Solution 12/7/2012

Chapter: 12

Problem: 10

Key Input Data: Used in the

forecast

Tax rate 40%

Dividend growth rate 8%

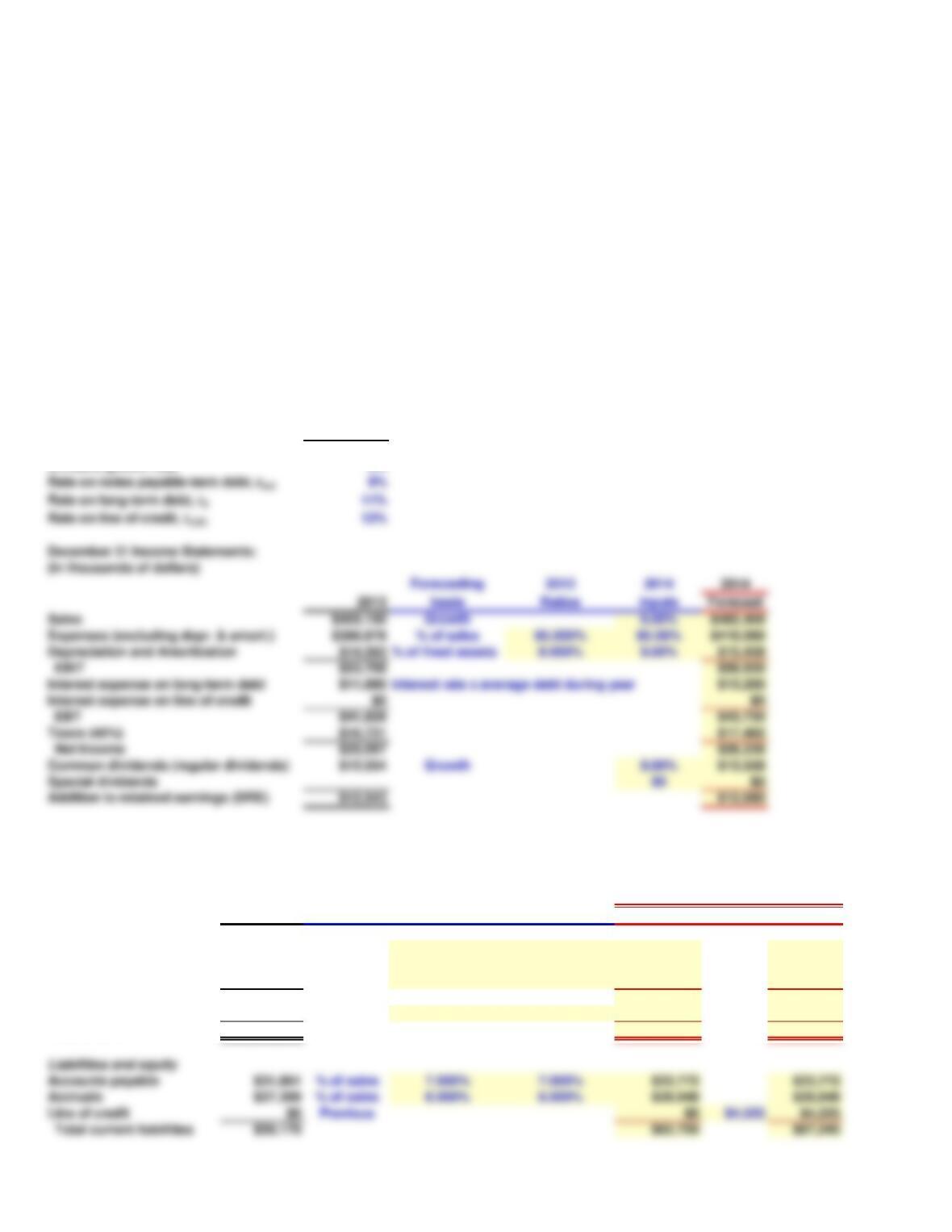

December 31 Balance Sheets

(in thousands of dollars)

Forecasting 2013 2014 2014

2013 basis Ratios Inputs Without adj. Adj. With Adj.

Assets:

Cash $18,206 % of sales 4.000% 4.000% $19,298 $19,298

Accounts Receivable $100,133 % of sales 22.000% 22.000% $106,141 $106,141

Inventories $45,515 % of sales 10.000% 10.000% $48,246 $48,246

Total current assets $163,854 $173,685 $173,685

Fixed assets $182,060 % of sales 40.000% 40.000% $192,984 $192,984

Total assets $345,914 $366,669 $366,669

Accounts payable $31,861 % of sales 7.000% 7.000% $33,772 $33,772

Accruals $27,309 % of sales 6.000% 6.000% $28,948 $28,948

Line of credit $0 Previous $0 $4,525 $4,525

Total current liabilities $59,170 $62,720 $67,245

Start with the partial model in the file Ch12 P10 Build a Model.xls on the textbook’s Web site, which contains the

2013 financial statements of Zieber Corporation. Forecast Zeiber’s 2014 income statement and balance sheets. Use

the following assumptions: (1) Sales grow by 6%. (2) The ratios of expenses to sales, depreciation to fixed assets,

cash to sales, accounts receivable to sales, and inventories to sales will be the same in 2014 as in 2013. (3) Zeiber

will not issue any new stock or new long-term bonds. (4) The interest rate is 11% for long-term debt and the interest

expense on long-term debt is based on the average balance during the year . (5) No interest is earned on cash. (6)

Dividends grow at an 8% rate. (6) Calculate the additional funds needed (AFN). If new financing is required, assume

it will be raised by drawing on a line of credit with an interest rate of 12%. Assume that any draw on the line of credit

will be made on the last day of the year, so there will be no additional interest expense for the new line of credit. If

surplus funds are available, pay a special dividend.

a. What are the forecasted levels of notes payable and special dividends?

December 31 Income Statements:

(in thousands of dollars)

Expenses (excluding depr. & amort.) $386,878 % of sales 85.000% 85.00% $410,090

Depreciation and Amortization $14,565 % of fixed assets 8.000% 8.00% $15,439

EBIT $53,708 $56,930

Interest expense on long-term debt $11,880 Interest rate x average debt during year $13,200

Interest expense on line of credit $0 $0

EBT $41,828 $43,730

Taxes (40%) $16,731 $17,492

Net Income $25,097 $26,238

Common dividends (regular dividends) $12,554 Growth 8.00% $13,558

Special dividends $0 $0

Addition to retained earnings (DRE) $12,543 $12,680

Long-term debt $120,000 Previous $120,000 $120,000

Total liabilities $179,170 $182,720 $187,245

Common stock $60,000 Previous $60,000 $60,000

Retained Earnings $106,745 Previous + DRE $119,424 $119,424

Total common equity $166,745 $179,424 $179,424

Total liabilities and equity $345,914 $362,144 $366,669

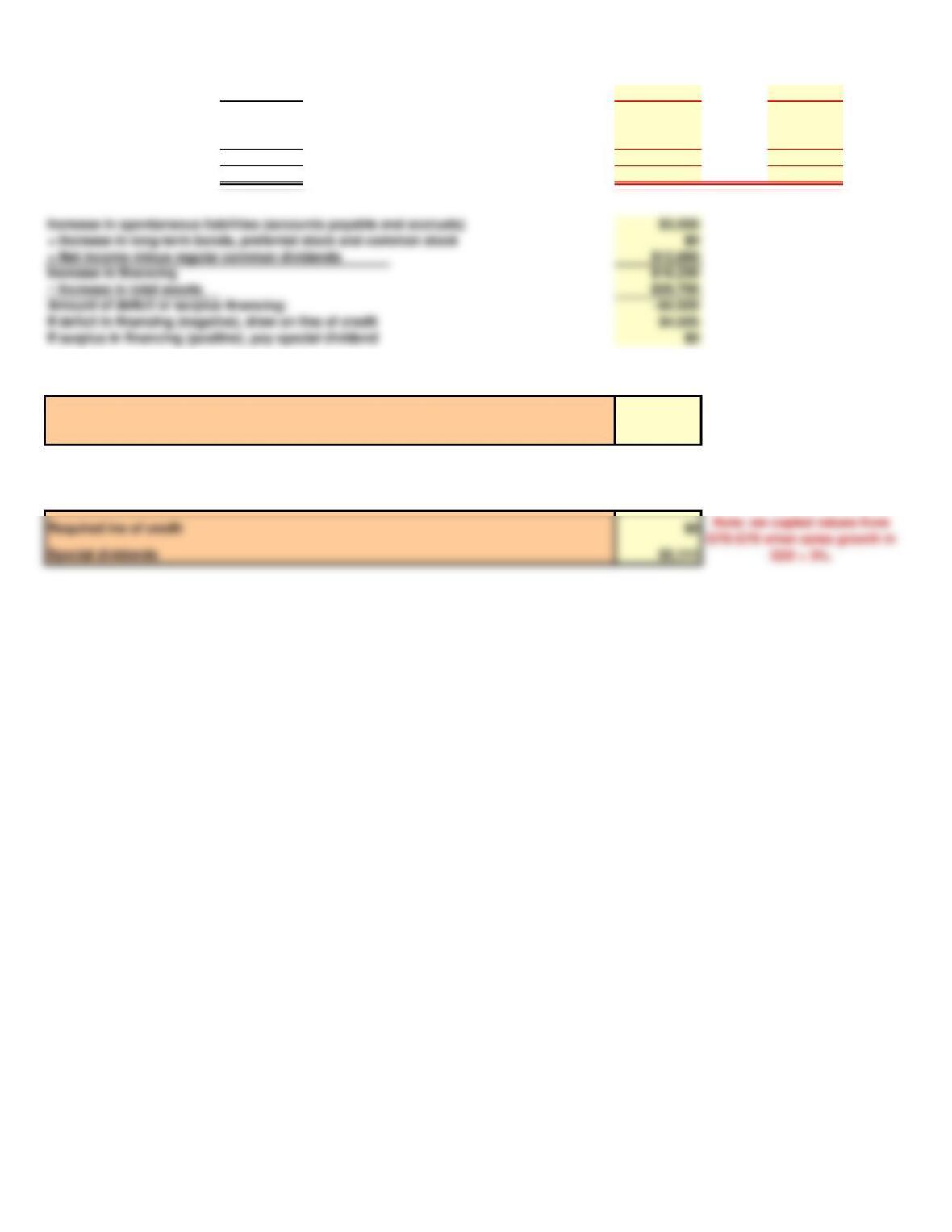

Note: we copied values from

G78:G79 when sales growth in

G32 = 3%.

Required ine of credit $4,525

Special dividends $0

a. What are the forecasted levels of the line of credit and special dividends?

b. Now assume that the growth in sales is only 3%. What are the forecasted levels of line of credit and special

dividends?

Note: we copied values from

G78:G79 when sales growth in

G32 = 6%.

Increase in spontaneous liabilities (accounts payable and accruals) $3,550

+ Increase in long-term bonds, preferred stock and common stock $0

+ Net income minus regular common dividends $12,680

Increase in financing $16,230

Amount of deficit or surplus financing: -$4,525

If deficit in financing (negative), draw on line of credit $4,525

If surplus in financing (positive), pay special dividend $0