Answers and Solutions: 12 – 1

Chapter 12

Corporate Valuation and Financial Planning

ANSWERS TO END-OF-CHAPTER QUESTIONS

12-1 a. The operating plan provides detailed implementation guidance designed to

accomplish corporate objectives. It details who is responsible for what particular

function, and when specific tasks are to be accomplished. The financial plan details

the financial aspects of the corporation’s operating plan.

b. Spontaneous liabilities are the first source of expansion capital as these accounts

will be lower. A firm’s payout ratio is calculated as dividends per share divided by

earnings per share. The less of its income a company distributes as dividends, the

larger its addition to retained earnings. Therefore, the firm’s need for external

financing will be lower.

Answers and Solutions: 12 – 2

needed

increase

liab. sspontaneou

earnings

AFN = (A0*/S0)S – (L0*/S0)S – MS1(1 – Payout rate)

Capital intensity is the dollar amount of assets required to produce a dollar of sales.

The capital intensity ratio is the reciprocal of the total assets turnover ratio. It is

calculated as Assets/Sales. The sustainable growth rate is the maximum growth rate

the firm could achieve without having to raise any external capital. A firm’s self-

supporting growth rate can be calculated as follows:

Self-supporting g =

)S)(POR1(M *L *A

)S)(POR1(M

000

0

−−−

−

d. The forecasted financial statement approach using percent of sales develops a

complete set of financial statements that can be used to calculate projected EPS, free

cash flow, various other financial ratios, and a projected stock price. This approach

first forecasts sales, the required assets, the funds that will be spontaneously

generated, and then net income, dividends, and retained earnings.

e. A firm has excess capacity when its sales can grow before it must add fixed assets

Answers and Solutions: 12 – 3

12-2 Accounts payable, accrued wages, and accrued taxes increase spontaneously. Retained

earnings may or may not increase, depending on profitability and dividend payout policy.

12-3 The equation gives good forecasts of financial requirements if the ratios A0*/S and L0*/S,

the profit margin, and payout ratio are stable. This equation assumes that ratios are

12-4 The five key factors that impact a firm’s external financing requirements are: Sales

growth, capital intensity, spontaneous liabilities-to-sales ratio, profit margin, and payout

ratio.

12-5 The self-supporting growth rate is the maximum rate a firm can achieve without having

to raise external capital. The self-supporting growth rate is calculated using the AFN

equation, setting AFN equal to zero, replacing the term ΔS with the term g × S0, and

replacing the term S1 with S0 × (1 + g). Once the AFN equation is rewritten with these

modifications, you can now solve for g. This “g” obtained is the firm’s self-supporting

growth rate.

Answers and Solutions: 12 – 4

SOLUTIONS TO END-OF-CHAPTER PROBLEMS

12-2 AFN =

000,000,8$

000,000,7$

$1,200,000 –

000,000,8$

000,900$

$1,200,000 – 0.06($9,200,000)(1 – 0.4)

= (0.875)($1,200,000) – $135,000 – $331,200

= $1,050,000 – $466,200

= $583,800.

The capital intensity ratio is measured as A0*/S0. This firm’s capital intensity ratio is

higher than that of the firm in Problem 9-1; therefore, this firm is more capital

intensive—it would require a large increase in total assets to support the increase in

sales.

12-4 S0 = $5,000,000; A0* = $2,500,000; CL = $700,000; NP = $300,000; AP = $500,000;

Accruals = $200,000; M = 7%; payout ratio = 80%; A0*/S0 = 0.50; L0* = (AP +

Accruals)/S0 = ($500,000 + $200,000)/$5,000,000 = 0.14.

AFN = (A0*/S0)∆S – (L0*/S0)∆S – (M)(S1)(1 – payout rate)

= (0.50)∆S – (0.14) ∆S – (0.07)(S1)(1 – 0.8)

= (0.50)∆S – (0.14)∆S – (0.014)S1

000,000,8$

000,000,5$

000,000,8$

Answers and Solutions: 12 – 5

Sales can increase by $5,202,312 – $5,000,000 = $202,312 without additional funds

being needed.

b. Assets/Sales (A0*/S0) = $2,170,000/$3,500,000 = 62%.

L0*/Sales = $560,000/$3,500,000 = 16%.

2014 Sales = (1.35)($3,500,000) = $4,725,000.

AFN = (A0*/S0)(∆S) – (L0*/S0)(∆S) – (M)(S1)(1 – payout) – New common stock

= (0.62)($1,225,000) – (0.16)($1,225,000) – (0.05)($4,725,000)(0.55) – $195,000

= $759,500 – $196,000 – $129,937 – $195,000 = $238,563.

Alternatively, using the forecasted financial statement method:

Forecast

Basis % Additions (New

2013 2014 Sales Financing, R/E) 2014

Total assets $2,170,000 0.62 $2,929,500

Answers and Solutions: 12 – 6

12-6 Cash $ 100.00 2.0 = $ 200.00

Accounts receivable 200.00 2.0 = 400.00

Inventories 200.00 2.0 = 400.00

Net fixed assets* 500.00 1.0 = 500.00

Total assets $1,000.00 $1,500.00

Target FA = 0.25($2,000) = $500 = Required FA. Since the firm currently has $500 of

fixed assets, no new fixed assets will be required.

**Addition to RE = (M)(S1)(1 – Payout ratio) = 0.05($2,000)(0.4) = $40.

12-7 a. AFN = (A0*/S0)(S) – (L0*/S0)(S) – (M)(S1)(1 – payout)

=

350$

5.122$

($70) –

350$

5.17$

($70) –

350$

5.10$

($420)(0.6) = $13.44 million.

Answers and Solutions: 12 – 7

c. Upton Computers

Pro Forma Balance Sheet

December 31, 2014

(Millions of Dollars)

2013

Forecast

Basis %

2014 Sales

Additions

2014 Pro

Forma

Financing

2014 Pro

Forma after

Financing

Cash

$ 3.5

0.0100

$ 4.20

$ 4.20

Receivables

26.0

0.0743

31.20

31.20

Inventories

58.0

0.1657

69.60

69.60

Total current assets

$ 87.5

$105.00

$105.00

Net fixed assets

35.0

0.100

42.00

42.00

Total assets

$122.5

$147.00

$147.00

Accounts payable

$ 9.0

0.0257

$ 10.80

$ 10.80

Notes payable

18.0

18.00

18.00

Line of credit

+13.44

Accruals

8.5

0.0243

10.20

10.20

Total current liabilities

$ 35.5

$ 39.00

$ 52.44

Mortgage loan

Common stock

15.0

15.00

15.00

Total liab. and equity

$122.5

$133.56

$147.00

$ 13.44

Answers and Solutions: 12 – 8

12-8 Stevens Textiles

Pro Forma Income Statement

December 31, 2014

(Thousands of Dollars)

a.

2014

Forecast 2014

2013 Basis Pro Forma

Sales $36,000 1.15 Sales13 $41,400

Operating costs 32,440 0.9011 Sales14 37,306

Answers and Solutions: 12 – 9

Stevens Textiles

Pro Forma Balance Sheet

December 31, 2014

(Thousands of Dollars)

2013

Forecast

Basis %

2014 Sales

Additions

2014 Pro

Forma

2014

Financing

2014 Pro

Forma after

Financing

Cash

$ 1,080

0.0300

$ 1,242

$ 1,242

Accts receivable

6,480

0.1800

7,452

7,452

Inventories

9,000

0.2500

10,350

10,350

Total curr. assets

$16,560

$19,044

$19,044

Fixed assets

12,600

0.3500

14,490

14,490

*From income statement.

b. Line of credit = $2,128 (thousands of $).

c. If debt is added throughout the year rather than only at the end of the year, interest

Total assets

$29,160

$33,534

$33,534

Accounts payable

$ 4,320

0.1200

$ 4,968

$ 4,968

Accruals

2,880

0.0800

3,312

3,312

Line of credit

+2,128

Notes payable

2,100

2,100

Total curr. liabilities

$ 9,300

$10,380

$12,508

Long-term debt

3,500

3,500

3,500

Total debt

$12,800

$13,880

$16,008

Common stock

3,500

3,500

3,500

Retained earnings

12,860

14,026

14,026

Total liab. and equity

$29,160

$31,406

$33,534

Deficit =

$ 2,128

Answers and Solutions: 12 – 10

12-9 Garlington Technologies Inc.

Pro Forma Income Statement

December 31, 2014

Forecast Pro Forma

2013 Basis 2014

Sales $3,600,000 1.10 Sales13 $3,960,000

Operating costs 3,279,720 0.911 Sales14 3,607,692

Garlington Technologies Inc.

Pro Forma Balance Statement

December 31, 2014

Forecast

Basis % AFN With AFN

2013 2014 Sales Additions 2014 Effects 2014

Cash $ 180,000 0.05 $ 198,000 $ 198,000

Receivables 360,000 0.10 396,000 396,000

Inventories 720,000 0.20 792,000 792,000

Total curr. assets $1,260,000 $1,386,000 $1,386,000

Fixed assets 1,440,000 0.40 1,584,000 1,584,000

*See income statement.

Answers and Solutions: 12 – 11

SOLUTION TO SPREADSHEET PROBLEMS

12-11 The detailed solution for is available in the file Ch12 P10 Build a Model Solution.xls at

the textbook’s Web site.

Mini Case: 12 – 12

MINI CASE

Hatfield Medical Supplies’s stock price had been lagging its industry averages, so its

board of directors brought in a new CEO, Jaiden Lee. Lee had brought in Ashley Novak, a

finance MBA who had been working for a consulting company, to replace the old CFO, and

Lee asked Ashley to develop the financial planning section of the strategic plan. In her

previous job, Novak’s primary task had been to help clients develop financial forecasts, and

that was one reason Lee hired her.

Novak began as she always did, by comparing Hatfield’s financial ratios to the

industry averages. If any ratio was substandard, she discussed it with the responsible manager

to see what could be done to improve the situation. The following data shows Hatfield’s latest

financial statements plus some ratios and other data that Novak plans to use in her analysis.

Hatfield Medical Supplies (Millions of Dollars Except Per Share Data)

Balance Sheet, 12/31/2013

Income Statement, Year Ending 2013

Cash

$ 20

Sales

$2,000

Accts. rec.

280

Op. costs (excl. depr.)

1,800

Inventories

400

Depreciation

50

Total CA

$ 700

EBIT

$ 150

Net fixed assets

500

Interest

Total assets

$1,200

Pretax earnings

$ 110

Taxes (40%)

Accts. pay. & accruals

$ 80

Net income

$ 66

Line of credit

Total CL

$ 80

Dividends

$20.0

Long-term debt

500

Add. to RE

$46.0

Total liabilities

$ 580

Common shares

Common stock

420

EPS

$6.60

Retained earnings

200

DPS

$2.00

Total common equ.

$620

Ending stock price

$52.80

Total liab. & equity

$1,200

Mini Case: 12 – 13

Selected Additional Data for 2013

Hatfield

Industry

Hatfield

Industry

Op. costs/Sales

90.0%

88.0%

Total liability/Total assets

48.3%

36.7%

Depr./FA

10.0%

12.0%

Times interest earned

3.8

8.9

Cash/Sales

1.0%

1.0%

Return on assets (ROA)

5.5%

10.2%

Note: Hatfield was operating at full capacity in 2013. Also, you may observe small differences in items like the ROE

when calculated in different ways. Any such differences are due to rounding, and they can be ignored.

Receivables/Sales

14.0%

11.0%

Profit margin (M)

3.30%

4.99%

Inventories/Sales

20.0%

15.0%

Sales/Assets

2.04

Fixed assets/Sales

25.0%

22.0%

Assets/Equity

1.94

Acc. pay. & accr. / Sales

4.0%

4.0%

Return on equity (ROE)

10.6%

16.1%

Tax rate

40.0%

40.0%

P/E ratio

8.0

16.0

ROIC

8.0%

12.5%

NOPAT/Sales

4.5%

5.6%

Total op. capital/Sales

56.0%

45.0%

Mini Case: 12 – 14

a. Using Hatfield’s data and its industry averages, how well run would you say

Hatfield appears to be in comparison with other firms in its industry? What are its

primary strengths and weaknesses? Be specific in your answer, and point to various

ratios that support your position. Also, use the Du Pont equation (see Chapter 3) as

one part of your analysis.

Answer: The Du Pont equation shows the relationship among asset management, profitability

ratios, and leverage. By examining this equation we can determine where Hatfield falls

short of the industry.

Mini Case: 12 – 15

b. Use the AFN equation to estimate Hatfield’s required new external capital for 2014

if the sale growth rate is 10%. Assume that the firm’s 2013 ratios will remain the

same in 2014. (Hint: Hatfield was operating at full capacity in 2013.)

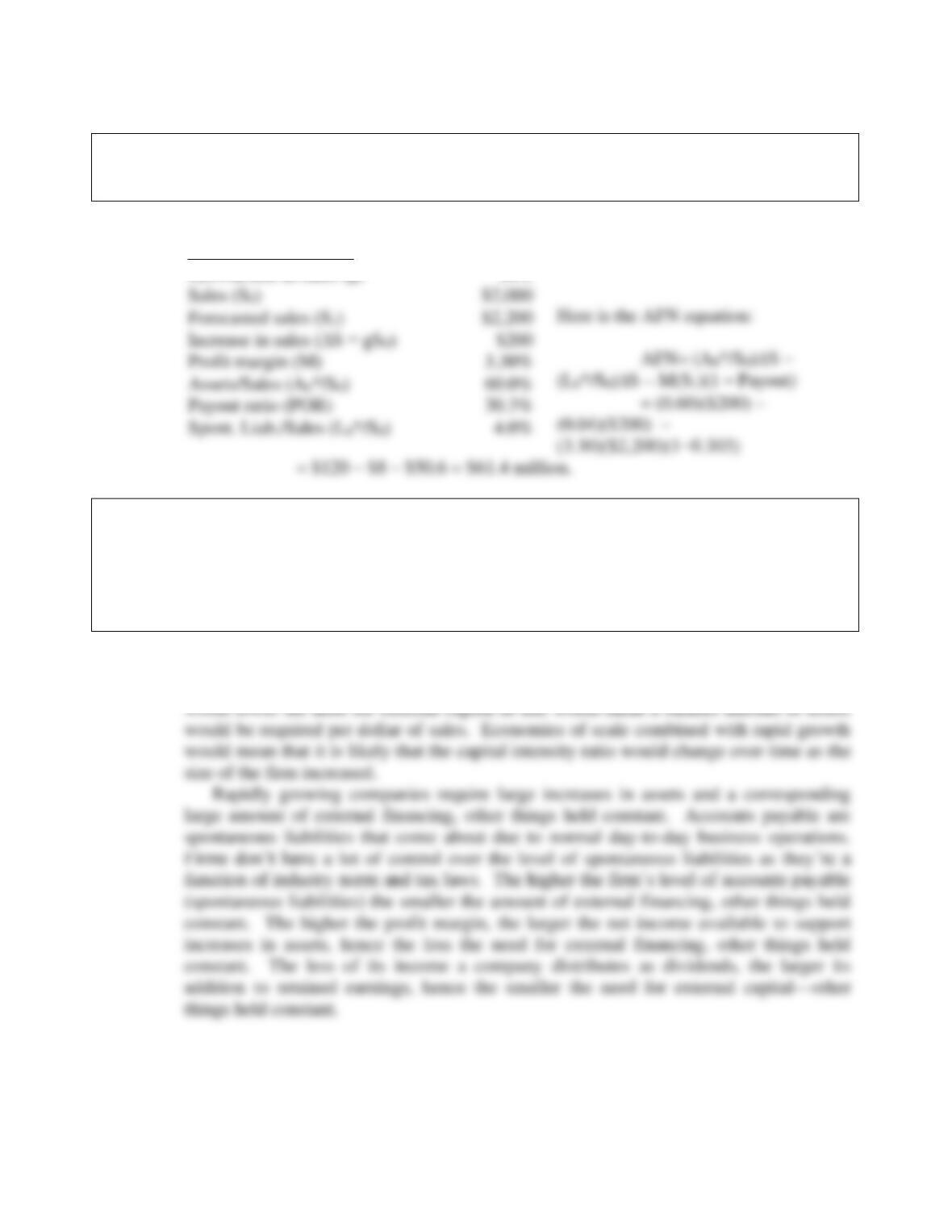

Answer:

Here is the AFN equation:

c. Define the term capital intensity. Explain how a decline in capital intensity would

affect the AFN, other things held constant. Would economies of scale combined

with rapid growth affect capital intensity, other things held constant? Also, explain

how changes in each of the following would affect AFN, holding other things

constant: the growth rate, the amount of accounts payable, the profit margin, and

the payout ratio.

Answer: The capital intensity ratio is the amount of assets required per dollar of sales, A0*/S0, and

it has a major effect on capital requirements. A decline in the capital intensity ratio

Data for AFN Method

Growth rate in sales (g)

10%

Sales (S0)

Forecasted sales (S1)

Profit margin (M)

Payout ratio (POR)

Spont. Liab./Sales (L0*/S0)

Mini Case: 12 – 16

d. Define the term self-supporting growth rate. What is Hatfield’s self-supporting

growth rate? Would the self-supporting growth rate be affected by a change in the

capital intensity ratio or the other factors mentioned in the previous question?

Other things held constant, would the calculated capital intensity ratio change over

time if the company were growing and were also subject to economies of scale

and/or lumpy assets?

Answer: The self-supporting growth rate is the maximum growth rate the firm could achieve if it

had no access to external capital. From the data given, Hatfield’s self-supporting growth

rate is calculated as:

Self-supporting g = [M(1 – POR)(S0)]/[A0* – L0* – M(1 – POR)(S0)]

Mini Case: 12 – 17

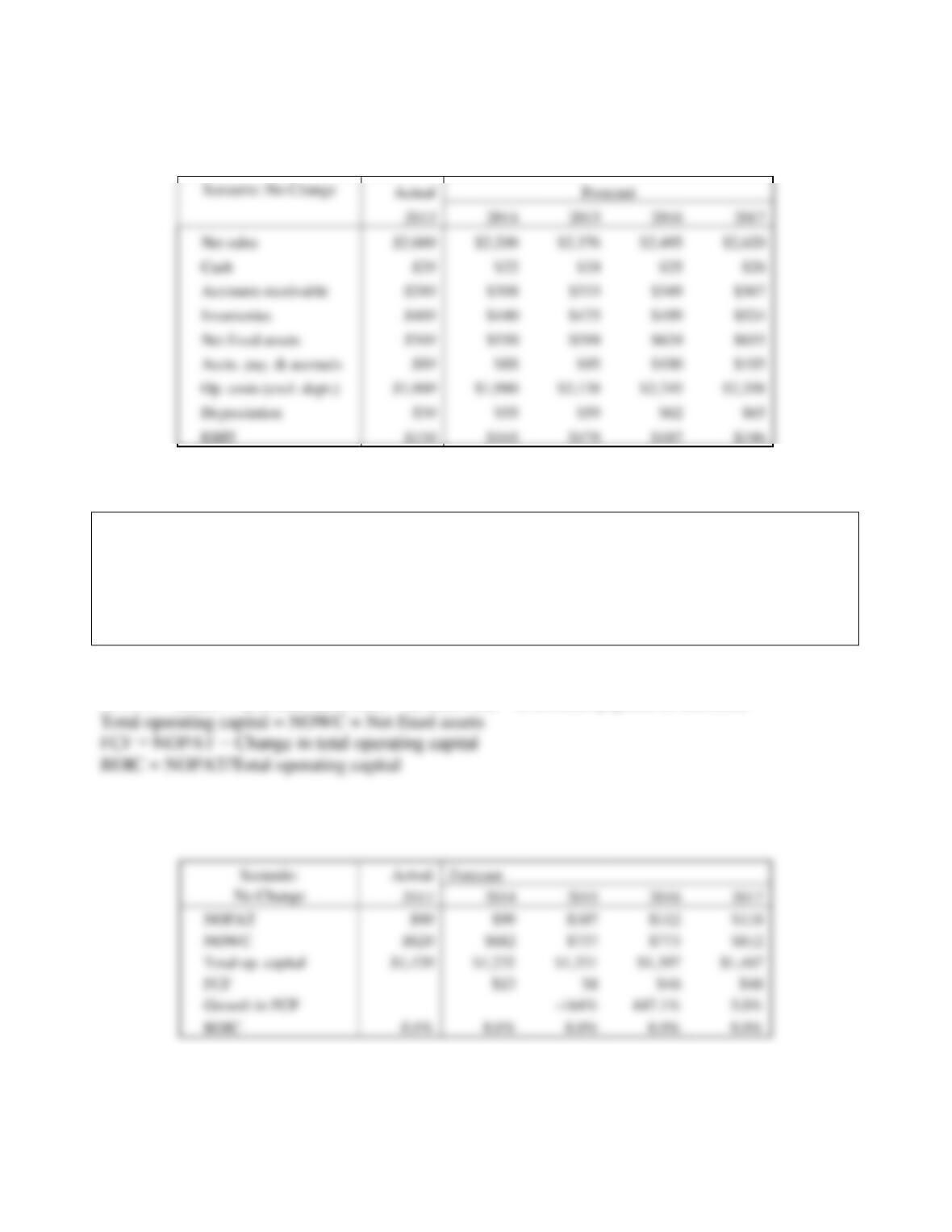

e. Use the following assumptions to answer the questions below: (1) Operating ratios

remain unchanged. (2) Sales will grow by 10%, 8%, 5%, and 5% for the next four

years. (3) The target weighted average cost of capital (WACC) is 9%. This is the

No Change scenario because operations remain unchanged.

Actual

Forecast

Inputs

2013

2014

2015

2016

2017

Sales growth rate:

10%

8%

5%

5%

Op. costs/Sales:

90%

90%

90%

90%

90%

e. 1. For each of the next four years, forecast the following items: sales, cash, accounts

receivable, inventories, net fixed assets, accounts payable & accruals, operating

costs (excluding depreciation), depreciation, and earnings before interest and taxes

(EBIT).

Forecast sales as Salest = Salest-1(1+gt). For example, Sales2014 = $2,000(1+0.10) =

$2,200.

Depr./FA

10%

10%

10%

10%

10%

Acct. rec. /Sales

14%

14%

14%

14%

14%

Inv./Sales:

20%

20%

20%

20%

20%

FA/Sales:

25%

25%

25%

25%

25%

AP & accr. / Sales:

4%

4%

4%

4%

Tax rate:

40%

40%

40%

40%

40%

Rate on all debt

8%

8%

8%

Div. growth rate:

10%

10%

10%

10%

Target WACC

9%

Mini Case: 12 – 18

e. 2. Using the previously forecasted items, calculate for each of the next four years the

net operating profit after taxes (NOPAT), net operating working capital, total

operating capital, free cash flow, (FCF), annual growth rate in FCF, and return on

invested capital. What does the forecasted free cash flow in the first year imply

about the need for external financing? Compare the forecasted ROIC compare

with the WACC. What does this imply about how well the company is performing?

NOPAT = EBIT(1-T)

NOWC = (Cash + accounts receivable + inventories) − (Accounts payable & accruals)

Mini Case: 12 – 19

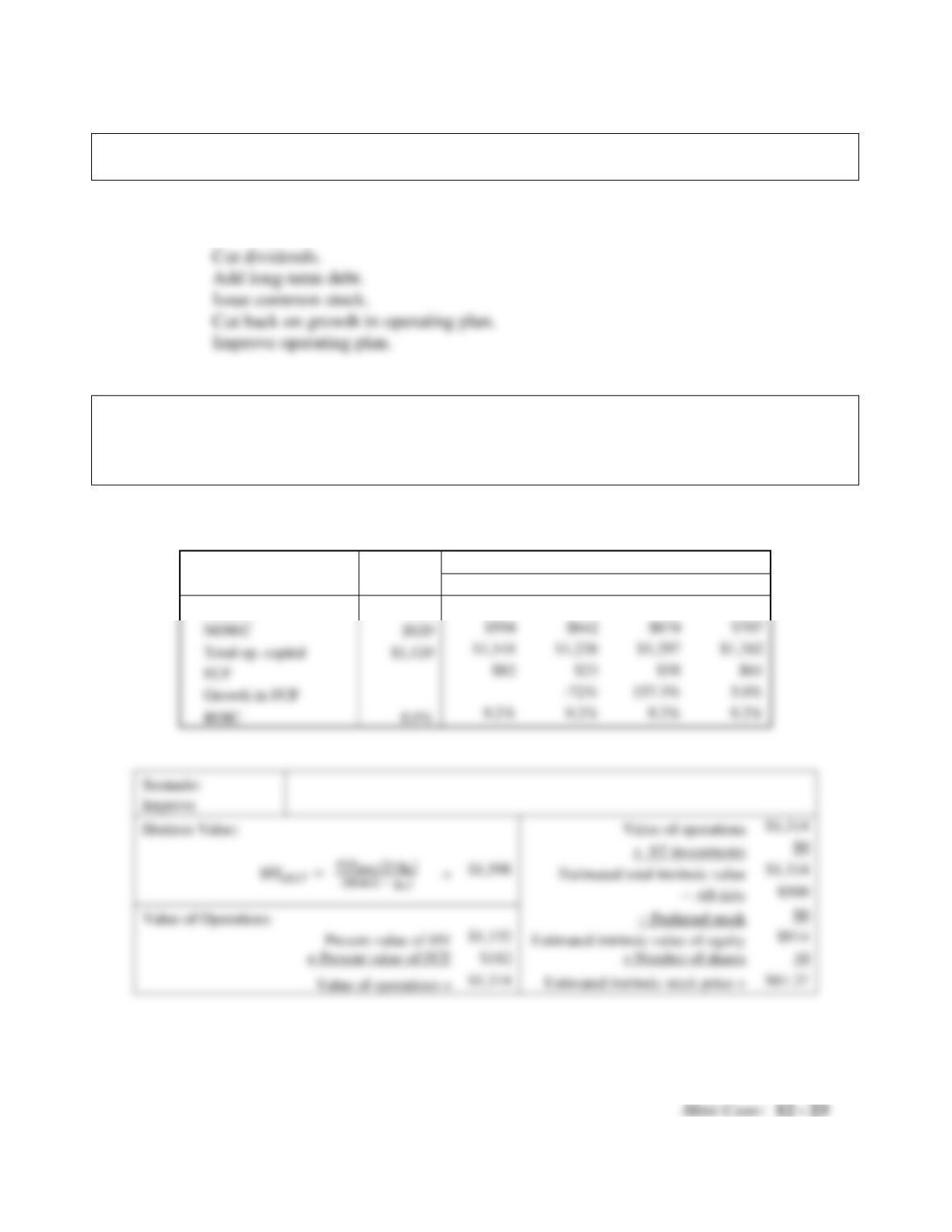

e. 3. Assume that FCF will continue to grow at the growth rate for the last year in the

forecast horizon (Hint: 5%). What is the horizon value at 2017? What is the present

value of the horizon value? What is the present value of the forecasted FCF? (Hint:

use the free cash flows for 2014 through 2017). What is the current value of

operations? Using information from the 2013 financial statements, what is the

current estimated intrinsic stock price?

With no rounding in intermediate steps, FCF2017 = $48.025.

HV2017 = FCF2017(1 + gL)

(WACC − gL)=$48.025(1 + 0.05)

(0.09 − 0.05)=$1,261

Mini Case: 12 – 20

f. Continue with the same assumptions for the No Change scenario from the previous

question, but now forecast the balance sheet and income statements for 2014 (but

not for the following three years) using the following preliminary financial policy.

(1) Regular dividends will grow by 10%. (2) No additional long-term debt or

common stock will be issued. (3) The interest rate on all debt is 8%. (4) Interest

expense for long-term debt is based on the average balance during the year. (5) If

the operating results and the preliminary financing plan cause a financing deficit,

eliminate the deficit by drawing on a line of credit. The line of credit would be

tapped on the last day of the year, so it would create no additional interest expenses

for that year. (6) If there is a financing surplus, eliminate it by paying a special

dividend. After forecasting the 2014 financial statements, answer the following

questions.

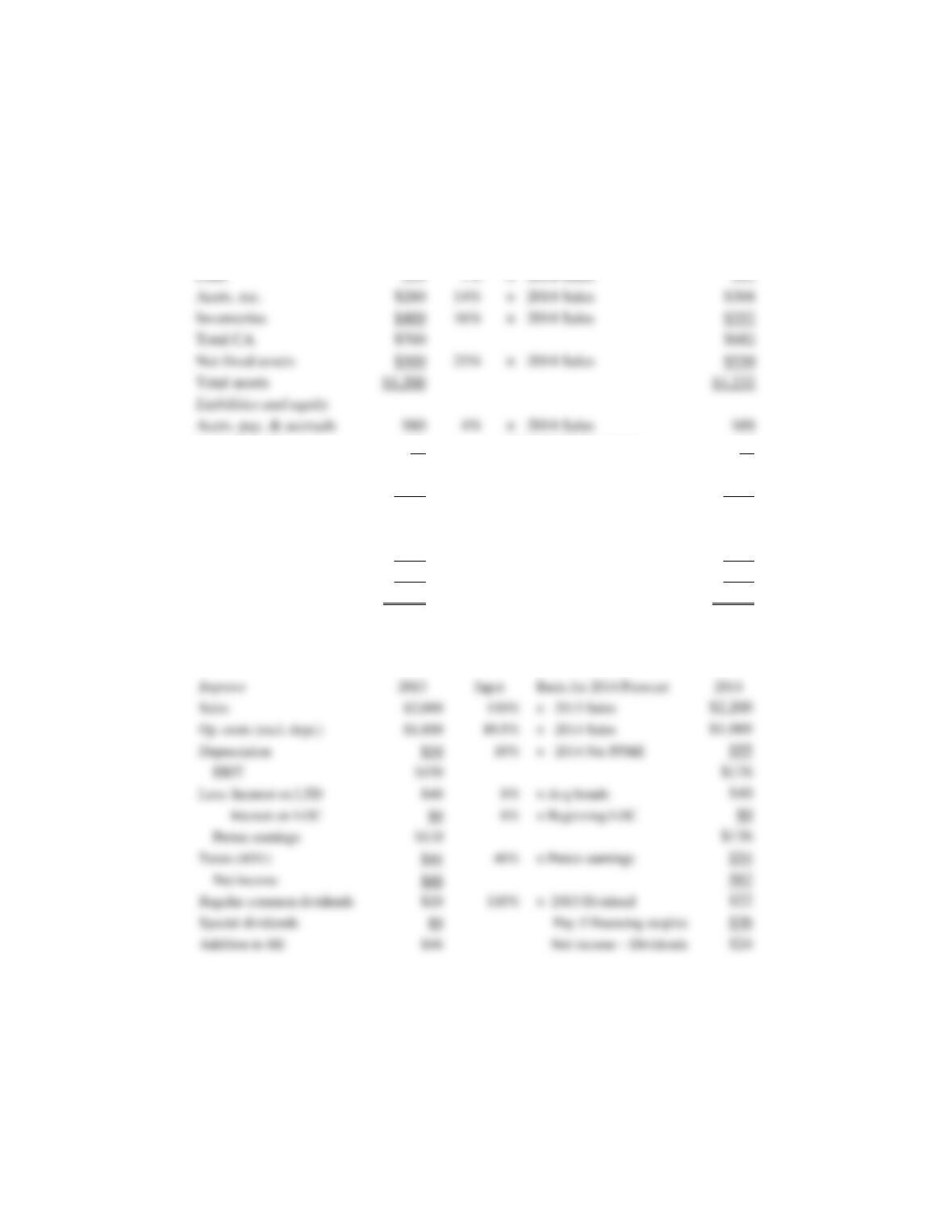

f. 1. How much will Hatfield need to draw on the line of credit?

Answer: Forecast sales and then items on the balance sheet. The forecast of sales is $2,200.

Forecast the operating items as a percent of sales. The preliminary financial policy

specifies no change in the long-term debt or common stock. Retained earnings increase

by the addition to retained earnings from the forecasted income statement. Leave the line

of credit blank for now.

Mini Case: 12 – 21

the interest rate and the average balance on the long-term debt (i.e., the average of the

beginning value and the ending value). Pay a regular dividend. Leave the special

dividend blank for now.

The next step is to identify the financing surplus or deficit. Start with the additions to

operating assets, subtract the increase in spontaneous liabilities (accounts payable and

accruals), subtract any new external financing from long-term debt or common stock,

and subtract the amount of reinvested net income (the amount that is not paid out in

common dividends). The result is the financing deficit (if it is negative) or the financing

surplus (if it is positive). If there is a deficit, draw on the LOC. If there is a surplus, pay a

special dividend.

Mini Case: 12 – 22

There is a deficit of $59, so update the balance sheets by adding $59 to the line of credit.

Because the LOC is added at the end of the year, there is no additional interest, so there

is no need to update the income statement. If the LOC were instead added earlier in the

year, there would be additional interest, which would cause lower net income, which

would cause a lower addition to retained earnings, which would cause a bigger financial

deficit. This is called financing feedback. See Ch12 Tool Kit.xls and look at the

worksheet CFO Model for a simple way to resolve financing feedback and for an

extension of the 1-year forecasted financial statements to multiple years.

f. 2. What are some alternative ways than those in the preliminary financial policy that

Hatfield might choose to eliminate the financing deficit?

Answer: Here are some alternative ways to eliminate the deficit:

Cut dividends.

g. Repeat the analysis performed the previous question but now assume that Hatfield

is able to improve the following inputs: (1) reduce operating costs (excluding

depreciation)/sales to 89.5% at a cost of $40 million; and (2) reduce

inventories/sales to 16% at a cost of $10 million. This is the Improve scenario.

Answer: The impact on the operating plan is shown below:

Scenario:

Actual

Forecast

Improve

2013

2014

2015

2016

2017

NOPAT

$90

$106

$114

$120

$126

NOWC

$594

$642

$674

$707

Total op. capital

FCF

Growth in FCF

ROIC

Scenario:

Horizon Value:

Value of Operations:

Mini Case: 12 – 24

The impact on the financial statements is shown below.

Scenario:

Improve

Assets

2013

Input

Basis for 2014 Forecast

2014

Line of credit

$0

Add LOC if fin. deficit

$0

Total CL

$80

$88

Long-term debt

$500

No Change

$500

Total liabilities

$580

$588

Common stock

$420

No Change

$420

Retained earnings

$200

Old RE + Add. to RE

$224

Total common equity

$620

$644

Total liabs. & equity

$1,200

$1,232

Check: TA − TL & Equ.

$0

Cash

$20

$22

Accts. rec.

$280

$308

Inventories

$400

$352

Total CA

$700

$682

Net fixed assets

$500

$550

Total assets

$1,200

$1,232

Liabilities and equity

Accts. pay. & accruals

$80

$88

Mini Case: 12 – 25

g. 1. Should Hatfield implement the plans? How much value would they add to the

company?

Answer: Improvement in value of operations: $1,314 − $958 = $356

g. 2. How much can Hatfield pay as a special dividend in the Improve Scenario? What

else might Hatfield do with the financing surplus?

Answer: Hatfield can pay a special dividend of $35. Instead, Hatfield could repurchase stock,

repay debt, or purchase marketable securities.