Chapter 12: Cash Flow Estimation and Risk Analysis

Comprehensive/Spreadsheet Problem

341

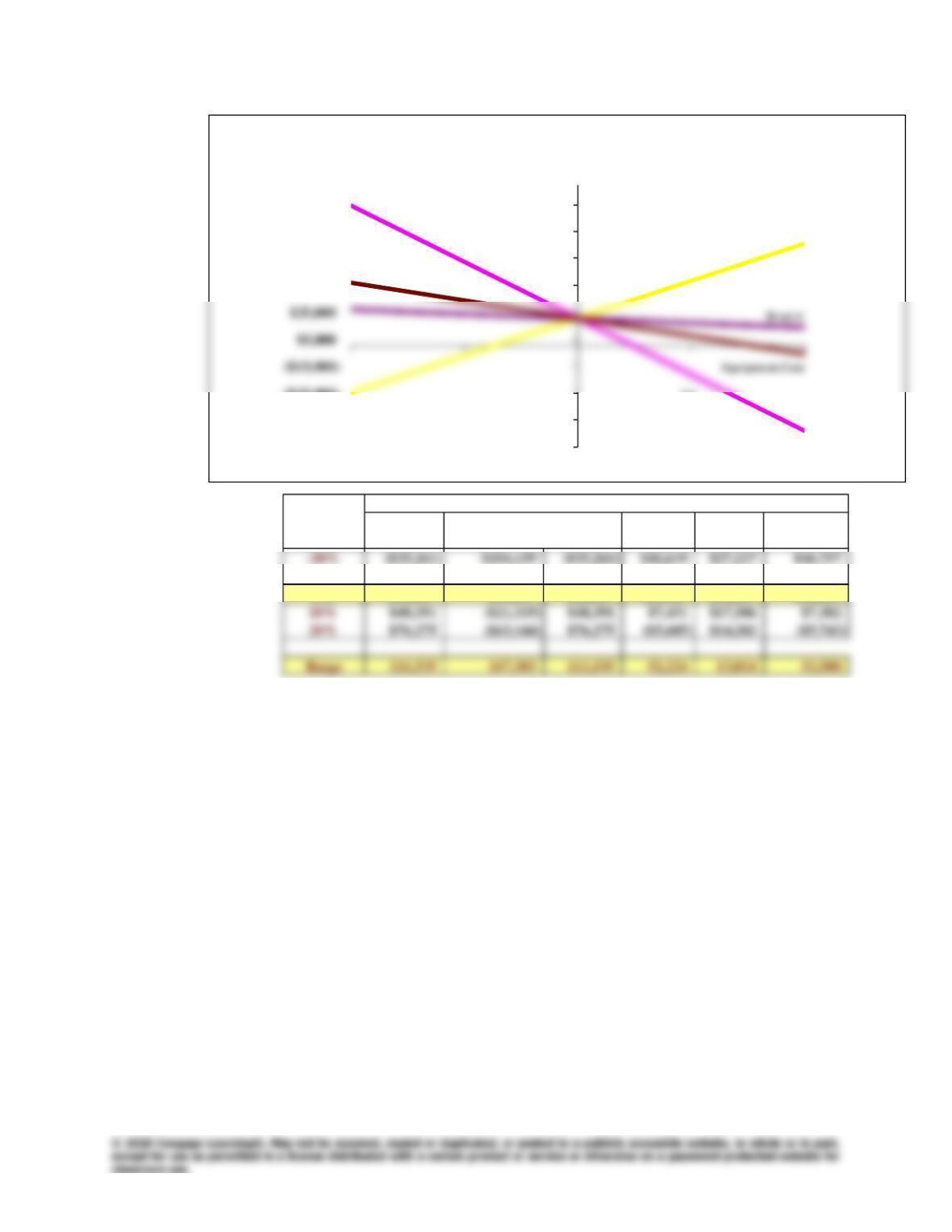

Deviation

from Sales Variable Unit Fixed Equipment

Base Case Price Costs Sales Costs WACC Cost

-10% ($7,377) $62,333 ($7,377) $33,563 $23,809 $33,632

0% $20,507 $20,507 $20,507 $20,507 $20,507 $20,507

NPV at Different Deviations from Base

($75,000)

($55,000)

($35,000)

$45,000

$65,000

$85,000

$105,000

-20% -10% 0% 10% 20%

NPV Sensitivity Analysis

VC

Sales Price

g. Note that “best-case” values for variable costs, fixed costs, WACC, and equipment cost are

20% less than base-case values, while the “worst-case” values for variable costs, fixed costs,

WACC, and equipment cost are 20% higher than base-case values.

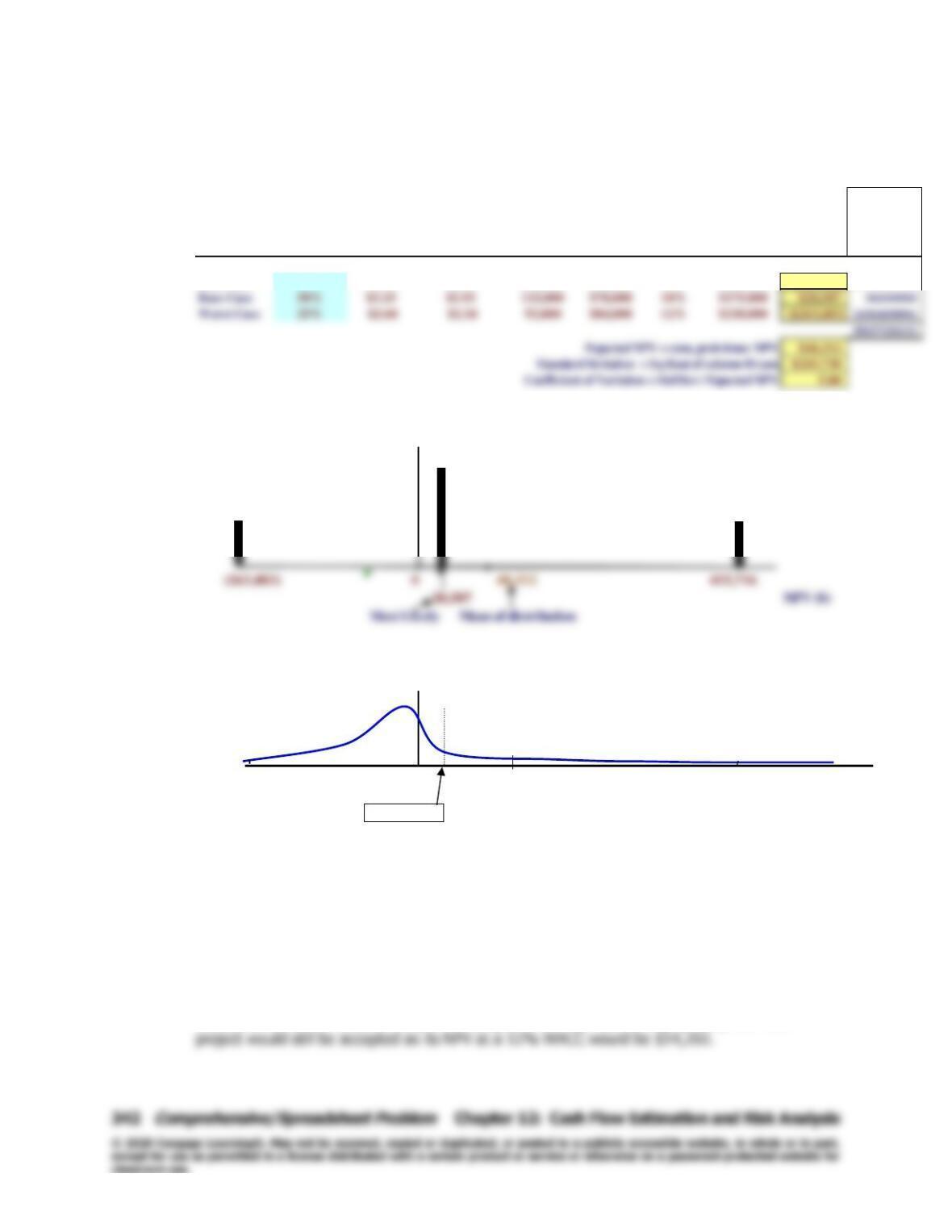

Squared

Deviation

Sales Variable Unit Fixed Equipment Times

Scenario Probability Price Costs Sales Costs WACC Cost NPV Probability

Best Case 25% $3.90 $1.56 138,000 $56,000 8% $140,000 $415,716 33746517548

a. Probability Graph Probability

50%

25%

b. Continuous Approximation

Probability Density

(263,483) 0 48,312 415,716

NPV ($)

20,507

The scenario analysis suggests that the project could be highly profitable, but also that it is

quite risky. There is a 25% probability that the project would result in a loss of $263,483.

There is also a 25% probability that it could produce an NPV of $415,716. The standard

deviation is high, at $241,738, and the coefficient of variation is high, 5.00.

h. A risk-adjusted discount rate is the cost of capital appropriate for a given project, given the

riskiness of that project. The greater its risk, the higher the project’s cost of capital. If Cory

used a risk-adjusted discount rate, this project’s cost of capital would be increased above the

firm’s 10% WACC to reflect its greater risk as determined from the project’s CV of 5.00. If Cory

increased the WACC used to analyze this project’s NPV by 2 percentage points, then this

Chapter 12: Cash Flow Estimation and Risk Analysis

Integrated Case

343

Integrated Case

12–19

Allied Food Products

Capital Budgeting and Cash Flow Estimation

Allied Food Products is considering expanding into the fruit juice business with a

new fresh lemon juice product. Assume that you were recently hired as assistant

to the director of capital budgeting, and you must evaluate the new project.

The lemon juice would be produced in an unused building adjacent to

Allied’s Fort Myers plant; Allied owns the building, which is fully depreciated.

The project is expected to operate for 4 years, at which time it will be

terminated. The cash inflows are assumed to begin 1 year after the project is

(t = 4), the equipment is expected to have a salvage value of $25,000.

Unit sales are expected to total 100,000 units per year, and the expected

sales price is $2.00 per unit. Cash operating costs for the project are expected

344

Integrated Case

Chapter 12: Cash Flow Estimation and Risk Analysis

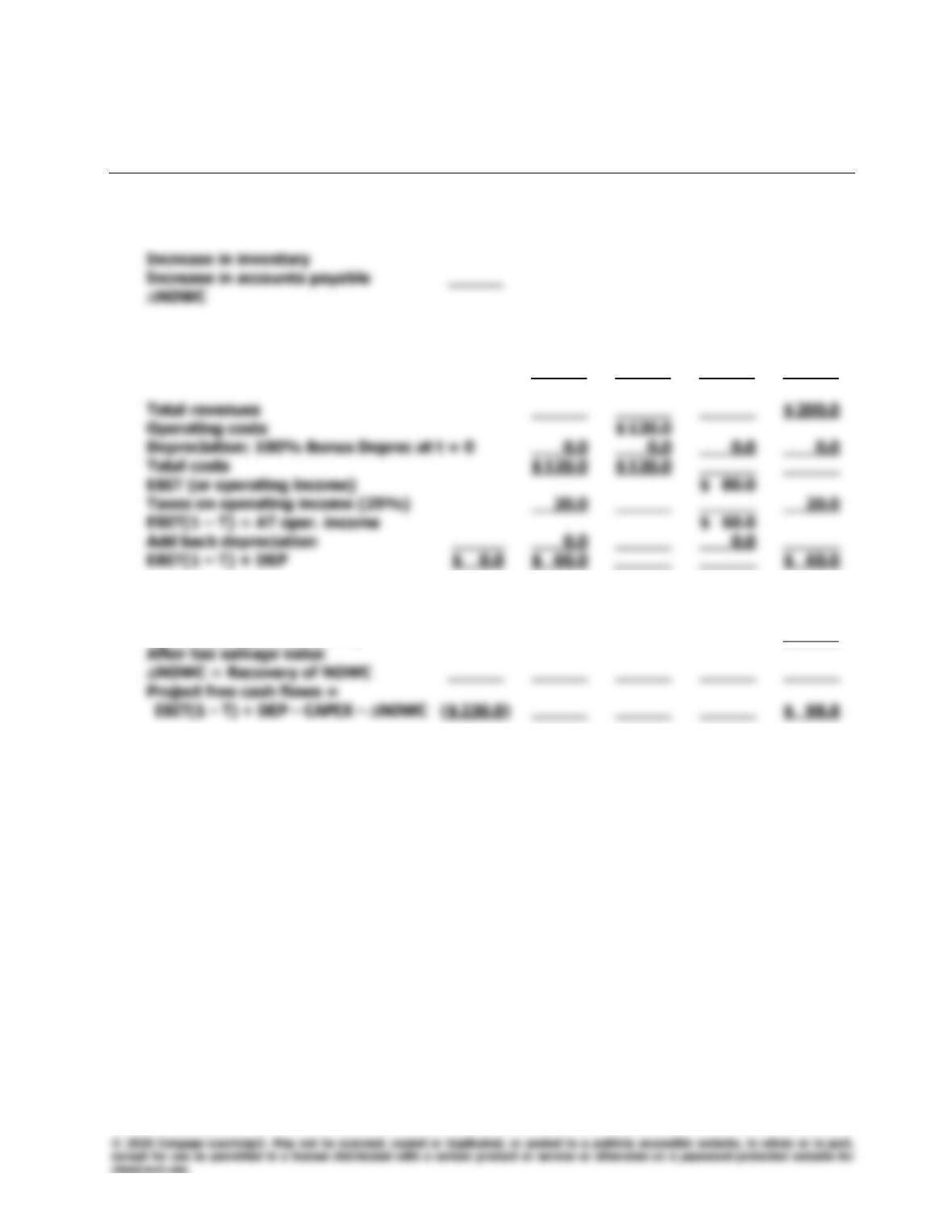

Table IC 12.1. Allied’s Lemon Juice Project (in Thousands)

End of Year: 0 1 2 3 4

I. Investment Outlays

CAPEX × (1 – T)

II. Project Operating Cash Flows

Unit sales (thousands) 100

Price/unit $ 2.00 $ 2.00

III. Project Termination Cash Flows

Salvage value (taxed as ord. income)

Tax on salvage value (25%)

IV. Results

NPV =

IRR =

MIRR =

Payback =

Chapter 12: Cash Flow Estimation and Risk Analysis

Integrated Case

345

A. Allied has a standard form that is used in the capital budgeting

process. (See Table IC 12.1.) Part of the table has been completed,

but you must replace the blanks with the missing numbers.

Complete the table using the following steps:

(1) Fill in the blanks under Year 0 for the initial investment outlays:

CAPEX × (1 – T) and NOWC.

Answer: [Show S12-1 through S12-6 here.] This answer is straightforward.

Note that accounts payable is an offset to the inventory buildup, so

A. (2) Complete the table for unit sales, sales price, total revenues, and

operating costs.

Answer: This answer requires no explanation. Students may note, though,

A. (3) Complete the table down to after-tax operating income and then

down to the project’s operating cash flows, EBIT(1 – T) + DEP.

Answer: [Show S12-7 here.] This is straightforward. Remember, that the

346

Integrated Case

Chapter 12: Cash Flow Estimation and Risk Analysis

A. (4) Fill in the blanks under Year 4 for the terminal cash flows and

complete the project free cash flow line. Discuss the recovery of net

operating working capital. What would have happened if the

machinery had been sold for less than its book value?

Answer: [Show S12-8 and S12-9 here.] These are all straightforward. Note

that the net operating working capital requirement is recovered at

Chapter 12: Cash Flow Estimation and Risk Analysis

Integrated Case

347

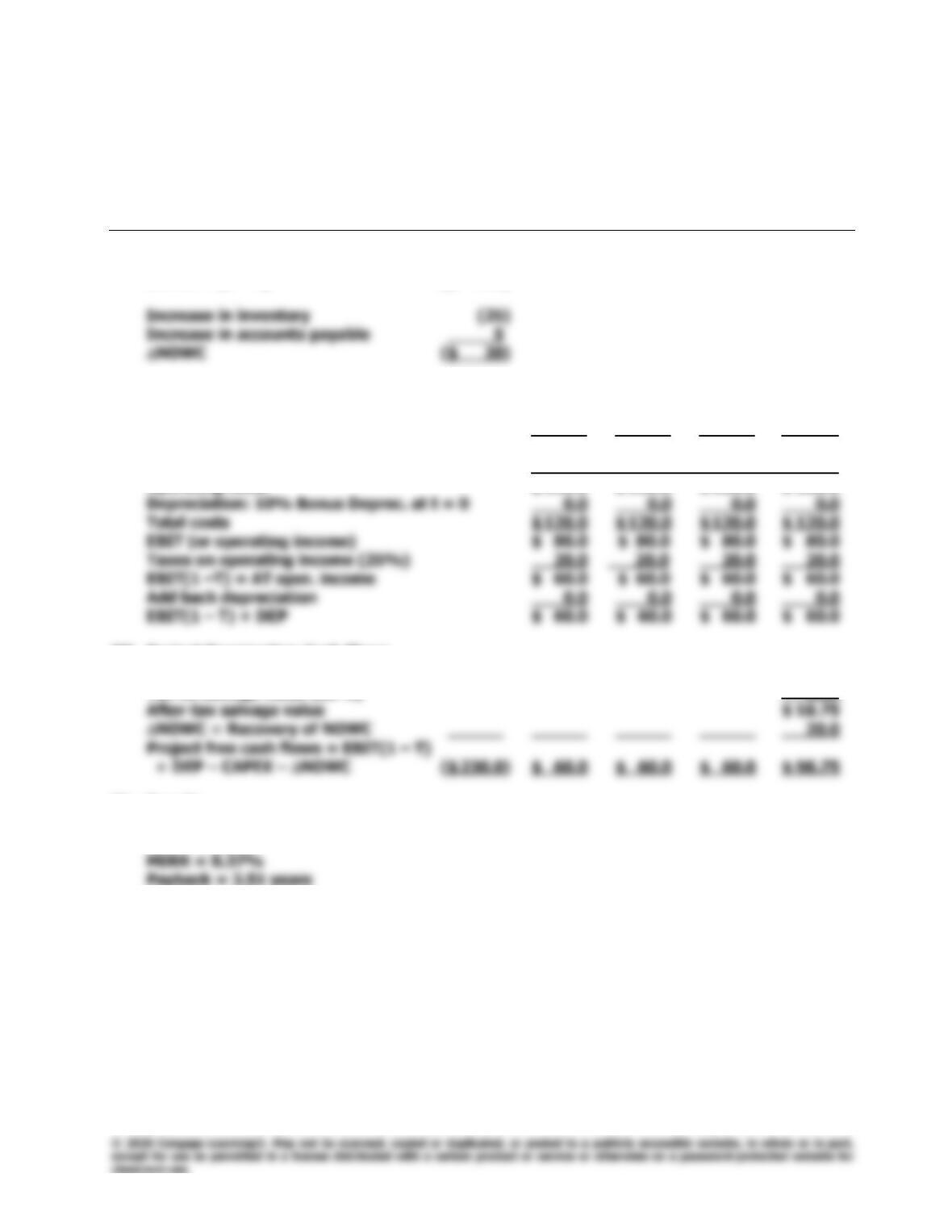

Table IC 12.1. Allied’s Lemon Juice Project (in Thousands)

Inputs: Price: $2.00 WACC: 10% Infl: 0.0%

VC rate: 60.0% T-rate: 25%

End of Year: 0 1 2 3 4

I. Investment Outlays

CAPEX × (1 – T) ($ 210)

II. Project Operating Cash Flows

Unit sales (thousands) 100 100 100 100

Price/unit $ 2.00 $ 2.00 $ 2.00 $ 2.00

Total revenues $ 200.0 $ 200.0 $ 200.0 $ 200.0

Operating costs $ 120.0 $ 120.0 $ 120.0 $ 120.0

III. Project Termination Cash Flows

Salvage value (taxed as ord. income) 25.0

Tax on salvage value (25%) 6.25

IV. Results

NPV = -$13.341

IRR = 7.50%

348

Integrated Case

Chapter 12: Cash Flow Estimation and Risk Analysis

B. (1) Allied uses debt in its capital structure, so some of the money used to

finance the project will be debt. Given this fact, should the projected

cash flows be revised to show projected interest charges? Explain.

Answer: [Show S12-10 here.] The projected cash flows in the table should

not be revised to show interest charges. The effects of debt

B. (2) Suppose you learned that Allied had spent $50,000 to renovate the

building last year, expensing these costs. Should this cost be

reflected in the analysis? Explain.

Answer: [Show S12-11 here.] This expenditure is a sunk cost; hence, it would

B. (3) Suppose you learned that Allied could lease its building to another

party and earn $25,000 per year. Should that fact be reflected in the

analysis? If so, how?

Answer: [Show S12–12 here.] The rental payment represents an opportunity

B. (4) Assume that the lemon juice project would take profitable sales away

from Allied’s fresh orange juice business. Should that fact be

reflected in your analysis? If so, how?

Answer: [Show S12-13 here.] The decreased sales from Allied’s fresh orange

Chapter 12: Cash Flow Estimation and Risk Analysis

Integrated Case

349

C. Disregard all the assumptions made in part B and assume there is no

alternative use for the building over the next 4 years. Now calculate

the project’s NPV, IRR, MIRR, and payback. Do these indicators

suggest that the project should be accepted? Explain.

Answer: [Show S12-14 here.] We refer to the completed time line and explain

how each of the indicators is calculated. We base our explanation on

350

Integrated Case

Chapter 12: Cash Flow Estimation and Risk Analysis

MIRR: 0 1 2 3 4

| | | | |

(230) 60 60 60 98.75

(1.10)2

72.60

79.86

Terminal value (TV) $317.21

Payback: Year Cash Flow Cumulative Cash Flow

0 ($230.00) ($230.00)

2 60.00 (110.00)

4 98.75 48.75

D. If this project had been a replacement rather than an expansion

project, how would the analysis have changed? Think about the

changes that would have to occur in the cash flow table.

Answer: [Show S12-15 here.] In a replacement analysis, we must find

differences in cash flows, i.e., the cash flows that would exist if we

(1.10)3

10%

Chapter 12: Cash Flow Estimation and Risk Analysis

Integrated Case

351

E. (1) What three levels, or types, of project risk are normally considered?

Answer: [Show S12-16 through S12-19 here.] Here are the three types of

project risk:

1. Stand-alone risk is the project’s total risk if it were operated

independently. Stand-alone risk ignores both the firm’s

2. Within-firm (corporate) risk is the total riskiness of the project

giving consideration to the firm’s other projects, that is, to

3. Market risk is the riskiness of the project to a well-diversified

E. (2) Which type is most relevant?

Answer: [Show S12-20 here.] Because management’s primary goal is