11 Chapter model 12/12/2018

NET PRESENT VALUE (Section 11-2)

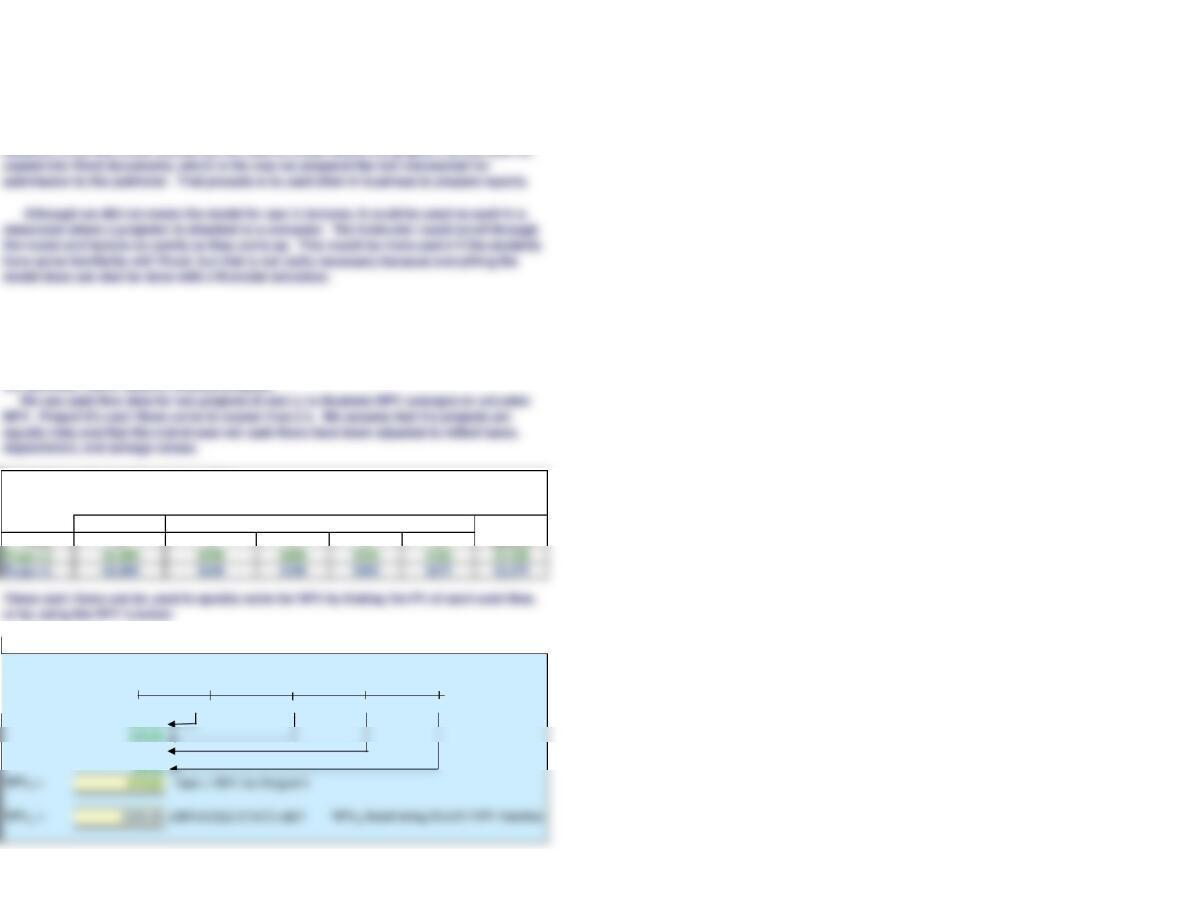

Table 11.1 Data on Projects S and L

WACC for both projects = 10%

Initial Cost Total

Year 0 1 2 3 4 Inflows

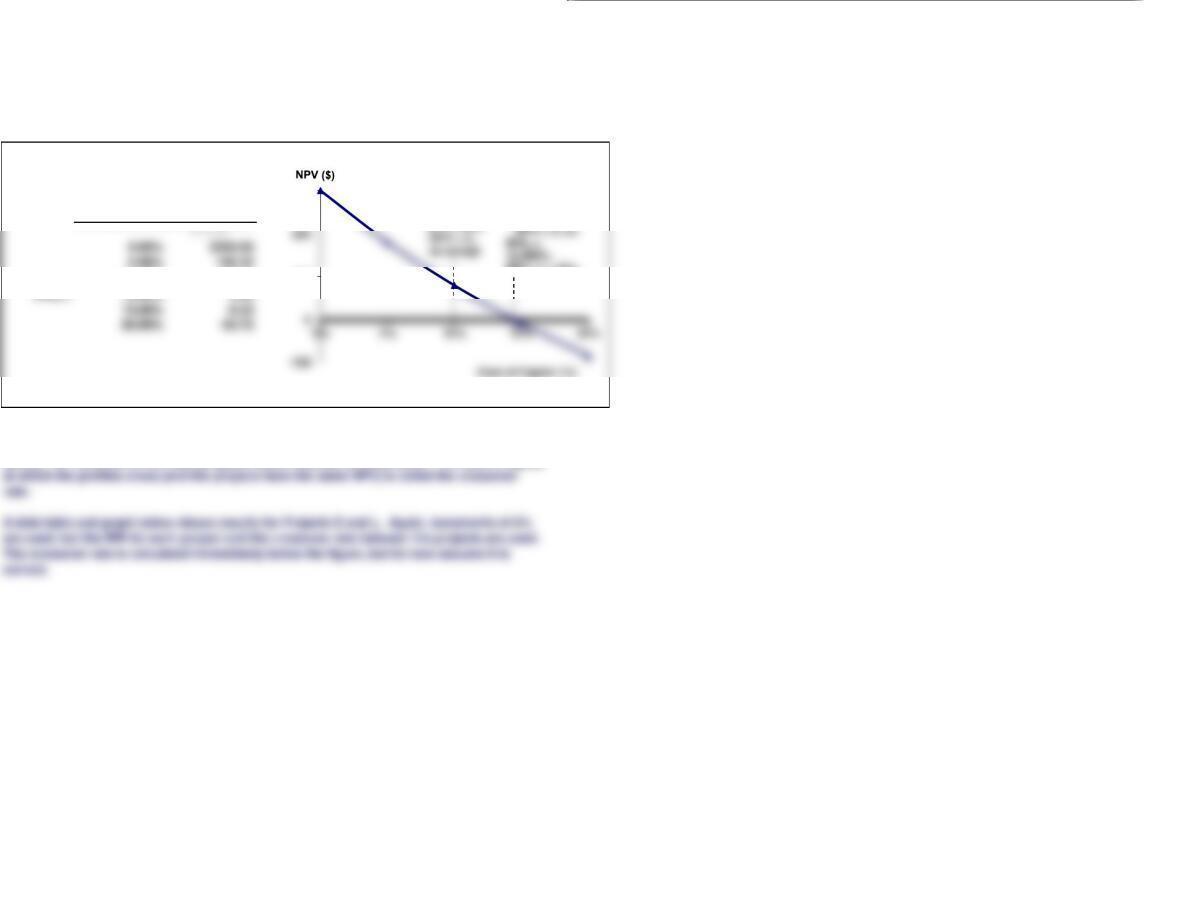

Figure 11.1 Finding the NPV for Projects S and L

0 1 2 3 4

-1,000.00 500 400 300 100

454.55

225.39

9/12/22 4:00 PM

Chapter 11. The Basics of Capital Budgeting

The Net Present Value (NPV) method estimates how much a potential project contributes to

shareholder wealth and is the primary capital budgeting decision criterion. While other

capital budgeting tools are important and provide valuable information, the NPV is clearly

the dominant metric used to evaluate projects.

We used this model to create most of the chapter exhibits (Tables and Figures). We pasted

in a few dialog boxes for specific Excel functions and features and show them off to the

right of where they apply, but in general we encourage students who want to know more

about Excel to use the Excel Tutorial and refer to it as necessary. We also like to let

students know that Excel models can be used to create tables and graphs that can then be

depreciation, and salvage values.

After-Tax, End-of-Year Cash Inflows, CFt

Project S

r = 10%

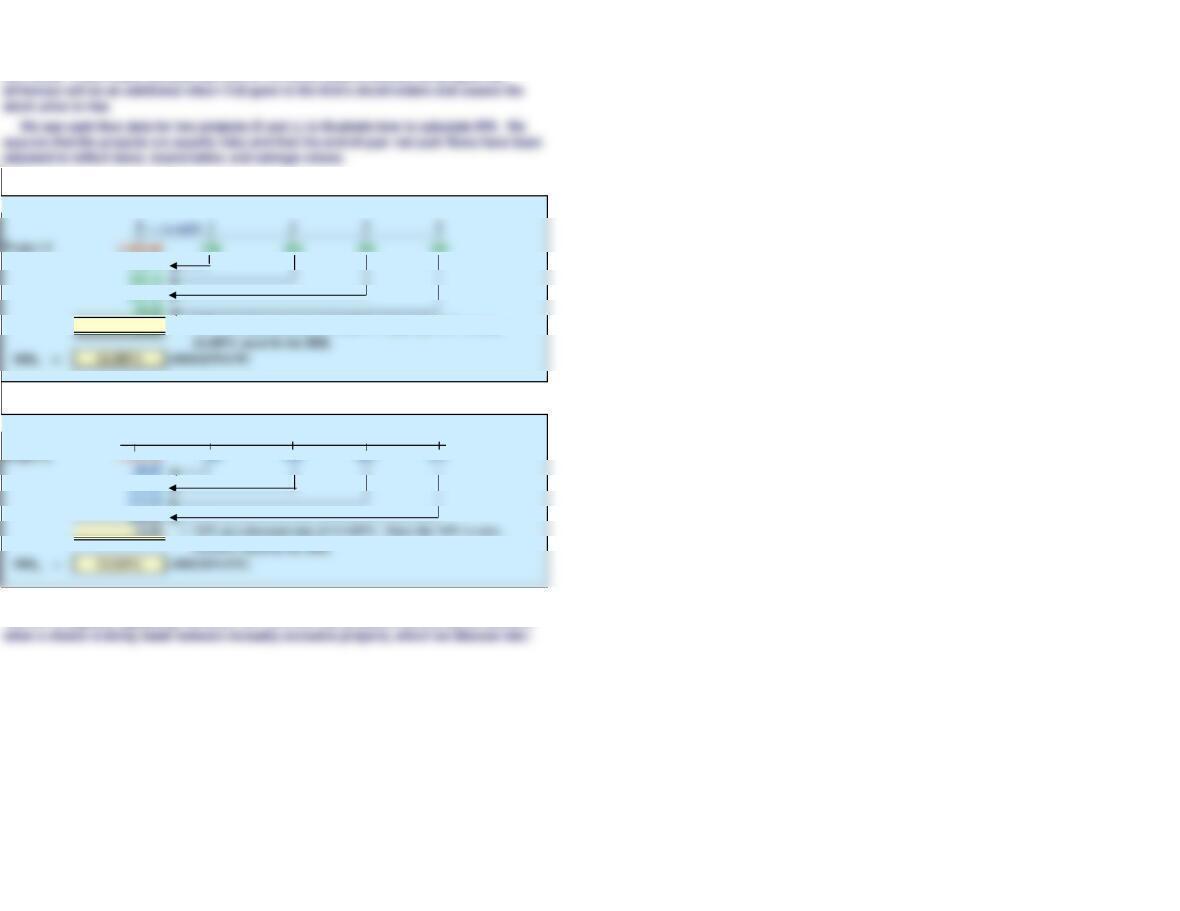

INTERNAL RATE OF RETURN (Section 11-3)

Figure 11.2 Finding the IRR for Project S

436.72

$0.00 = NPV at a discount rate of 14.489%. Since the NPV is zero,

Finding the IRR for Project L

0 1 2 3 4

232.68

The Internal Rate of Return (IRR) is the discount rate that forces a project’s NPV to equal

zero. The IRR is an estimate of the project’s rate of return, and it is comparable to the YTM

on a bond. If this return exceeds the cost of the funds used to finance the project, the

The IRR is logically appealing; however, NPV and IRR can produce conflicting conclusions

r = 13.549%

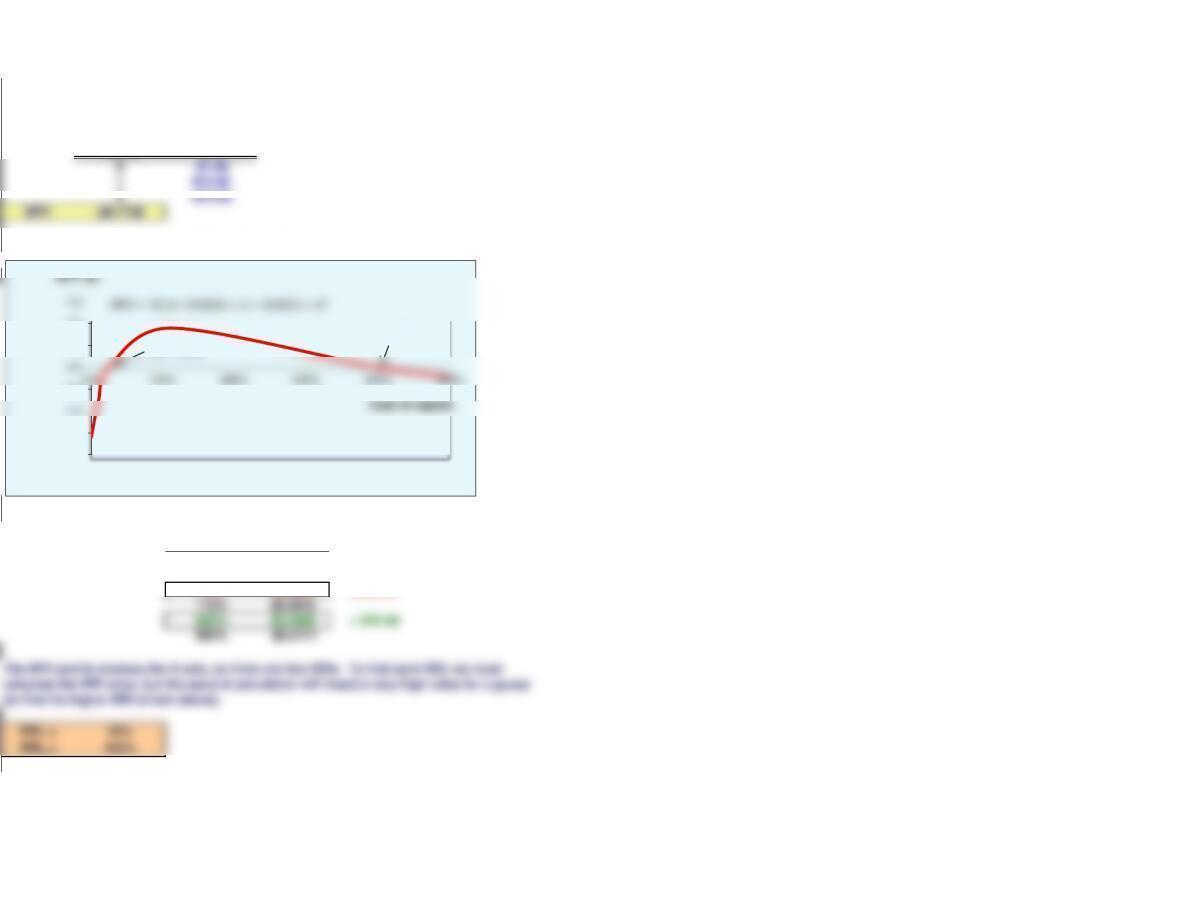

MULTIPLE IRRs (Section 11-4)

Multiple IRRs: NPV profile and IRR calculation

WACC 10%

Project M

Year (t) CFs

Figure 11.3 Graph for Multiple IRRs: Project M

WACC = 10%

Discount

Rate

NPV

0% -$1.6000

10% -$0.7736

25% $0.0000 = IRR #1

If a project has nonnormal cash flows (more than one sign change), the project may have

multiple IRRs. Consider Project M below, which has nonnormal cash flows. Construct an

NPV profile for Project M and determine its IRRs.

-2.0

-1.5

-0.5

0.5

1.0

IRR = 400%

IRR = 25%

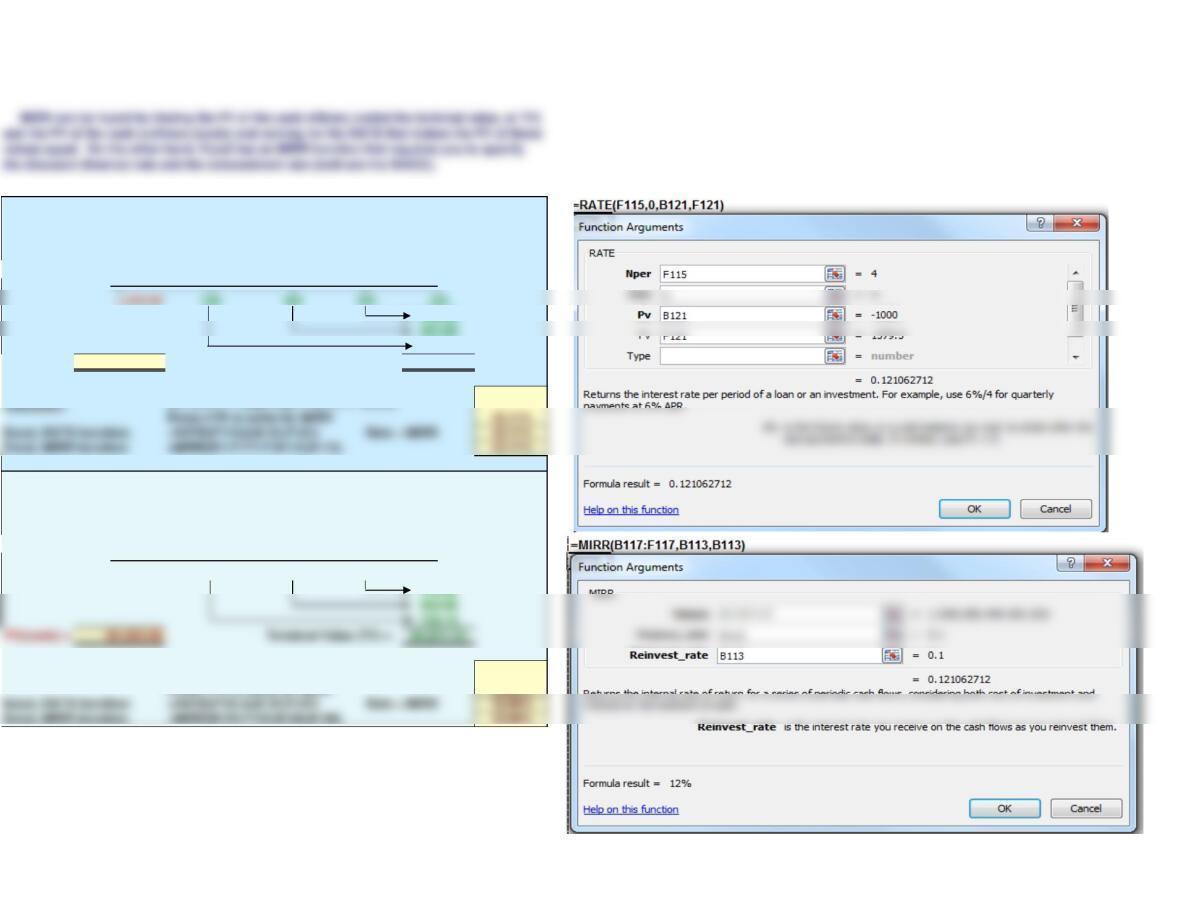

MODIFIED IRR (Section 11-6)

Figure 11.4 Finding the MIRR for Project S, WACC = 10%

WACC = 10%

Project S 0 1 2 3 4

330.00

484.00

665.50

PV(costs) = -$1,000.00 $1,579.50

Press I/YR to solve for MIRR

Finding the MIRR for Project L, WACC = 10%

WACC = 10%

Project L 0 1 2 3 4

| | | | |

-1,000.00 100 300 400 675

440.00

363.00

133.10

PV(costs) = -$1,000.00 $1,611.10

Calculator: 12.66%

The MIRR calculates a project’s expected rate of return based upon the assumption that

cash flows are reinvested at the cost of capital, rather than the IRR. The MIRR uses a better

reinvestment assumption than the IRR and is immune to the multiple IRR problem. For

these reasons, many analysts believe it is a better indicator of relative profitability.

N = 4, PV = -1000, PMT = 0, FV = 1579.5,

N = 4, PV = -1000, PMT = 0, FV = 1611.1,

Press I/YR to solve for MIRR

Terminal Value (TV) =

NPV PROFILES (Section 11-7)

Figure 11.5 NPV Profile for Project S

Cost of

Capital

NPVS

10.00% 78.82

IRRS = 14.49% 0.00

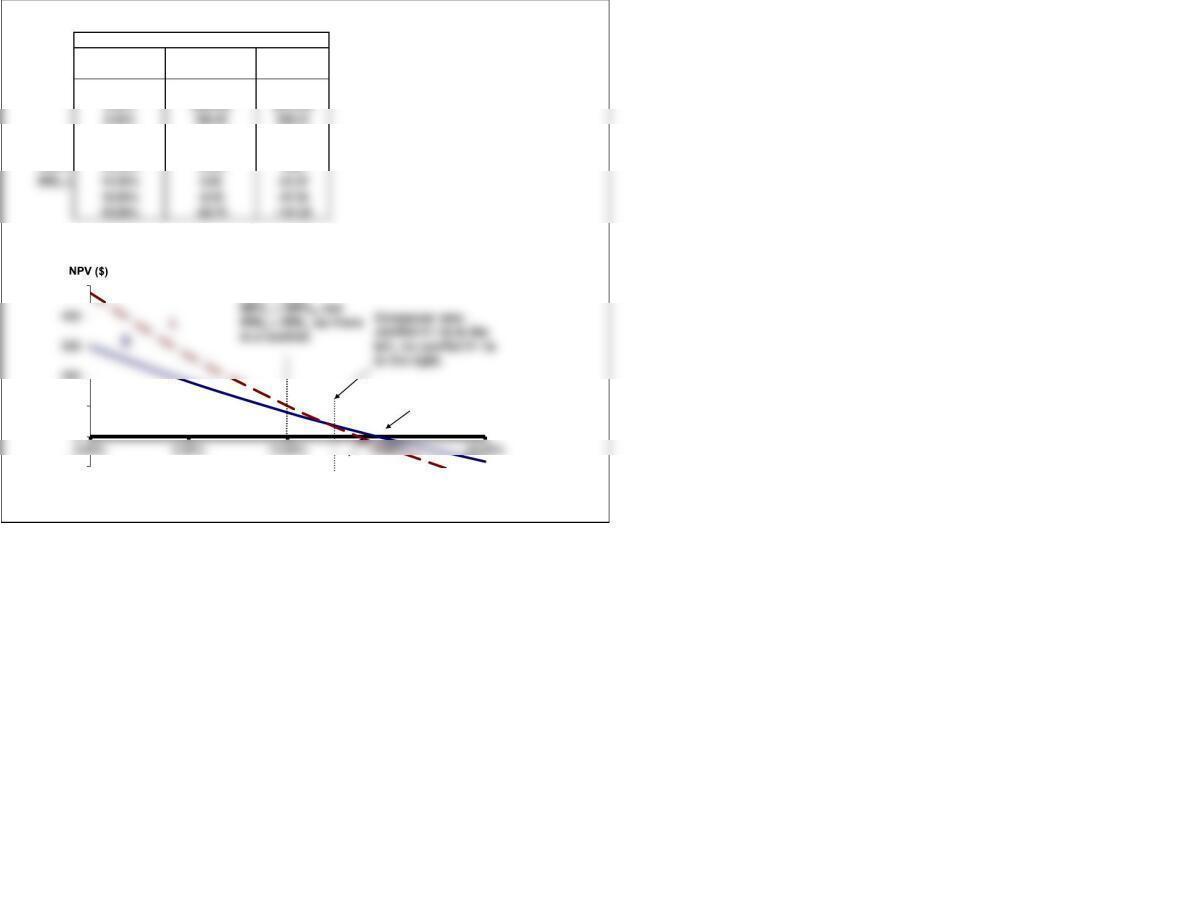

The NPV and IRR methods can provide conflicting results when used to evaluate mutually

exclusive projects. Therefore, it is important that you understand the IRR method and know

how it is related to the NPV. An NPV profile helps analyze the situation better.

An NPV profile is a graph that plots a project’s NPV against the discount rate. To create

an NPV profile, first we construct a data table that calculates NPVs at various costs of

capital. Notice, we have used increments of 5% and added Project S’s IRR.

at which the profiles cross (and the projects have the same NPV) is called the crossover

are used, but the IRR for each project and the crossover rate between the projects are used.

The crossover rate is calculated immediately below the figure, but for now assume it is

When comparing mutually exclusive projects whose cash flows differ with respect to size or

timing, conflicts arise between the NPV and IRR methods (as indicated by calculations

above). NPV profiles of two such projects would intersect at some point. The cost of capital

Data for the Graph:

* For a primer on making data

tables, refer to the Excel Tutorial.

100

300

At r = 10%,

IRR > r = 10%,

Figure 11.6 NPV Profiles for Projects S and L

Cost of

Capital

NPVS NPVL

$78.82 $100.40

10.00% 78.82 100.40

Crossover = 11.97% 42.84 42.84

IRRL = 13.55% 15.64 0.00

IRRS = 14.49% 0.00 -24.37

Data for the Graph:

-100

100

200

500

Cost of Capital (%)

IRRS

IRRL

At r = 10%,

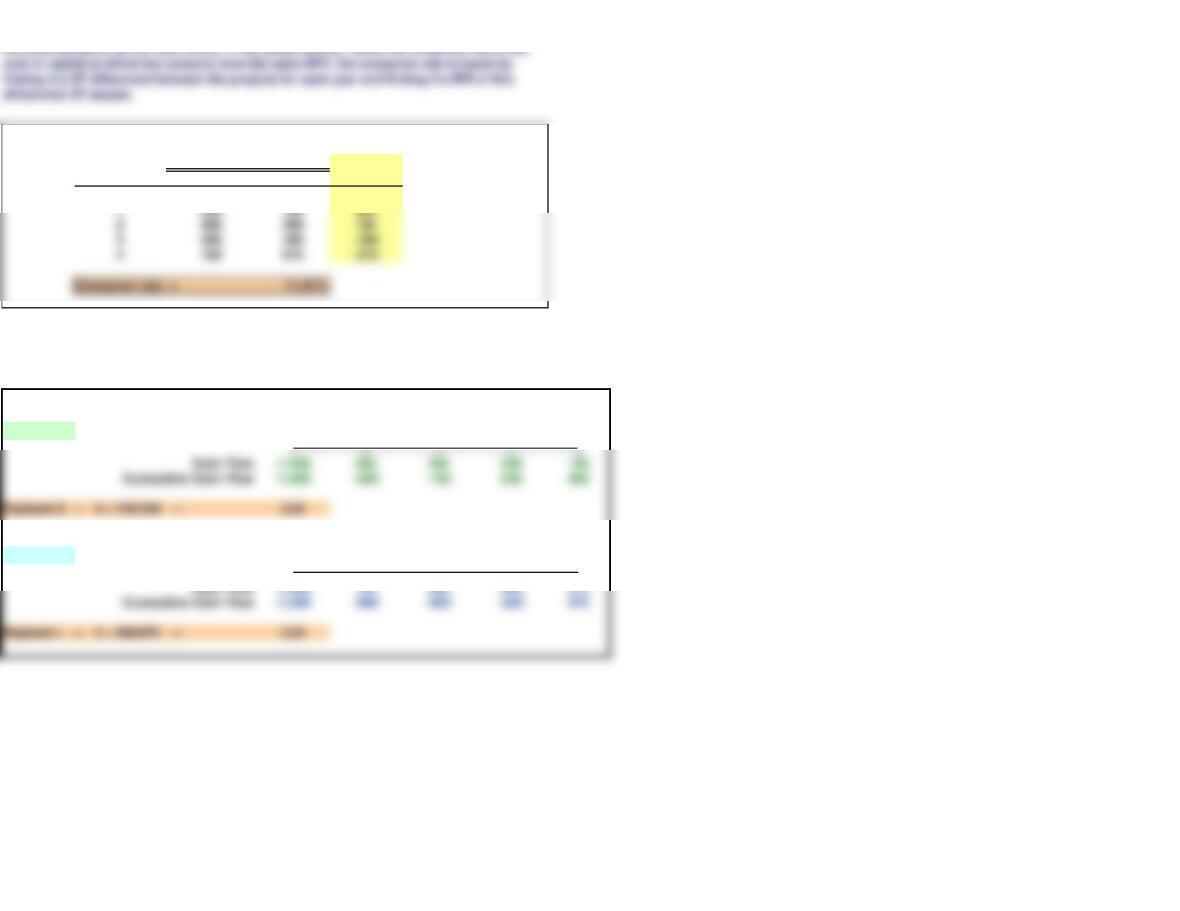

CALCULATING THE CROSSOVER RATE

Year (t) Project S Project L

0 -$1,000 -$1,000 $0

PAYBACK PERIOD (Section 11-8)

Figure 11.7 Payback Calculations

Project S Years 0 1 2 3 4

Project L Years 0 1 2 3 4

| | | | |

Expected After-Tax Net

Cash Flows, CFt

CF

Differential

The payback period is defined as the length of time required for an investment’s cash flows

to cover its costs.

The NPV and IRR methods can provide conflicting results when used to evaluate mutually

Figure 11.8 Discounted Payback Calculations at 10% Cost of Capital

WACC 10%

Project S Years 0 1 2 3 4

| | | | |

Cash Flow -1,000 500 400 300 100

Project L Years 0 1 2 3 4

| | | | |

Cash Flow -1,000 100 300 400 675

However, the payback period ignores cash flows occurring after the cost is recovered and it

ignores the time value of money. In an effort to alleviate the second concern, the discounted

payback was developed, which incorporates the present value of cash flows received.

SECTION 11-4 12/12/2018

SOLUTIONS TO SELF-TEST QUESTIONS

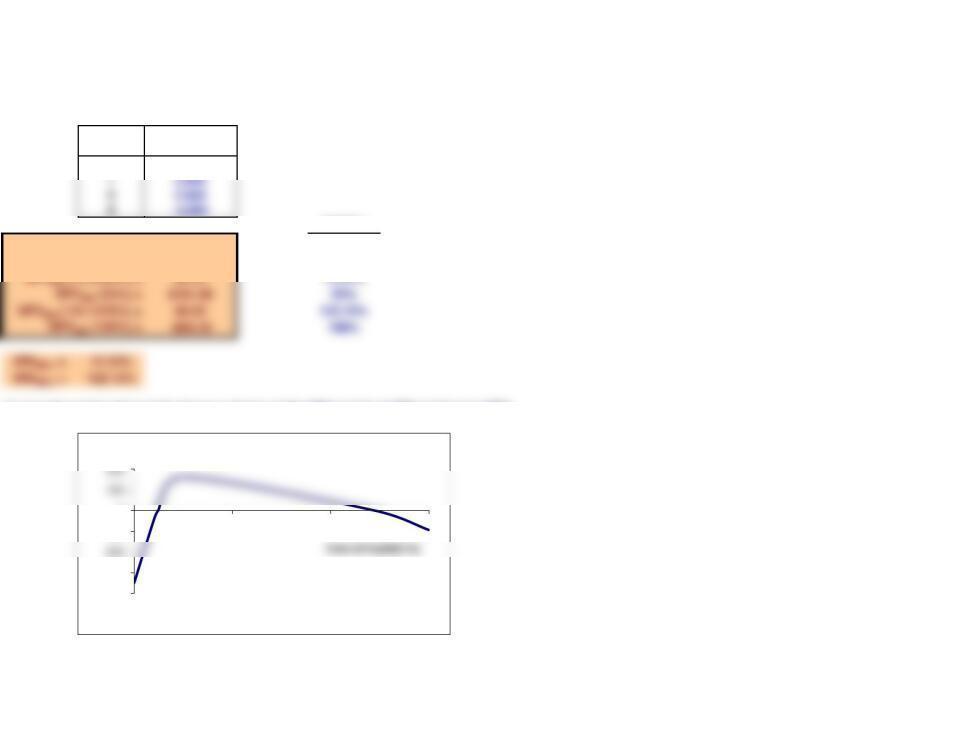

Project MM

Year (t) CFs

0-$1,000

WACCs

NPVMM (0%) = -$350.00 0%

NPVMM (10%) = -$45.83 10%

NPVMM (12.2258%) = $0.00 12.23%

NPVMM (25%) = $164.80 25%

2. Project MM has the cash flows shown below. Calculate MM’s NPV at discount rates of 0%,

10%,12.2258%, 25%, 122.1470%, and 150%. What are MM’s IRRs? If the cost of capital were

10%, should the project be accepted or rejected?

*** A quick scatter plot graph shows a sketch of the NPV profile of MM and its two IRRs.

-400

-300

-100

0

0% 50% 100% 150%

NPV ($)

Multiple IRRs: Project MM

SECTION 11-8 12/12/2018

SOLUTIONS TO SELF-TEST QUESTIONS

Regular payback

Years 0 1 2 3 4

Discounted payback

WACC 15%

Years 0 1 2 3 4

| | | | |

Cash Flow -1,000 300 300 300 1,000

3. Project P has a cost of $1,000 and cash flows of $300 per year for 3 years plus another

$1,000 in Year 4. The project’s cost of capital is 15%. What are P’s regular and discounted

paybacks? If the company requires a payback of 3 years or less, would the project be

accepted? Would this be a good accept/reject decision, considering the NPV and/or the IRR?

| | | | |

Cash Flow -1,000 300 300 300 1,000