170

Integrated Case

Chapter 7: Bonds and Their Valuation

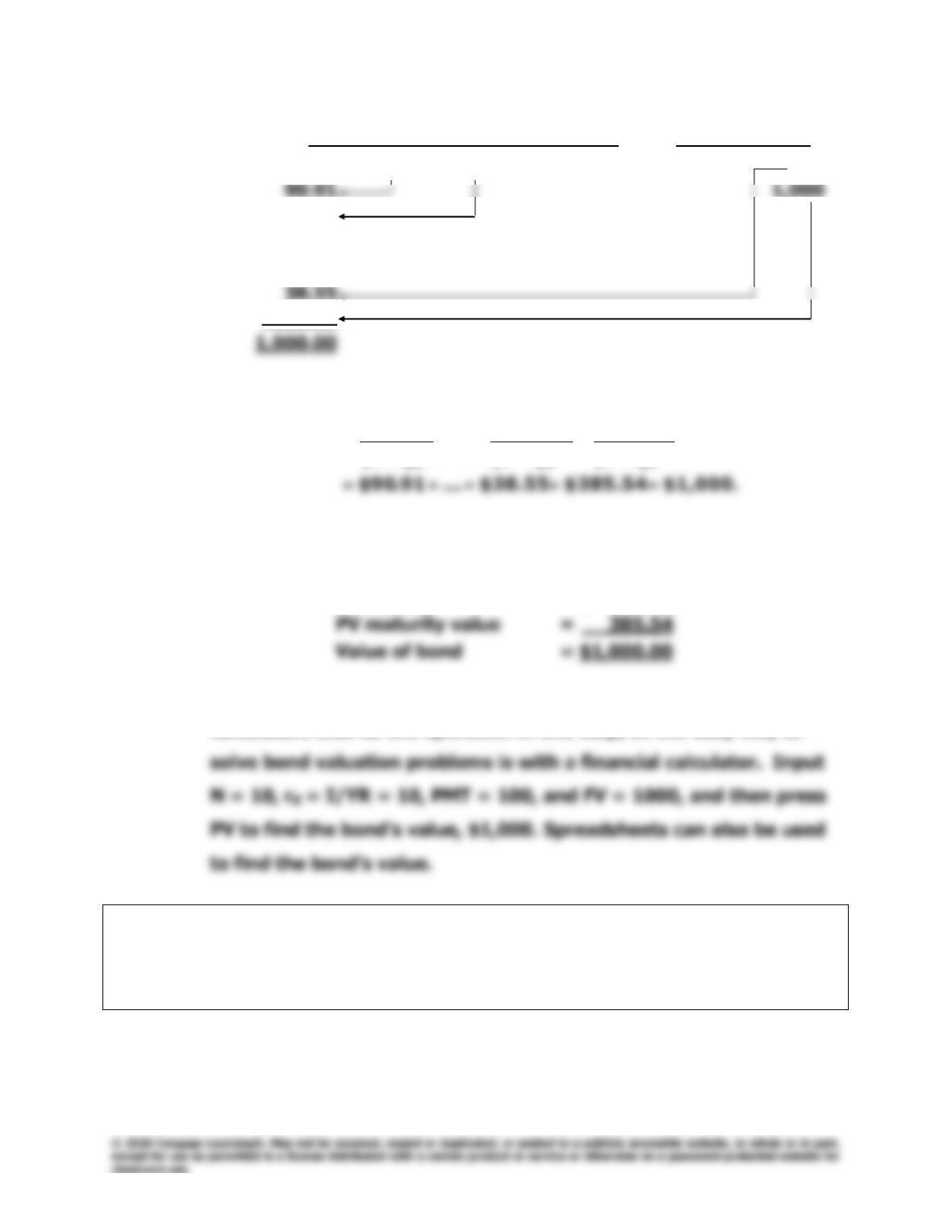

0 1 2 3 9 10

| | | | • • • | |

100 100 100 100 100

82.64

.

.

.

385.54

Expressed as an equation, we have:

)r1(

000,1$

)r(1

$100

…

)r1(

100$

V10

d

10

d

1

d

B

+

+

+

++

+

=

The bond consists of a 10-year, 10% annuity of $100 per year plus

a $1,000 lump sum payment at t = 10:

PV annuity = $ 614.46

The mathematics of bond valuation is programmed into financial

calculators that do the operation in one step, so the easy way to

E. (1) What is the value of a 13% coupon bond that is otherwise identical

to the bond described in part d? Would we now have a discount or

a premium bond?

10%

Chapter 7: Bonds and Their Valuation

Integrated Case

171

Answer: [Show S7-13 here.] With a financial calculator, just change the

value of PMT from $100 to $130, and press the PV button to

determine the value of the bond:

E. (2) What is the value of a 7% coupon bond with these characteristics?

Would we now have a discount or premium bond?

Answer: [Show S7-14 here.] In the second situation, where the coupon rate

(7%) is below the bond’s required return (10%), the price of the

E. (3) What would happen to the values of the 7%, 10%, and 13%

coupon bonds over time if the required return remained at 10%?

[Hint: With a financial calculator, enter PMT, I/YR, FV, and N; then

change (override) N to see what happens to the PV as it approaches

maturity.]

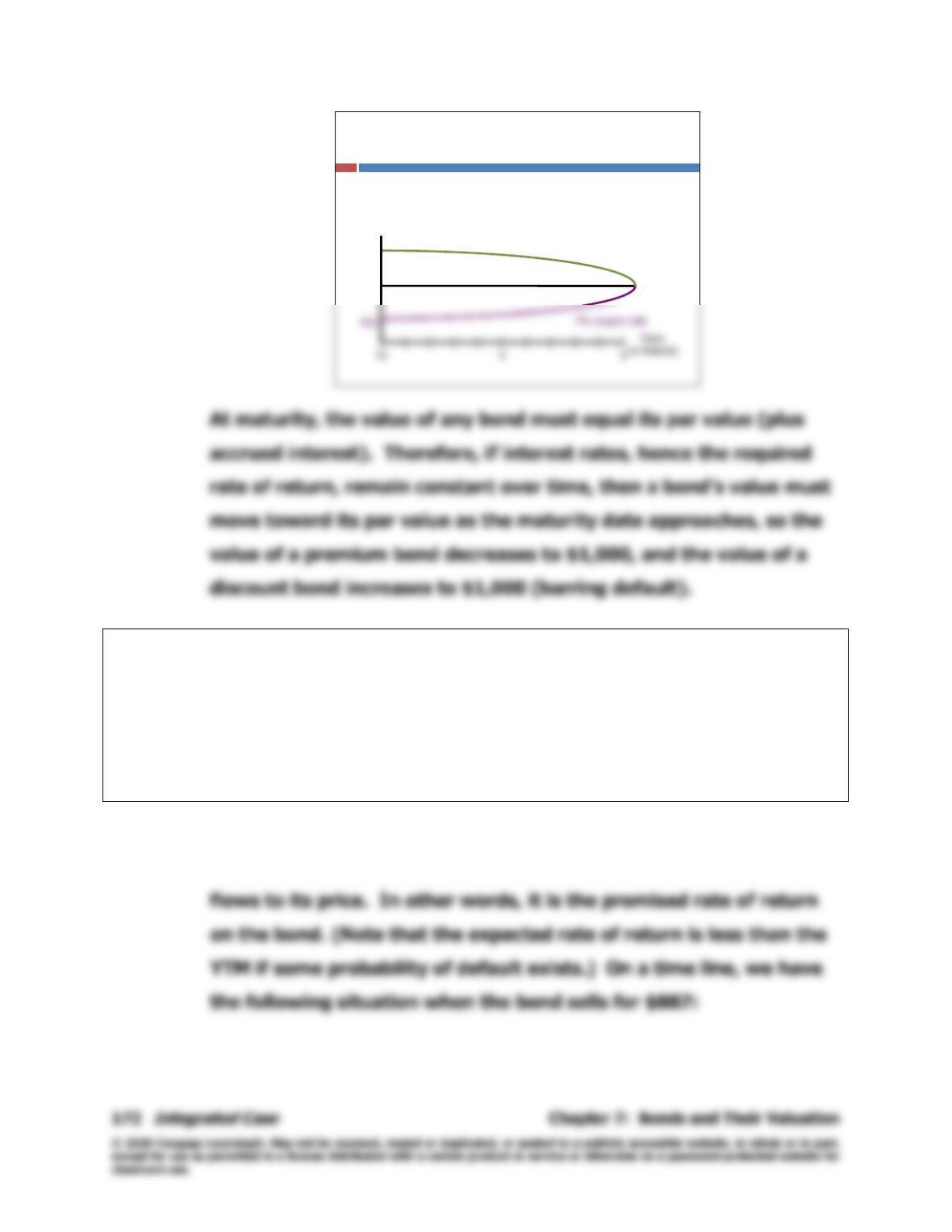

Answer: [Show S7-15 and S7-16 here.] If interest rates remain constant (at

10%), we could find the bond’s value as time passes, and as the

maturity date approaches. If we then plotted the data, we would

find the situation shown below:

Changes in Bond Value over Time

▪What would happen to the value of these

three bonds if the required rate of return

remained at 10%?

1,184

1,000

13% coupon rate

10% coupon rate

VB

F. (1) What is the yield to maturity on a 10-year, 9%, annual coupon,

$1,000 par value bond that sells for $887.00? That sells for

$1,134.20? What does the fact that it sells at a discount or at a

premium tell you about the relationship between rd and the coupon

rate?

Answer: [Show S7-17 through S7-19 here.] The yield to maturity (YTM) is

the discount rate that equates the present value of a bond’s cash

Chapter 7: Bonds and Their Valuation

Integrated Case

173

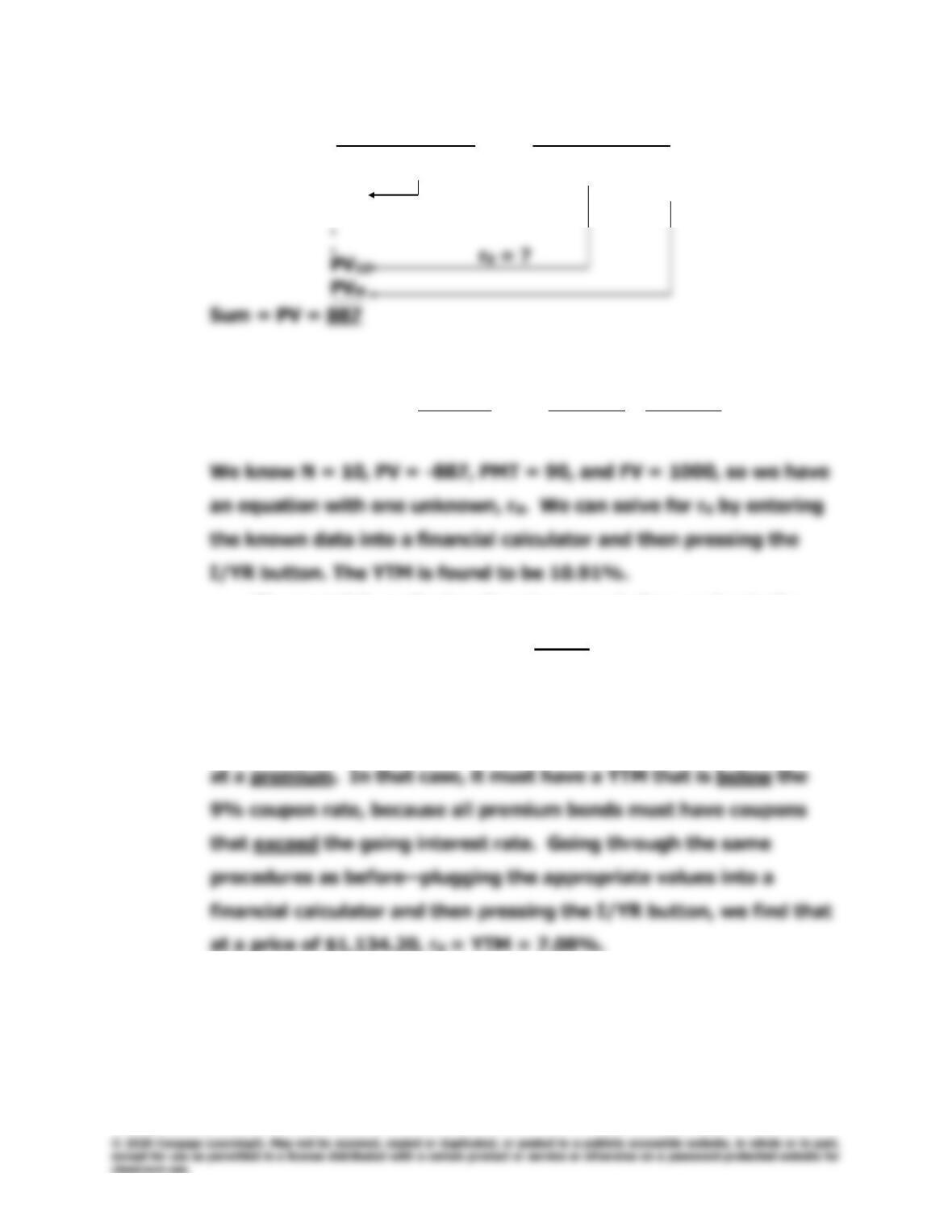

0 1 9 10

| | • • • | |

90 90 90

PV1 1,000

.

We want to find rd in this equation:

VB = PV =

N

d

N

d

1

d)r1(

M

)r(1

INT

…

)r1(

INT

+

+

+

++

+

.

We can tell from the bond’s price, even before we begin the

calculations, that the YTM must be above the 9% coupon rate. We

know this because the bond is selling at a discount, and discount

bonds always have rd > coupon rate.

If the bond were priced at $1,134.20, then it would be selling

174

Integrated Case

Chapter 7: Bonds and Their Valuation

F. (2) What are the total return, the current yield, and the capital gains

yield for the discount bond? Assume that it is held to maturity and

the company does not default on it. (Hint: Refer to footnote 6 for

the definition of the current yield and to Table 7.1.)

Answer: [Show S7-20 through S7-22 here.] The current yield is defined as

follows:

Current yield =

bond the of priceCurrent

paymentinterest coupon Annual

.

The capital gains yield is defined as follows:

Chapter 7: Bonds and Their Valuation

Integrated Case

175

until it does hold, and equilibrium is established. Therefore, for the

marginal investor:

For our 9% coupon, 10-year bond selling at a price of $887 with a

YTM of 10.91%, the current yield is:

Knowing the current yield and the total return, we can find the

capital gains yield:

YTM = Current yield + Capital gains yield

and

The capital gains yield calculation can be checked by asking this

question: “What is the expected value of the bond 1 year from

now, assuming that interest rates remain at current levels?” This is

the same as asking, “What is the value of a 9-year, 9% annual

coupon bond if its YTM (its required rate of return) is 10.91%?”

The answer, using the bond valuation function of a calculator, is

$893.87. With this data, we can now calculate the bond’s capital

gains yield as follows:

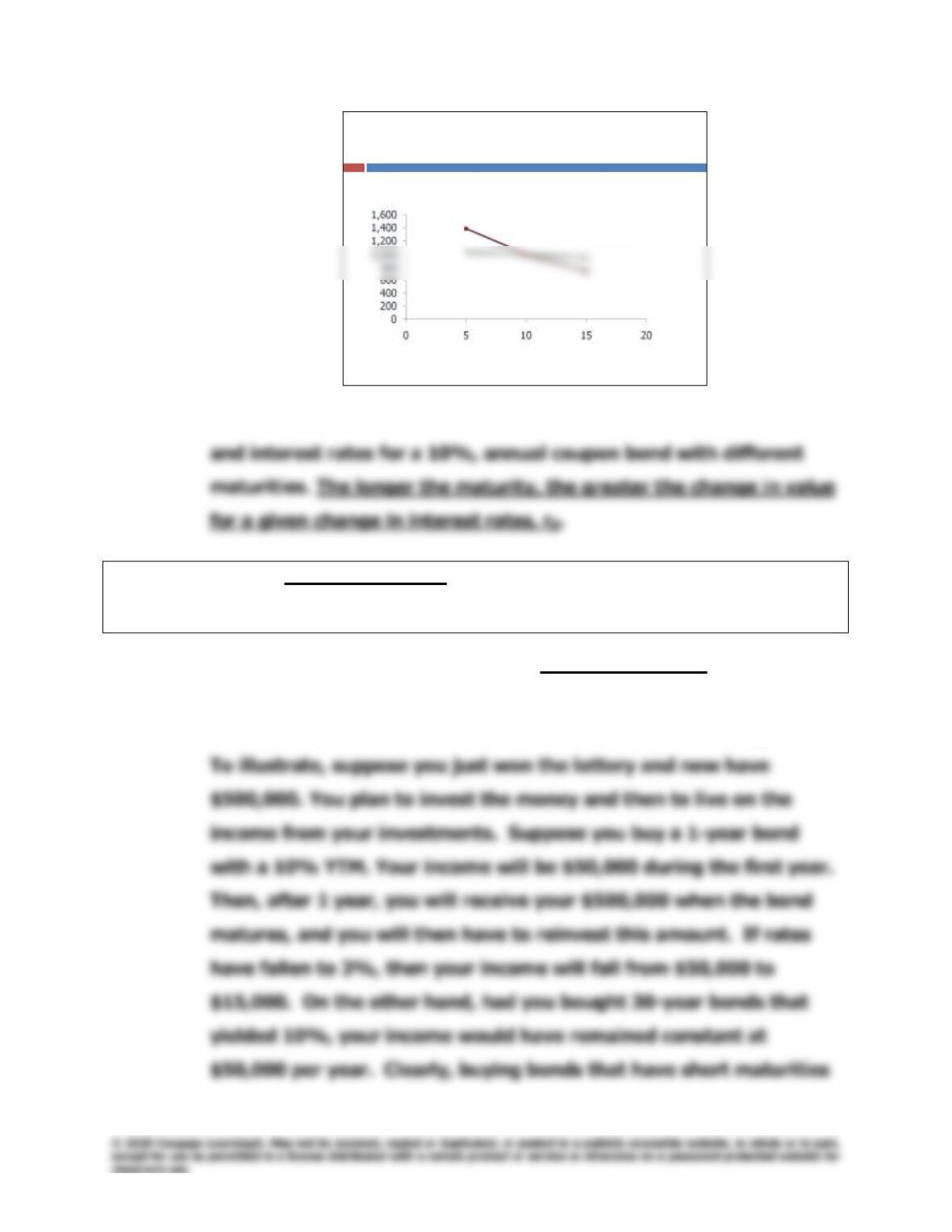

G. What is price risk? Which has more price risk, an annual payment

1-year bond or a 10-year bond? Why?

Answer: [Show S7-23 and S7-24 here.] Price risk is the risk that a bond will

lose value as the result of an increase in interest rates. The table

below gives values for a 10%, annual coupon bond at different

values of rd:

Maturity

rd 1-Year Change 10-Year Change

5% $1,048 $1,386

A 5% increase in rd causes the value of the 1-year bond to decline

Chapter 7: Bonds and Their Valuation

Integrated Case

177

©2012 Cengage Learning. All Rights Reserved. May not be scanned, copied, or duplicated, or posted to a publicly accessible website, in whole or in part.

Illustrating Price Risk

10-Year Bond

1-Year Bond

Value ($)

YTM(%)

The graph above shows the relationship between bond values

H. What is reinvestment risk? Which has more reinvestment risk, a

1-year bond or a 10-year bond?

Answer: [Show S7-25 through S7-27 here.] Reinvestment risk is defined as

the risk that cash flows (interest plus principal repayments) will

have to be reinvested in the future at rates lower than today’s rate.

178

Integrated Case

Chapter 7: Bonds and Their Valuation

carries reinvestment risk. Note that long-term bonds also have

reinvestment risk, but the risk applies only to the coupon payments,

Optional Question

Suppose a firm will need $100,000 20 years from now to replace some

equipment. It plans to make 20 equal payments, starting today, into an

investment fund. It can buy bonds that mature in 20 years or bonds that

mature in 1 year. Both types of bonds currently sell to yield 10%, i.e., rd =

YTM = 10%. The company’s best estimate of future interest rates is that they

will stay at current levels, i.e., they may rise, or they may fall, but the

expected rd is the current rd.

There is some chance that the equipment will wear out in less than 20

years, in which case the company will need to cash out its investment before

20 years. If this occurs, the company will desperately need the money that has

been accumulated—this money could save the business. How much should

the firm plan to invest each year?

Answer: Start with a time line:

0 1 2 18 19 20

| | | • • • | | |

10%

Chapter 7: Bonds and Their Valuation

Integrated Case

179

Optional Question

If the company decides to invest enough right now to produce the future

$100,000, how much is its outlay?

Answer: To find the required initial lump sum, we would find the PV of $100,000

discounted back for 20 years at 10%: PV = $14,864.36. If the

company invested this amount now and earned 10%, it would end up

180

Integrated Case

Chapter 7: Bonds and Their Valuation

0 1 2 18 19 20

| | | • • • | | |

14,864.36 100,000

1-year 16,351 ? ? Greater uncertainty

Optional Question

Can you think of any other type of bond that might be useful for this

company’s purposes?

Answer: A zero coupon bond is one that pays no interest—it has zero

coupons, and its issuer simply promises to pay a stated lump sum at

some future date. J.C. Penney was the first major company to issue

10%

Chapter 7: Bonds and Their Valuation

Integrated Case

181

PV of $100,000 discounted back 20 years at 10%. Here is the

relevant time line:

0 1 2 19 20

| | | • • • | |

Optional Question

What type of bond would you recommend that it actually buy?

Answer: It is tempting to say that the best investment for this company

would be the zeros, because they have no reinvestment risk. But

suppose the company needed to liquidate its bond portfolio in less

than 20 years; could that affect the decision? The answer is “yes.”

If 1-year bonds were purchased, an increase in interest rates would

not cause much of a drop in the value of the bonds, but if interest

rates rose to 20% the year after the purchase, the value of the

zeros would fall from the initial $14,864 to:

10%

182

Integrated Case

Chapter 7: Bonds and Their Valuation

happen under different conditions, but, in the end, a decision

involving judgment must be made.

Answer: [Show S7-28 and S7-29 here.] In reality, virtually all bonds issued

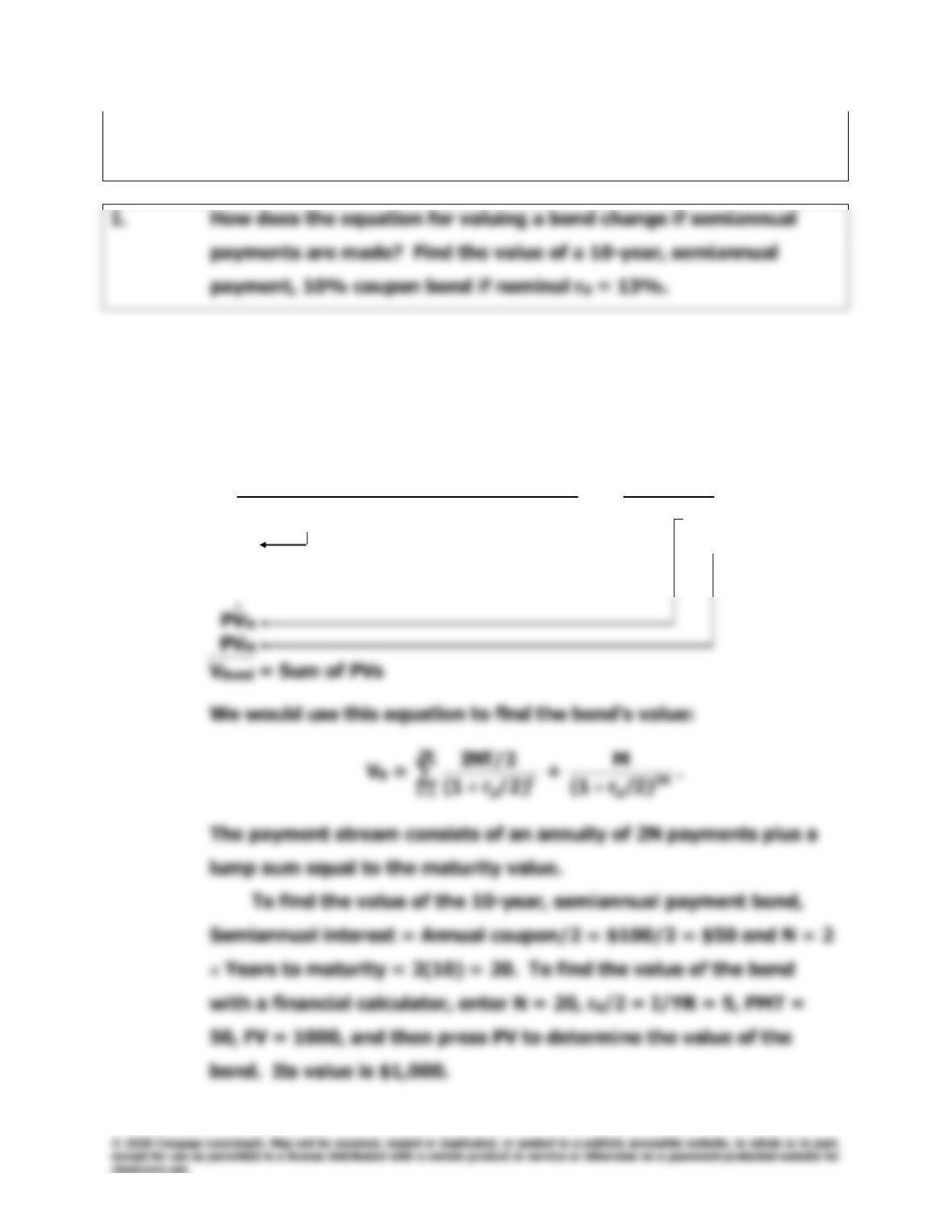

in the U.S. have semiannual coupons and are valued using the setup

shown below:

1 2 N Years

0 1 2 3 4 2N – 1 2N SA periods

| | | | | • • • | |

INT/2 INT/2 INT/2 INT/2 INT/2 INT/2

PV1 M

.

.

Chapter 7: Bonds and Their Valuation

Integrated Case

183

J. Suppose for $1,000 you could buy a 10%, 10-year, annual payment

bond or a 10%, 10-year, semiannual payment bond. They are

equally risky. Which would you prefer? If $1,000 is the proper

price for the semiannual bond, what is the equilibrium price for the

annual payment bond?

Answer: [Show S7-30 and S7-31 here.] The semiannual payment bond

would be better. Its EAR would be:

184

Integrated Case

Chapter 7: Bonds and Their Valuation

Note that, if the annual payment bond were selling for $984.80

in the market, its EAR would be 10.25%. This value can be found

by entering N = 10, PV = -984.80, PMT = 100, and FV = 1000 into a

K. Suppose a 10-year, 10%, semiannual coupon bond with a par value

of $1,000 is currently selling for $1,135.90, producing a nominal

yield to maturity of 8%. However, it can be called after 4 years for

$1,050.

(1) What is the bond’s nominal yield to call (YTC)?

Answer: [Show S7-32 and S7-33 here.] If the bond were called,

bondholders would receive $1,050 at the end of Year 4. Thus, the

time line would look like this:

Chapter 7: Bonds and Their Valuation

Integrated Case

185

which is the par value plus a call premium of $50; and then press

the I/YR button to find I/YR = 3.568%. However, this is the 6-

month rate, so we would find the nominal rate on the bond as

follows:

K. (2) If you bought this bond, would you be more likely to earn the YTM

or the YTC? Why?

Answer: [Show S7-34 and S7-35 here.] Since the coupon rate is 10% versus

YTC = rd = 7.137%, it would pay the company to call the bond, to

get rid of the obligation of paying $100 per year in interest, and to

186

Integrated Case

Chapter 7: Bonds and Their Valuation

L. Does the yield to maturity represent the promised or expected

return on the bond? Explain.

Answer: [Show S7-36 here.] The yield to maturity is the rate of return

earned on a bond if it is held to maturity. It can be viewed as the

M. These bonds were rated AA– by S&P. Would you consider them

investment-grade or junk bonds?

Answer: [Show S7-37 here.] These bonds would be investment-grade bonds.

Triple-A, double-A, single-A, and triple-B bonds are considered

N. What factors determine a company’s bond rating?

Answer: [Show S7-38 and S7-39 here.] Bond ratings are based on both

qualitative and quantitative factors, some of which are listed below.

Chapter 7: Bonds and Their Valuation

Integrated Case

187

2. Qualitative factors—bond contract terms:

a. Secured vs. unsecured debt

3. Miscellaneous qualitative factors:

a. Earnings stability

b. Regulatory environment

O. If this firm were to default on the bonds, would the company be

immediately liquidated? Would the bondholders be assured of

receiving all of their promised payments? Explain.

Answer: [Show S7-40 through S7-43 here.] When a business becomes

insolvent, it does not have enough cash to meet scheduled interest

and principal payments. A decision must then be made whether to

may call for a restructuring of the firm’s debt, in which case the

interest rate may be reduced, the term to maturity lengthened, or

If the firm is deemed to be too far gone to be saved, it will be

liquidated and the priority of claims (as seen in Web Appendix 7C)

would be as follows:

1. Secured creditors.

3. Expenses incurred after bankruptcy was filed.

5. Claims for unpaid contributions to employee benefit plans.

7. Federal, state, and local taxes.

9. General unsecured creditors.

11. Common stockholders, if anything is left.

If the firm’s assets are worth more “alive” than “dead,” the