Chapter 7: Bonds and Their Valuation

Learning Objectives

151

Chapter 7

Bonds and Their Valuation

Learning Objectives

After reading this chapter, students should be able to do the following:

◆ Identify the different features of corporate and government bonds.

152

Lecture Suggestions

Chapter 7: Bonds and Their Valuation

Lecture Suggestions

This chapter serves two purposes. First, it provides important and useful information on bonds per se.

Second, it provides a good example of the use of time value concepts, so it reinforces the topics covered

in Chapter 5.

DAYS ON CHAPTER: 5 OF 56 DAYS (50-minute periods)

Answers to End-of-Chapter Questions

7-1 From the corporation’s viewpoint, one important factor in establishing a sinking fund is that its

own bonds generally have a higher yield than do government bonds; hence, the company saves

more interest by retiring its own bonds than it could earn by buying government bonds. This

factor causes firms to favor the second procedure. Investors also would prefer the annual

7-3 False. Short-term bond prices are less sensitive than long-term bond prices to interest rate

changes because funds invested in short-term bonds can be reinvested at the new interest rate

sooner than funds tied up in long-term bonds.

For example, consider two bonds, both with a 10% annual coupon and a $1,000 par value.

The only difference between them is their maturity. One bond is a 1-year bond, while the other is

a 20-year bond. Consider the values of each at 5%, 10%, 15%, and 20% interest rates.

1-year 20-year

5% $1,047.62 $1,623.11

7-4 The price of the bond will fall and its YTM will rise if interest rates rise. If the bond still has a

long term to maturity, its YTM will reflect long-term rates. Of course, the bond’s price will be less

affected by a change in interest rates if it has been outstanding a long time and matures soon.

While this is true, it should be noted that the YTM will increase only for buyers who purchase the

7-5 The yield to maturity can be viewed as the bond’s

promised

rate of return, which is the return

that investors will receive if all the

promised

payments are made. However, the yield to maturity

7-6 If interest rates decline significantly, the values of callable bonds will not rise by as much as the

7-7 As an investor with a short investment horizon, you would view the 20-year Treasury security as

being riskier than the 1-year Treasury security. If you bought the 20-year security, you would

7-8 a. If a bond’s price increases, its YTM decreases.

b. If a company’s bonds are downgraded by the rating agencies, its YTM increases.

7-9 If a company sold bonds when interest rates were relatively high, and the issue is callable, then

the company could sell a new issue of low-yielding securities if and when interest rates drop. The

7-10 A sinking fund provision facilitates the orderly retirement of the bond issue. Although sinking

funds are designed to protect investors by ensuring that the bonds are retired in an orderly

7-11 A call for sinking fund purposes is quite different from a refunding call. A sinking fund call

requires no call premium, and only a small percentage of the issue is normally callable in a given

7-12 Convertibles and bonds with warrants are offered with lower coupons than similarly-rated straight

bonds because both offer investors the chance for capital gains as compensation for the lower

7-13 This statement is false. Extremely strong companies can use debentures because they simply do

7-14 The yield spread between a corporate bond over a Treasury bond with the same maturity reflects

7-15 Assuming a bond issue is callable, the YTC is a better estimate of a bond’s expected return when

7-16 d. The 15-year zero coupon bonds have the most price risk. Longer-maturity bonds have a high

level of price risk as do lower–coupon bonds. Since the maturities of the bonds in a, b, and c

7-17 b. The 1-year bonds with a 12% coupon have the most reinvestment risk. Shorter-maturity

bonds have more reinvestment risk than longer-maturity bonds, so immediately the bonds in a,

156

Answers and Solutions

Chapter 7: Bonds and Their Valuation

Solutions to End-of-Chapter Problems

7-1 With your financial calculator, enter the following:

N = 23; I/YR = YTM = 11%; PMT = 0.09 1,000 = 90; FV = 1000; PV = VB = ?

7-2 VB = $980; M = $1,000; Int = 0.08 $1,000 = $80.

a. N = 12; PV = –980; PMT = 80; FV = 1000; YTM = ?

7-3 The problem asks you to find the price of a semiannual bond, given the following facts: N = 2 14 =

7-4 With your financial calculator, enter the following to find YTM:

N = 8 2 = 16; PV = -1283.09; PMT = 0.11/2 1,000 = 55; FV = 1000; I/YR = YTM = ?

YTM = 3.21% 2 = 6.42%.

With your financial calculator, enter the following to find YTC:

7-5 a. 1. 6%: Bond L: Input N = 12, I/YR = 6, PMT = 110, FV = 1000, PV = ?, PV = $1,419.19.

Bond S: Change N = 1, PV = ? PV = $1,047.17.

one–month bond’s value because of the difference in the timing of receipts. However, its value

would still be close to $1,000 even if interest rates doubled. A long-term bond paying semiannual

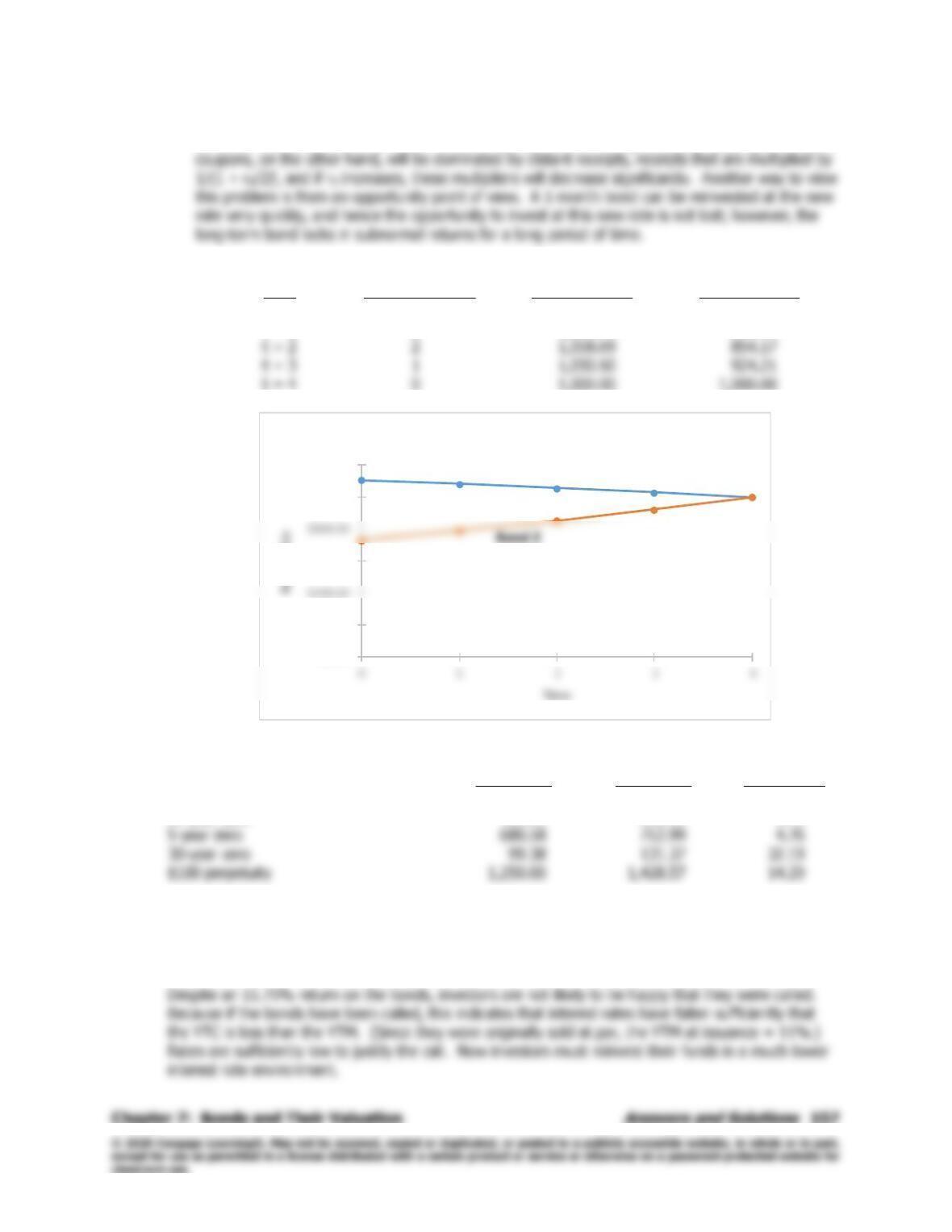

7-6 a. Time Years to Maturity Price of Bond C Price of Bond Z

t = 0 4 $1,108.82 $ 729.61

t = 1 3 1,084.74 789.44

t = 4 0 1,000.00 1,000.00

b.

7-7 Percentage

Price at 8% Price at 7% Change

10-year, 10% annual coupon $1,134.20 $1,210.71 6.75%

10-year zero 463.19 508.35 9.75

7-8 The rate of return is approximately 11.75%, found with a calculator using the following inputs:

N = 7; PV = -1000; PMT = 110; FV = 1075; I/YR = ? Solve for I/YR = 11.75%.

$0.00

$200.00

$600.00

$1,000.00

$1,200.00

Bond Price Paths

Bond C

158

Answers and Solutions

Chapter 7: Bonds and Their Valuation

7-9 a. VB =

=+

+

+

N

1t

N

d

t

d)r1(

M

)r1(

INT

M = $1,000, PMT = 0.10($1,000) = $100, N = 6.

b. Yes. At a price of $865, the yield to maturity, 13.42%, is greater than your required rate of

7-10 a. Solving for YTM:

N = 9, PV = –910.30, PMT = 90, FV = 1000

b. The current yield is defined as the annual coupon payment divided by the current price.

CY = $90/$910.30 = 9.8869% 9.887%.

Expected capital gains yield can be found as the difference between YTM and the current yield.

c. As rates change they will cause the end–of-year price to change and thus the realized capital

7-11 a. Using a financial calculator, input the following to solve for YTM:

N = 18, PV = –1200, PMT = 65, FV = 1000, and solve for YTM = I/YR = 4.813867%.

However, this is a periodic rate. The nominal YTM = 4.813867%(2) = 9.627733% 9.63%.

For the YTC, input the following:

Chapter 7: Bonds and Their Valuation

Answers and Solutions

159

b. The current yield = $130/$1,200 = 10.83%. The current yield will remain the same; however, if

7-12 a. Yield to maturity (YTM):

With a financial calculator, input N = 28, PV = –1191.20, PMT = 80, FV = 1000, I/YR = ? I/YR =

YTM = 6.50%.

Yield to call (YTC):

b. Knowledgeable investors would expect the return to be closer to 3.7% than to 6.5%. If interest

rates remain substantially lower than 8%, the company can be expected to call the issue at the

7-13 The problem asks you to solve for the YTM and Price, given the following facts:

N = 4 2 = 8, PMT = 70/2 = 35, and FV = 1000. To solve for I/YR we need PV.

However, you are also given that the current yield is equal to 7.5401%. Given this information, we

can find PV (Price).

Current yield = Annual interest/Current price

7-14 a. The bond is selling at a large premium, which means that its coupon rate is much higher than the

going rate of interest. Therefore, the bond is likely to be called—it is more likely to be called than

7-15 First, we must find the amount of money we can expect to sell this bond for in 5 years. This is found

using the fact that in five years, there will be 15 years remaining until the bond matures and that the

expected YTM for this bond at that time will be 7.5%.

N = 15, I/YR = 7.5, PMT = 80, FV = 1000

7-16 Before you can solve for the price, we must find the appropriate semiannual rate at which to evaluate

this bond.

EAR = (1 + INOM/2)2 – 1

7-17 First, we must find the price Janet paid for this bond.

N = 15, I/YR = 10.45, PMT = 80, FV = 1000

PV = –$818.34. VB = $818.34.

Chapter 7: Bonds and Their Valuation

Answers and Solutions

161

7-18 a. Find the YTM as follows:

N = 10, PV = –1185, PMT = 110, FV = 1000

I/YR = YTM = 8.216% 8.22%.

b. Find the YTC, if called in Year 5 as follows:

d. Similarly, from above, YTC can be found, if called in each subsequent year.

If called in Year 6:

N = 6, PV = –1185, PMT = 110, FV = 1080

I/YR = YTC = 8.0772% 8.08%.

162

Comprehensive/Spreadsheet Problem

Chapter 7: Bonds and Their Valuation

Comprehensive/Spreadsheet Problem

Note to Instructors:

The solution to this problem is not provided to students at the back of their text. Instructors

can access the

Excel

file on the textbook’s website.

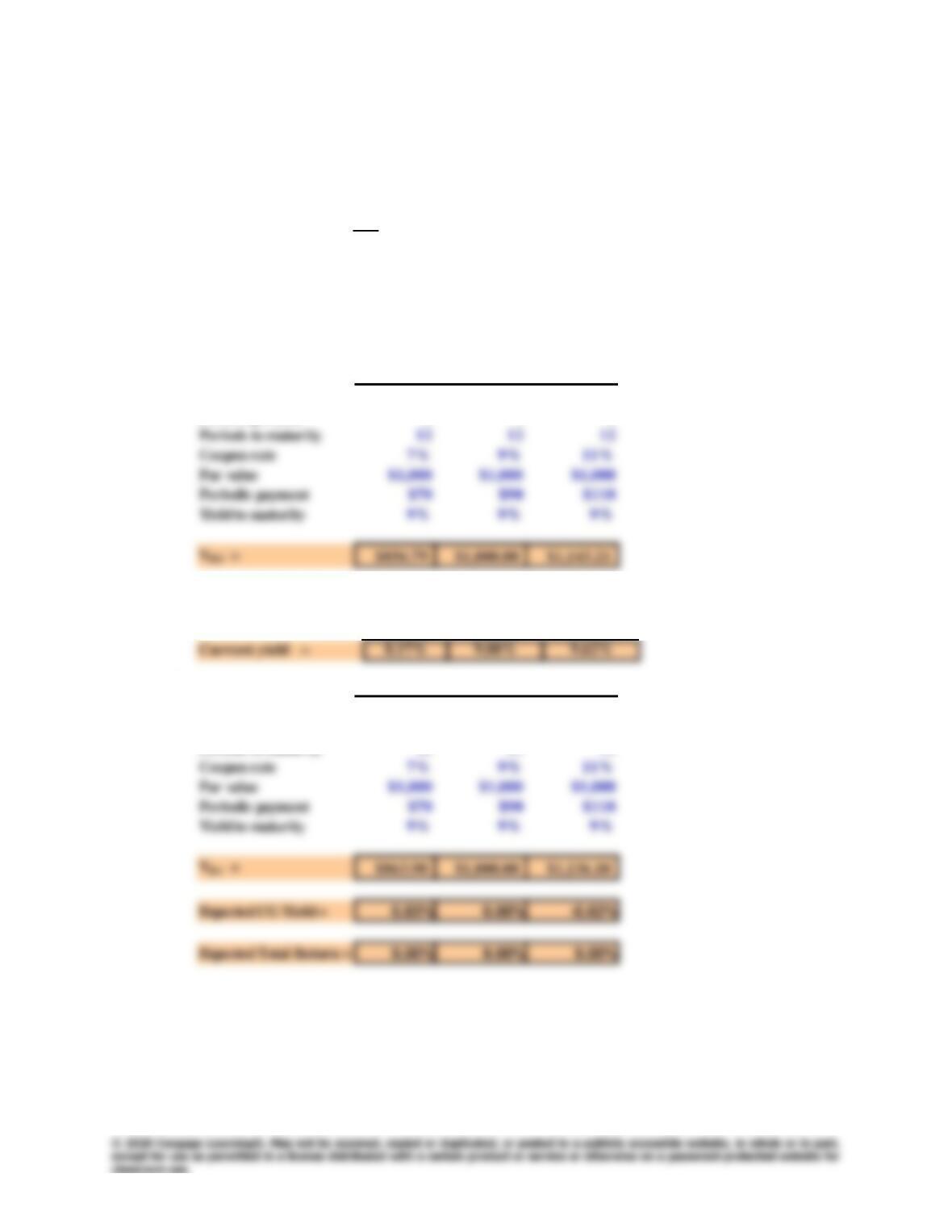

7-19 a. Bond A is selling at a discount because its coupon rate (7%) is less than the going interest rate

(YTM = 9%). Bond B is selling at par because its coupon rate (9%) is equal to the going

interest rate (YTM = 9%). Bond C is selling at a premium because its coupon rate (11%) is

greater than the going interest rate (YTM = 9%).

b.

c.

d.

Current yield = Annual coupon / Price

Bond A Bond B Bond C

Basic Input Data Bond A Bond B Bond C

Years to maturity 12 12 12

Periods per year 1 1 1

Basic Input Data Bond A Bond B Bond C

Years to maturity 11 11 11

Periods per year 1 1 1

Periods to maturity 11 11 11

Chapter 7: Bonds and Their Valuation

Comprehensive/Spreadsheet Problem

163

e.

3. The bond is selling at a premium, which means that interest rates have declined since the

bond was issued. If interest rates remain at current levels, then Mr. Clark should expect

the bond to be called. Consequently, he would earn the YTC not the YTM.

f.

A 5-year bond with a zero coupon $649.93 $620.92 -4.46%

A 10-year bond with a zero coupon

Ranking the bonds above in order from the most price risk to the least price risk: 10-year bond

with a zero coupon, 10-year bond with a 9% annual coupon, 5-year bond with a zero coupon,

5-year bond with a 9% annual coupon, and a 1-year bond with a 9% annual coupon.

Basic Input Data Bond D

Years to maturity 9

Periods per year 2

Par value $1,000

Periodic payment $40

YTM = 5.83%

9% 10%

% Price

Chge

A 1-year bond with a 9% annual coupon $1,000.00 $990.91 -0.91%

A 5-year bond with a 9% annual coupon $1,000.00 $962.09 -3.79%

164

Comprehensive/Spreadsheet Problem

Chapter 7: Bonds and Their Valuation

g.

1.

8.17% 9.00% 9.62%

8.03% 9.00% 9.75%

7.87% 9.00% 9.90%

7.69% 9.00% 10.09%

7.48% 9.00% 10.33%

7.26% 9.00% 10.63%

Years Remaining Until Maturity Bond A Bond B Bond C

12 $856.79 $1,000.00 $1,143.21

11 $863.90 $1,000.00 $1,136.10

10 $871.65 $1,000.00 $1,128.35

9 $880.10 $1,000.00 $1,119.90

Time Paths of Bonds A, B, and C

$0.00

$200.00

$400.00

$800.00

$1,000.00

$1,200.00

$1,400.00

Bond Value

Bond A

Years Remaining Until Maturity Bond A Bond B Bond C

11

8.10% 9.00% 9.68%

9

7.95% 9.00% 9.82%

7

7.78% 9.00% 9.99%

5

7.59% 9.00% 10.21%

3

7.37% 9.00% 10.47%

1

7.13% 9.00% 10.80%

Chapter 7: Bonds and Their Valuation

Comprehensive/Spreadsheet Problem

165

2.

11

0.90% 0.00% -0.68%

9

7

1.22% 0.00% -0.99%

5

3

1.63% 0.00% -1.47%

1

1.87% 0.00% -1.80%

3.

10

9.00% 9.00% 9.00%

8

9.00% 9.00% 9.00%

6

9.00% 9.00% 9.00%

4

9.00% 9.00% 9.00%

2

9.00% 9.00% 9.00%

Years Remaining Until Maturity Bond A Bond B Bond C

12

0.83% 0.00% -0.62%

10

0.97% 0.00% -0.75%

8

1.13% 0.00% -0.90%

6

1.31% 0.00% -1.09%

4

1.52% 0.00% -1.33%

2

1.74% 0.00% -1.63%

Years Remaining Until Maturity Bond A Bond B Bond C

12

9.00% 9.00% 9.00%

11

9.00% 9.00% 9.00%

9

9.00% 9.00% 9.00%

7

9.00% 9.00% 9.00%

5

9.00% 9.00% 9.00%

3

9.00% 9.00% 9.00%

1

9.00% 9.00% 9.00%

166

Integrated Case

Chapter 7: Bonds and Their Valuation

Integrated Case

7-20

Western Money Management Inc.

Bond Valuation

Robert Black and Carol Alvarez are vice presidents of Western Money

Management and codirectors of the company’s pension fund management

division. A major new client, the California League of Cities, has requested

that Western present an investment seminar to the mayors of the represented

cities. Black and Alvarez, who will make the presentation, have asked you to

help them by answering the following questions.

A. What are a bond’s key features?

Answer: [Show S7-1 through S7-5 here.] Here is a list of key features:

1. Par or face value. We generally assume a $1,000 par value, but

2. Coupon rate. The dollar coupon is the “rent” on the money

borrowed, which is generally the par value of the bond. The

3. Maturity. This is the number of years until the bond matures and

the issuer must repay the loan (return the par value).

4. Call provision. Most bonds (except U.S. Treasury bonds) can be

called and paid off ahead of schedule after some specified “call

Chapter 7: Bonds and Their Valuation

Integrated Case

167

5. Issue date. The date when the bond issue was originally sold.

6. Default risk is inherent in all bonds except Treasury bonds—will

the issuer have the cash to make the promised payments?

7. Special features, such as convertibility and zero coupons, will be

B. What are call provisions and sinking fund provisions? Do these

provisions make bonds more or less risky?

Answer: [Show S7-6 through S7-8 here.] A call provision is a provision in a

bond contract that gives the issuing corporation the right to redeem

the bonds under specified terms prior to the normal maturity date.

168

Integrated Case

Chapter 7: Bonds and Their Valuation

A sinking fund provision is a provision in a bond contract that

requires the issuer to retire a portion of the bond issue each year. A

sinking fund provision facilitates the orderly retirement of the bond

issue.

Although sinking funds are designed to protect bondholders by

ensuring that an issue is retired in an orderly fashion, it must be

recognized that sinking funds will at times work to the detriment of

C. How is the value of any asset whose value is based on expected

future cash flows determined?

Answer: [Show S7-9 and S7-10 here.]

0 1 2 3 N

| | | | • • • |

CF1 CF2 CF3 CFN

PV CF1

PV CF2

Chapter 7: Bonds and Their Valuation

Integrated Case

169

Value = PV =

N

d

N

3

d

3

2

d

2

1

d

1

)r(1

CF

…

)r1(

CF

)r1(

CF

)r1(

CF

+

++

+

+

+

+

+

If the cash flows have widely varying risk, or if the yield curve is not

horizontal, which signifies that interest rates are expected to

D. How is a bond’s value determined? What is the value of a 10-year,

$1,000 par value bond with a 10% annual coupon if its required

return is 10%?

Answer: [Show S7–11 and S7–12 here.] A bond has a specific cash flow

pattern consisting of a stream of constant interest payments plus the