12/10/2012

Chapter 11 Mini Case

Situation

Analysis of New Expansion Project

Part I: Input Data

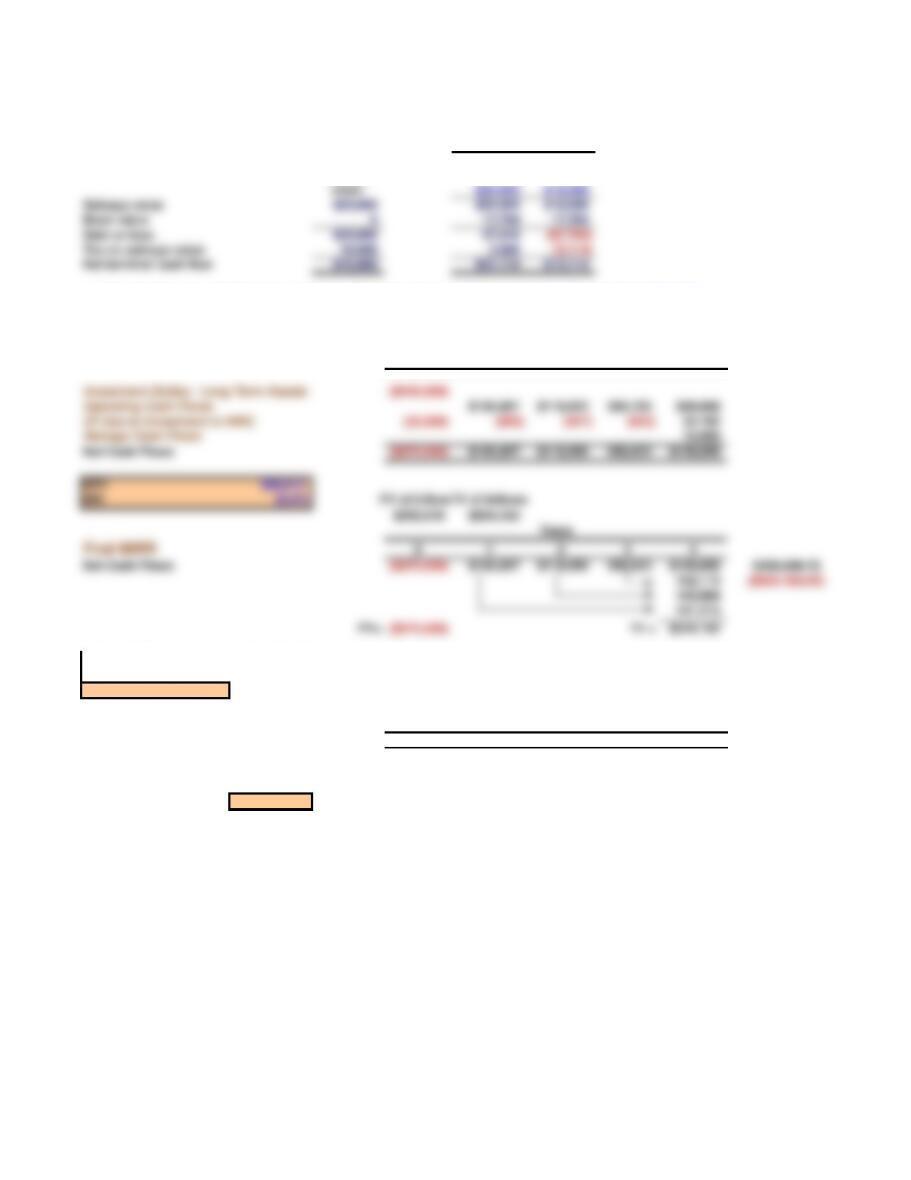

Equipment cost $200,000 Key Output: NPV = $88,010

Shipping charge $10,000

Installation charge $30,000

Economic Life 4

Salvage Value $25,000

Annual Depreciation Expense

Depreciable Basis = Equipment + Freight + Installation

Depreciable Basis = $240,000

Shrieves Casting Company is considering adding a new line to its product mix, and the capital budgeting

analysis is being conducted by Sidney Johnson, a recently graduated MBA. The production line would be set

up in unused space in Shrieves’ main plant. The machinery’s invoice price would be approximately $200,000,

another $10,000 in shipping charges would be required, and it would cost an additional $30,000 to install the

equipment. The machinery has an economic life of 4 years, and Shrieves has obtained a special tax ruling

that places the equipment in the MACRS 3-year class. The machinery is expected to have a salvage value of

$25,000 after 4 years of use.

The new line would generate incremental sales of 1,250 units per year for 4 years at an incremental cost of

$100 per unit in the first year, excluding depreciation. Each unit can be sold for $200 in the first year. The

sales price and cost are expected to increase by 3% per year due to inflation. Further, to handle the new line,

the firm’s net working capital would have to increase by an amount equal to 12% of sales revenues. The firm’s

tax rate is 40%, and its overall weighted average cost of capital is 10%.

a. Define “incremental cash flow.” Answer: See Chapter 11 Mini Case Show

(2.) Suppose the firm had spent $100,000 last year to rehabilitate the production line site. Should this be

included in the analysis? Explain. Answer: See Chapter 11 Mini Case Show

(1.) Should you subtract interest expense or dividends when calculating project cash flow? Answer: See

(3.) Now assume that the plant space could be leased out to another firm at $25,000 per year. Should this

be included in the analysis? If so, how? Answer: See Chapter 11 Mini Case Show

Show

b. Disregard the assumptions in Part a. What is Shrieves’ depreciable basis? What are the annual

depreciation expenses?

Tax Rate 40%

Cost of Capital 10%

Units Sold 1,250

Sales Price Per Unit $200

Incremental Cost Per Unit $100

Annual Operating Cash Flows

Year 1 Year 2 Year 3 Year 4

Units 1,250 1,250 1,250 1,250

Unit price $200.00 $206.00 $212.18 $218.55

Unit cost $100.00 $103.00 $106.09 $109.27

Depreciation 79,992 106,680 35,544 17,784

Operating income before taxes (EBIT) $45,008 $22,070 $97,069 $118,807

Taxes (40%) 18,003 8,828 38,827 47,523

Depreciation 79,992 106,680 35,544 17,784

Annual Cash Flows due to Investments in Net Working Capital

NWC (% of sales) 30,000 30,900 31,827 32,782

CF due to investment in NOWC) (30,000) (900) (927) (955) 32,782

d. Construct annual incremental operating cash flow statements.

e. Estimate the required net working capital for each year, and the cash flow due to investments in net

working capital.

c. Calculate the annual sales revenues and costs (other than depreciation). Why is it important to include

inflation when estimating cash flows? See answer to part d.

f. Calculate the after-tax salvage cash flow.

After-tax Salvage Value

Based on

facts in

Projected Net Cash Flows

Year 0 Year 1 Year 2 Year 3 Year 4

Net Cash Flows ($270,000) $106,097 $118,995 $92,830 $136,850

Net Cash Flows ($270,000) $106,097 $118,995 $92,830 $136,850 $358,009.72

MIRR = 18.0%

Find Payback

0 1 2 3 4

Cash Flow ($270,000) $106,097 $118,995 $92,830 $136,850

Cumulative Cash Flow for Payback ($270,000) ($163,903) ($44,908) $47,922 $184,772

Payback = 2.5

Hypothetical: If sold

after 3 years for

Years

g. Calculate the net cash flows for each year. Based on these cash flows, what are the project’s NPV, IRR,

MIRR, and payback? Do these indicators suggest the project should be undertaken?

To find MIRR, we could now find the discount rate that equates the PV and TV. But it is easier to use the MIRR

function.

Salvage value $25,000 $25,000 $10,000

Book value 0 17,784 17,784

Gain or loss $25,000 $7,216 ($7,784)

Tax on salvage value 10,000 2,886 (3,114)

Net terminal cash flow $15,000 $22,114 $13,114

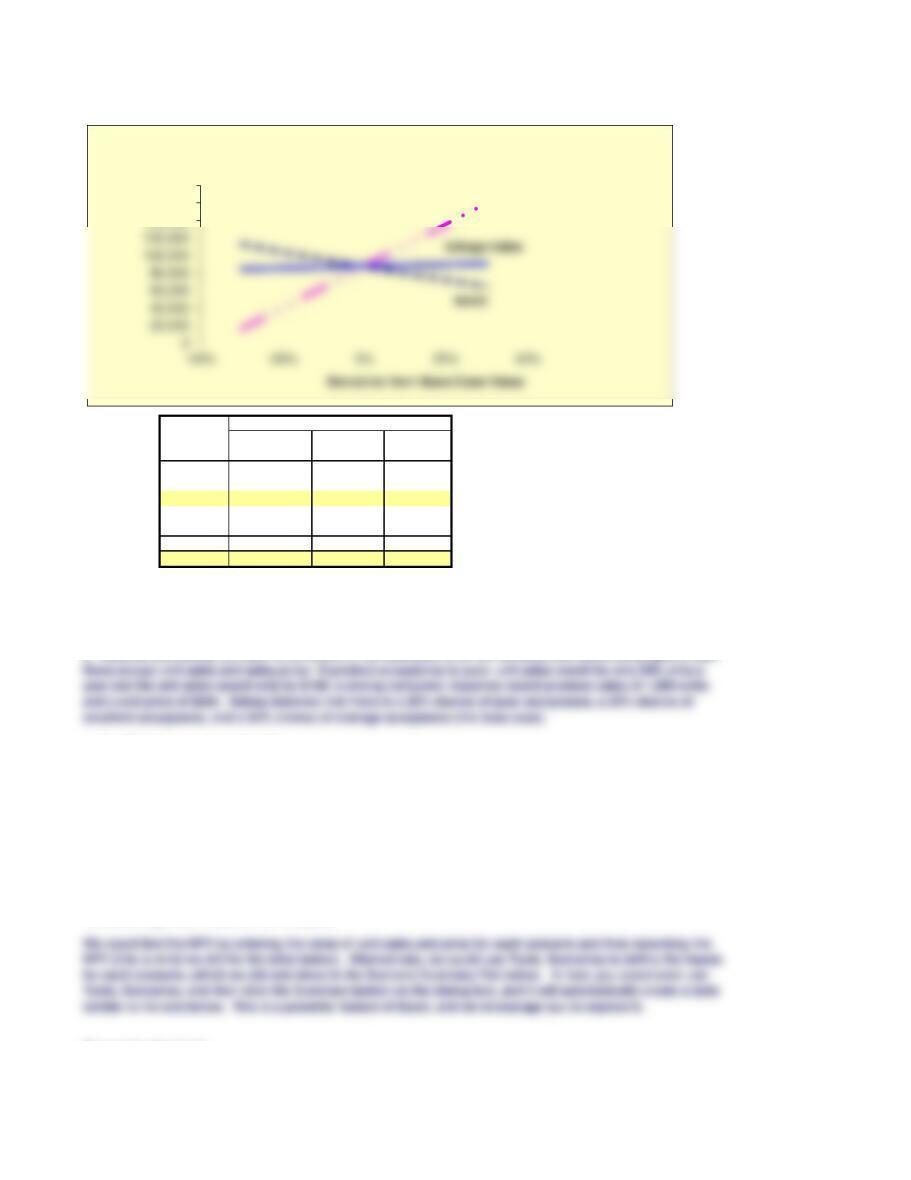

Evaluating Risk: Sensitivity Analysis

Sensitivity of NPV and to Variations in Input Variables

i. (1.) What are the three types of risk that are relevant in capital budgeting? Answer: See Chapter 11 Mini

Case Show

(3.) How is each type of risk used in the capital budgeting process? Answer: See Chapter 11 Mini Case

Show

(2.) Perform a sensitivity analysis on the unit sales, salvage value, and cost of capital for the project.

Assume that each of these variables can vary from its base-case, or expected, value by plus and minus 10%,

20%, and 30%. Include a sensitivity diagram, and discuss the results.

(2.) How is each of these risk types measured, and how do they relate to one another? Answer: See

Chapter 11 Mini Case Show

h. What does the term ”risk” mean in the context of capital budgeting; to what extent can risk be quantified;

and when risk is quantified, is the quantification based primarily on statistical analysis of historical data or on

subjective, judgmental estimates?

Risk in capital budgeting really means the probability that the actual outcome will be worse than the expected

outcome. For example, if there were a high probability that the expected NPV as calculated above will actually

examine the project’s sensitivity to changes in the input variables.

j. (1.) What is sensitivity analysis? Answer: See Chapter 11 Mini Case Show

Evaluating Risk: Sensitivity Analysis

Deviation NPV Deviation from Base Case

from Units

Base Case WACC Sold Salvage

-30% $113,270 $16,649 $84,936

-15% 100,291 52,329 86,473

0% 88,010 88,010 88,010

15% 76,378 123,690 89,546

30% 65,350 159,371 91,083

Range $47,920 $176,020 $6,147

Evaluating Risk: Scenario Analysis

Scenario Analysis

(3.) What is the primary weakness of sensitivity analysis? What is its primary usefulness? Answer: See

Chapter 11 Mini Case Show

and a unit price of $240. Sidney believes that there is a 25% chance of poor acceptance, a 25% chance of

excellent acceptance, and a 50% chance of average acceptance (the base case).

k. Assume that Sidney Johnson is confident of her estimates of all the variables that affect the project’s cash

(1.) What is scenario analysis?

(2.) What is the worst-case NPV? The best-case NPV?

(3.) Use the worst-, most likely, and best-case NPVs and probabilities of occurrence to find the project’s

expected NPV, standard deviation, and coefficient of variation.

Scenario analysis extends risk analysis in two ways: (1) It allows us to change more than one variable at a

time, hence to see the combined effects of changes in several variables on NPV, and (2) it allows us to bring

in the probabilities of changes in the key variables.

140,000

160,000

180,000

NPV ($)

Sensitivity Analysis

Units Sold

Probability Unit Sales Unit Price NPV

Monte Carlo Simulation

Risk Adjusted Cost of Capital

(2.) Shrieves typically adds or subtracts 3 percentage points to the overall cost of capital to adjust for risk.

Should the new line be accepted?

(3.) Are there any subjective risk factors that should be considered before the final decision is made?

Answer: See Chapter 11 Mini Case Show

Squared Deviation

times Probability

n. What is a real option? What are some types of real options? Answer: See Chapter 11 Mini Case Show

m. (1.) Assume that Shrieves’ average project has a coefficient of variation in the range of 0.2 to 0.4. Would

the new line be classified as high risk, average risk, or low risk? What type of risk is being measured here?

Answer: See Chapter 11 Mini Case Show

Monte Carlo simulation is similar to scenario analysis in that different values of key input variables are used.

Unlike scenario analysis, Monte Carlo simulation draws the input values from specified probability

distributions and then computes the NPV. It repeats this process hundreds, or even thousands, of times. It

then averages the NPVs from each repetition.

Scenario

l. Are there problems with scenario analysis? Define simulation analysis, and discuss its principal

advantages and disadvantages. Answer: See Chapter 11 Mini Case Show

Scenario Summary

Current Values: Base Case Best Case Worst Case Base-but forget inflation

Changing Cells:

$D$36 $200,000 $200,000 $200,000 $200,000 $200,000

$D$37 $10,000 $10,000 $10,000 $10,000 $10,000

$D$38 $30,000 $30,000 $30,000 $30,000 $30,000

$D$39 4 4 4 4 4

$D$40 $25,000 $25,000 $25,000 $25,000 $25,000

Result Cells:

12/10/2012

Analysis of New Expansion Project

Part I: Input Data

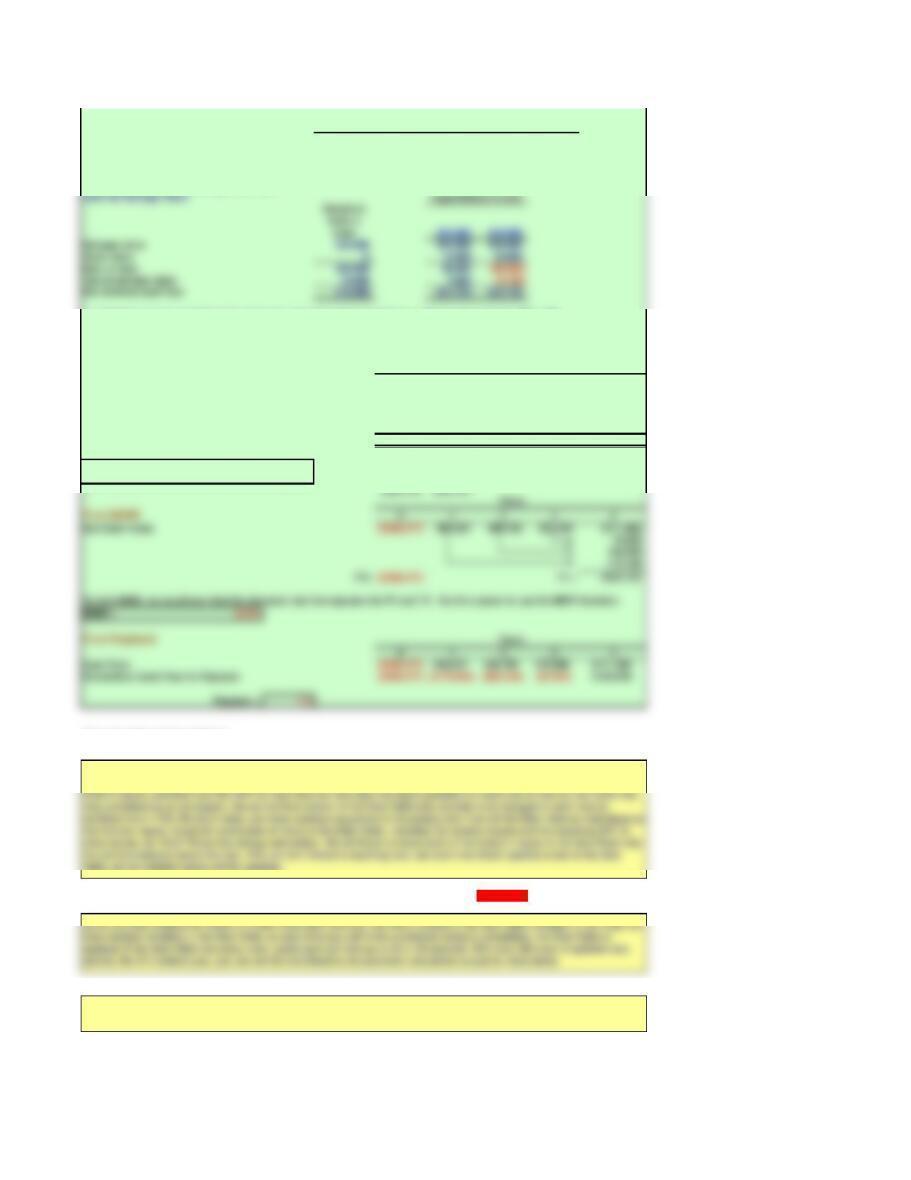

Equipment cost $200,000 Key Output: NPV = $25,263

Shipping charge $10,000

Installation charge $30,000

Economic Life 4

Salvage Value $25,000

Annual Depreciation Expense

Depreciable Basis = Equipment + Freight + Installation

Depreciable Basis = $240,000

Year % x Basis = Depr.

Remainin

g Book

Value

Annual Operating Cash Flows

Year 1 Year 2 Year 3 Year 4

Units 1,279 1,279 1,279 1,279

Unit price $172.53 $177.70 $183.03 $188.52

Unit cost $100.00 $103.00 $106.09 $109.27

Depreciation 79,200 108,000 36,000 16,800

Operating income before taxes (EBIT) $13,551 ($12,467) $62,397 $84,551

Taxes (40%) 5,420 (4,987) 24,959 33,820

Depreciation 79,200 108,000 36,000 16,800

Annual Cash Flows due to Investments in Net Working Capital

e. Estimate the required net working capital for each year, and the cash flow due to investments in net working

capital.

Section 11.7 Scenario Analysis

Monte Carlo simulation is similar to scenario analysis in that different values of key inputs are used Unlike scenario

analysis, Monte Carlo simulation draws a trial set of input values from specified probability distributions and then computes

the NPV for this trial. This process is repeated for hundreds, or even thousands, of trials, with key results (like NPV) saved

from each trial. After running the number of desired trials, the NPVs from the trials can be averaged to estimate the project’s

expected NPV; the trial results can also be used to provide a histogram showing the project’s possible outcomes.

c. Calculate the annual sales revenues and costs (other than depreciation). Why is it important to include

inflation when estimating cash flows? See answer to part d.

b. Disregard the assumptions in Part a. What is Shrieves’ depreciable basis? What are the annual

d. Construct annual incremental operating cash flow statements.

Tax Rate 40%

Units Sold Random variable = 1,279 1,250 200

Sales Price Per Unit Random variable = $173 $200 $30

Incremental Cost Per Unit $100

Inflation rate 3%

Year 0 Year 1 Year 2 Year 3 Year 4

Sales $220,638 $227,257 $234,072 $241,093

NWC (% of sales) 26,477 27,271 28,089 28,931

CF due to investment in NOWC) (26,477) (794) (818) (842) 28,931

f. Calculate the after-tax salvage cash flow.

Projected Net Cash Flows

Year 0 Year 1 Year 2 Year 3 Year 4

Investment Outlay: Long Term Assets

($240,000)

Operating Cash Flows

$87,331 $100,520 $73,438 $67,531

CF due to investment in NWC

(26,477) (794) (818) (842) 28,931

Salvage Cash Flows 15,000

Net Cash Flows ($266,477) $86,537 $99,702 $72,596 $111,462

NPV $25,263

IRR 14.2%

PV of Inflows

TV of Inflows

Find MIRR 0 1 2 3 4

Net Cash Flows ($266,477) $86,537 $99,702 $72,596 $111,462

MIRR = 12.5%

Cash Flow ($266,477) $86,537 $99,702 $72,596 $111,462

Cumulative Cash Flow for Payback ($266,477) ($179,940) ($80,239) ($7,642) $103,819

How the Simulation Works

Column input cell to “trick” Excel into updating random variables in Data Table: 1Don’t change the the red cell.

You don’t need to change anything in this section. It will be updated automatically if you do a simulation. The summary of

the simulation results and the histogram are based on the simulation trials n the Data Table below and are updated

automatically when you do a simulation. You can do an updated simulation by hitting the F9 key.

g. Calculate the net cash flows for each year. Based on these cash flows, what are the project’s NPV, IRR,

MIRR, and payback? Do these indicators suggest the project should be undertaken?

We use a Data Table to perform the simulation (the Data Table is below, shaded bright yellow). When the Data Table is

updated, it will insert new random variables for each of the inputs we allow to change in Panel A above, run the analysis is

Table, all the random values will be updated.

Salvage value $25,000 $25,000 $10,000

Book value 0 16,800 16,800

Gain or loss $25,000 $8,200 ($6,800)

Tax on salvage value 10,000 3,280 (2,720)

Net terminal cash flow $15,000 $21,720 $12,720

Number of Trials = 100

Scratch work for chart: see comments.

Count

Range bottom 0Percent

-$306,270 0 0%

-$284,393 0 0%

-$262,517 0 0%

-$240,640 0 0%

-$218,764 0 0%

-$196,888 0 0%

Output of Simulation in Data Table

Trial Number Units Sold

Sales

Price Per

Unit

NPV

1,279 $173 $25,263

1 1549.2439 180.2574 85565.0196

2 1129.057 179.04317 19050.6786

3 1368.9238 217.06253 156031.855

4 1200.4633 169.08357 6501.97329

5 1450.8464 189.49232 96629.5009

6 1615.3433 231.87061 257558.829

7 1374.3042 233.06231 199956.285

8 1346.0799 179.36168 52339.3347

9 1253.4387 237.49918 179987.48

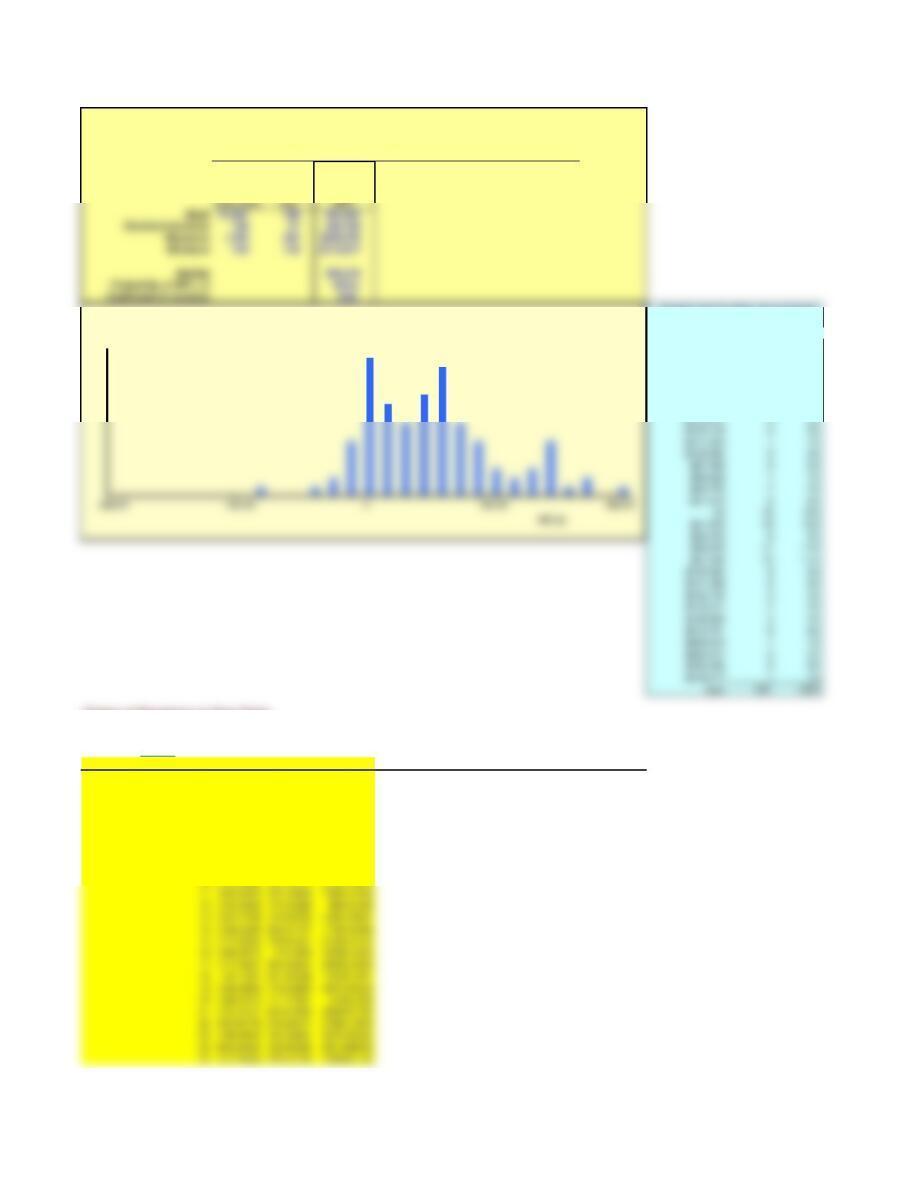

Figure 11-27 Summary of Simulation Results (Thousands of Dollars)

Sales

Price Per

Simulated Input Variables and Key Results

Key Results:

Probability

Units Sold

26 1089.8577 168.87897 -8340.68356

35 1457.0543 236.69662 231295.079

36 839.81992 205.21054 18473.7454

37 1255.1591 183.29047 48262.2957

38 1439.4991 183.68336 78464.0382

39 1631.8013 202.99668 170182.963

40 1209.3076 142.71423 -54288.6856

41 1300.2693 181.3835 50568.53

42 1334.3627 173.10723 34372.7179

43 1255.085 212.75838 120106.707

44 1248.0614 203.11229 95200.7859

45 1313.894 162.64423 4843.02397

59 1178.7318 207.88691 92529.7312

60 1157.4502 186.23583 39471.0865

61 1292.4625 196.49043 87298.8929

62 1349.0912 198.34679 102555.175

63 1403.2338 241.40022 230038.457

64 1083.5914 117.69926 -116876.905

65 964.58781 188.72092 12577.1982

66 1182.9824 219.51536 120120.093

75 1374.1586 227.40936 184825.811

76 1326.809 168.43704 21285.9497

77 898.88534 192.19184 7580.74606

78 1684.7558 189.52012 136457.391

79 1475.9078 200.646 132877.43

80 959.45861 221.37248 72572.4393

81 1347.2946 163.46753 10923.7853

82 1761.5787 235.32555 306269.661

83 1405.7894 187.88447 84592.1369

84 1514.2106 196.10571 126851.781

85 1308.3114 253.48184 235052.125

86 1151.9958 214.15883 101063.259

87 1148.4777 227.99731 131170.839

88 1099.4388 237.74523 139989.164