Chapter 6: Interest Rates

Learning Objectives

125

Chapter 6

Interest Rates

Learning Objectives

After reading this chapter, students should be able to do the following:

◆ List the various factors that influence the cost of money.

◆ Discuss how market interest rates are affected by borrowers’ need for capital, expected inflation,

different securities’ risks, and securities’ liquidity.

126

Lecture Suggestions

Chapter 6: Interest Rates

Lecture Suggestions

Chapter 6 is important because it lays the groundwork for the following chapters. Additionally, students

have a curiosity about interest rates, so this chapter stimulates their interest in the course.

DAYS ON CHAPTER: 2 OF 56 DAYS (50-minute periods)

Chapter 6: Interest Rates

Answers and Solutions

127

Answers to End-of-Chapter Questions

6-1 Regional mortgage rate differentials do exist, depending on supply/demand conditions in the

different regions. However, relatively high rates in one region would attract capital from other

regions, and the result would be a differential that was just sufficient to cover the costs of effecting

6-2 Short-term interest rates are more volatile because (1) the Fed operates mainly in the short-term

6-3 Interest rates will fall as the recession takes hold because (1) business borrowings will decrease

and (2) the Fed will increase the money supply to stimulate the economy. Thus, it would be better

6-4 a. If transfers between the two markets are costly, interest rates would be different in the two

areas. Area Y, with the relatively young population, would have less in savings accumulation

and stronger loan demand. Area O, with the relatively old population, would have more

equilibrium would be at a higher rate of interest in Area Y.

b. Yes. Nationwide branching, and so forth, would reduce the cost of financial transfers between

the areas. Thus, funds would flow from Area O with excess relative supply to Area Y with

6-5 A significant increase in productivity would raise the rate of return on producers’ investment, thus

6-6 a. The immediate effect on the yield curve would be to lower interest rates in the short-term end

of the market, since the Fed deals primarily in that market segment. However, people would

6-7 a. S&Ls would have a higher level of net income with a “normal” yield curve. In this situation their

liabilities (deposits), which are short-term, would have a lower cost than the returns being

b. It depends on the situation. A sharp increase in inflation would increase interest rates along

the entire yield curve. If the increase were large, short-term interest rates might be boosted

above the long-term interest rates that prevailed prior to the inflation increase. Then, since the

6-8 Treasury bonds, along with all other bonds, are available to investors as an alternative investment

to common stocks. An increase in the return on Treasury bonds would increase the appeal of these

6-9 A trade deficit occurs when the U.S. buys more than it sells. In other words, a trade deficit occurs

6-10 The yield on corporates is equal to:

rt = r* + IPt + MRPt + DRP + LP.

Chapter 6: Interest Rates

Answers and Solutions

129

Solutions to End-of–Chapter Problems

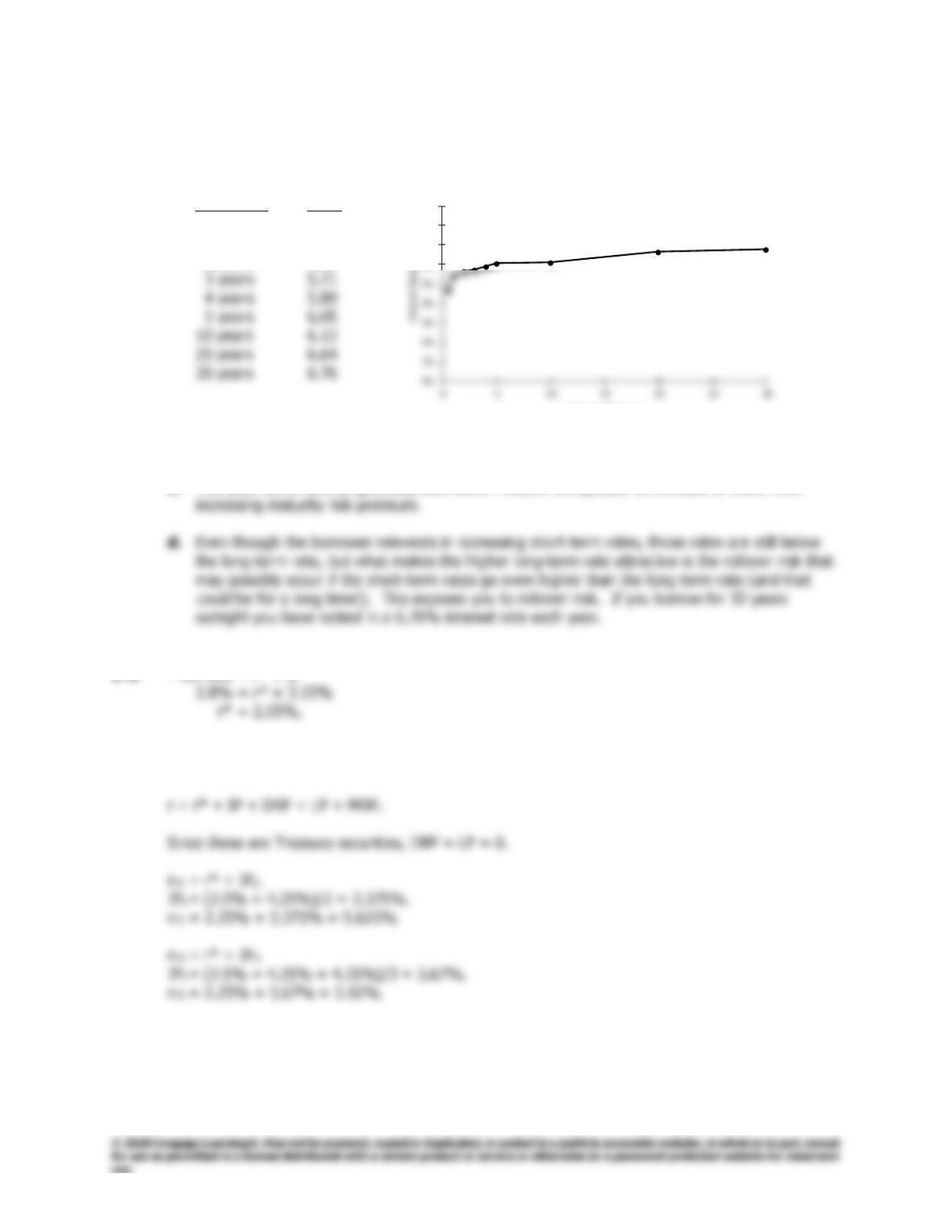

6-1 a. Term Rate

6 months 4.69%

1 year 5.49

2 years 5.66

b. The yield curve shown is an upward sloping yield curve.

c. This yield curve tells us generally that either inflation is expected to increase or there is an

6-2 T-bill rate = r* + IP

6-3 r* = 2.25%; I1 = 2.5%; I2 = 4.25%; I3 = 4.25%; MRP = 0; rT2 = ?; rT3 = ?

6%

7%

8%

9%

Years to Maturity

6-4 rT10 = 5.75%; rC10 = 8.75%; LP = 0.35%; DRP = ?

r = r* + IP + DRP + LP + MRP.

rT10 = 5.75% = r* + IP10 + MRP10; DRP = LP = 0.

6-5 r* = 2.5%; IP2 = 2.75%; rT2 = 5.55%; MRP2 = ?

6-6 r* = 5%; IP4 = 18%; MRP = DRP = LP = 0; rRF4 = ?

6-7 rT1 = 4.85%; 1rT1 = 5.2%; rT2 = ?

6-8 Let X equal the yield on 2-year securities 4 years from now:

(1.067)4(1 + X)2 = (1.0725)6

6-9 r7 = r* + IP7 + MRP7 + DRP + LP.

6-10 Basic relevant equations:

rt = r* + IPt + DRPt + MRPt + IPt.

But here IPt is the only premium, so rt = r* + IPt.

We can set up this table:

r* I IPt r = r* + IPt

1 2.5% 3.25% 3.25%/1 = 3.25% 5.75%

2 2.5% I (3.25% + I)/2 = IP2

6-11 We’re given all the components to determine the yield on the bonds except the default risk

premium (DRP) and MRP. Calculate the MRP as 0.1 x (5 – 1)% = 0.4%. Now, we can solve for

6-12 First, calculate the inflation premiums for the next three and five years, respectively. They are IP3

= (2.1% + 2.7% + 3.65%)/3 = 2.82% and IP5 = (2.1% + 2.7% + 3.65% + 3.65% + 3.65%)/5 =

3.15%. The real risk-free rate is given as 1.95%. Since the default and liquidity premiums are

6-13 rC11 = r* + IP11 + MRP11 + DRP11 + LP11

132

Answers and Solutions

Chapter 6: Interest Rates

6-14 a. (1.041)2 = (1.032)(1 + X)

b. For riskless bonds under the expectations theory, the interest rate for a bond of any maturity is

rN = r* + average inflation over N years. If r* = 1%, we can solve for IPN:

Year 1: r1 = 1% + I1 = 3.2%;

6-15 r* = 2%; MRP = 0%; rT1 = 5%; rT2 = 7%; X = ?

X represents the one-year rate on a bond one year from now (Year 2).

(1.07)2 = (1.05)(1 + X)

1449.1

= 1 + X

6-16 rRF6 = 20.84%; MRP = DRP = LP = 0; r* = 6%; IP6 = ?

rRF6 = (1 + r*)(1 +IP6) – 1

6-17 rT5 = 5.2%; rT10 = 6.4%; rC10 = 8.4%; IP10 = 2.5%; MRP = 0. For Treasury securities, DRP = LP = 0.

DRP5 + LP5 = DRP10 + LP10. rC5 = ?

Chapter 6: Interest Rates

Answers and Solutions

133

rT5 = r* + IP5

rC10 = r* + IP10 + DRP10 + LP10

8.4% = 3.9% + 2.5% + DRP10 + LP10

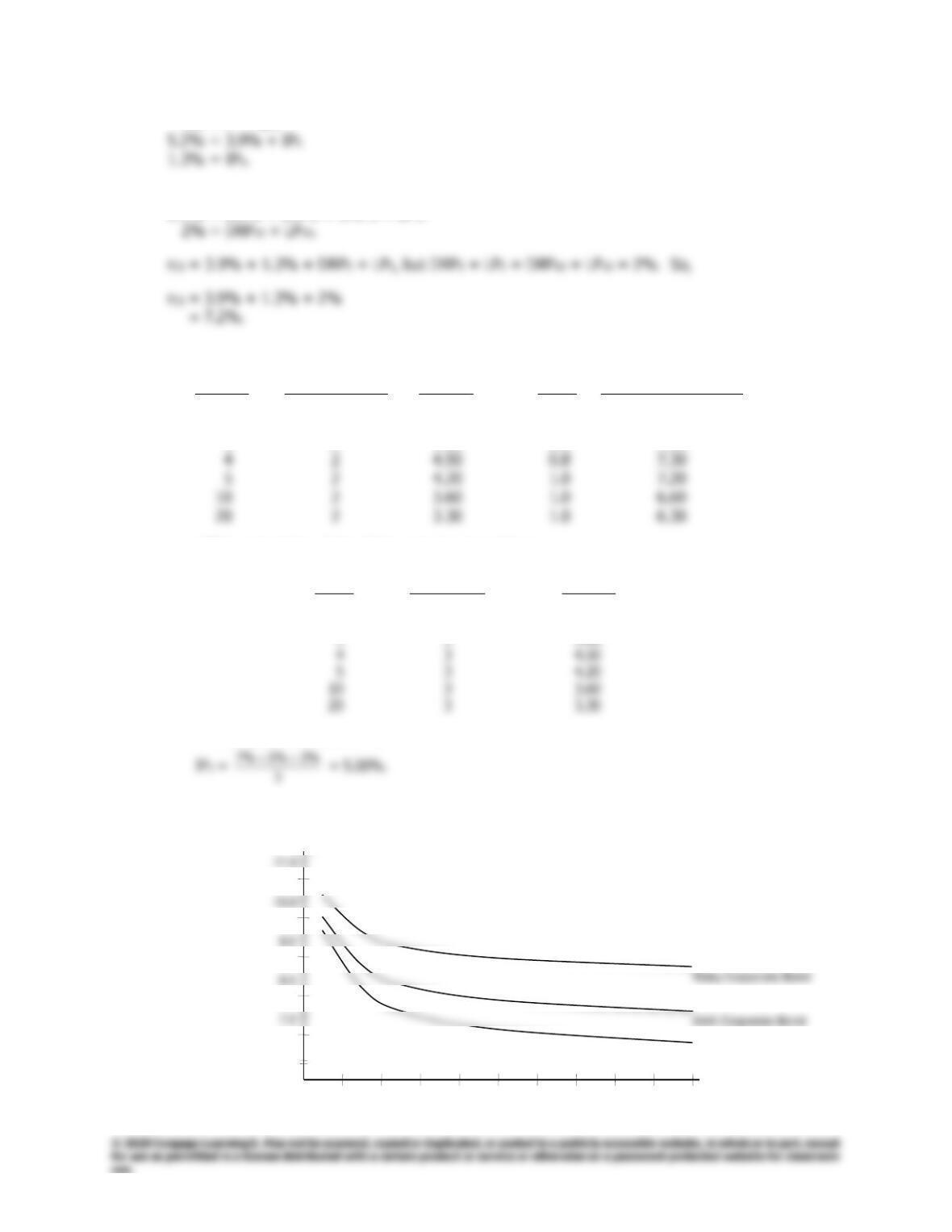

6-18 a. Years to Real Risk-Free

Maturity Rate (r*) IPt** MRP rT = r* + IPt + MRPt

1 2% 7.00% 0.2% 9.20%

2 2 6.00 0.4 8.40

3 2 5.00 0.6 7.60

**The computation of the inflation premium is as follows:

Expected

Year Inflation IPt

1 7% 7.00%

2 5 6.00

3 3 5.00

For example, the calculation for IP3 is as follows:

Thus, the yield curve would be as follows:

8.0

7.0

T-bonds

11.0

10.5

10.0

9.5

9.0

8.5

7.5

0

2

4

6

8

10

12

14

16

18

20

Interest Rate

(%)

6.5

Years to

Maturity

134

Answers and Solutions

Chapter 6: Interest Rates

b. The interest rate on the AAA–rated corporate bonds has the same components as the Treasury

securities, except that the AAA–rated corporate bonds have default risk, so a default risk premium

must be included. Therefore,

c. The lower-rated corporate bonds would have significantly more default risk than either

6-19 a. The average rate of inflation for the 5-year period is calculated as:

b. rT5 = r* + IP5 = 2% + 8.2% = 10.20%.

c. Here is the general situation:

Year

Expected Annual

Inflation (It)

IPt

r*

MRPt

rt

1

13%

13.0%

2%

0.1%

15.1%

2

9

11.0

2

0.2

13.2

5

6

2

0.5

10.7

6

2

2.0

10.6

(%)

Interest Rate

15.0

10.0

5.0

2.5

Chapter 6: Interest Rates

Answers and Solutions

135

d. The “normal” yield curve is upward sloping because, in “normal” times, inflation is not expected to

trend either up or down, so IP is the same for debt of all maturities, but the MRP increases with

e. If inflation rates are expected to be constant, then the expectations theory holds that the yield

curve should be horizontal. However, in this event it is likely that maturity risk premiums would be

applied to long-term bonds because of the greater risks of holding long–term rather than short–term

bonds:

Maturity

premium

Pure expectations yield curve

Years to Maturity

risk

If maturity risk premiums were added to the yield curve in Part e above, then the yield curve

would be more nearly normal; that is, the long-term end of the yield curve would be raised.

(%)

Percent

Actual yield curve

136

Comprehensive/Spreadsheet Problem

Chapter 6: Interest Rates

Comprehensive/Spreadsheet Problem

Note to Instructors:

The solution to this problem is not provided to students at the back of their text. Instructors

can access the

Excel

file on the textbook’s website.

2. This action will cause interest rates to increase.

4. This expectation will cause interest rates to increase.

b.

12–year Treasury Bond

Real risk–free rate (r*): 4.000%

Maturity: 12

Expected inflation: for the next 2years = 2%

Expected inflation: for the next 4years = 3%

7–year Corporate Bond

Rating : A

Real risk–free rate (r*): 4.000%

Maturity: 7

Expected inflation: for the next 2years = 2%

Expected inflation: for the next 4years = 3%

Chapter 6: Interest Rates

Comprehensive/Spreadsheet Problem

137

c.

d. The real risk-free rate would be the same for the corporate and treasury bonds. Similarly,

without information to the contrary, we would assume that the maturity and inflation premiums

would be the same for bonds with the same maturities. However, the corporate bond would

have a liquidity premium and a default premium. If we assume that these premiums are

constant across maturities, then we can use the LP and DRP as determined above and add

them to the T-bond yields to find the corporate yields. This procedure was used in the table

below.

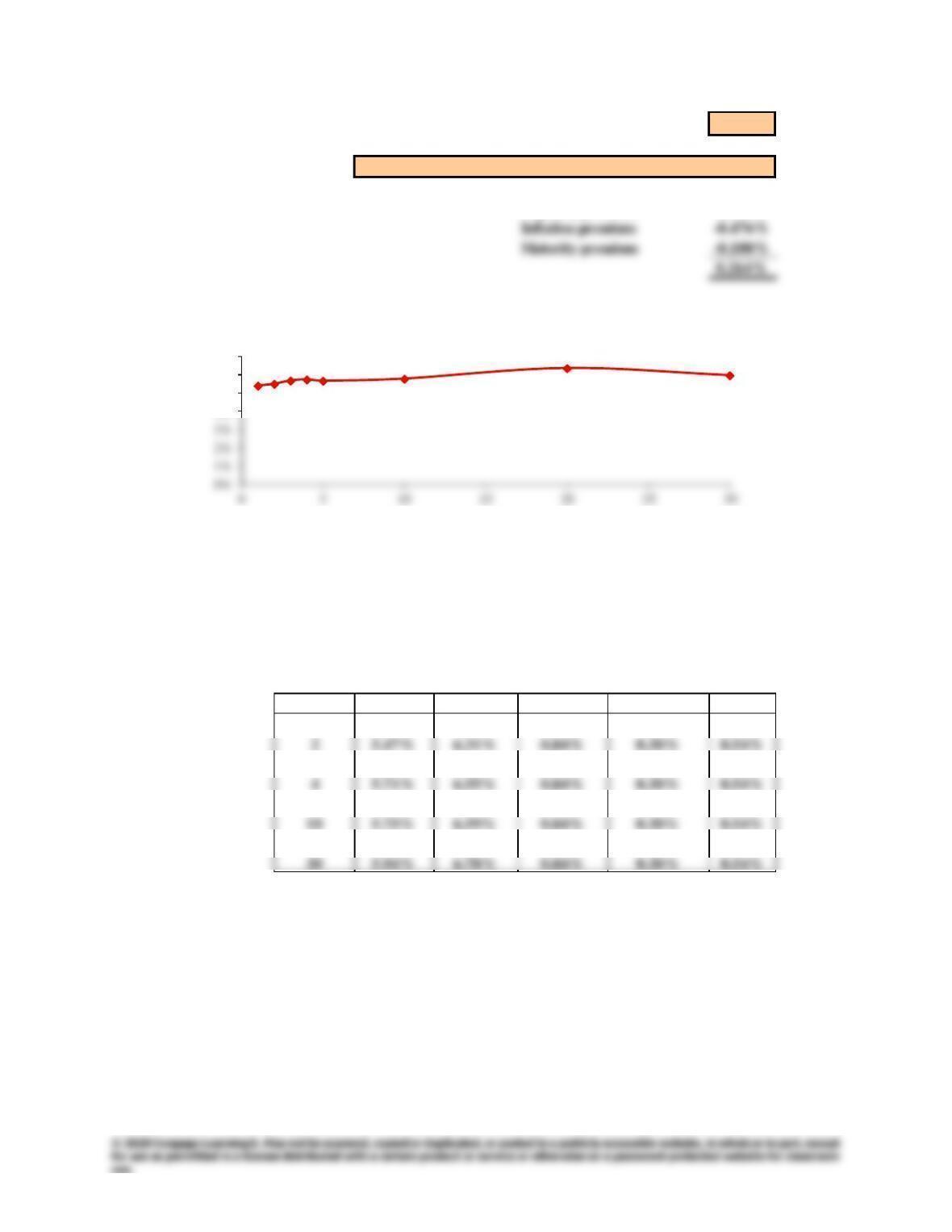

Years Treasury A–Corporate Spread LP DRP

1 5.37% 6.21% 0.84% 0.30% 0.54%

3 5.65% 6.49% 0.84% 0.30% 0.54%

5 5.64% 6.48% 0.84% 0.30% 0.54%

20 6.33% 7.17% 0.84% 0.30% 0.54%

7–year Corporate yield = r* + IP7 + MRP7 + LP + DRP = 7.817%

Yield Spread = Corporate – Treasury = 0.264%

Reconciliation: Default premium 0.540%

Liquidity premium 0.300%

4%

5%

6%

7%

Interest Rate

Years to Maturity

Yield Curve