Chapter 9: Stocks and Their Valuation

Learning Objectives

225

Chapter 9

Stocks and Their Valuation

Learning Objectives

After reading this chapter, students should be able to do the following:

◆ Discuss the legal rights of stockholders.

◆ Explain the distinction between a stock’s price and its intrinsic value.

◆ Identify the two models that can be used to estimate a stock’s intrinsic value: the discounted

dividend model and the corporate valuation model.

◆ List the key characteristics of preferred stock, and describe how to estimate the value of preferred

stock.

226

Lecture Suggestions

Chapter 9: Stocks and Their Valuation

Lecture Suggestions

This chapter provides important and useful information on common and preferred stocks. Moreover, the

valuation of stocks reinforces the concepts covered in Chapters 5, 7, and 8, so Chapter 9 extends and

reinforces concepts discussed in those chapters.

We begin our lecture with a discussion of the characteristics of common stocks and how stocks

are valued in the market. Models are presented for valuing constant growth stocks, zero growth stocks,

and nonconstant growth stocks. We then present the corporate valuation model, which can be used to

value divisions and firms that do not pay dividends. We conclude the lecture with a discussion of

preferred stocks.

What we cover, and the way we cover it, can be seen by scanning the slides and Integrated Case

solution for Chapter 9, which appears at the end of this chapter’s solutions. For other suggestions about

the lecture, please see the “Lecture Suggestions” in Chapter 2, where we describe how we conduct our

classes.

DAYS ON CHAPTER: 3 OF 56 DAYS (50-minute periods)

Answers to End-of-Chapter Questions

9-1 a. The average investor of a firm traded on the NYSE is not really interested in maintaining his

or her proportionate share of ownership and control. If the investor wanted to increase his

or her ownership, the investor could simply buy more stock on the open market.

9-2 No. The correct equation has D1 in the numerator and a minus sign in the denominator between

9-3 Yes. If a company decides to increase its payout ratio, then the dividend yield component will

rise, but the expected long-term capital gains yield will decline.

9-4 Yes. The value of a share of stock is the PV of its expected future dividends. If the two investors

9-5 A perpetual bond is like a no-growth stock and to a share of perpetual preferred stock in the

following ways:

1. All three derive their values from a series of cash inflows—coupon payments from the

perpetual bond and dividends from both types of stock.

2. All three are assumed to have indefinite lives with no maturity value (M) for the perpetual

bond and no capital gains yield for the stocks.

9-6 The discounted dividend model uses the firm’s cost of equity as the discount rate to discount

future dividends per share an investor expects to receive starting at t = 1 to calculate the firm’s

intrinsic value,

0

P

ˆ

, today. The corporate valuation model uses the firm’s weighted average cost of

9-7 The P/E approach can be used as a starting point in stock valuation. If a stock’s P/E ratio is well

above its industry average and if the stock’s growth potential and risk are similar to other firms in

the industry, the stock’s price may be too high. To estimate a ball–park value multiply the firm’s

EPS by the industry-average P/E ratio.

9-8 Non-operating assets are added to the market value of the firm’s operations to arrive at the firm’s

Solutions to End-of-Chapter Problems

9-1 D0 = $1.00; g1-3 = 12%; gn = 5%; D1 through D5 = ?

9-2 D1 = $1.80; g = 4%; rs = 10%;

0

P

ˆ

= ?

9-3 P0 = $38; D0 = $2.00; g = 5%;

1

P

ˆ

= ?; rs = ? If the stock is in a constant growth state, the

constant dividend growth rate is also the capital gains yield for the stock and the stock price growth

rate. Hence, to find the price of the stock one year from today:

1

P

ˆ

9-4 a. The horizon date is the date when the growth rate becomes constant—refer to Section 9-6 in

your text. In this problem, the horizon date occurs at the end of Year 2.

b. D1 = D0 × (1.18) = $2.75 × (1.18) = $3.2450

230

Answers and Solutions

Chapter 9: Stocks and Their Valuation

0 1 2 3

| | | |

2.75 3.2450 3.8291 4.0588

c. The firm’s intrinsic value is calculated as the sum of the present value of all dividends during

the supernormal growth period plus the present value of the terminal value. Using your

financial calculator, enter the following inputs: CF0 = 0, CF1 = 3.2450, CF2 = 3.8291 + 67.65 =

9-5 The firm’s free cash flow is expected to grow at a constant rate, hence we can apply a constant

growth formula to determine the total value of the firm. (Since the firm has zero non-operating

assets, the market value of the firm’s operations equal the total firm value.)

Firm value = FCF1/(WACC – gFCF)

9-6 Dp = $2.75; Vp = $30; rp = ?

p

gs = 18%

gs = 18%

gn = 6%

rs = 12%

Chapter 9: Stocks and Their Valuation

Answers and Solutions

231

9-7 Vp = Dp/rp; therefore, rp = Dp/Vp. Dividend = Dp = 0.10 × $100 = $10.

a. rp = $10/$61 = 16.39%.

9-8 a. Dp = 0.08 × $100 = $8.

.29.114$

07.0

8$

r

D

V

p

p

p===

9-9 a. The preferred stock pays $4 (4 × $1.00) annually in dividends. Therefore, its nominal rate of

return would be:

Nominal rate of return = $4/$45 = 8.8889%.

Or alternatively, you could determine the security’s periodic return and multiply by 4 as follows:

b. EAR = (1 + rNOM/4)4 – 1

82.2$

)94.0(3$

)]06.0(1[3$

)g1(D

D

s

s

−+

+

9-11 First, solve for the current price. Note that the value for D1 was given in the problem.

0

P

ˆ

= D1/(rs – g)

232

Answers and Solutions

Chapter 9: Stocks and Their Valuation

4

P

ˆ

9-12 a. 1.

.25.12$

10.0

2250.1$

02.008.0

)02.01(25.1$

P

ˆ

0==

+

−

=

0

P

ˆ

05.0

03.008.0

−

3125.1$

)05.1(25.1$

ˆ

b. 1.

0

P

ˆ

= [$1.25(1.08)]/(0.08 – 0.08) = $1.35/0 = Undefined.

0

P

ˆ

c. No, the results of part b show this. It is not reasonable for a firm to grow indefinitely at a rate

9-13 The problem asks you to determine the value of

3

P

ˆ

, given the following facts: D1 = $2.25, b = 0.9,

rRF = 4.9%, RPM = 5%, and P0 = $46. As stated in the problem, the market is assumed to be in

equilibrium, so the expected return is equal to the required return. Proceed as follows:

Step 1: Calculate the required rate of return:

Chapter 9: Stocks and Their Valuation

Answers and Solutions

233

Step 3: Calculate

3

P

ˆ

:

If the stock is in a constant growth state, the constant dividend growth rate is also the capital gains

yield for the stock and the stock price growth rate. Hence, to find the price of the stock three years

from today:

3

P

ˆ

3

P

ˆ

3

P

ˆ

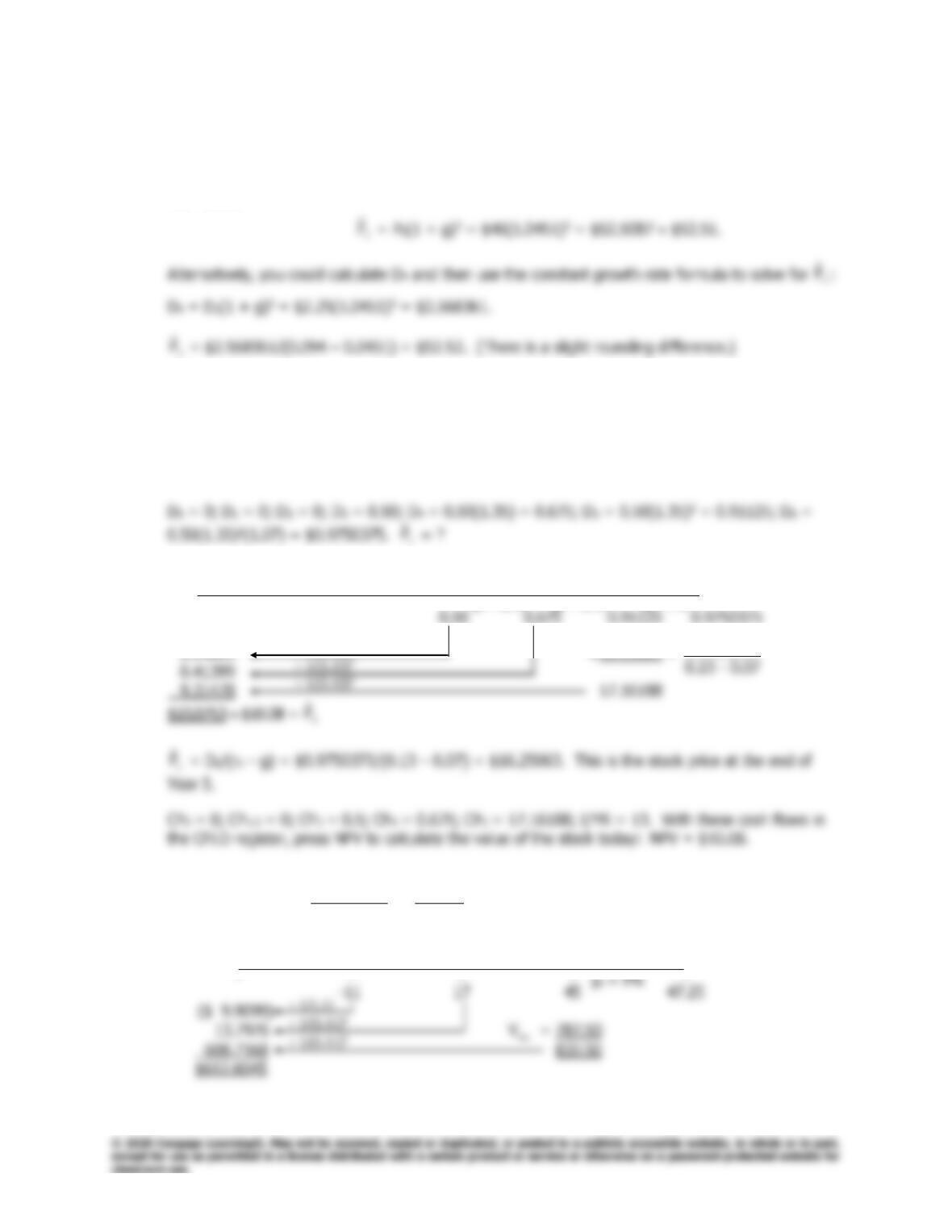

9-14 Calculate the dividend cash flows and place them on a time line. Also, calculate the stock price at the

end of the supernormal growth period, and include it, along with the dividend to be paid at t = 5, as

CF5. Then, enter the cash flows as shown on the time line into the cash flow register, enter the

required rate of return as I/YR = 13, and then find the value of the stock using the NPV calculation.

Be sure to enter CF0 = 0, or else your answer will be incorrect.

0 1 2 3 4 5 6

| | | | | | |

0

P

ˆ

5

P

ˆ

9-15 a. Horizon value =

05.011.0

)05.1(45$

−

=

06.0

25.47$

= $787.50 million.

b. 0 1 2 3 4

| | | | |

rs = 13%

gs = 35%

gn = 7%

9750375.0

1/(1.13)3

WACC = 11%

gs = 35%

234

Answers and Solutions

Chapter 9: Stocks and Their Valuation

9-16 The value of any asset is the present value of all future cash flows expected to be generated from the

asset. Hence, if we can find the present value of the dividends during the period preceding long-run

constant growth and subtract that total from the current stock price, the remaining value would be

the present value of the cash flows to be received during the period of long-run constant growth.

9-17 0 1 2 3 4

| | | | |

D0 = 2.00 D1 D2 D3 D4

3

P

ˆ

a. D1 = $2(1.05) = $2.10; D2 = $2(1.05)2 = $2.2050; D3 = $2(1.05)3 = $2.31525.

rs = 12%

g = 5%

Chapter 9: Stocks and Their Valuation

Answers and Solutions

235

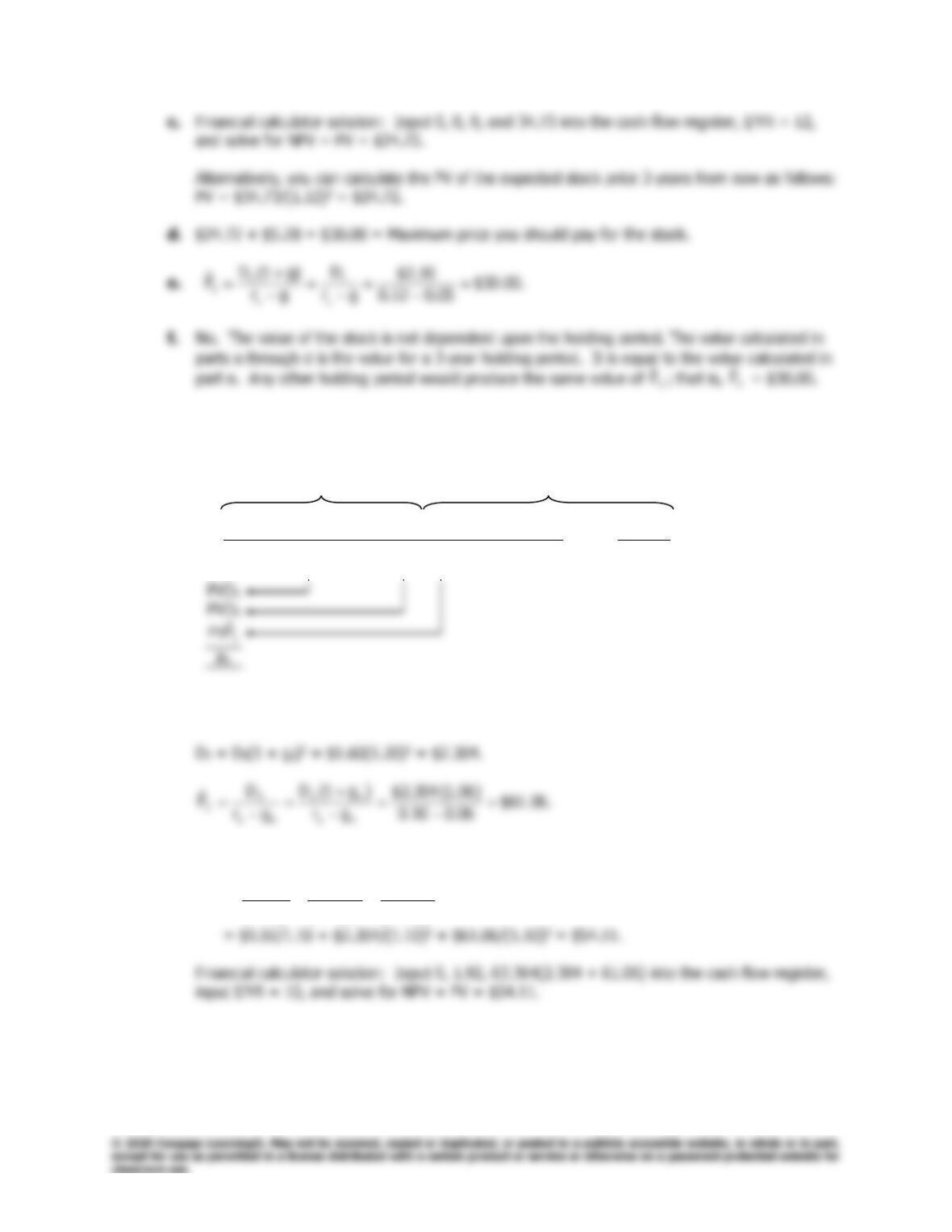

9-18 a. Part 1: Graphical representation of the problem:

Supernormal Normal

growth growth

0 1 2 3

| | | | • • • |

D0 D1 (D2 +

2

P

ˆ

) D3 D

D1 = D0(1 + gs) = $1.6(1.20) = $1.92.

0

P

ˆ

= PV(D1) + PV(D2) + PV(

2

P

ˆ

)

=

2

s

2

2

s

2

s

1

)r1(

P

ˆ

)r1(

D

)r1(

D

+

+

+

+

+

236

Answers and Solutions

Chapter 9: Stocks and Their Valuation

Part 2: Expected dividend yield:

D1/P0 = $1.92/$54.11 = 3.55%.

Second, find the capital gains yield:

11.54$60.57$

PP

ˆ

01 =

−

−

b. Due to the longer period of supernormal growth, the value of the stock will be higher for each

year. Although the total return will remain the same, rs = 10%, the distribution between

dividend yield and capital gains yield will differ: The dividend yield will start off lower and the

c. Throughout the supernormal growth period, the total yield, rs, will be 10%, but the dividend

yield is relatively low during the early years of the supernormal growth period and the capital

d. Some investors need cash dividends (retired people), while others would prefer growth. Also,

investors must pay taxes each year on the dividends received during the year, while taxes on

the capital gain can be delayed until the gain is realized. Currently (2018), dividends to

9-19 a. 0 1 2 3 4

| | | | |

3,000,000 6,000,000 8,000,000 16,000,000

WACC = 9%

Chapter 9: Stocks and Their Valuation

Answers and Solutions

237

Alternatively, calculate the PV of the FCFs in Years 1 through 4 as follows:

b. The firm’s horizon value is calculated as follows:

c. The market value of the firm’s operations is calculated as follows:

0 1 2 3 4 5

| | | | | |

3,000,000 6,000,000 8,000,000 16,000,000 16,480,000

d. To find Brandtly’s stock price, you need to first find the value of its equity. The value of

Brandtly’s equity is equal to the market value of the total firm less the market value of its debt

and preferred stock.

gn = 3%

WACC = 9%

238

Answers and Solutions

Chapter 9: Stocks and Their Valuation

9-20 FCF1 = EBIT(1 – T) + Depreciation –

esexpenditur

Capital

–

capital work ing

operatingNet

Since the firm has $200 million of non-operating assets, the firm’s total market value is

$7,875,000,000 + $200,000,000 = $8,075,000,000. Now find the market value of its equity.

9-21 a. End of Year: 19 20 21 22 23 24 25

| | | | | | |

D0 = 1.75 D1 D2 D3 D4 D5 D6

Dt = D0(1 + g)t.

D2020 = $1.75(1.15)1 = $2.01.

b. Step 1:

PV of dividends =

=+

5

1t

t

s

t

)r1(

D

.

rs = 12%

gs = 15%

gn = 5%

Chapter 9: Stocks and Their Valuation

Answers and Solutions

239

Step 2:

Expected P2024 = D2025/(rs – gn) = [D2024(1 + g)]/(rs – gn) = [$3.52(1.05)]/(0.12 – 0.05)

This is the price of the stock 5 years from now. The PV of this price, discounted back 5 years,

is as follows:

Step 3:

The price of the stock today is as follows:

0

P

ˆ

= PV dividends Years 2020–2024 + PV of Expected P2024

c. 2020

D1/P0 = $2.01/$39.43 = 5.10%

Capital gains yield = 6.90*

The main points to note here are as follows:

1. The total yield is always 12% (except for rounding errors).

240

Answers and Solutions

Chapter 9: Stocks and Their Valuation

Chapter 9: Stocks and Their Valuation

Comprehensive/Spreadsheet Problem

241

Comprehensive/Spreadsheet Problem

Note to Instructors:

The solution for part a of this problem is provided at the back of the text; however, the

solutions to parts b through d are not. Instructors can access the

Excel

file on the textbook’s

website.

9-22 a. 1. Find the price today.

gn6% Long-run g; for Year 3 and all following years.

2. Find the expected dividend yield.

Recall that the expected dividend yield is equal to the next expected annual dividend

divided by the price at the beginning of the period.

3. Find the expected capital gains yield.

The capital gains yield can be calculated by simply subtracting the dividend yield from the

expected total return.

rs10.0%

gS20% Short-run g; for Years 1-2 only.

PV of dividends

$1.7455