CHAPTER 12

Aggregate Demand II:

Applying the IS–LM Model

Notes to the Instructor

1929. They may also want to draw parallels with the bursting of the so–called “Internet bubble”

and the subsequent retreat of the stock market in 2000–2001. The lessons that the Great

Depression teaches about the importance of financial and credit markets are also timely given

the problems of U.S. banks and savings institutions in the early 1990s, the Asian financial crisis

of the late 1990s, and the worldwide financial crisis of 2008-2009. (For instructors who wish to

pursue the subject of the stock market, Chapter 17 of the Instructor’s Resources contains a series

of chapter supplements on asset pricing, including discussions of stock market efficiency.)

Use of the Web Site

The Chapter 12 model can be used to derive aggregate demand curves by making use of the fact

that increases in the price level and decreases in the nominal money stock have identical effects

(this is a useful lesson to drive home anyway). Thus, one can find {M, Y} pairs for which the

money and goods markets are in equilibrium and then convert this to the corresponding {P, Y}

pairs.

Use of the Dismal Scientist Web Site

268 | CHAPTER 12 Aggregate Demand II: Applying the IS–LM Model

Chapter Supplements

This chapter includes the following supplements:

12-1 Do High Deficits Cause High Interest Rates?

12-3 Credit Rationing and the Great Depression

12-5 Proportional Income Taxes and the IS Curve

12-6 Additional Readings

Lecture Notes | 269

Lecture Notes

12–1 Explaining Fluctuations with the IS–LM Model

We have now developed the basic IS–LM model of the economy and are in a position to use it to

try to explain the behavior of the economy in the short run. Output can vary in the IS–LM model

whenever exogenous shocks to the economy cause shifts in either the IS or the LM curve.

How Fiscal Policy Shifts the IS Curve and Changes the Short–

Run Equilibrium

Let us first consider fiscal–policy shocks. Suppose that we start in equilibrium and that

government spending is increased by ∆G. Then the IS curve shifts to the right. The increased

spending increases income and, through the multiplier effects from the circular flow, also

increases consumption; income increases further. [Recall that the rightward shift of the IS curve

How Monetary Policy Shifts the LM Curve and Changes the

Short–Run Equilibrium

Now consider the effects of an increase in the money supply (an expansionary monetary policy).

This shifts the LM curve out. The increased money supply causes interest rates to fall in order to

bring the demand for money in line with the new higher supply. This fall in interest rates

encourages investment, leading ultimately to an increase in GDP. Thus, interest rates are lower

and GDP is higher. The linkage from a change in the money supply to GDP is known as the

monetary transmission mechanism.

The Interaction Between Monetary and Fiscal Policy

The policy changes discussed above took the form of an exogenous change in one policy,

holding all other exogenous variables constant. In reality, monetary and fiscal policy do not exist

in isolation from each other. The Federal Reserve and the fiscal authorities both pursue policy

goals that may or may not be compatible. We consider the details and problems of policy–

making in Chapter 18. Here we note simply that the ultimate effects of a fiscal–policy change

depend upon how the monetary authorities react to that change.

Shocks in the IS–LM Model

The IS and LM curves shift whenever they are hit by exogenous shocks. We have already

discussed how changes in fiscal policy shift the IS curve and how changes in monetary policy

shift the LM curve. The IS curve also shifts if other components of planned spending change. For

example, the “animal spirits” of businesspeople shift the IS curve. Similarly, changes in

consumer confidence alter consumption behavior and cause the IS curve to shift. Shocks to the

!

Supplement 12-1,

“Do High Deficits

Cause High

Interest Rates?”

!

Figure 12-3

!

Supplement 12–2,

“Macroeconometric

Models”

270 | CHAPTER 12 Aggregate Demand II: Applying the IS–LM Model

financial side of the economy cause the LM curve to shift. In particular, anything that causes an

exogenous increase in money demand implies an inward shift of the LM curve.

Case Study: The U.S. Recession of 2001

The U.S. economy slowed sharply in 2001, with unemployment rising and output growth

stalling. Three major shocks can help understand the onset of this economic recession. First, the

stock–market boom of the 1990s ended abruptly in the spring of 2000 as optimism about new

information technology waned. The decline in the stock market lowered the wealth of

households and, in turn, lowered consumer spending. Also, the dimmed outlook for new

technologies led to a pullback in business investment. These effects can be interpreted as a shift

to the left in the IS curve. Second, the September 11 terrorist attacks on New York and

Washington led to a further decline in the stock market—which, at the time, was the largest one–

What Is the Fed’s Policy Instrument—the Money Supply or the

Interest Rate?

The analysis in this chapter assumes that the Fed influences the economy by controlling the

money supply, but the Fed’s short–term policy instrument is an interest rate target (the federal

funds rate). These are not inconsistent. To control the federal funds rate (the rate banks charge

one another for overnight loans), the Fed conducts open–market operations. These open–market

operations change the money supply, shifting the LM curve and thus changing the interest rate.

12–2 IS–LM as a Theory of Aggregate Demand

From the IS–LM Model to the Aggregate Demand Curve

We now consider how the IS–LM model can also be viewed as a theory of aggregate demand.

We defined the IS and LM curves in terms of equilibrium in the goods and money markets,

respectively. Aggregate demand summarizes equilibrium in both of these markets.

Thus we find that the aggregate demand curve is downward sloping; high values of the price

!

Figure 12-6

Lecture Notes | 271

The IS–LM Model in the Short Run and Long Run

We can also analyze the transition to the long run in the IS–LM model. If the economy is not at

full employment, then the price level adjusts. In terms of the AD–AS diagram, the economy

moves along the AD curve. In terms of the IS–LM diagram, the LM curve shifts. Thus we can see

that the process of adjustment to equilibrium has subtle economic forces lying behind it. If, for

example, we start in recession, then over time prices fall. This increases the real money supply,

pushing down interest rates and encouraging investment. This increase in investment, in turn,

leads to higher spending and higher GDP.

As another example, suppose that, starting in long–run equilibrium at the natural rate of

output, we increase government spending. In the short run, with the price level fixed, this leads

12–3 The Great Depression

In the 1930s, the United States and other economies experienced a severe depression. The desire

to explain this phenomenon was Keynes’s principal motivation for his new approach to

economics. The magnitude of the economic upheaval and the accompanying human misery, in

turn, fascinate economists and lead them to study the Great Depression to avoid any recurrence

of such an event. The data for the Great Depression years are set out in Table 12-1. Economists

have suggested a number of explanations for these data, each of which may contain part of the

truth.

The Spending Hypothesis: Shocks to the IS Curve

The IS–LM model teaches that an inward shift in the IS curve reduces income and interest rates.

Since nominal interest rates fell during the Depression, negative shocks to the IS curve are one

possible explanation. This is the spending hypothesis. Significant falls occurred in both

consumption and investment spending between 1929 and 1933. Consumption may have fallen

The Money Hypothesis: A Shock to the LM Curve

A particularly striking feature of the Depression–era data is the substantial fall in the money

supply (over 25 percent between 1929 and 1933). A monetary contraction shows up in the IS–

LM model as an inward shift of the LM curve, which would reduce output. There are two

problems with this money hypothesis, however. The first is that prices also fell substantially over

The Money Hypothesis Again: The Effects of Falling Prices Another aspect of

the money hypothesis is that even if both money and prices fell so that real money balances

changed little and the LM curve was hardly affected, the deflation itself might have played a

!

Figure 12-7

!

Table 12-1

!

Supplement 12–3,

“Credit Rationing

and the Great

272 | CHAPTER 12 Aggregate Demand II: Applying the IS–LM Model

major role in the Depression. The basic IS–LM model suggests that falling prices increase output

because falling prices increase real money balances for any given money supply. Falling prices

might also increase output because of the Pigou effect: Decreases in the price level increase the

real value of wealth, increasing consumption and shifting the IS curve out.

Other arguments, however, suggest that deflation might decrease output. Consider first the

effect of an unexpected fall in the price level. As explained in Chapter 5, this represents a

redistribution, in real terms, from debtors to creditors; a given nominal debt becomes larger in

real terms. Now suppose that creditors and debtors also differ in terms of their marginal

propensities to consume. In particular, it is reasonable to think that debtors have higher

propensities to consume than do creditors. Then the redistribution from debtors to creditors

reduces aggregate spending, shifting the IS curve in. This is known as the debt–deflation theory.

In an IS–LM diagram with the nominal interest rate on the vertical axis and income on the

horizontal axis, the position of the IS curve depends upon the expected inflation rate. Higher

expected inflation lowers the real interest rate, increases investment, and shifts the IS curve to

the right, thereby increasing output and raising the nominal interest rate. Conversely, lower

expected inflation (or higher expected deflation) raises the real interest rate, reduces investment,

and shifts the IS curve to the left, reducing output and lowering the nominal interest rate. .

Could the Depression Happen Again?

After the major stock market fall of October 1987, some commentators worried about whether

this might presage a severe decline in economic activity, just as the 1929 stock market crash did.

While economists cannot be completely confident that such a severe depression will never recur,

our greater understanding of the macroeconomy today does give modern policymakers a

significant advantage over their 1930s counterparts. Above all, the Fed is likely to avoid

Case Study: The Financial Crisis and the Great Recession of

2008 and 2009

During 2008, the U.S. economy experienced a financial crisis and economic downturn that to

some observers mirrored events from the 1930s. The crisis began with a boom in the housing

market a few years earlier, the result of low interest rates that made buying a home more

affordable. Increased use of securitization in the mortgage market further fueled the housing

boom by making it easier for subprime borrowers to obtain credit. These borrowers had a higher

risk of default that may not have been fully appreciated by the purchasers of mortgage–backed

securities (banks and insurance companies). The high level of house prices proved unsustainable

!Figure 12-8

!Table 12-2

Lecture Notes | 273

and prices fell by 30 percent from 2006–2009. This decline had several repercussions that

intensified what was a moderate–to–severe house–price correction into a full–blown crisis.

First, mortgage defaults and home foreclosures increased sharply, in large part due to loose

mortgage–lending standards that had permitted little or no money down on home purchases. As

prices fell, these homeowners were “under water,” and many decided to stop paying on their

mortgages. Sales of foreclosed properties further depressed house prices. Second, numerous

financial institutions suffered heavy losses on the mortgage–backed securities that they owned.

As a result, banks cut back on lending to other banks out of fear and distrust that they might not

be repaid. Third, companies that rely on the financial system for funds to run their business

found it difficult to obtain short–term loans. Concern about the profitability of these companies

led to sharp swings in their stock prices. Finally, gyrations in stock prices, in turn, led to a sharp

decline in consumer confidence and resulted in a huge drop in consumer spending.

Government responded strongly to the crisis. The Fed lowered its target for the federal

funds rate from 5.25 percent in September 2007 to approximately zero in December 2008.

Congress appropriated $700 billion for the Treasury to use to stabilize the financial system by

The Liquidity Trap (also known as the Zero Lower Bound) Interest rates

reached levels close to zero in the United States during the 1930s and, more recently, during late

2008, when the Fed lowered its target for the federal funds rate to a range of zero to 0.25 percent

and kept it there for several years. Economists refer to this situation as a liquidity trap. Because

nominal interest rates cannot fall below zero, an expansion in the money supply would not be

able to lower nominal interest rates and therefore might not be able to affect spending. The

economy could become “trapped” at a low level of aggregate demand, output, and income. But

since spending directly depends on real interest rates rather than nominal rates, a higher rate of

inflation could push real interest rates below zero and stimulate spending. This is the reason why

some economists argue for targeting a rate of inflation that is above zero—say, around 4 percent

per year. Such an inflation target would give the central bank the ability to lower the real interest

12-4 Conclusion

The IS–LM model with fixed prices is still an incomplete model of the economy in the short run.

!Supplement 12–4,

275

12–1 Do High Deficits Cause High Interest Rates?

The IS–LM model of Chapter 12 predicts that expansionary fiscal policy—that is, increases in government

spending or decreases in taxes, both of which imply increases in the deficit—leads to high interest rates.

Increases in the deficit increase the demand for goods and services and thus shift the IS curve to the right.

The associated increase in income increases the demand for money, and so interest rates must rise to keep

the money market in equilibrium. In the long run, the effect is even stronger: Increases in the price level

cause the LM curve to shift back to the left, resulting in still higher interest rates. This can be seen

equivalently in the classical model of Chapter 3; that model shows how increases in the deficit decrease

national saving and so increase interest rates.

Increases in interest rates in turn imply reduced investment—crowding out—in both the short run and

the long run. Economists worry, therefore, that high deficits imply low levels of investment, leading

ultimately to a lower capital stock and so lower living standards. It is, therefore, important to see if this

prediction that high deficits lead to high interest rates is supported by the data.1

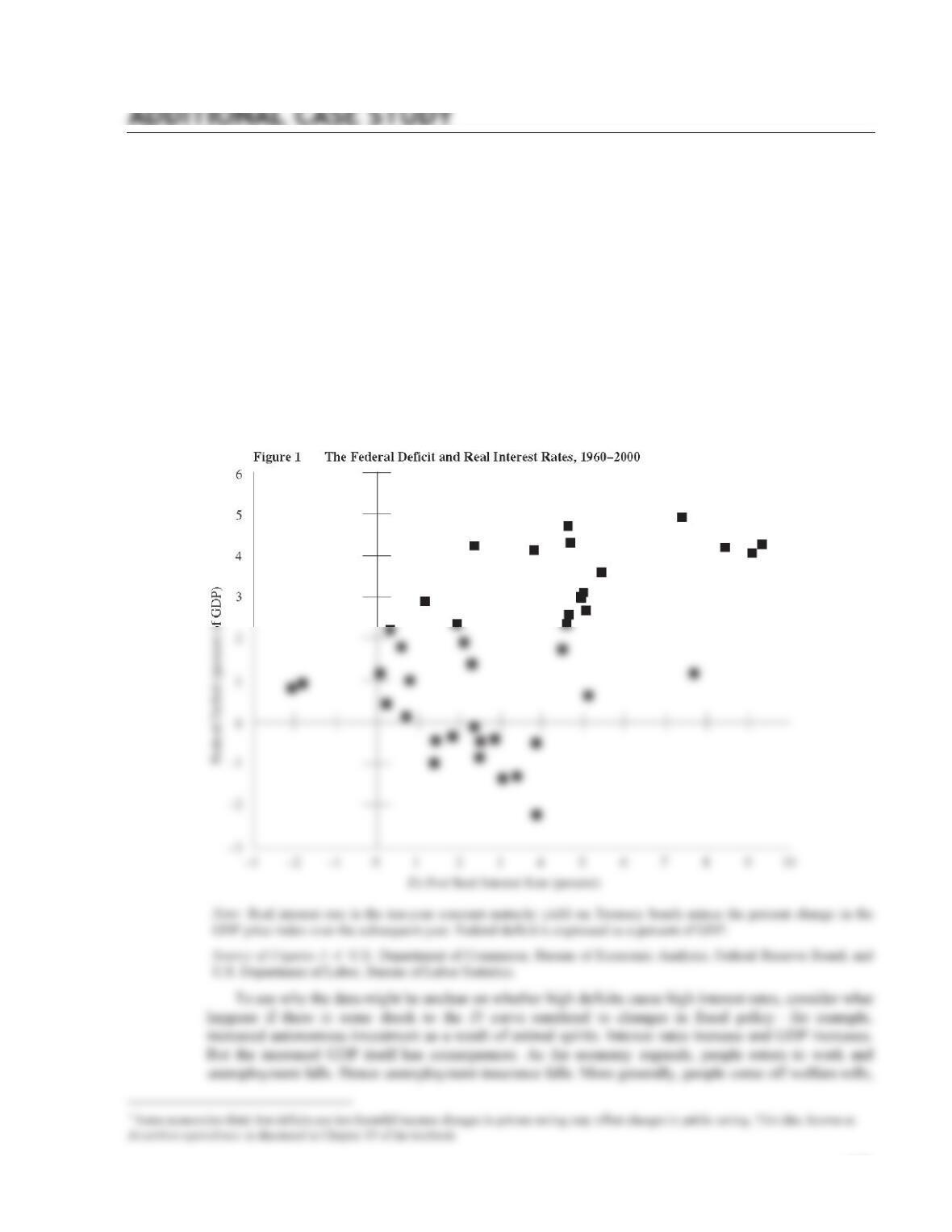

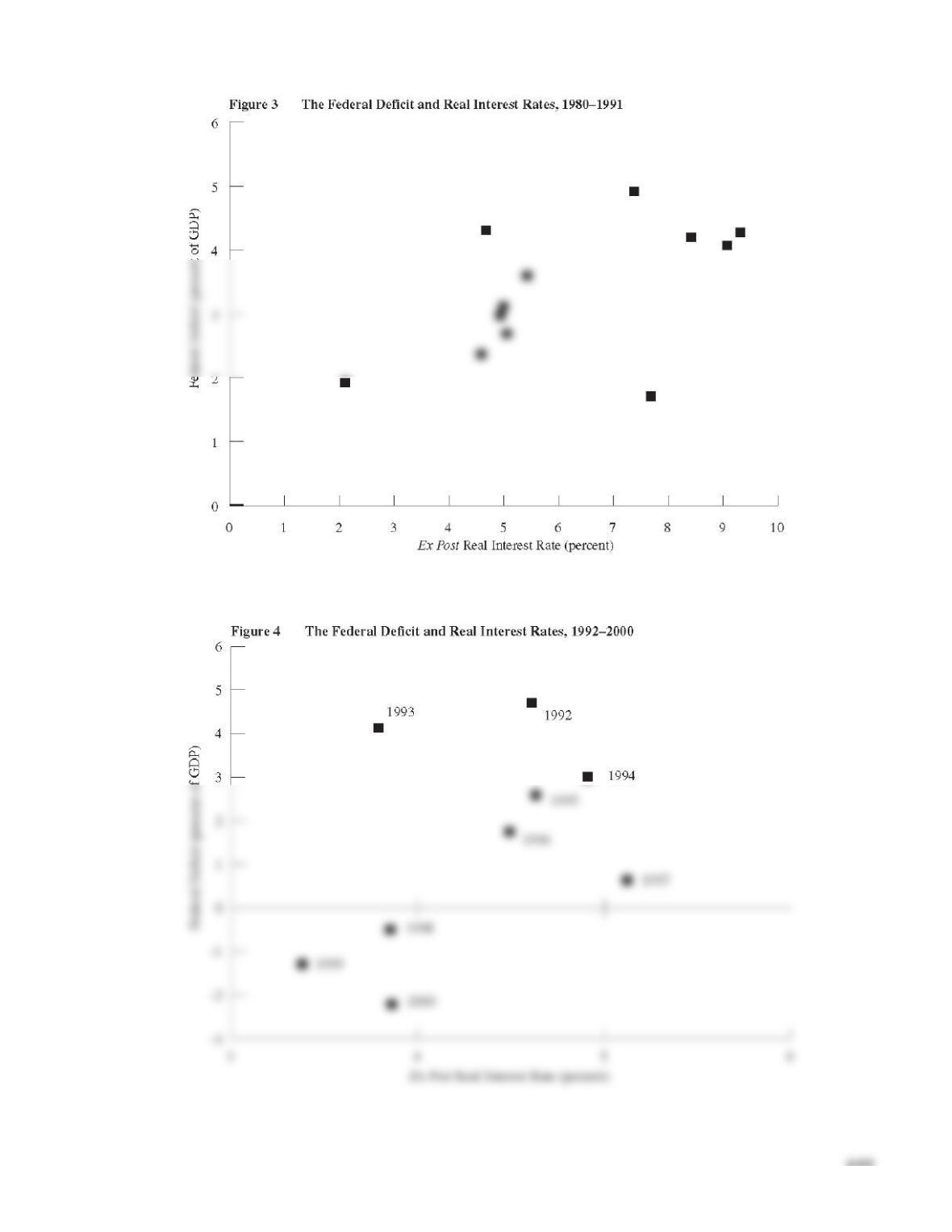

Like many empirical questions in economics, this one is difficult to answer unequivocally. Figure 1

shows a scatterplot of the real government deficit and the ex post real interest rate between 1960 and 2000.

While there is some evidence of a positive association, it is not strong.

and transfers such as Medicaid fall. Further, increased GDP means that the government takes in more in

tax revenues. The presence of these automatic stabilizers results in a decrease in the deficit. (Automatic

stabilizers are discussed in more detail in Chapter 18 of the textbook.) In the data, we would observe

interest rates rising and the deficit falling, although there was no direct causal link between the two. Figure

2 illustrates this relationship between the unemployment rate and the federal deficit.

Exactly the opposite would occur given an LM shock (the result, for example, of a change in money

demand or money supply). If the LM curve shifts out, we observe interest rates falling and the deficit

falling, but again with no causal link. The data are thus likely to be substantially contaminated by these

sorts of effects, since shocks other than changes in the deficit are likely to swamp the effects of exogenous

changes in the deficit. Overall, economists have not yet managed categorically to establish either the

presence or the absence of a link between deficits and interest rates.2

277

Although interest rates rose at first as the deficit declined, they fell sharply during the last three years

of the decade. Thus, disentangling the effect of deficits on real interest rates remains a difficult task.

ADDITIONAL CASE STUDY

12–2 Macroeconometric Models

To estimate the magnitude of the effects of policy changes, economists sometimes use large–scale

macroeconometric models of the economy. These models use statistical and econometric techniques to

analyze the economy. On the basis of existing data, it is possible to obtain estimates of the magnitude of

key parameters, such as the marginal propensity to consume. The model with these estimated parameters

Fair’s model is more complicated partly because he considers more disaggregated data (and so has

three different consumption functions, for example), partly because he considers labor–market variables

and asset–market variables that are not included in a simple IS–LM model, and partly because he considers

price adjustment.

Models such as Fair’s were initially developed in the 1950s, and at one time the refinement of these

criticism. Lucas pointed out that these models might not be good for evaluating different economic

policies because agents will change their behavior in response to changed policies. Thus, according to

Lucas, it does not make sense to suppose that a behavioral equation estimated under one set of policies

will be unchanged when policies are changed.

Fair, not surprisingly, is a strong advocate of the usefulness of large–scale models of the economy,

ADDITIONAL CASE STUDY

12–3 Credit Rationing and the Great Depression

Economist and former Fed Chair Ben Bernanke has made a strong case that failures in credit markets were

an important aspect of the Great Depression.1 As noted in Chapter 12 of the textbook, this is an element of

the spending hypothesis. Bernanke documents the connection between the decline in output in the

1983): 257–76.

LECTURE SUPPLEMENT

12-4 The Simple Algebra of the IS–LM Model and Aggregate Demand

Curve

The IS Curve

To analyze the mathematics of the IS curve, let us suppose that

C(Y – T) = a + b(Y – T)

explains how much Y changes for a given change in G, holding r fixed. It thus tells us how far to the right

the IS curve shifts for a given increase in G. (See Supplement 12-5, “Proportional Income Taxes and the IS

Curve” for details of how proportional taxes affect the IS curve.)

The LM Curve

Let us suppose a simple linear expression for money demand:

L(r, Y) = eY – fr

⇒ M/P = eY – fr.

The Aggregate Demand Curve

Substituting for r from the LM curve into the IS curve yields

Y=1

1−b

a+c+G−bT

( )

−d elf

( )

Y−1 / f

( )

M/P

( )

( )

⇒Y1+de /f

+M/P

The Effectiveness of Monetary and Fiscal Policy

Around the 1960s, the biggest debate in macroeconomics was probably the one centering on the relative

efficacy of fiscal and monetary policies. Some economists implied that d was small by arguing that

investment was not very responsive to the interest rate. The aggregate demand equation then implies that

monetary policy cannot have a big effect on output. When investment does not respond to interest rate

changes, a crucial link in the monetary transmission mechanism breaks down. We can interpret this in

terms of the IS–LM diagram: When d is small, the IS curve is steep, so shifts in the LM curve result in

large changes in interest rates and small changes in GDP.

Other economists, known as monetarists, believed that money demand was not very responsive to the

LECTURE SUPPLEMENT

12-5 Proportional Income Taxes and the IS Curve

The textbook makes the simplifying assumption that the level of (net) tax revenue, T, is independent of the

level of GDP. In reality, we expect that T is likely to increase as Y increases. There are two reasons for

this. First, income taxes are important in the United States. Income taxes imply that the government

collects more tax revenue when income is higher. Second, transfer payments go down as income

increases—when the economy is booming, more people are employed, so unemployment insurance and

The remainder of our analysis is as before:

C = a + b(Y – T)

I = c – dr.

Substituting into the goods–market equilibrium condition (Y = C + I + G), we get

Y=a+b Y –T

( )

+c–dr +G

Our earlier equation for the IS curve was

Y=1

1−b

⎛

⎝

⎜⎞

⎠

⎟a+c+G−bT

( )

−dr

( )

.

Comparing the two, we see that the new IS curve no longer contains a bT term. This is because the level of

tax revenue, T, is no longer an exogenous variable in the model. More important, we see that the multiplier

term, which was previously 1/(1 – b), is now 1/(1 – b(1 – t)). Proportional income taxes reduce the value

of the multiplier. This can be understood in terms of the circular flow of income. Suppose, as considered

in the text, government purchases are increased. This increases GDP and so increases income. But now

1 See also the discussion of the Great Depression in Chapter 12 of the textbook and Supplement 12–1, “Do High Deficits Cause High Interest Rates?”

LECTURE SUPPLEMENT

12-6 Additional Readings

The Spring 1993 edition of the Journal of Economic Perspectives contains a symposium on the Great

Depression, with articles by Christina Romer, Robert Margo, Charles Calomaris, and Peter Temin.

Economists have, of course, written a great deal on the Depression; a good place to start is Peter Temin’s

book, Lessons From the Great Depression (Cambridge, Mass.: MIT Press, 1989).

For some interpretations of the most recent recession, see G. Perry and C. Schultze, “Was This

Recession Different? Are They All Different?” Brookings Papers on Economic Activity 1 (1993): 145–