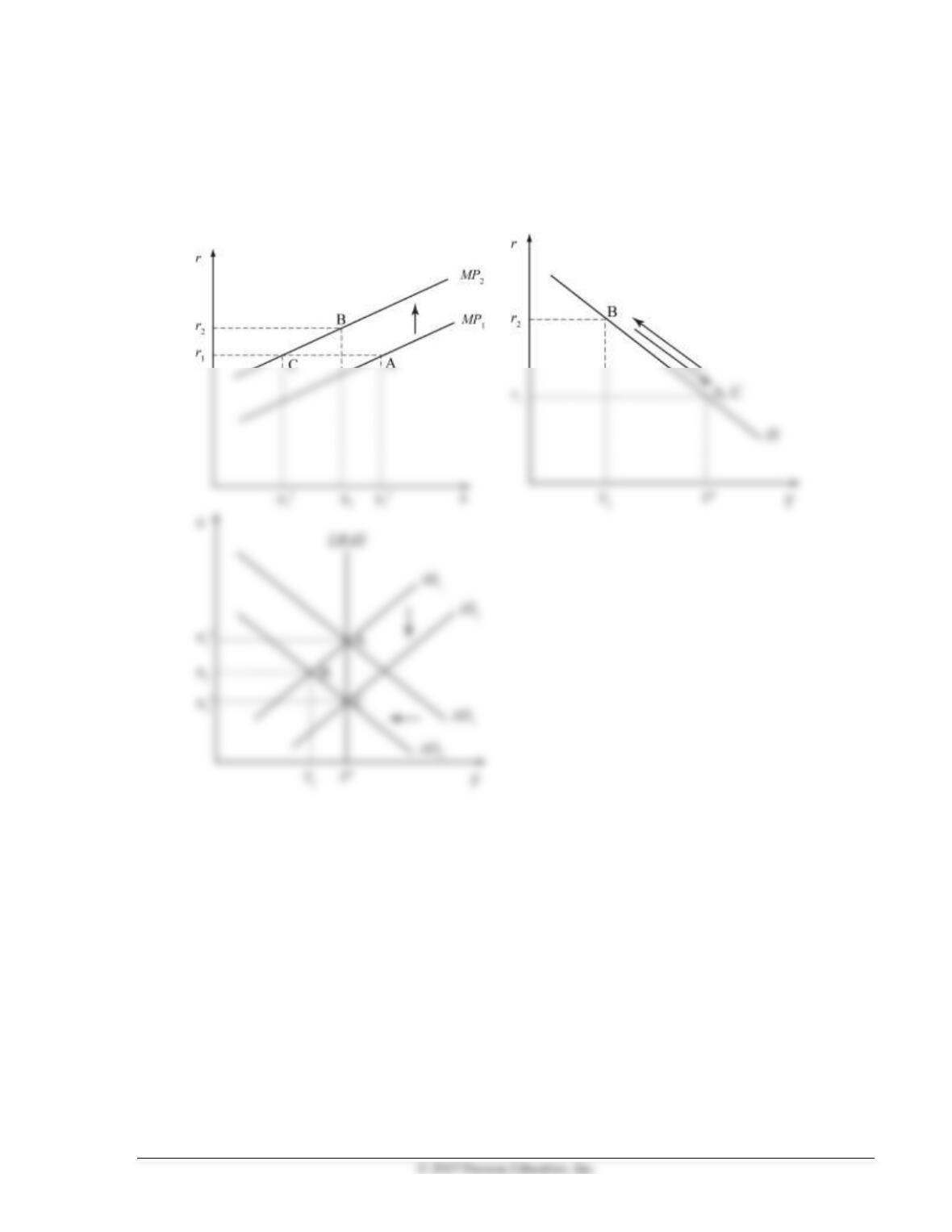

10. a. Policy makers were worried that a shock could push the economy into a deflationary spiral, in

which the short-term nominal policy rate would be bound at the zero lower bound. At that point,

conventional monetary policy would be ineffective. Policy makers viewed the risk of economic

11. a. A financial panic will increase

f

, thus raising the real interest rate on investments at any given

inflation rate. A sufficiently large panic will push the economy to point B, where the self-

correcting mechanism will lower inflation, and real rates will rise because the economy is beyond

the ZLB. This results in a deflationary spiral in which the economy will move toward (and past) a

146 Mishkin • Macroeconomics: Policy and Practice, Second Edition

b. A sufficient enough asset purchase will lower

f

, reversing the effects of the panic, and lower

the real interest rate on investments at any given inflation rate. This moves the economy from

point A to a point such as point B, where the economy is no longer at risk of a deflationary spiral.

At point B, the self-correcting mechanism can move the economy to a stable, long-run

equilibrium because the ZLB inflection point lies to the right of the LRAS curve along that AD

curve.

◼ Answers to Data Analysis Problems

1. a. From 2012:Q2: 2013:Q1, the average inflation gap was –0.5 percent.

b. From 2012:Q2: 2013:Q1, the average output gap was –5.7 percent.

2. The period from around early 2001 to around the end of 2003 appears to be influenced by demand-

pull inflation conditions because inflation is a bit lower than what appears to be normal at the time

Chapter 13 Macroeconomic Policy and Aggregate Demand and Supply Analysis 147

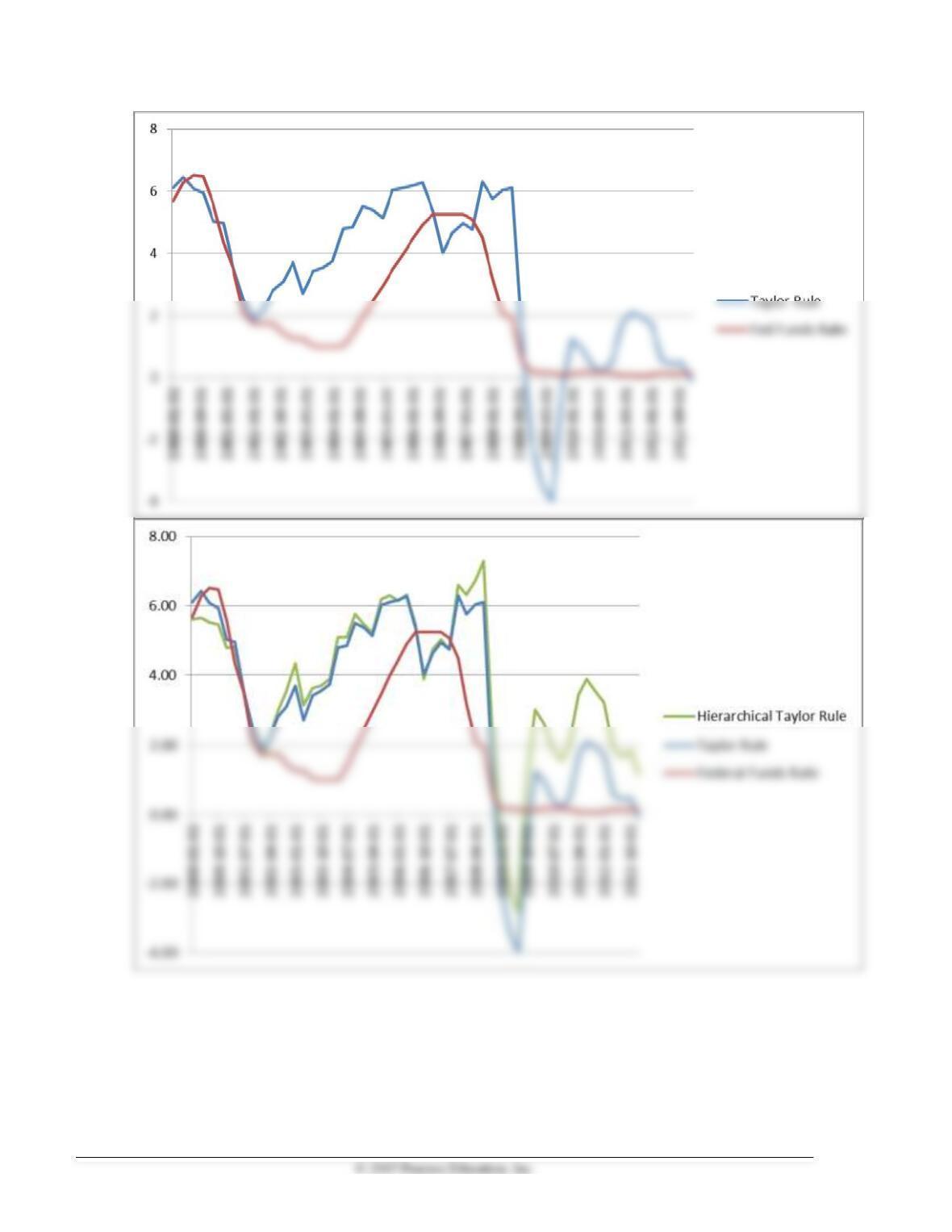

a. For the most recent period in 2013:Q1, the Fed Funds Rate is 0.14 percent, while the Taylor Rule

predicts a slightly negative –0.07 percent, representing a gap of 0.21 percent. Compared to other

significant deviations, this seems to be a fairly close correspondence, although the negative value

is not possible in practice.

b. See graph below. The Taylor rule since 2000 has periods in which they are fairly closely

correlated, particularly from 2000 to 2002. However, there are significant gaps in other times, or

c. Because the Fed funds rate was at the zero lower bound during that time, conventional monetary

policy through adjustments in the fed funds rate was not possible, and highlights a limitation of

d. See graph below. For the most part, the baseline Taylor rule and the hierarchical Taylor rule

148 Mishkin • Macroeconomics: Policy and Practice, Second Edition

Chapter 13 Macroeconomic Policy and Aggregate Demand and Supply Analysis 149

◼ Data Sources, Related Articles, and Discussion Questions

A. For Information About Policy and Practice: The Federal Reserve’s Use of

the Equilibrium Real Interest Rate, r*

Data Source

page you can access previous blue and green books. There are also short descriptions of these publications.

Related Article

Federal Reserve System: FOMC Transcripts and Other Historical Materials, 2004.

Discussion Question

Suppose a new wave of technological innovation shifts the long-run aggregate supply curve to the right.

Everything else the same, what would be the effect on the equilibrium level of the real interest rate?

Answer: According to the aggregate demand and supply model, a permanent shift to the right on the long-

B. For Information About Policy and Practice: The Activist/Nonactivist Debate

Over the Obama Fiscal Stimulus Package

Data Source

about the American Recovery and Reinvestment Act of 2009, including how and when the stimulus

money was spent.

Related Article

discontent that the stimulus package of 2009 created among many U.S. economists.

Discussion Question

Explain why some economists suggest that a stimulus plan could have no effect on the economy.

Answer: Some economists argue that the increase in government spending (or the decrease in taxes) will

150 Mishkin • Macroeconomics: Policy and Practice, Second Edition

C. For Information About Policy and Practice: The Fed’s Use of the Taylor Rule

Data Source

Federal Reserve Bank of Dallas: “Measuring the Taylor’s Rule Performance”:

Related Article

Walsh, Carl E. “The Science (and Art) of Monetary Policy”:

Discussion Question

Suppose that current conditions determine a positive inflation gap but with a negative output gap (also

known as “stagflation”). What would the Taylor rule suggest to with the federal funds rate?

Answer: From an empirical point of view, one would have to measure the magnitude of the inflation and

D. For Information About Application: The Great Inflation

Data Source

Related Article

Meltzer, Allan A., “Origins of the Great Inflation”:

Discussion Question

Suppose somebody in charge of advising the president on economic topics suggests that the U.S.

government should enact policy measures to reach a 2 percent unemployment rate. Would you agree with

such a recommendation?

Answer: In light of the experience of the Great Inflation, this would be a great mistake. Trying to reach such a

E. For Information About Application: Nonconventional Monetary Policy and

Quantitative Easing

Data Source

Federal Reserve Bank of St. Louis database (FRED):

Chapter 13 Macroeconomic Policy and Aggregate Demand and Supply Analysis 151

Related Article

Federal Reserve System: “Monetary Policy Report”:

Discussion Question

The Federal Reserve System is a central bank that has a good reputation as an inflation fighter. How do you

think this good reputation might not work in the best interests of the Federal Reserve in the context of

nonconventional monetary policy?

Answer: Quite paradoxically, in the context of a management of expectations strategy, to be a central bank

F. For Information About Policy and Practice: Abenomics and the Shift in

Japanese Monetary Policy

Data Source

Federal Reserve Bank of St. Louis database (FRED):

Related Article

arrow-reform-has-fallen-well-short-its-target-time-shinzo-abe-rethink-not. In this article you can find a

description of “Abenomics” in its first steps and the controversy that ensued about its efficacy.

Discussion Question

The central banks of both Japan and the United States tried to increase inflation expectations in the context of

nonconventional monetary policy. What do you think the risk of increasing inflation expectations for a central

bank is?

Answer: In the context of nonconventional monetary policy, increasing inflation expectations might work