Chapter 8: Risk and Rates of Return

Integrated Case

207

tax–exempt bonds, they would be truly riskless, but all actual

securities are exposed to some type of risk.

A. (2) Why are High Tech’s returns expected to move with the economy,

whereas Collections’ are expected to move counter to the economy?

Answer: [Show S8-8 here.] High Tech’s returns move with, hence are

positively correlated with, the economy, because the firm’s sales, and

hence profits, will generally experience the same type of ups and

downs as the economy. If the economy is booming, so will High Tech.

B. Calculate the expected rate of return on each alternative, and fill in

the blanks on the row for

r

ˆ

in the previous table.

Answer: [Show S8-9 and S8–10 here.] The expected rate of return,

r

ˆ

, is

expressed as follows:

=

=

N

1i

iirPr

ˆ

.

Here Pi is the probability of occurrence of the ith state, ri is the

estimated rate of return for that state of the economy, and N is the

r

ˆ

208

Integrated Case

Chapter 8: Risk and Rates of Return

We use the same formula to calculate

r

ˆ

’s for the other alternatives:

r

ˆ

T–bills = 3.0%.

r

ˆ

Collections = 1.2%.

r

ˆ

C. You should recognize that basing a decision solely on expected

(1) Calculate this value for each alternative and fill in the blank on the

row for in the table.

Answer: [Show S8-11 and S8-12 here.] The standard deviation is calculated as

follows:

=

=

−

N

1i

i

2

iP)r

ˆ

r(

.

Here are the standard deviations for the other alternatives:

T–bills = 0.0%.

Chapter 8: Risk and Rates of Return

Integrated Case

209

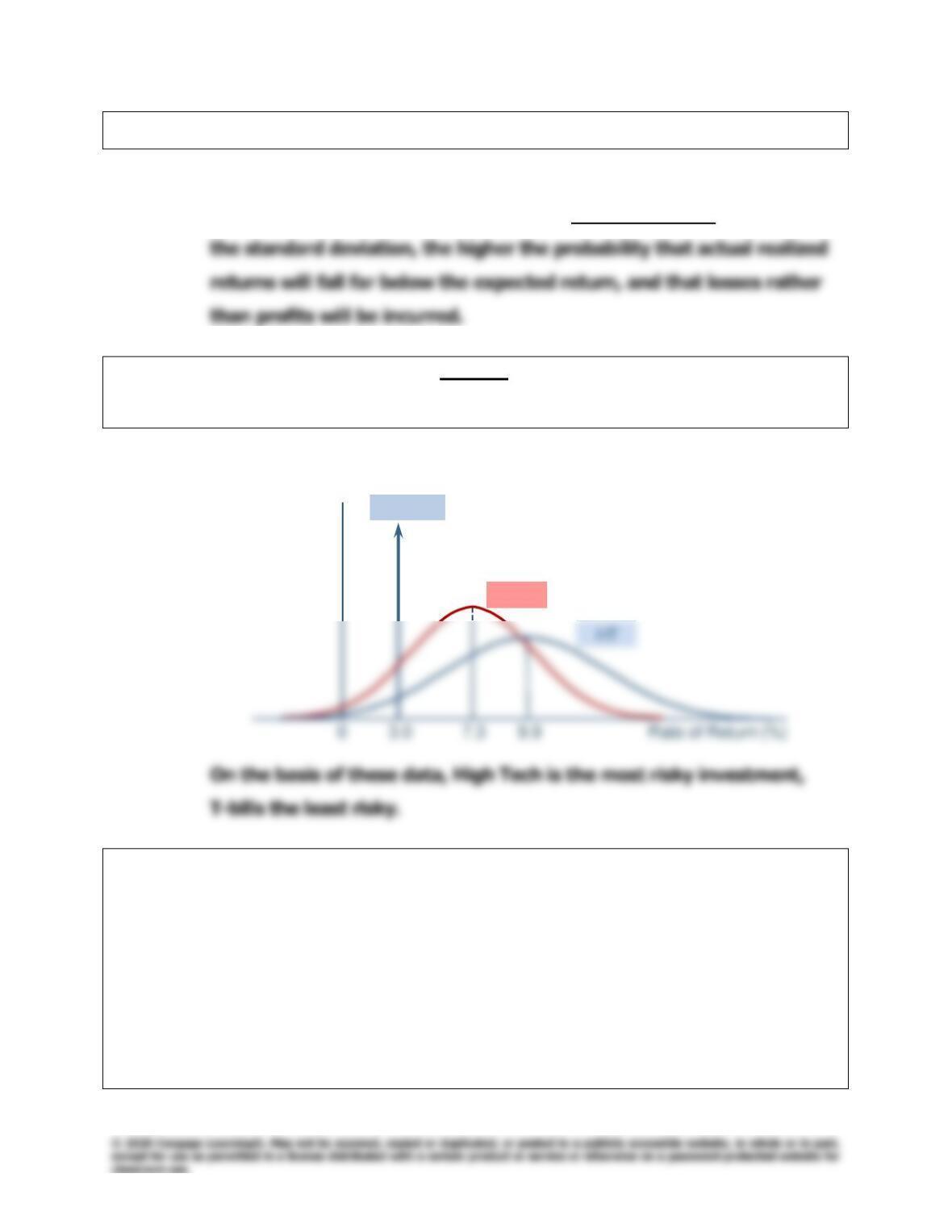

C. (2) What type of risk is measured by the standard deviation?

Answer: [Show S8-13 through S8-15 here.] The standard deviation is a

measure of a security’s (or a portfolio’s) stand-alone risk. The larger

C. (3) Draw a graph that shows roughly the shape of the probability

distributions for High Tech, U.S. Rubber, and T-bills.

Answer:

USR

Prob.

T-bills

D. Suppose you suddenly remembered that the coefficient of variation

(CV) is generally regarded as being a better measure of stand-alone

risk than the standard deviation when the alternatives being

considered have widely differing expected returns. Calculate the

missing CVs, and fill in the blanks on the row for CV in the table.

Does the CV produce the same risk rankings as the standard

deviation? Explain.

210

Integrated Case

Chapter 8: Risk and Rates of Return

Answer: [Show S8-16 through S8-18 here.] The coefficient of variation (CV) is

a standardized measure of dispersion about the expected value; it

shows the amount of risk per unit of return.

CV = /

r

ˆ

.

CVT–bills = 0.0%/3.0% = 0.0.

CVM = 15.2%/8.0% = 1.9.

r

E. Someone mentioned that you might also want to calculate the Sharpe

ratio as a measure of stand-alone risk. Calculate the missing ratios

and fill in the blanks on the row for the Sharpe ratio in the table.

Briefly explain what the Sharpe ratio actually measures.

Answer: [Show S8-19 here.] The Sharpe ratio is a measure of stand-alone

risk that compares the asset’s realized excess return to its standard

deviation over a specified period. An investment with a higher ratio

Chapter 8: Risk and Rates of Return

Integrated Case

211

The Sharpe ratio has already been provided for Collections. It is

calculated follows:

Collections’ Sharpe ratio = (1.2% – 3%)/11.2% = -0.161

F. Suppose you created a two–stock portfolio by investing $50,000 in

High Tech and $50,000 in Collections.

(1) Calculate the expected return (

p

r

ˆ

), the standard deviation (p), and

the coefficient of variation (CVp), and the Sharpe ratio for this

portfolio and fill in the appropriate blanks in the table.

Answer: [Show S8-20 through S8-25 here.] To find the expected rate of return

on the two-stock portfolio, we first calculate the rate of return on the

212

Integrated Case

Chapter 8: Risk and Rates of Return

rp = 0.5(-29.5%) + 0.5(24.5%) = –2.5%. We would do similar

calculations for the other states of the economy, and obtain these

results:

State

Portfolio

Recession

–2.5%

Below average

Average

Above average

Now we can multiply the probability times the outcome in each state

of the economy to calculate the expected return on this two-stock

portfolio, 5.5%.

Alternatively, we could apply this formula,

It is tempting to find the standard deviation of the portfolio as

the weighted average of the standard deviations of the individual

securities, as follows:

However, this is not correct—it is necessary to use a different formula, the

one for that we used earlier, applied to the two–stock portfolio’s returns.

The portfolio’s depends jointly on (1) each security’s and (2)

p = [(-2.5 – 5.5)2(0.1) + (0.5 – 5.5)2(0.2) + (5.8 – 5.5)2(0.4)

F. (2) How does the riskiness of this two-stock portfolio compare with the

riskiness of the individual stocks if they were held in isolation?

Answer: [Show S8-26 through S8-29 here.] Using either or CV as our stand-

alone risk measure, the stand-alone risk of the portfolio is significantly

Optional Question

Does the expected rate of return on the portfolio depend on the percentage of

the portfolio invested in each stock? What about the riskiness of the portfolio?

Answer: Using a spreadsheet model, it’s easy to vary the composition of the

portfolio to show the effect on the portfolio’s expected rate of return

and standard deviation:

High Tech Plus Collections

% in High Tech

0% 1.2% 11.2%

20 2.9 5.1

40 4.7 1.7

60 6.4 7.6

p

r

ˆ

p

214

Integrated Case

Chapter 8: Risk and Rates of Return

70 7.3 10.7

90 9.0 16.9

100 9.9 20.0

The expected rate of return on the portfolio is merely a linear

combination of the two stock’s expected rates of return. However,

portfolio risk is another matter. p begins to fall as High Tech and

G. Suppose an investor starts with a portfolio consisting of one

randomly selected stock.

(1) What would happen to the riskiness and to the expected return of

the portfolio as more randomly selected stocks were added to the

portfolio?

Chapter 8: Risk and Rates of Return

Integrated Case

215

Answer: [Show S8-30 and S8-31 here.]

The standard deviation gets smaller as more stocks are combined in

the portfolio, while rp (the portfolio’s return) remains constant. Thus,

by adding stocks to your portfolio, which initially started as a 1-stock

portfolio, risk has been reduced.

216

Integrated Case

Chapter 8: Risk and Rates of Return

with an index such as the S&P 500 rather than holding all the stocks

in the index.)

H. (1) Should the effects of a portfolio impact the way investors think about

the riskiness of individual stocks?

Answer: [Show S8-32 here.] Portfolio diversification does affect investors’

views of risk. A stock’s stand–alone risk as measured by its , CV, or

the Sharpe ratio may be important to an undiversified investor, but it

H. (2) If you decided to hold a one–stock portfolio (and consequently were

exposed to more risk than diversified investors), could you expect to be

compensated for all of your risk; that is, could you earn a risk premium

on the part of your risk that you could have eliminated by diversifying?

Answer: [Show S8-33 here.] If you hold a one-stock portfolio, you will be

exposed to a high degree of risk, but you won’t be compensated for it.

Chapter 8: Risk and Rates of Return

Integrated Case

217

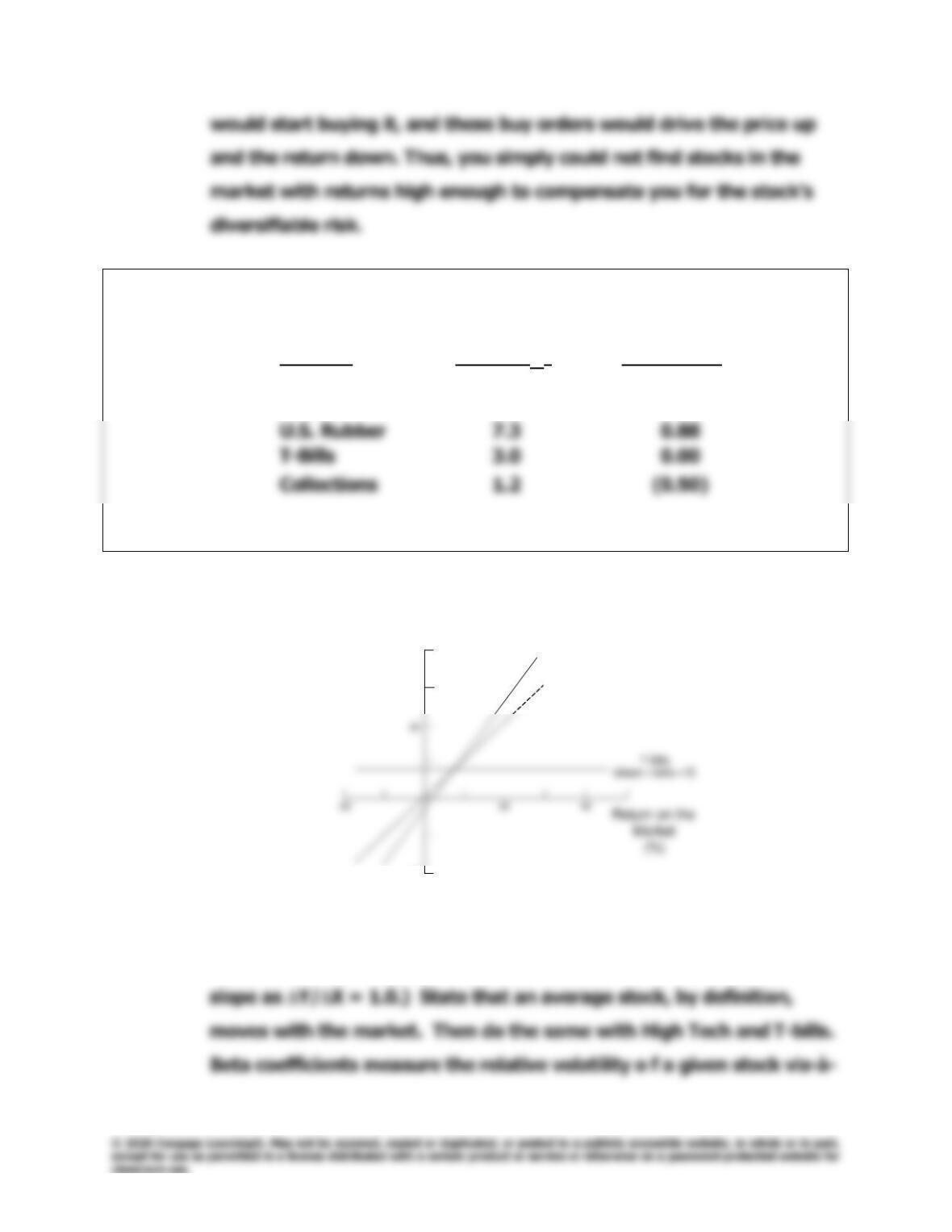

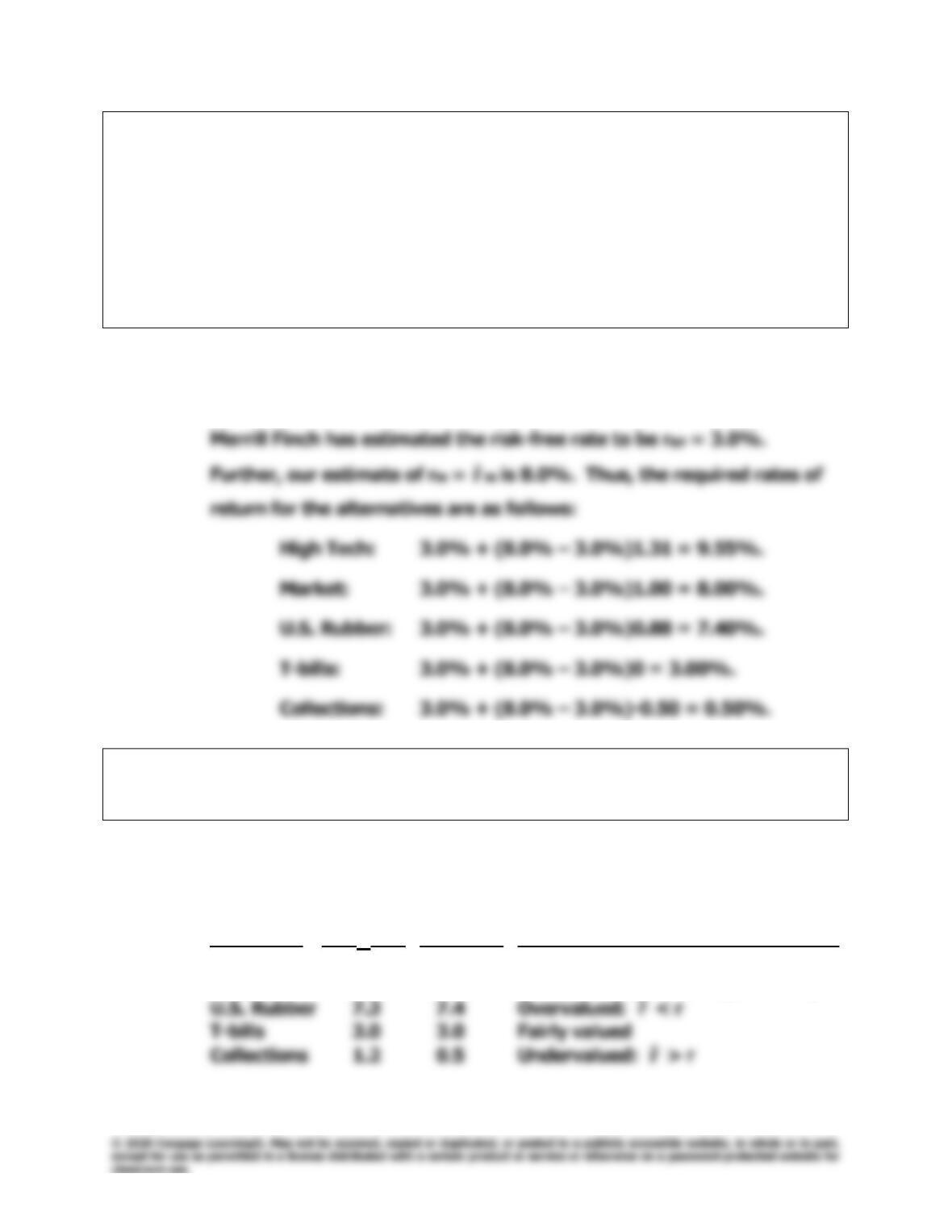

I. The expected rates of return and the beta coefficients of the alternatives

supplied by Merrill Finch’s computer program are as follows:

Security Return (

r

ˆ

) Risk (Beta)

High Tech 9.9% 1.31

Market 8.0 1.00

(1) What is a beta coefficient, and how are betas used in risk analysis?

Answer: [Show S8-34 through S8-40 here.]

(Draw the framework of the graph, put up the data, then plot the

points for the market (45 line) and connect them, and then get the

High Tech

(slope = beta = 1.31)

Market

(slope = beta = 1.0)

Return on Stock i

(%)

Market

(%)

20

–

20

40

T

–

40

–

20

218

Integrated Case

Chapter 8: Risk and Rates of Return

vis an average stock. The average stock’s beta is 1.0. Most stocks

have betas in the range of 0.5 to 1.5. Theoretically, betas can be

negative, but in the real world they are generally positive.

Betas are calculated as the slope of the “characteristic” line,

I. (2) Do the expected returns appear to be related to each alternative’s

market risk?

Answer: [Show S8-41 here.] The expected returns are related to each

alternative’s market risk—that is, the higher the alternative’s rate of

I. (3) Is it possible to choose among the alternatives on the basis of the

information developed thus far? Use the data given at the start of the

problem to construct a graph that shows how the T–bill’s, High Tech’s,

and the market’s beta coefficients are calculated. Then discuss what

betas measure and how they are used in risk analysis.

Answer: We do not yet have enough information to choose among the various

Chapter 8: Risk and Rates of Return

Integrated Case

219

J. The yield curve is currently flat; that is, long-term Treasury bonds also

have a 3.0% yield. Consequently, Merrill Finch assumes that the risk-

free rate is 3.0%.

(1) Write out the Security Market Line (SML) equation; use it to calculate

the required rate of return on each alternative, and graph the

relationship between the expected and required rates of return.

Answer: [Show S8-42 through S8-44 here.] Here is the SML equation:

ri = rRF + (rM – rRF)bi.

r

ˆ

J. (2) How do the expected rates of return compare with the required rates

of return?

Answer: [Show S8-45 and S8-46 here.] We have the following relationships:

Expected Required

Return Return

Security (

r

ˆ

) (r) Condition

High Tech 9.9% 9.55% Undervalued:

r

ˆ

> r

Market 8.0 8.0 Fairly valued (market equilibrium)

r

ˆ

r

ˆ

220

Integrated Case

Chapter 8: Risk and Rates of Return

-2

8

Risk, bi

SML: ri= 3.0% + (5.0%)bi

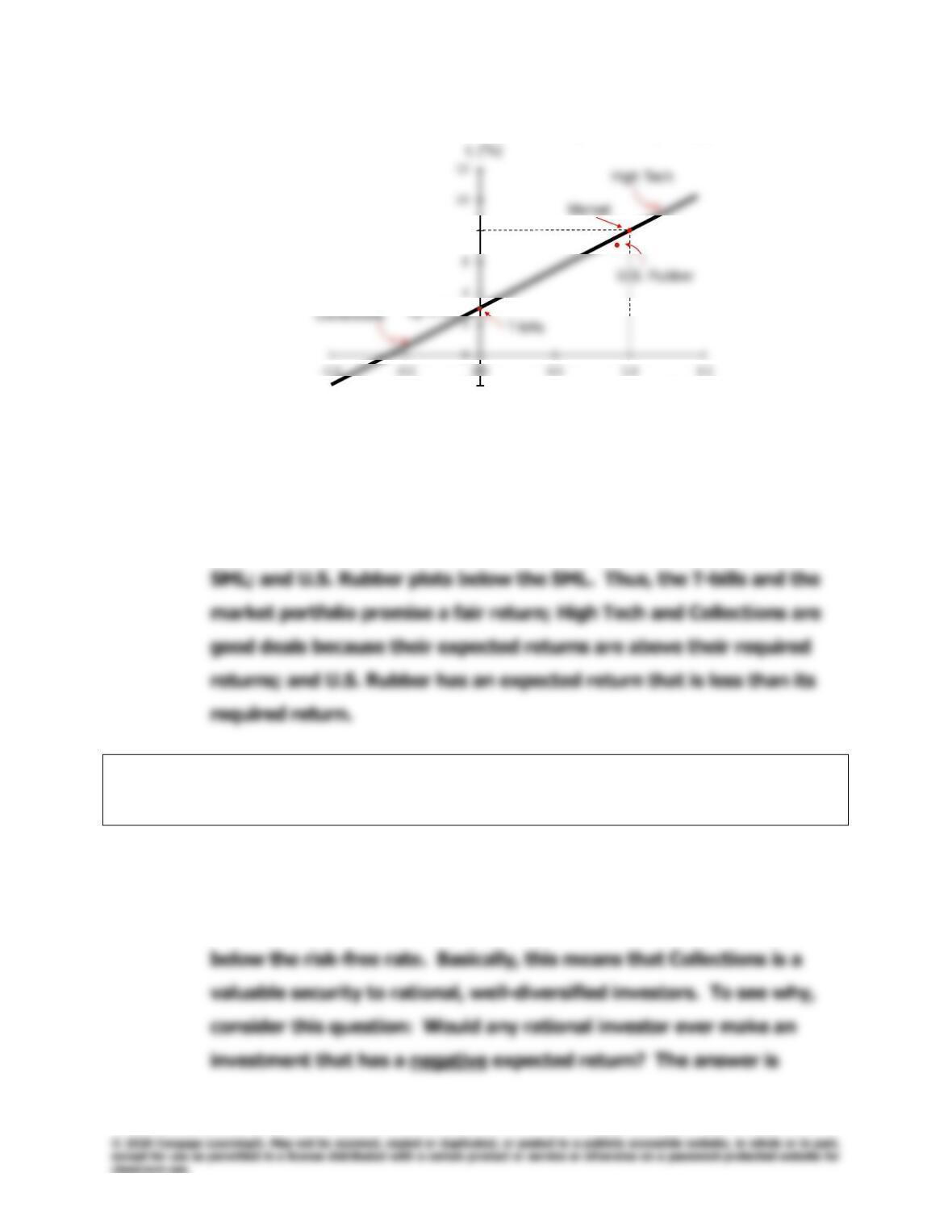

rM= 8.0

(Note: The plot looks somewhat unusual in that the X-axis extends to

the left of zero. We have a negative–beta stock, hence a required

return that is less than the risk-free rate.) The T–bills and market

portfolio plot on the SML; High Tech and Collections plot above the

J. (3) Does the fact that Collections has an expected return that is less than

the T-bill rate make any sense? Explain.

Answer: Collections is an interesting stock. Its negative beta indicates

negative market risk—including it in a portfolio of “normal” stocks will

lower the portfolio’s risk. Therefore, its required rate of return is

Chapter 8: Risk and Rates of Return

Integrated Case

221

J. (4) What would be the market risk and the required return of a 50-50

portfolio of High Tech and Collections? Of High Tech and U.S. Rubber?

Answer: [Show S8-47 and S8-48 here.] Note that the beta of a portfolio is

simply the weighted average of the betas of the stocks in the

portfolio. Thus, the beta of a portfolio with 50% High Tech and 50%

Collections is:

=

=

N

1i

iip bwb

.

For a portfolio consisting of 50% High Tech plus 50% U.S.

Rubber, the required return would be:

bp = 0.5(1.31) + 0.5(0.88) = 1.095.

222

Integrated Case

Chapter 8: Risk and Rates of Return

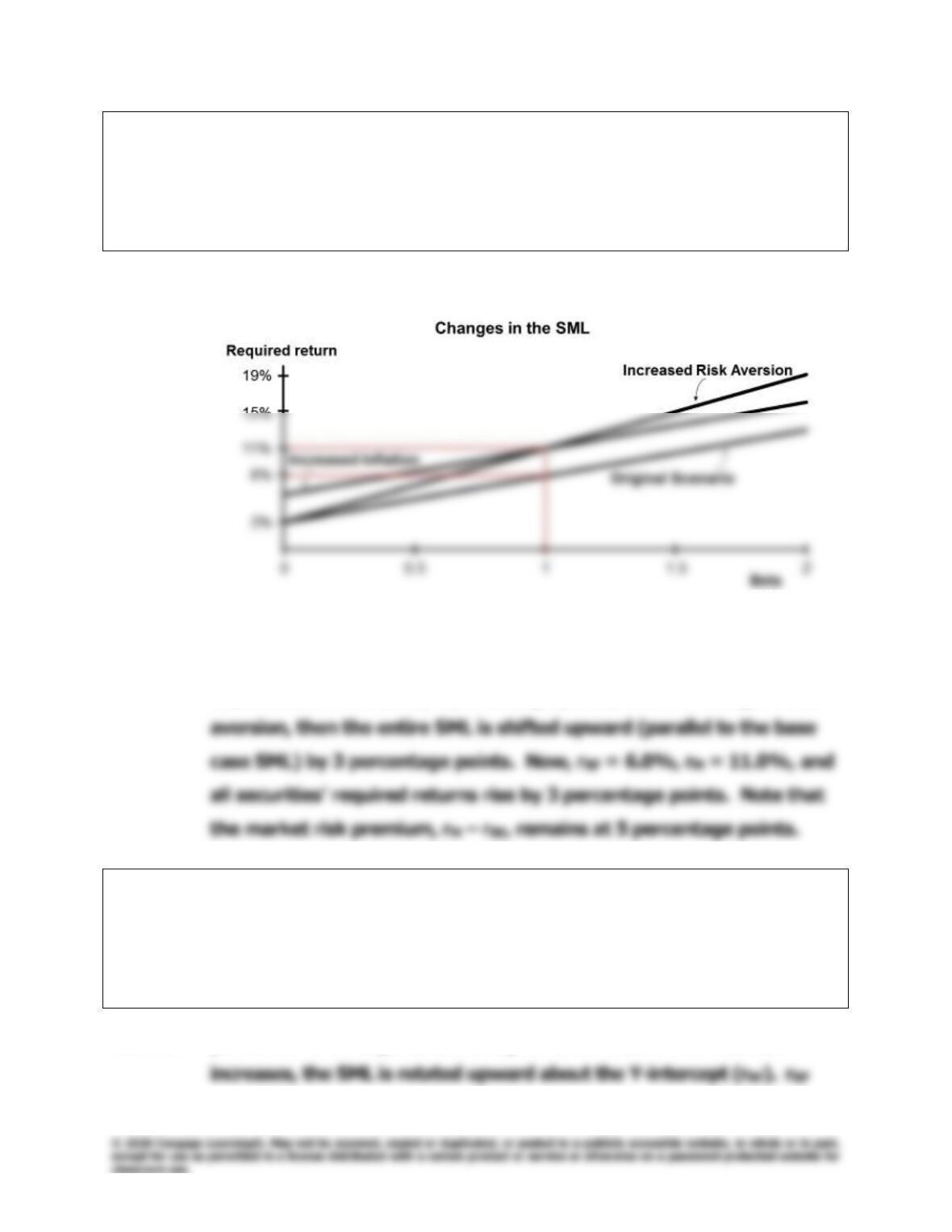

K. (1) Suppose investors raised their inflation expectations by 3 percentage

points over current estimates as reflected in the 3.0% risk-free rate.

What effect would higher inflation have on the SML and on the

returns required on high- and low-risk securities?

Answer: [Show S8-49 here.]

Here we have plotted the SML for betas ranging from 0 to 2.0. The

base–case SML is based on rRF = 3.0% and rM = 8.0%. If inflation

expectations increase by 3 percentage points, with no change in risk

K. (2) Suppose instead that investors’ risk aversion increased enough to

cause the market risk premium to increase by 3 percentage points.

(Inflation remains constant.) What effect would this have on the SML

and on returns of high- and low–risk securities?

Answer: [Show S8–50 through S8-52 here.] When investors’ risk aversion

Chapter 8: Risk and Rates of Return

Integrated Case

223

Optional Question

Financial managers are more concerned with investment decisions relating to

real assets such as plant and equipment than with investments in financial

assets such as securities. How does the analysis that we have gone through

relate to real-asset investment decisions, especially corporate capital budgeting

decisions?

Answer: There is a great deal of similarity between your financial asset

decisions and a firm’s capital budgeting decisions. Here is the

linkage:

1. A company may be thought of as a portfolio of assets. If the

company diversifies its assets, and especially if it invests in

2. Companies obtain their investment funds from investors, who

buy the firm’s stocks and bonds. When investors buy these

3. Therefore, when a manager makes a decision to build a new

not its stand-alone risk. Accordingly, managers need to know

how physical-asset investment decisions affect their firm’s beta