Chapter 12: Cash Flow Estimation and Risk Analysis

Learning Objectives

307

Chapter 12

Cash Flow Estimation and Risk Analysis

Learning Objectives

After reading this chapter, students should be able to:

◆ Identify “relevant” cash flows that should and should not be included in a capital budgeting analysis.

◆ Estimate a project’s relevant cash flows and put them into a time line format that can be used to

calculate a project’s NPV, IRR, and other capital budgeting metrics.

308

Lecture Suggestions

Chapter 12: Cash Flow Estimation and Risk Analysis

Lecture Suggestions

This chapter covers some important but relatively technical topics. Note too that this chapter is more

modular than most, i.e., the major sections are discrete, hence they can be omitted without loss of

DAYS ON CHAPTER: 3 OF 56 DAYS (50-minute periods)

Chapter 12: Cash Flow Estimation and Risk Analysis

Answers and Solutions

309

Answers to End-of-Chapter Questions

12-1 Only cash can be spent or reinvested, and since accounting profits do not represent cash, they

12-2 Capital budgeting analysis should only include those cash flows that will be affected by the

decision. Sunk costs are unrecoverable and cannot be changed, so they have no bearing on the

12-3 When a firm takes on a new capital budgeting project, it typically must increase its investment in

receivables and inventories, over and above the increase in payables and accruals, thus

12-4 The costs associated with financing are reflected in the weighted average cost of capital. To

12-5 Daily cash flows would be theoretically best, but they would be costly to estimate and probably

no more accurate than annual estimates because we simply cannot forecast accurately at a daily

12-6 In replacement projects, the benefits are generally cost savings, although the new machinery

may also permit additional output. The data for replacement analysis are generally easier to

12-7 Stand-alone risk is the project’s risk if it is held as a lone asset. It disregards the fact that it is

but one asset within the firm’s portfolio of assets and that the firm is but one stock in a typical

310

Answers and Solutions

Chapter 12: Cash Flow Estimation and Risk Analysis

12-8 It is often difficult to quantify market risk. On the other hand, we can usually get a good idea of

a project’s stand-alone risk, and that risk is normally correlated with market risk: The higher the

12-9 Simulation analysis involves working with continuous probability distributions, and the output of a

simulation analysis is a distribution of net present values or rates of return. Scenario analysis

12–10 Scenario analyses, and especially simulation analyses, would probably be reserved for very

important “make–or–break” decisions. They would not be used for every project decision because

12-11 The replacement chain approach is a method of comparing projects with unequal lives that

12-12 The equivalent annual annuity method calculates the annual payments a project would provide if it

12-13 Generally, the failure to employ replacement chain analysis or the equivalent annual annuity

Chapter 12: Cash Flow Estimation and Risk Analysis

Answers and Solutions

311

Solutions to End-of-Chapter Problems

12-1 a. Equipment purchase ($ 9,000,000)

12-2 a. Project cash flows: t = 1

Sales revenues $10,000,000

b. The cannibalization of existing sales needs to be considered in this analysis on an after–tax

c. If the tax rate fell to 30%, the project’s cash flow would change to:

EBIT $1,000,000

12-3 Equipment’s original cost $20,000,000

Depreciation (80%) 16,000,000

312

Answers and Solutions

Chapter 12: Cash Flow Estimation and Risk Analysis

12-4 Cash outflow = $40,000.

Increase in annual after-tax cash flows: CF = $9,000.

12-5 First, solve for each project’s NPV.

Project A: CF0 = –20000, CF1 = 6000, Nj = 6, I/YR = 10; solve for NPV = $6,131.56.

12-6 a. The applicable depreciation values are as follows for the two scenarios:

Scenario 1 Scenario 2

Year (Straight-Line) (MACRS)

1 $200,000 $264,000

b. To find the difference in net present values under these two methods, we must determine the

difference in incremental cash flows each method provides. The depreciation expenses cannot

simply be subtracted from each other, as there are tax ramifications due to depreciation

Chapter 12: Cash Flow Estimation and Risk Analysis

Answers and Solutions

313

12-7 E(NPV) = 0.05(-$70) + 0.20(-$25) + 0.50($12) + 0.20($20) + 0.05($30)

b.

Project’s operating cash flows:

Year 1 Year 2 Year 3

Savings $50,000 $50,000 $50,000

314

Answers and Solutions

Chapter 12: Cash Flow Estimation and Risk Analysis

Notes:

1. The depreciation expense in each year is the depreciable basis, $170,000, times the MACRS

c. The project has an NPV of ($19,549). Thus, it should not be accepted.

Year Cash Flows PV @ 12%

Alternatively, place the free cash flows on a time line:

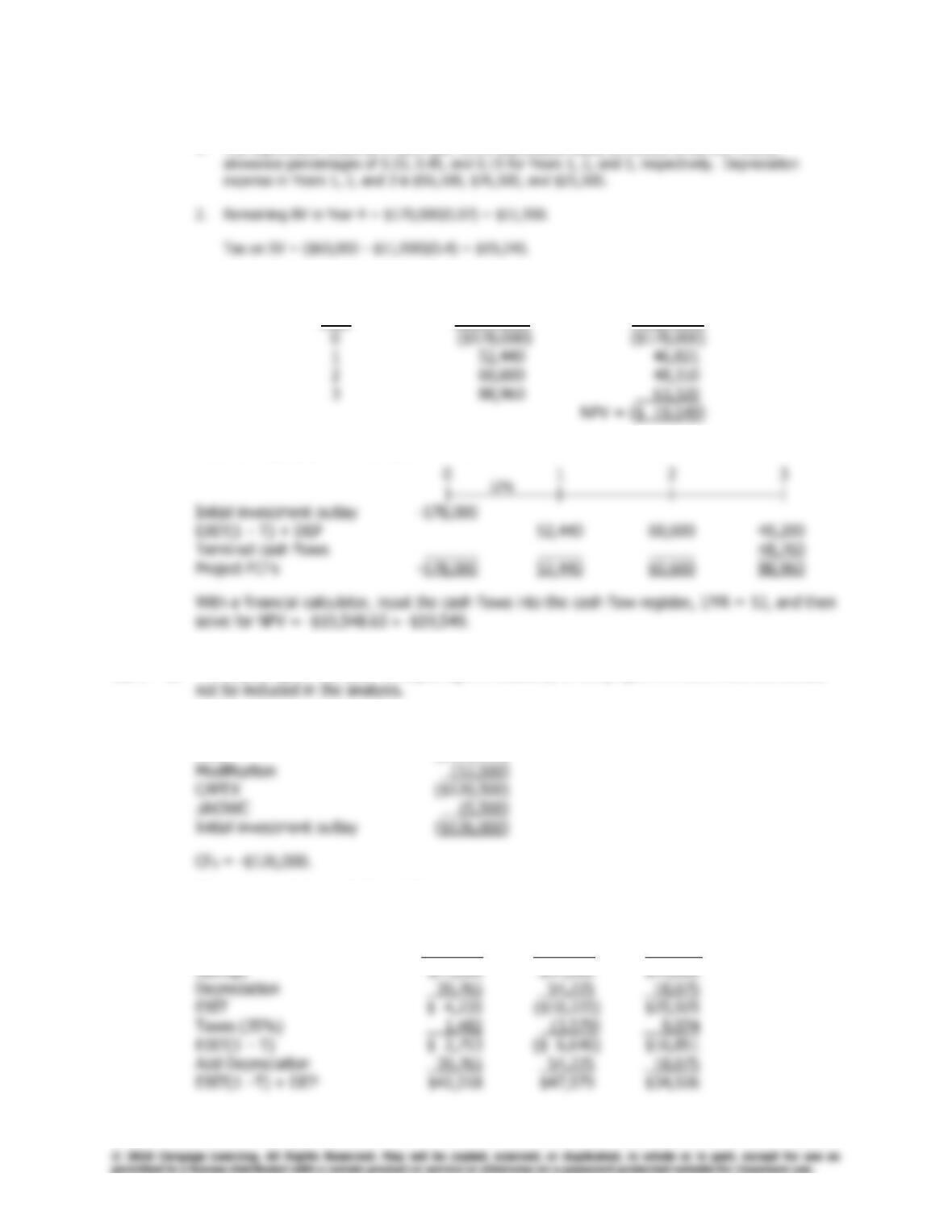

12-9 a. The $5,000 spent last year on exploring the feasibility of the project is a sunk cost and should

b. The initial investment outlay at t = 0 is $126,000:

Price ($108,000)

c. The annual project cash flows follow:

Project’s operating cash flows:

Year 1 Year 2 Year 3

Chapter 12: Cash Flow Estimation and Risk Analysis

Answers and Solutions

315

Terminal cash flows at time = 3:

Salvage value $65,000

Tax on salvage value 19,798

AT salvage value $45,202

d. The project has an NPV of $10,841; thus, it should be accepted.

Year Cash Flows PV @ 12%

Alternatively, place the free cash flows on a time line:

12–10 First determine the net cash flow at t = 0:

Purchase price ($8,000)

316

Answers and Solutions

Chapter 12: Cash Flow Estimation and Risk Analysis

After-tax revenue increase:

Depreciation:

Year 1 2 3 4 5 6

Newa $1,600 $2,560 $1,520 $960 $880 $480

Finally, place all the cash flows on a time line:

0 1 2 3 4 5 6

| | | | | | |

Net investment (7,160)

After-tax revenue increase 1,500 1,500 1,500 1,500 1,500 1,500

Depreciation tax savings 500 884 468 244 212 52

12-11 1. Net investment at t = 0:

15%

Chapter 12: Cash Flow Estimation and Risk Analysis

Answers and Solutions

317

2. After–tax

Year Earnings T(Dep) Annual CFt

1 $16,200 $ 6,600 $22,800

Notes:

3. Now find the NPV of the replacement machine:

Place the cash flows on a time line:

12-12 a. Expected annual cash flows:

Project A: Probable

Probability × Cash Flow = Cash Flow

0.2 $6,000 $1,200

318

Answers and Solutions

Chapter 12: Cash Flow Estimation and Risk Analysis

Coefficient of variation:

b. Project B is the riskier project because it has the greater variability in its probable cash flows,

whether measured by the standard deviation or the coefficient of variation. Hence, Project B is

evaluated at the 12% cost of capital, while Project A requires only a 10% cost of capital.

12–13 a. Project A: 0 1 2

| | |

-10,000 6,000 8,000

Using a financial calculator, input the following data: CF0 = -10000, CF1 = 6000, CF2 = 8000,

I/YR = 10, and then solve for NPVA = $2,066.12.

Project B: 0 1 2 3 4

| | | | |

-10,000 4,000 4,000 4,000 4,000

Using a financial calculator, input the following data: CF0 = -10000, CF1-4 = 4000, I/YR = 10,

and then solve for NPVB = $2,679.46.

Since neither project can be repeated, Project B should be selected because it has a higher NPV

than Project A.

10%

10%

Chapter 12: Cash Flow Estimation and Risk Analysis

Answers and Solutions

319

b. To determine the answer to Part b, we use the replacement chain (common life) approach to

calculate the extended NPV for Project A. Project B already extends out to 4 years, so its NPV is

$2,679.46.

Project A: 0 1 2 3 4

| | | | |

c. From Part a, NPVA = $2,066.12 and NPVB = $2,679.46. Solving for PMT determines the EAA:

12–14 0 1 2 3

| | | |

-190,000 87,000 87,000 87,000

10%

14%

320

Answers and Solutions

Chapter 12: Cash Flow Estimation and Risk Analysis

12–15 Since Plane A’s renewal investment changes the EAA method cannot be used, so the replacement

12–16 A: 0 1 2 3 4 5 6 7 8

| | | | | | | | |

–10 4 4 4 4

–12 4.2 4.2 4.2 4.2

-8

10%

Chapter 12: Cash Flow Estimation and Risk Analysis

Answers and Solutions

321

12–17 First, solve for each project’s NPV.

Project X: CF0 = -100000, CF1 = 30000, CF2 = 50000, CF3 = 70000, I/YR = 12; solve for NPV =

$16,470.0255.

12–18 If actual life is 5 years:

Using a time line approach:

0 1 2 3 4 5

If actual life is 4 years:

Using a time line approach:

10%

10%

322

Answers and Solutions

Chapter 12: Cash Flow Estimation and Risk Analysis

If actual life is 8 years:

Using a time line approach:

12-19 a. 0 1 2 3 4 5

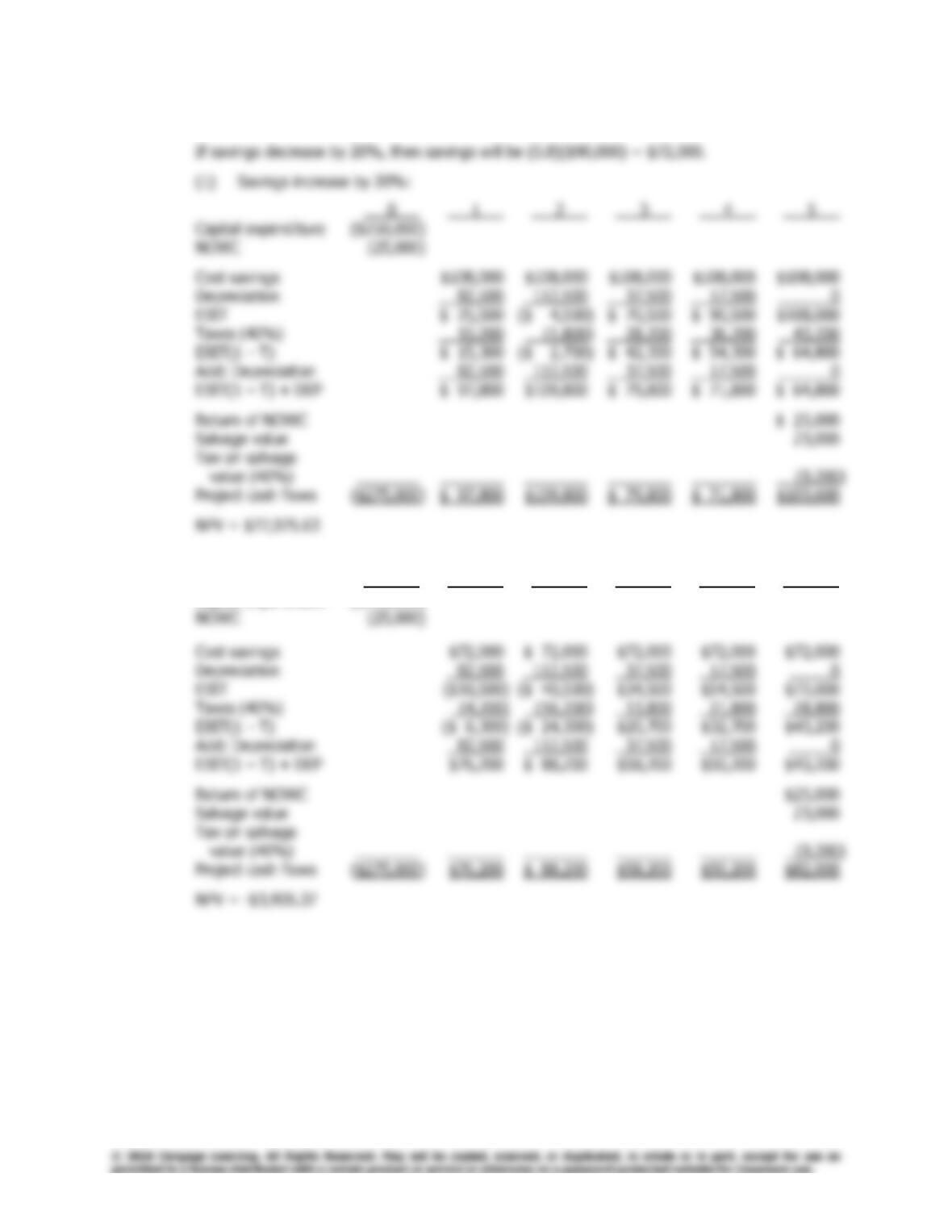

Capital expenditure ($250,000)

NOWC (25,000)

Cost savings $90,000 $ 90,000 $90,000 $90,000 $90,000

Chapter 12: Cash Flow Estimation and Risk Analysis

Answers and Solutions

323

b. If savings increase by 20%, then savings will be (1.2)($90,000) = $108,000.

(2) Savings decrease by 20%:

0 1 2 3 4 5

Capital expenditure ($250,000)

324

Answers and Solutions

Chapter 12: Cash Flow Estimation and Risk Analysis

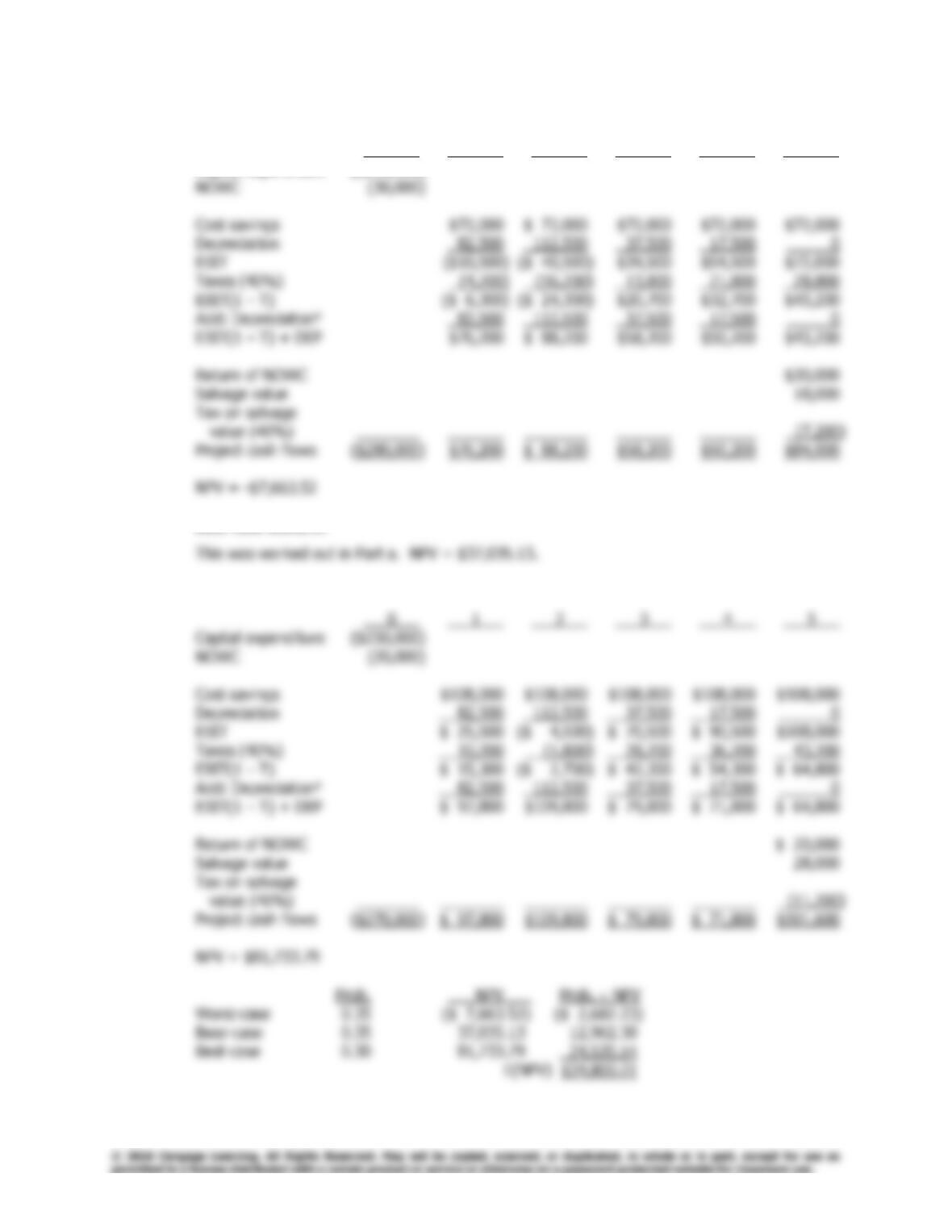

c. Worst-case scenario:

0 1 2 3 4 5

Capital expenditure ($250,000)

Base-case scenario:

Best-case scenario:

Chapter 12: Cash Flow Estimation and Risk Analysis

Answers and Solutions

325

12–20 a. Old depreciation = $9,000 per year.

b. Recovery Depreciable Depreciation Depreciation Change in

Year Percentage Basis Allowance, New Allowance, Old Depreciation

326

Answers and Solutions

Chapter 12: Cash Flow Estimation and Risk Analysis

b. Recovery Depreciable Depreciation Depreciation Change in

Year Percentage Basis Allowance, New Allowance, Old Depreciation

1 20% $1,175,000 $235,000 $120,000 $115,000

c. CFt = (Operating expenses)(1 – T) + (Depreciation)(T).

A time line of the cash flows looks like this:

d. From part c input the data into your calculator as follows: CF0 = -792750; CF1 = 206000; CF2

e. 1. If the expected life of the old machine decreases, the new machine will look better as cash