138

Comprehensive/Spreadsheet Problem

Chapter 6: Interest Rates

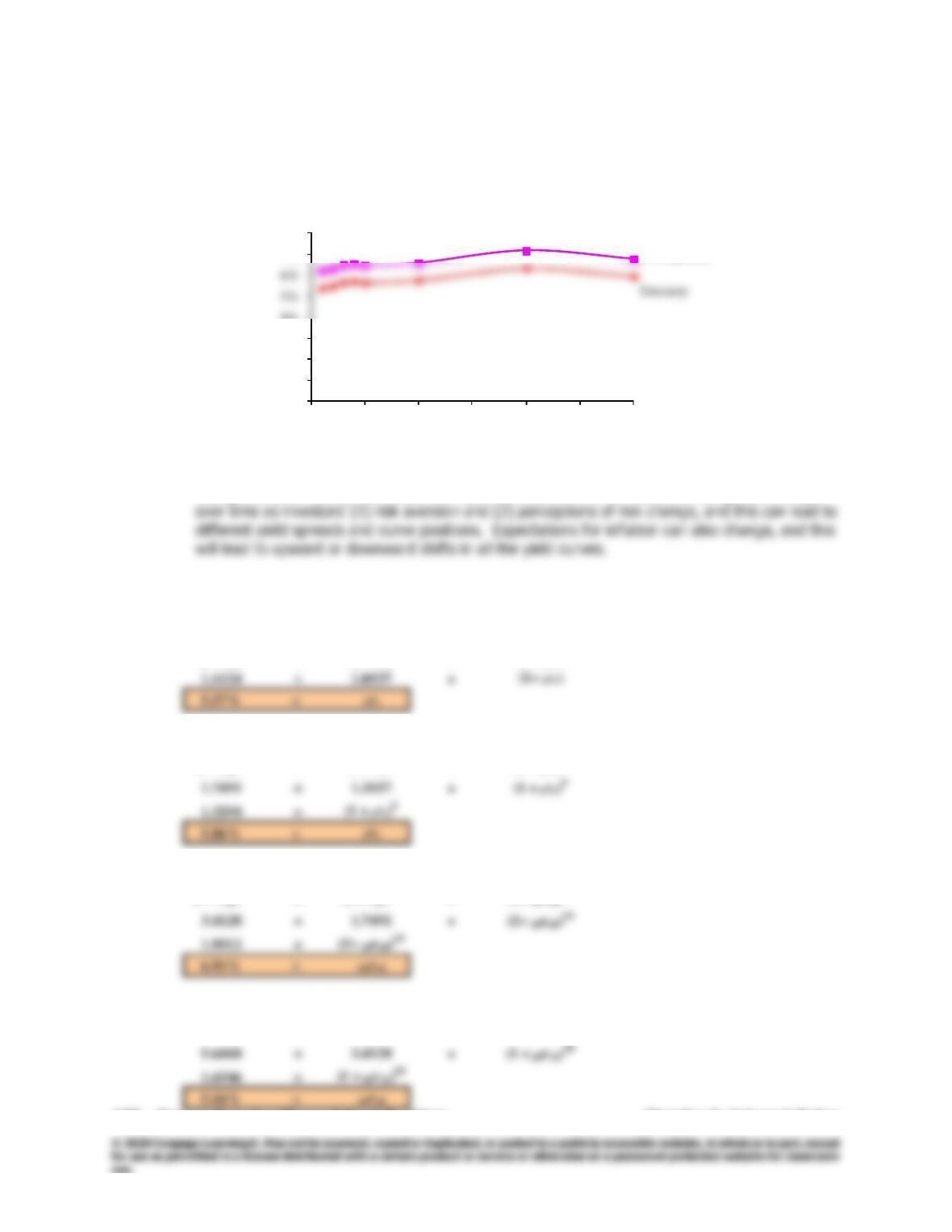

Now we can graph the data in the first 3 columns of the above table to get the Treasury and A-

rated Corporate yield curves:

0%

1%

2%

3%

4%

7%

8%

0 5 10 15 20 25 30

Interest Rate

Years to Maturity

Treasury and A-Rated Corporate Yield Curves

A Corporate

Note that if we constructed yield curves for corporate bonds with other ratings, the higher the

rating, the lower the curves would be. Note too that the DRP for different ratings can change

e. Short-term rates are more volatile than longer-term rates; therefore, the left side of the yield

curve would be most volatile over time.

f.

(1) The 1-year rate, 1 year from now

(1 + r2)2 = (1 + r1)×(1+ 1r1)

(2) The 5-year rate, 5 years from now

(1 + r10)10 = (1 + r5)5×(1 + 5r5)5

(3) The 10–year rate, 10 years from now

(1 + r20)20 = (1+ r10)10 ×(1+ 10r10)10

(4) The 10–year rate, 20 years from now

(1+ r30)30 = (1+ r20)20 ×(1 + 20r10)10

Chapter 6: Interest Rates

Integrated Case

139

Integrated Case

6-21

Morton Handley & Company

Interest Rate Determination

Maria Juarez is a professional tennis player, and your firm manages her

money. She has asked you to give her information about what determines

A. What are the four most fundamental factors that affect the cost of

money, or the general level of interest rates, in the economy?

Answer: [Show S6-1 through S6-3 here.] The four most fundamental

factors affecting the cost of money are (1) production

opportunities, (2) time preferences for consumption, (3) risk, and

(4) inflation.

Production opportunities are the investment opportunities in

productive (cash-generating) assets. Time preferences for

consumption are the preferences of consumers for current

140

Integrated Case

Chapter 6: Interest Rates

B. What is the real risk-free rate of interest (r*) and the nominal risk-

free rate (rRF)? How are these two rates measured?

Answer: [Show S6-4 and S6-5 here.] Keep these equations in mind as we

discuss interest rates. We will define the terms as we go along:

r = r* + IP + DRP + LP + MRP.

The nominal risk-free rate, rRF, is equal to the real risk-free

rate plus an inflation premium, which is equal to the average rate

Chapter 6: Interest Rates

Integrated Case

141

C. Define the terms

inflation premium (IP), default risk premium

(DRP), liquidity premium (LP), and maturity risk premium (MRP)

.

Which of these premiums is included in determining the interest

rate on (1) short-term U.S. Treasury securities, (2) long-term U.S.

Treasury securities, (3) short-term corporate securities, and (4)

long-term corporate securities? Explain how the premiums would

vary over time and among the different securities listed.

Answer: [Show S6-6 here.] The inflation premium (IP) is a premium added

to the real risk-free rate of interest to compensate for expected

inflation.

142

Integrated Case

Chapter 6: Interest Rates

3. The rate on short-term corporate securities is equal to the real

risk-free rate plus premiums for inflation, default risk, and

4. The rate for long-term corporate securities also includes a

premium for maturity risk. Thus, long-term corporate

D. What is the term structure of interest rates? What is a yield

curve?

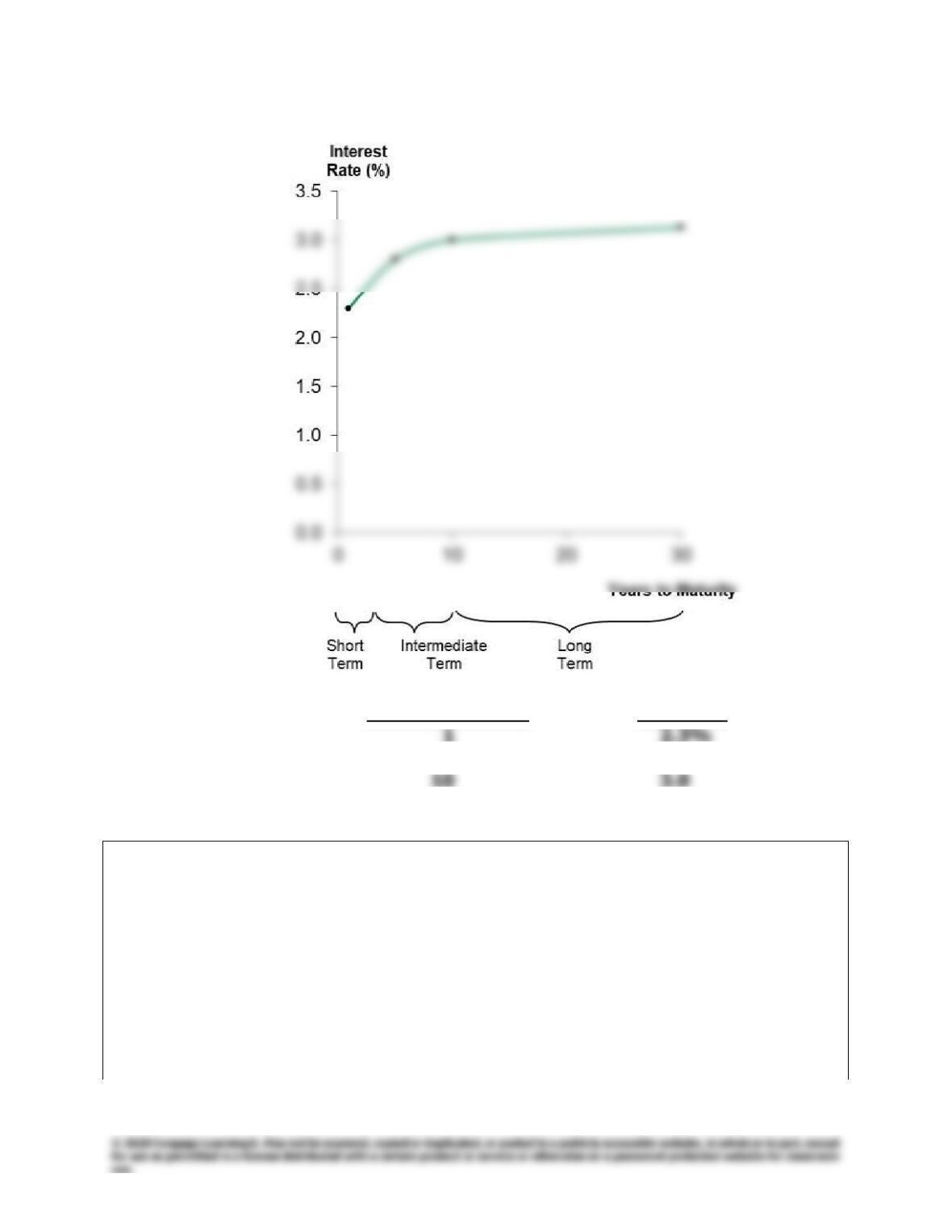

Answer: [Show S6-7 here. S6-7 shows a recent (May 2018) Treasury yield

curve.] The term structure of interest rates is the relationship

Chapter 6: Interest Rates

Integrated Case

143

Yield Curve for May 2018

Years to Maturity Yield

5 2.8

30 3.1

E. Suppose most investors expect the inflation rate to be 5% next

year, 6% the following year, and 8% thereafter. The real risk-free

rate is 3%. The maturity risk premium is zero for bonds that

mature in 1 year or less and 0.1% for 2-year bonds; then the MRP

increases by 0.1% per year thereafter for 20 years, after which it

is stable. What is the interest rate on 1-, 10-, and 20-year

Treasury bonds? Draw a yield curve with these data. What factors

144

Integrated Case

Chapter 6: Interest Rates

can explain why this constructed yield curve is upward-sloping?

Answer: [Show S6-8 through S6-13 here.]

Step 1: Find the average expected inflation rate over Years 1 to 20:

Yr 1: IP = 5.0%.

Yr 10: IP = (5 + 6 + 8 + 8 + 8 + . . . + 8)/10 = 7.5%.

Step 2: Find the maturity risk premium in each year:

Yr 1: MRP = 0.0%.

Chapter 6: Interest Rates

Integrated Case

145

146

Integrated Case

Chapter 6: Interest Rates

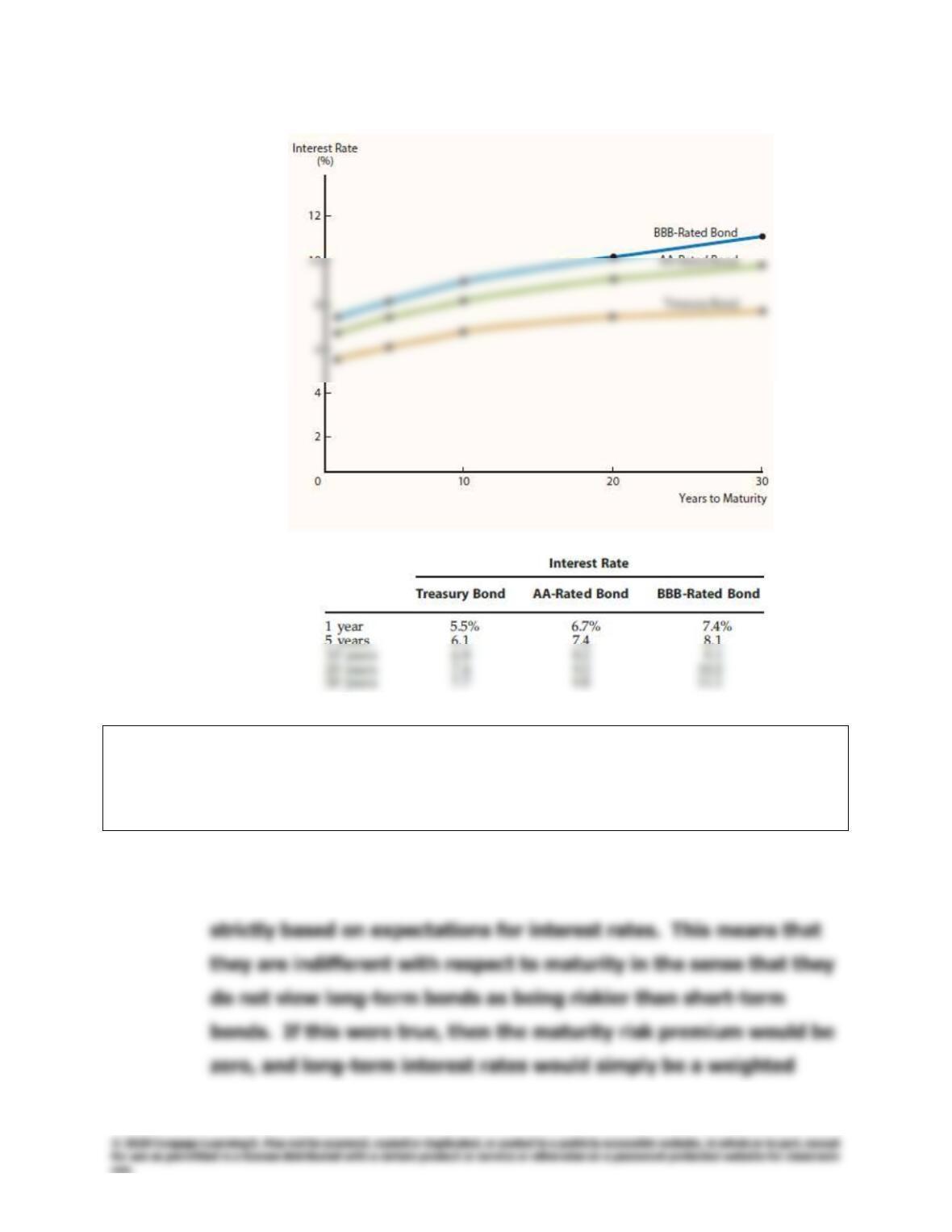

F. At any given time, how would the yield curve facing a AAA-rated

company compare with the yield curve for U.S. Treasury

securities? At any given time, how would the yield curve facing a

BB-rated company compare with the yield curve for U.S. Treasury

securities? Draw a graph to illustrate your answer.

Answer: [Show S6-14 and S6-15 here.] (Curves for AAA-rated and BB–

rated securities have been added to an illustrative yield curve to

demonstrate that riskier securities require higher returns.) The

yield curve normally slopes upward, indicating that short-term

Chapter 6: Interest Rates

Integrated Case

147

Illustrative Corporate and Treasury Yield Curves

G. What is the pure expectations theory? What does the pure

expectations theory imply about the term structure of interest

rates?

Answer: [Show S6-16 and S6-17 here.] The pure expectations theory

assumes that investors establish bond prices and interest rates

H. Suppose you observe the following term structure for Treasury

securities:

Maturity Yield

1 year 6.0%

2 years 6.2

3 years 6.4

4 years 6.5

5 years 6.5

Assume that the pure expectations theory of the term structure is

correct. (This implies that you can use the yield curve provided to

“back out” the market’s expectations about future interest rates.)

What does the market expect will be the interest rate on 1-year

securities, 1 year from now? What does the market expect will be

the interest rate on 3-year securities, 2 years from now? Calculate

these yields using geometric averages.

Answer: [Show S6-18 through S6-21 here.] Calculation for r on 1-year

securities one year from now:

(1.062)2 = (1.06)(1 + X)

Chapter 6: Interest Rates

Integrated Case

149

Calculation for r on 3-year securities two years from now:

(1.065)5 = (1.062)2(1 + X)3

I. Describe how macroeconomic factors affect the level of interest

rates. How do these factors explain why interest rates have been

lower in recent years?

Answer: [Show S6-22 and S6-23 here.] Expected inflation, default risk,

maturity risk, and liquidity concerns influence the level of interest

rates over time and across different markets. Macroeconomic

150

Integrated Case

Chapter 6: Interest Rates

increases the demand for funds and pushes interest rates up. If

the government prints money the result will be increased inflation.

The larger the foreign trade deficit, the more money the U.S.

must borrow. Foreigners will only hold U.S. debt if and only if U.S.

The Fed has been printing money—increasing the money

supply. As a result, short-term rates are quite low. However, at

some point, interest rates will rise due to inflationary pressure.

In fact, the Federal Reserve stopped its policy of quantitative