b. 1. Find the price today.

2. Find the expected dividend yield.

3. Find the expected capital gains yield.

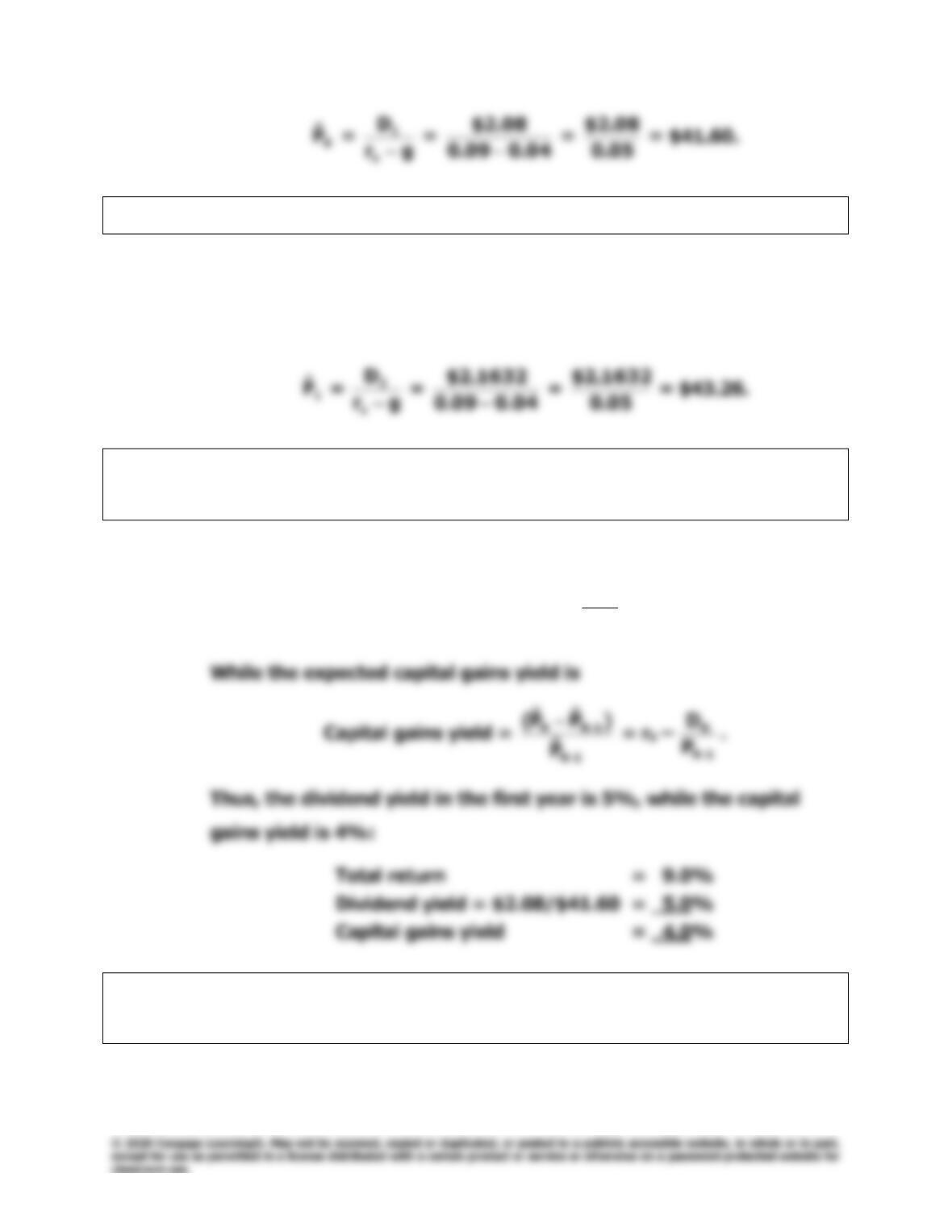

Cap. gain yield =Expected total return −

Dividend yield

c. We used the 5-year supernormal growth scenario for this calculation, but ultimately it does not

P 2+D 2

Cap. gain yield =

(P1 – P0) / P0

(1 + rs)

P 1

=

Dividend yield =

D1/ 0

D0$1.60

rs10.0%

PV of dividends

$1.7455

$1.9041

$2.2661

Dividend yield =

DN+1 / PN

Dividend yield = $4.2202 / $105.5048

Upon reflection, we see that these calculations were unnecessary because the constant growth

d.

Year

0 1 2 3 4 5 6 7 8 9 10 11

Value of Company‘s Operations $2,829.44

Market value of non-operating assets $0.00

Value of Total Corporation $2,829.44

Less: MV of Debt and Preferred $1,200.00

9%

INPUT DATA

WACC 9%

gn6%

244

Integrated Case

Chapter 9: Stocks and Their Valuation

9-23

Mutual of Chicago Insurance Company

Stock Valuation

Robert Balik and Carol Kiefer are senior vice presidents of the Mutual of

Chicago Insurance Company. They are codirectors of the company’s pension

fund management division, with Balik having responsibility for fixed-income

securities (primarily bonds) and Kiefer being responsible for equity

A. Describe briefly the legal rights and privileges of common

stockholders.

Answer: [Show S9-1 through S9-4 here.] The common stockholders are the

owners of a corporation, and as such they have certain rights and

privileges as described below.

1. Ownership implies control. Thus, a firm’s common stockholders

Chapter 9: Stocks and Their Valuation

Integrated Case

245

B. (1) Write a formula that can be used to value any stock, regardless of

its dividend pattern.

Answer: [Show S9-5 and S9-6 here.] The value of any stock is the present

value of its expected dividend stream:

B. (2) What is a constant growth stock? How are constant growth stocks

valued?

Answer: [Show S9-7 and S9-8 here.] A constant growth stock is one whose

dividends are expected to grow at a constant rate forever.

“Constant growth” means that the best estimate of the future

246

Integrated Case

Chapter 9: Stocks and Their Valuation

B. (3) What are the implications if a company forecasts a constant g that

exceeds its rs? Will many stocks have expected g > rs in the short

run (i.e., for the next few years)? In the long run (i.e., forever)?

Answer: [Show S9-9 here.] The model is derived mathematically, and the

derivation requires that rs > g. If g is greater than rs, the model gives

C. Assume that Bon Temps has a beta coefficient of 1.2, that the risk–

free rate (the yield on T-bonds) is 3%, and that the required rate of

return on the market is 8%. What is Bon Temps’s required rate of

return?

Answer: [Show S9-10 here.] Here we use the SML to calculate Bon Temps’s

required rate of return:

rs = rRF + (rM – rRF)bBon Temps

D. Assume that Bon Temps is a constant growth company whose last

dividend (D0, which was paid yesterday) was $2.00 and whose

dividend is expected to grow indefinitely at a 4% rate.

(1) What is the firm’s expected dividend stream over the next 3 years?

Answer: [Show S9-11 here.] Bon Temps is a constant growth stock, and its

dividend is expected to grow at a constant rate of 4% per year.

D. (2) What is its current stock price?

Answer: [Show S9-12 here.] We could extend the time line on out forever,

find the value of Bon Temps’s dividends for every year on out into

the future, and then the PV of each dividend discounted at rs = 9%.

248

Integrated Case

Chapter 9: Stocks and Their Valuation

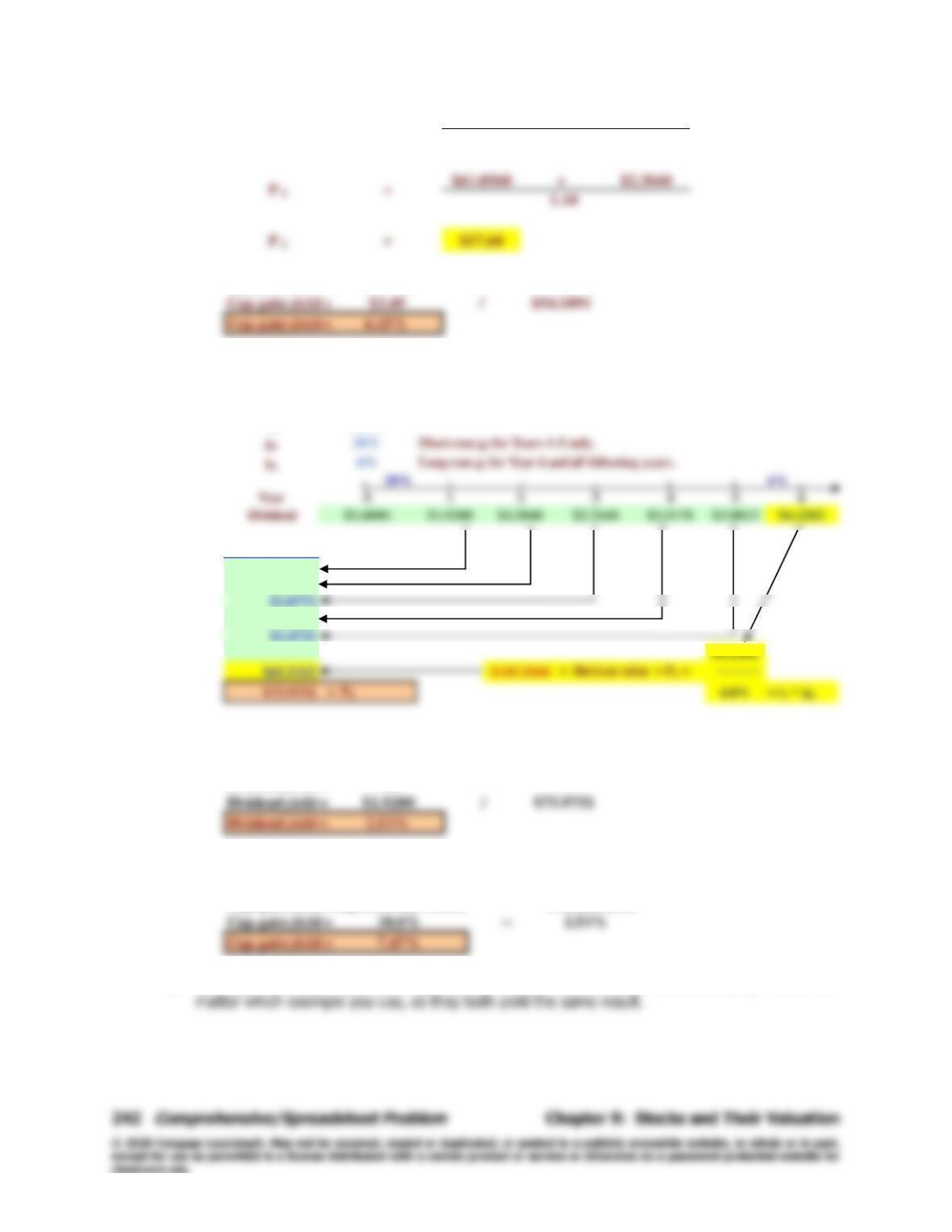

D. (3) What is the stock’s expected value 1 year from now?

Answer: [Show S9-13 here.] After one year, D1 will have been paid, so the

expected dividend stream will then be D2, D3, D4, and so on. Thus,

the expected value one year from now is $43.26:

D. (4) What are the expected dividend yield, capital gains yield, and total

return during the first year?

Answer: [Show S9-14 here.] The expected dividend yield in any Year N is

Dividend yield =

1N

N

P

ˆ

D

−

,

E. Now assume that the stock is currently selling at $40.00. What is

its expected rate of return?

Chapter 9: Stocks and Their Valuation

Integrated Case

249

Answer: The constant growth model can be rearranged to this form:

s

r

ˆ

=

g

P

D

0

1+

.

s

r

ˆ

F. What would the stock price be if its dividends were expected to have

zero growth?

Answer: [Show S9-15 here.] If Bon Temps’s dividends were not expected to

grow at all, then its dividend stream would be a perpetuity.

Perpetuities are valued as shown below:

250

Integrated Case

Chapter 9: Stocks and Their Valuation

G. Now assume that Bon Temps’s dividend is expected to grow 30%

the first year, 20% the second year, 10% the third year, and return

to its long-run constant growth rate of 4%. What is the stock’s

value under these conditions? What are its expected dividend and

capital gains yields in Year 1? Year 4?

Answer: [Show S9-16 through S9-18 here.] Bon Temps is no longer a

constant growth stock, so the constant growth model is not

applicable. Note, however, that the stock is expected to become a

Simply enter $2 and multiply by (1.30) to get D1 = $2.60; multiply

that result by 1.2 to get D2 = $3.12, and multiply that result by 1.1

to get D3 = 3.432. Then recognize that after Year 3, Bon Temps

Chapter 9: Stocks and Their Valuation

Integrated Case

251

With the cash flows for D1, D2, D3, and

3

P

ˆ

shown on the time

line, we discount each value back to Year 0, and the sum of these

four PVs is the value of the stock today, P0 = $62.784.

H. Suppose Bon Temps is expected to experience zero growth during

the first 3 years and then resume its steady-state growth of 4% in

the fourth year. What would be its value then? What would be its

expected dividend and capital gains yields in Year 1? In Year 4?

Answer: [Show S9-19 and S9-20 here.] Now we have this situation:

0 1 2 3 4

| | | | |

2.00 2.00 2.00 2.08

1.68

rs = 9%

g = 0%

g = 0%

g = 0%

gn = 4%

05.0

08.2

252

Integrated Case

Chapter 9: Stocks and Their Valuation

During Year 1:

Dividend yield =

19.37$

00.2$

= 0.0538= 5.38%.

I. Finally, assume that Bon Temps’s earnings and dividends are

expected to decline at a constant rate of 4% per year, that is,

g = -4%. Why would anyone be willing to buy such a stock, and at

what price should it sell? What would be its dividend and capital

gains yields in each year?

Answer: [Show S9-21 and S9-22 here.] The company is earning something

and paying some dividends, so it clearly has a value greater than

zero. That value can be found with the constant growth formula,

but where g is negative:

Since it is a constant growth stock:

g = Capital gains yield = –4.0%,

Hence:

Chapter 9: Stocks and Their Valuation

Integrated Case

253

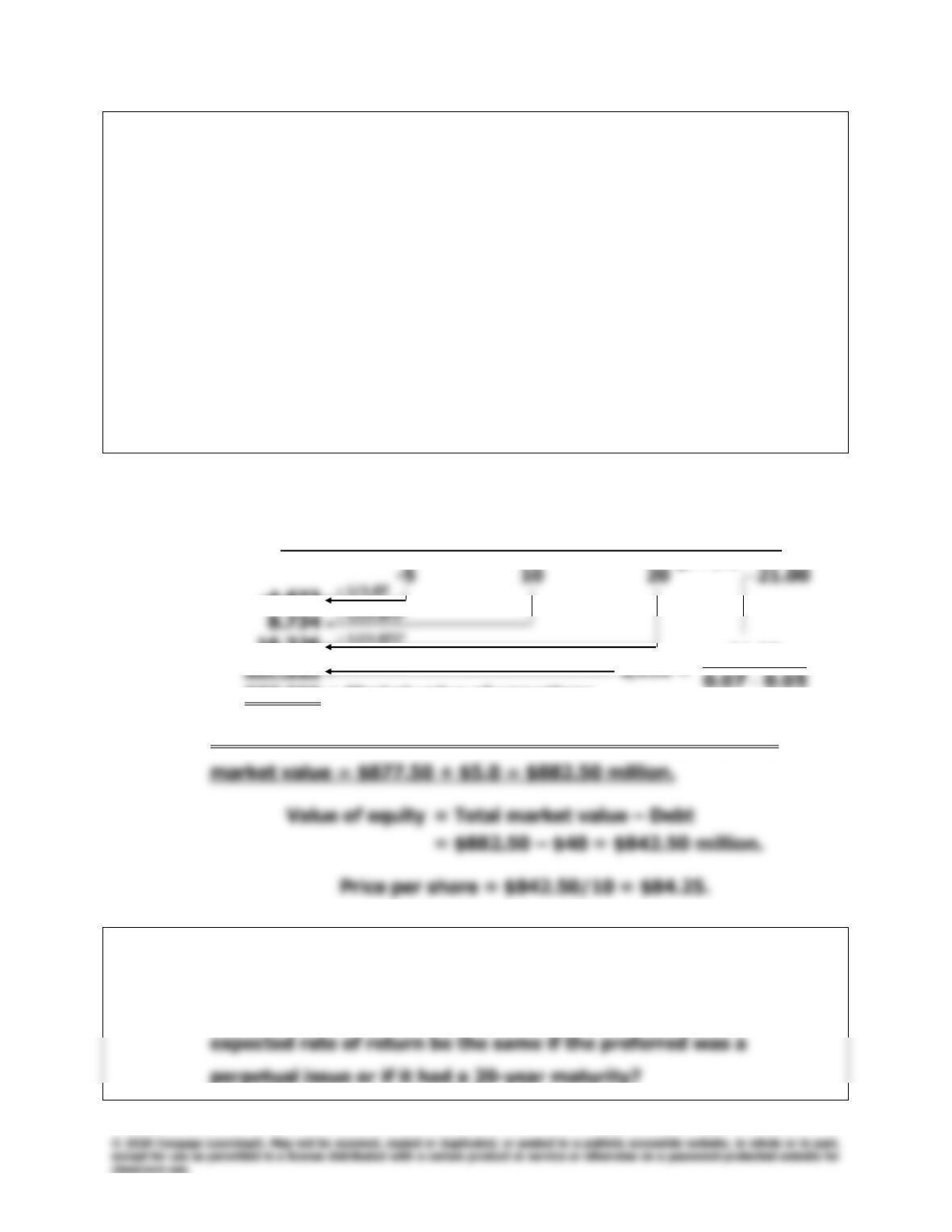

J. Suppose Bon Temps embarked on an aggressive expansion that

requires additional capital. Management decided to finance the

expansion by borrowing $40 million and by halting dividend

payments to increase retained earnings. Its WACC is now 7%, and

the projected free cash flows for the next 3 years are –$5 million,

$10 million, and $20 million. After Year 3, free cash flow is

projected to grow at a constant 5%. What is Bon Temps’s market

value of operations? If it has 10 million shares of stock, $40 million

of debt and preferred stock combined, and $5 million of non–

operating assets, what is the price per share?

Answer: [Show S9-23 through S9-28 here.]

0 1 2 3 4

| | | | |

–4.673

1/(1.07)2

16.326

877.500 = Market value of operations

Since the firm has $5 million of non-operating assets, its total

K. Suppose Bon Temps decided to issue preferred stock that would pay

an annual dividend of $5.00 and that the issue price was $100.00

per share. What would be the stock’s expected return? Would the

WACC = 7%

gn = 5%

00.21

1/(1.07)3

254

Integrated Case

Chapter 9: Stocks and Their Valuation

Answer: [Show S9-29 through S9-31 here.]

p

r

ˆ

=

p

p

V

D

Appendix 9A: Stock Market Equilibrium

Answers and Solutions

255

Appendix 9A

Stock Market Equilibrium

Answers to End-of-Chapter Questions

9A-1 For a stock to be in equilibrium, two related conditions must hold:

1. A stock’s expected rate of return as seen by the marginal investor must equal its required

00 P

9A-2 Some individual investors may believe that

ii rr

ˆ

and

00 PP

ˆ

(hence they would invest most of

their funds in the stock), while other investors might have an opposite view and sell all their shares.

00 PP

ˆ=

256

Answers and Solutions

Appendix 9A: Stock Market Equilibrium

Solutions to End-of-Chapter Problems

9A-1 a. ri = rRF + (rM – rRF)bi.

b. In this situation, the expected rate of return is as follows:

C

r

ˆ

= D1/P0 + g = $1.50/$25 + 4% = 10%.

9A-2 a. rs = rRF + (rM – rRF)b = 6% + (10% – 6%)1.5 = 12.0%.

0

P

ˆ

= D1/(rs – g) = $2.25/(0.12 – 0.05) = $32.14.

b. rs = 5% + (9% – 5%)1.5 = 11.0%.

0

P

ˆ

= $2.25/(0.11 – 0.05) = $37.50.

0

P

ˆ

Appendix 9A: Stock Market Equilibrium

Answers and Solutions

257

9A-3 a. Old rs = rRF + (rM – rRF)b = 6% + (3%)1.2 = 9.6%.

New rs = 6% + (3%)0.9 = 8.7%.

b. POld = $58.89. PNew =

04.0r

)04.1(2$

s−

.

Solving for rs we have the following:

$58.89 =

04.0r

08.2$