288

Comprehensive/Spreadsheet Problem

Chapter 11: The Basics of Capital Budgeting

Calculate MIRRB at WACC = 10%:

Step 1: Calculate the NPV of the uneven cash flow stream, so its FV can then be calculated.

With a financial calculator, enter the cash flow stream into the cash flow registers,

then enter I/YR = 10, and solve for NPV = $36.55.

Enter N = 4, PV = -30, PMT = 0, and FV = 53.52 to solve for I/YR = 15.57%.

Payback B (cash flows in millions):

Annual

Period Cash Flows Cumulative

0 ($30) ($30)

Discounted Payback B (cash flows in millions):

Annual Discounted @10% Cumulative

Period Cash Flows Cash Flows Cash Flows

Summary:

Project A Project B

NPV $7.74 $6.55

Chapter 11: The Basics of Capital Budgeting

Comprehensive/Spreadsheet Problem

289

d. WACC NPVA NPVB

0% $20.00 $14.00

5 13.24 9.96

15

20

25

NPV

($)

Project A

Project B

e. At WACC = 5% and the two projects are mutually exclusive, NPVA > NPVB so choose Project

f. The crossover rate is the cost of capital at which the NPV profiles of two projects cross and,

g. It is not possible for conflicts between NPV and IRR when independent projects are being

290

Comprehensive/Spreadsheet Problem

Chapter 11: The Basics of Capital Budgeting

i. The cutoff chosen for both payback periods is arbitrary—but usually based on specific

j. The MIRR is the discount rate at which the present value of a project’s cost is equal to the

present value of its terminal value, where the terminal value is found as the sum of the

Chapter 11: The Basics of Capital Budgeting

Integrated Case

291

Integrated Case

11–24

Allied Components Company

Basics of Capital Budgeting

You recently went to work for Allied Components Company, a supplier of auto

repair parts used in the after-market with products from Daimler AG, Ford,

Toyota, and other automakers. Your boss, the chief financial officer (CFO), has

just handed you the estimated cash flows for two proposed projects. Project L

involves adding a new item to the firm’s ignition system line; it would take

Here are the projects’ after-tax cash flows (in thousands of dollars):

0 1 2 3

| | | |

Project L –100 10 60 80

Project S –100 70 50 20

Depreciation, salvage values, net operating working capital requirements, and

tax effects are all included in these cash flows. The CFO also made subjective

risk assessments of each project, and he concluded that both projects have

A. What is capital budgeting? Are there any similarities between a firm’s

capital budgeting decisions and an individual’s investment decisions?

292

Integrated Case

Chapter 11: The Basics of Capital Budgeting

Answer: [Show S11–1 through S11-3 here.] Capital budgeting is the process

of analyzing additions to fixed assets. Capital budgeting is important

because, more than anything else, fixed asset investment decisions

chart a company’s course for the future. Conceptually, the capital

B. What is the difference between independent and mutually exclusive

projects? Between projects with normal and nonnormal cash flows?

Answer: [Show S11–4 and S11-5 here.] Projects are independent if the cash

flows of one are not affected by the acceptance of the other.

Chapter 11: The Basics of Capital Budgeting

Integrated Case

293

C. (1) Define the term net present value (NPV). What is each project’s NPV?

Answer: [Show S11-6 through S11–10 here.] The net present value (NPV) is

simply the sum of the present values of a project’s cash flows:

294

Integrated Case

Chapter 11: The Basics of Capital Budgeting

C. (2) What is the rationale behind the NPV method? According to NPV,

which project(s) should be accepted if they are independent?

Mutually exclusive?

Answer: [Show S11-11 here.] The rationale behind the NPV method is

straightforward: If a project has NPV = $0, then the project

generates exactly enough cash flows (1) to recover the cost of the

Chapter 11: The Basics of Capital Budgeting

Integrated Case

295

C. (3) Would the NPVs change if the WACC changed? Explain.

Answer: The NPV of a project is dependent on the WACC used. Thus, if the

D. (1) Define the term internal rate of return (IRR). What is each project’s

IRR?

Answer: [Show S11-12 here.] The internal rate of return (IRR) is that

discount rate which forces the NPV of a project to equal zero:

0 1 2 3

| | | |

CF0 CF1 CF2 CF3

PVCF1

296

Integrated Case

Chapter 11: The Basics of Capital Budgeting

D. (2) How is the IRR on a project related to the YTM on a bond?

Answer: [Show S11-13 here.] The IRR is to a capital project what the YTM

D. (3) What is the logic behind the IRR method? According to IRR, which

project(s) should be accepted if they are independent? Mutually

exclusive?

Answer: [Show S11–14 here.] IRR measures a project’s profitability in the

rate of return sense: If a project’s IRR equals its cost of capital, then

Chapter 11: The Basics of Capital Budgeting

Integrated Case

297

D. (4) Would the projects’ IRRs change if the WACC changed?

Answer: IRRs are independent of the WACC. Therefore, neither IRRS nor

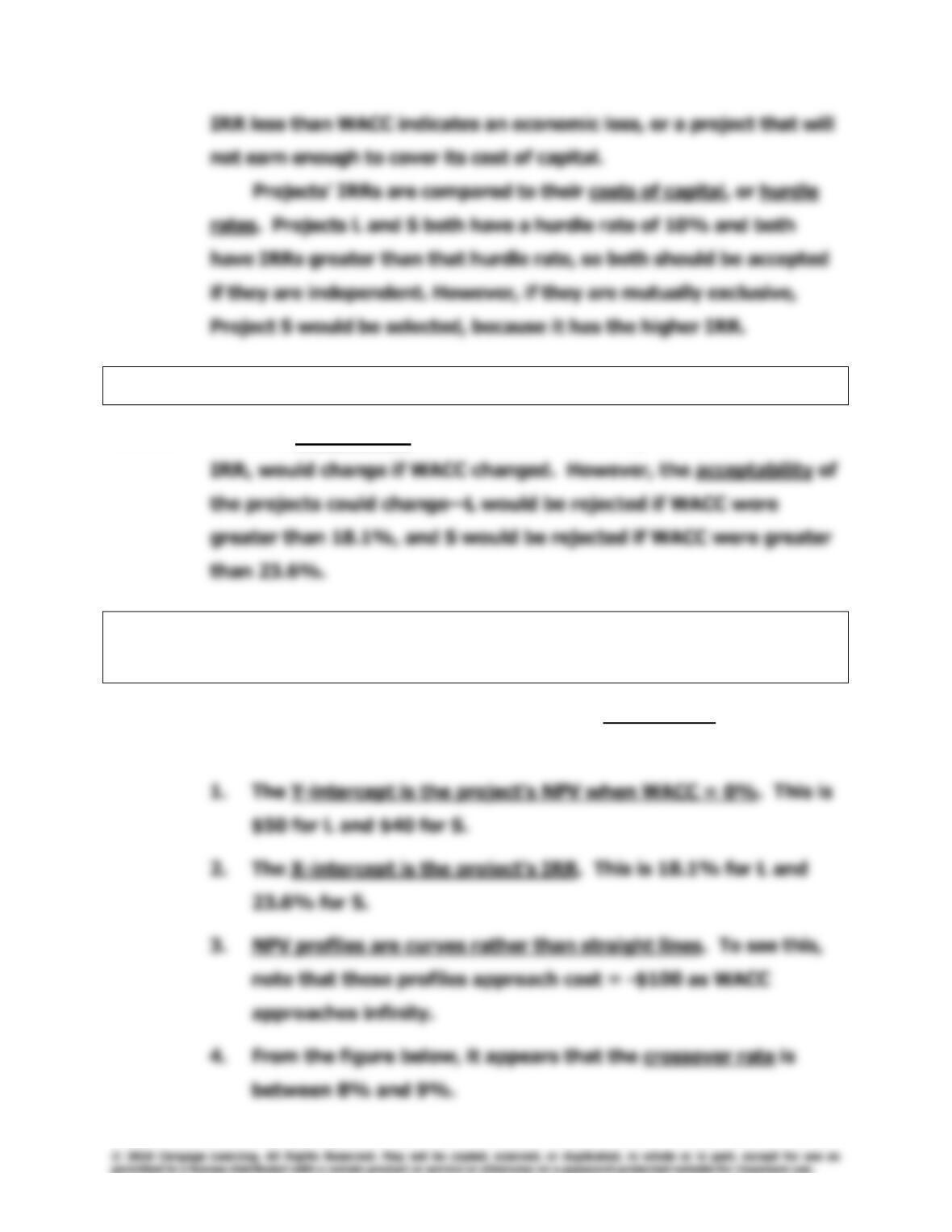

E. (1) Draw NPV profiles for Projects L and S. At what discount rate do

the profiles cross?

Answer: [Show S11-15 through S11-18 here.] The NPV profiles are plotted

in the figure below. Note the following points:

298

Integrated Case

Chapter 11: The Basics of Capital Budgeting

NPV

($)

40

50

Crossover Rate 9%

Project L

NPV

($)

40

50

Crossover Rate 9%

Project L

NPV

($)

40

50

Crossover Rate 9%

Project L

E. (2) Look at your NPV profile graph without referring to the actual NPVs

and IRRs. Which project(s) should be accepted if they are

independent? Mutually exclusive? Explain. Are your answers

correct at any WACC less than 23.6%?

Answer: The NPV profiles show that the IRR and NPV criteria lead to the

Chapter 11: The Basics of Capital Budgeting

Integrated Case

299

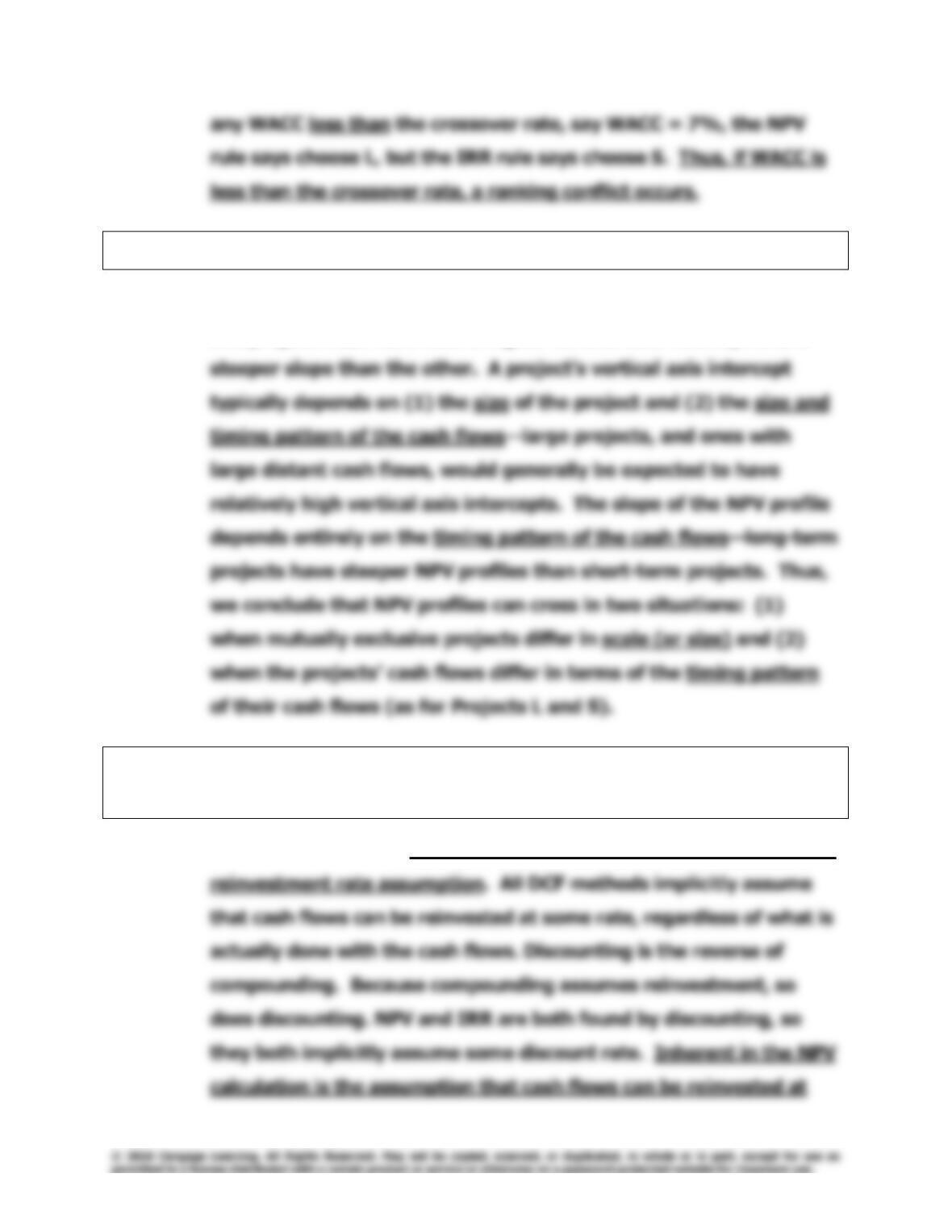

F. (1) What is the underlying cause of ranking conflicts between NPV and IRR?

Answer: [Show S11-19 here.] For normal projects’ NPV profiles to cross,

one project must have both a higher vertical axis intercept and a

F. (2) What is the reinvestment rate assumption, and how does it affect

the NPV versus IRR conflict?

Answer: [Show S11–20 here.] The underlying cause of ranking conflicts is the

300

Integrated Case

Chapter 11: The Basics of Capital Budgeting

F. (3) Which method is the best? Why?

Answer: Whether NPV or IRR gives better rankings depends on which has

the better reinvestment rate assumption. Normally, the NPV’s

G. (1) Define the term modified IRR (MIRR). Find the MIRRs for Projects L

and S.

Answer: [Show S11–21 and S11-22 here.] MIRR is that discount rate which

Chapter 11: The Basics of Capital Budgeting

Integrated Case

301

G. (2) What are the MIRR’s advantages and disadvantages as compared to

the NPV?

Answer: [Show S11-23 here.] MIRR does not always lead to the same

decision as NPV when mutually exclusive projects are being

considered. In particular, small projects often have a higher MIRR,

302

Integrated Case

Chapter 11: The Basics of Capital Budgeting

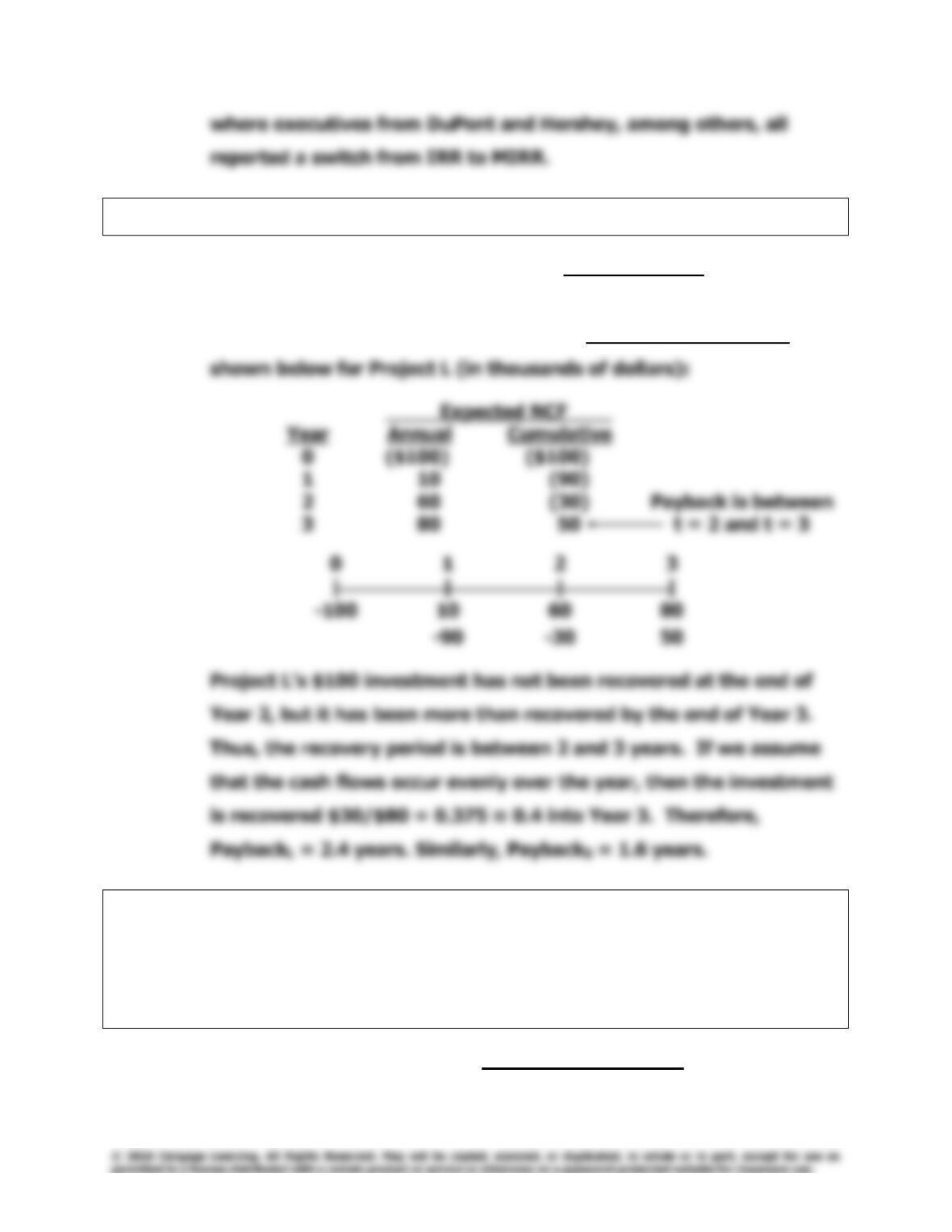

H. (1) What is the payback period? Find the paybacks for Projects L and S.

Answer: [Show S11-24 and S11–25 here.] The payback period is the

expected number of years required to recover a project’s cost. We

calculate the payback by developing the cumulative cash flows as

H. (2) What is the rationale for the payback method? According to the

payback criterion, which project(s) should be accepted if the firm’s

maximum acceptable payback is 2 years, if Projects L and S are

independent? If Projects L and S are mutually exclusive?

Answer: Payback represents a type of “break–even” analysis: The payback

period tells us when the project will break even in a cash flow

Chapter 11: The Basics of Capital Budgeting

Integrated Case

303

H. (3) What is the difference between the regular and discounted payback

methods?

Optional Question

What is Project L’s discounted payback, assuming a 10% cost of capital?

Answer: Expected Net Cash Flows

Year Raw Discounted Cumulative

0 ($100) ($100.00) $100.00)

1 10 9.09 (90.91)

2 60 49.59 (41.32)

3 80 60.11 18.79

Discounted paybackL = 2 + ($41.32/$60.11) = 2.69 = 2.7 years.

Versus 2.4 years for the regular payback.

H. (4) What are the two main disadvantages of discounted payback? Is the

payback method useful in capital budgeting decisions? Explain.

Answer: [Show S11-27 here.] Regular payback has three critical

304

Integrated Case

Chapter 11: The Basics of Capital Budgeting

I. As a separate project (Project P), the firm is considering sponsoring

a pavilion at the upcoming World’s Fair. The pavilion would cost

$800,000, and it is expected to result in $5 million of incremental

cash inflows during its 1 year of operation. However, it would then

take another year, and $5 million of costs, to demolish the site and

return it to its original condition. Thus, Project P’s expected cash

flows (in millions of dollars) look like this:

0 1 2

| | |

-0.8 5.0 -5.0

The project is estimated to be of average risk, so its WACC is 10%.

I. (1) What is Project P’s NPV? What is its IRR? Its MIRR?

Answer: [Show S11-28 here.] Here is the time line for the cash flows, and

the NPV:

Chapter 11: The Basics of Capital Budgeting

Integrated Case

305

I. (2) Draw Project P’s NPV profile. Does Project P have normal or

nonnormal cash flows? Should this project be accepted? Explain.

Answer: [Show S11-29 through S11–31 here.] You could put the cash flows

in your calculator and then enter a series of I/YR values, get an

NPV for each, and then plot the points to construct the NPV profile.

1 Looking at the figure on the next page, if you guess an IRR to the left of the peak NPV rate,

the lower IRR will appear. If you guess IRR > peak NPV rate, the higher IRR will appear.

306

Integrated Case

Chapter 11: The Basics of Capital Budgeting